Here are the key economic events and data releases to look out for this week:

Monday, January 17

- CNH: China 4Q GDP, December industrial production and retail sales

- US markets closed for Martin Luther King Jr. holiday

Tuesday, January 18

- JPY: Bank of Japan decision

- EUR: Germany ZEW survey expectations

- GBP: UK November jobless claims, December unemployment

- Goldman Sachs Q4 earnings

Wednesday, January 19

- EUR: Germany December inflation

- GBP: UK December inflation

- GBP: Bank of England Governor Andrew Bailey speech

- Bank of America Q4 earnings

- Morgan Stanley Q4 earnings

Thursday, January 20

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

- CNY: PBOC loan prime rate decision

- JPY: Japan December external trade

- AUD: Australia December unemployment

- EUR: European Central Bank publishes Dec meeting account

- USD: US weekly initial jobless claims

- US crude oil: EIA inventory report

- Netflix Q4 earnings

Friday, January 21

- JPY: Japan December inflation

- GBP: BOE policy maker Catherine Mann speech, UK December retail sales

- EUR: Eurozone January consumer confidence

The potential for the removal of the liquidity punchbowl (aka monetary policy tightening) is dominating the market’s thinking at present.

The strong US CPI report released last week added more pressure on the US Federal Reserve to stat lifting rates earlier than once thought, potentially as soon as March. We’ve had numerous FOMC members recently marking a more hawkish bias to the committee’s views, including notably, the fabled dove Brainard in her Fed chair nomination appearance before the Senate.

Another Fed official, Waller, also mentioned the chance of five rates hikes this year, although he doesn’t favour a 50bp hike in March. It’s worth remembering that it is a US holiday on Monday, so their markets are closed, and the blackout period has started before the next Fed meeting on 26 January so there won’t be any more Committee members to listen out for on the wires.

Company earnings also continue with more bulge bracket US banks releasing their fourth quarter results. US stocks notched their second straight weekly decline, pushed lower by disappointing earnings from financial industry bellwether JPMorgan Chase which has clouded an already mixed outlook for the US economy.

Asian policymakers in focus

We kick off the week with Chinese fourth quarter GDP (4% y/y vs. 3.3% est.), as well as December’s industrial production (4.3% vs. 3.7% est.) and retail sales (1.7% vs. 3.8% est.). The full-year GDP came in at 8.1%, slightly above the median estimate by economists but well above the government’s 2021 target of over 6%. Still, the data confirmed that the final quarter was losing momentum but the real test for the domestic economy will come in the first quarter of this year, due to current regional lockdowns on top of the ongoing woes in the property sector.

With this in mind, the PBoC lowered both the one-year medium-term lending facility rate abd the seven-day reverse repurchase rate by 10 basis points respectively, a move not seen in nearly two years, and also injected more liquidity into the financial system via US$110 billion in loans.

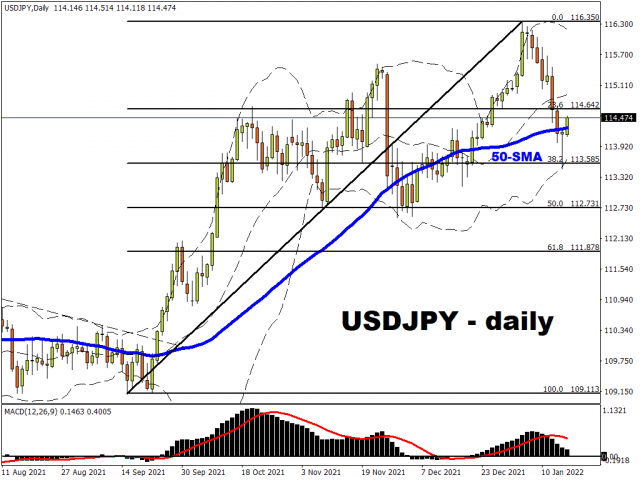

The Bank of Japan meeting on Tuesday is also getting some airtime after “sources” said it is thinking of a rate hike at some point beyond this year and debating how to manage the messaging. Inflation is picking up and possibly risks to prices may now be described as “balanced” but hitting the 2% inflