– Two words: policy divergence (read on to find out more).

But first, let’s take a look at just how dismal the Yen’s performance has been so far in 2022.

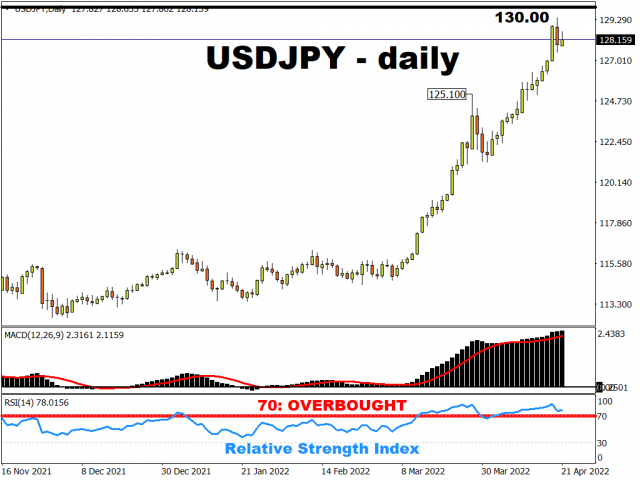

The Japanese Yen is now trading around a 20-year low against the US dollar.

Last Tuesday, USDJPY posted its biggest single-day climb since November 2020, only to then take a breather for the time being.

(Note: weaker Yen versus the US dollar = USDJPY climbs higher).

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

FUN FACT: The last time USDJPY traded at these levels just below 130, Eminem had just released his hit 2002 track, “Without Me”.

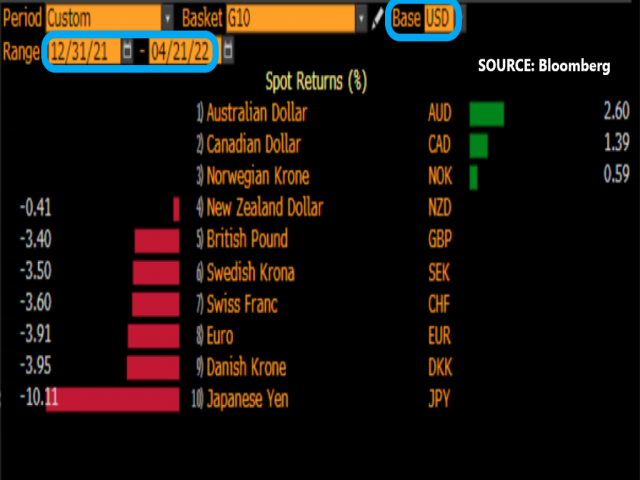

In fact, JPY is the worst performer against the US dollar amongst all G10 currencies … by far.

And the Yen’s woes aren’t just limited to its performance against the US dollar alone.

Consider how the JPY Index has weakened by almost 9% so far this year.

Note that the index shown above comprises a basket of currency pairs measuring the Yen against its G10 peers, all in equal weights:

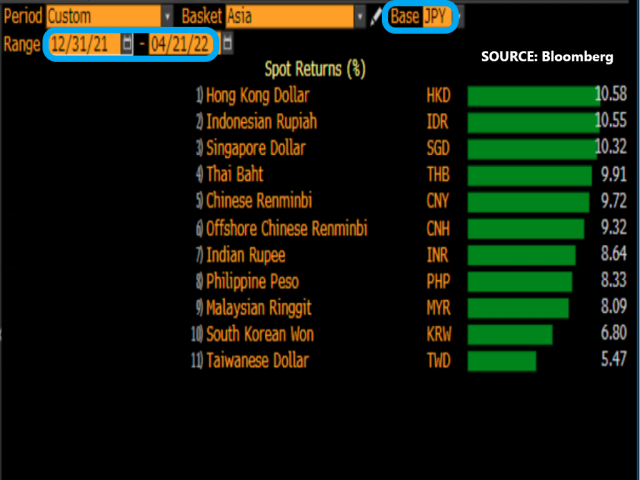

The Yen also has a year-to-date decline against all its major Asian counterparts as well.

So why is the Yen so weak?

The main reason is because of monetary policy divergence.

Let’s break it down.

Firstly, monetary policy is the way a central bank achieves its goals for the economy (e.g. maximum employment, stable prices, etc.), using tools like interest rates, money supply, and even currency levels.

And where’s the divergence?

The Bank of Japan is still using its monetary policy to support its economy.

This is in stark contrast to what most other central banks around the world are doing = pulling back that support. They do this by raising interest rates/easing back on bond purchases.

The goal of such policy-tightening (not what the BOJ is doing) is to reduce money supply and demand levels in an economy = less money chasing after scarce goods = to lower consumer prices/inflation.

Monetary policy: Comfort food vs. a regular diet

Consider when a child is feeling down, his/her parents may have no qualms treating the child to some ice cream, candy, or chocolate bars.

Such sweet indulgences are meant to make the child feel better in a jiffy, but is (hopefully) just a short-term fix and also (again, hopefully) far different from the regular diet the child consumes as part of the daily routine.

Similarly, when the economy was suffering during the pandemic, central banks rolled out record-low interest rates and printed money out of thin air to keep financial markets supported.

Low interest rates = cheaper for households/businesses to borrow money = they have money to spend in the economy = the economy gets better

But now that economies are recovering and even posting red-hot inflation numbers, they no longer need record-low interest rates and unlimited bond purchases

Hence, central banks are returning to their economy’s “regular diet” by tightening policy = paring down bond purchases/reducing the supply of money in the economy/raising interest rates.

Who’s already hiking rates?

Within the G10 space alone:

- Bank of New Zealand – raised its benchmark rate by 125 basis points (1.25%) since Q3 2021

- Bank of Canada – raised its benchmark rate by 75 basis points so far this year

- Bank of England – raised its benchmark rate by 65 basis points since December

- US Federal Reserve – raised rates by 25 basis points in March, perhaps another 50-basis point hike in May

But not so the Bank of Japan.

It’s keeping Japan’s benchmark interest rate at a record low of negative 0.1%, while buying up even more bonds.

Hence, the divergence in monetary policy.

How is policy divergence playing out in markets?

This divergence is evident in the widening gap in yields between Japanese bonds and its global counterparts.

Firstly, what are yields?

Yields are a way to measure how much money you could earn on an investment over a set period of time.

In the case for bonds, it’s calculated in terms of how much interest one would get paid if they held on to that bond till it matures/reaches the end of its tenure.

For context, bond yields have been climbing around the world.

This is because investors are selling off bonds in tandem with central banks that are reducing their balance sheets.

And when bond prices drop, their yields rise.

Here are the benchmark 10-year yields for these other countries (at the time of writing):

- US = 2.88%

- Canada = 2.87%

- China = 2.82%

- UK = 1.95%

- Germany = 0.89%

Contrast the numbers above with Japan’s 10-year yields, which are capped at 0.25%.

As a policy, the Bank of Japan is buying even more bonds to keep bond prices elevated and limit its benchmark 10-year yields to no higher than 0.25% (this process is also known as “yield curve control”).

The goal for capping those yields is to keep borrowing costs low in Japan so that households/businesses can still borrow to stimulate the economy.

Government bond yields are often used as the benchmark by which other banks/financial institutions calculate the interest to charge the customers who borrow money.Here are two charts that show how the widening gap/spread between US benchmark yields vs. Japan’s benchmark yields (10-year government bonds) correspond with the USDJPY’s performance:

See how those two lines are moving in sync with one another?

In essence, the wider the gap between US and Japan’s yields, the higher USDJPY goes (the weaker the Japanese Yen against the US dollar).

How are Japan’s capped yields affecting the yen?

The lower yields on offer in Japan suggests that investors would get more bang for their buck by buying bonds in other countries that are now posting higher yields (again, yields in this case are a measure of how much one could earn from investing in that particular bond).

At risk of oversimplifying matters:

- Less demand for Japanese assets = less demand for the Japanese yen.

- And when there’s lower demand = prices fall (all else equal).

Hence, the Yen has been falling as investors shun Japanese bonds.

From a fundamental perspective, markets are getting the sense that the Japanese economy is still too fragile – or at least the Bank of Japan thinks so of its own economy – and is nowhere near strong enough to be able to do without the ‘comfort food’ from the central bank.

But of course all that could change, as the BOJ faces increasing pressure to follow suit with other central banks in tightening policy … or perhaps even just to stem the Yen’s weakness.

Which brings us to this final point …

Will the Yen eventually rebound?

As a market cliche goes … nothing lasts forever.

So yes, theoretically the Yen could eventually rebound.

But one of two things may need to happen first:

1) The Bank of Japan has to signal that its willing to abandon its ultra-loose monetary policies.

Policymakers need to be convicted that Japan’s economic recovery is sustainable, and that inflation is being fuelled by robust demand (a.k.a. demand-pull inflation) as opposed to cost-push inflation.

To be clear, this seems unlikely for a while more, at least through the end of 2022.

Still, look out for the Bank of Japan policy meeting next week (April 28th).

The slightest clue that the BOJ is ready to tweak its policy stance could trigger a big move in the Yen.

2) Policymakers intervene to curb Yen weakness

This has been done before, but not for quite some time.

The last time the Japanse government propped up the yen was back in 1998, when USDJPY traded above 140 and peaked at 147.66 in September 1998.

However, back in 2002 even when USDJPY surpassed 135, the government sat on its hands and didn’t intervene.

So it remains to be seen at what level Japanese policymakers will tolerate before trying to stop the Yen from weakening further.

Keep in mind that a drastically-weaker Yen causes its own problems for the economy.

Japan is a net importer of energy, which are widely denominated in US dollars. The weaker Yen forces Japan to spend more of its currency to buy the same amount of fuel, not to mention the other imported goods (e.g. food) and services that it now has to spend more money on. If the imported costs become too great and weigh on businesses/households, then the Japanese government may be forced to pay for subsidies to ease the pain. That’s money out of the Japanese government’s pocket that could be spent on other things.

So until either of the above scenarios happen, shorting the Yen has remained a popular bet.

Last week, asset managers raised their short bets on the Yen to the most ever on record, according to CFTC data.

Overall, as long as this policy and yields divergence continues to play out between Japan and other major economies, that’s likely to keep the Yen on its weakening path for longer.

That is, unless the BOJ or Japan’s Finance Ministry switches tact and, in intervening to halt the Yen’s weakness, might do so while dropping bars from Eminem’s monster hit from 2002 …

“Now this looks like a job for me

So everybody, just follow me

‘Cause we need a little, controversy

‘Cause it feels so empty, without me”

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- The Central Bank of Mexico kept its interest rate unchanged. Iran plans to introduce strict bans for US and Israeli vessels in the Strait of Hormuz Aug 7, 2026

- USD/JPY Holds Firm: Yen Loses Some Support Aug 7, 2026

- Australian trade balance returned to positive territory Aug 6, 2026

- Results in Line for Most Reporting Companies Aug 5, 2026

- Stock indices continue to break records. Oil is falling amid intensified diplomatic dialogue between the US and Iran Aug 5, 2026

- USD/JPY Holds Steady After Intervention: Outlook Remains Uncertain Aug 5, 2026

- EUR/USD: Busy Week Ahead Aug 3, 2026

- Positive sentiment in the AI sector supported stock indices. Oil prices remain volatile Aug 3, 2026

- The Tech‑heavy NASDAQ Index jumped by more than 3.3%. The offshore yuan is trading at its highest level since 2023 Jul 31, 2026

- USD/JPY After Volatility: Multiple Events in One Day Jul 31, 2026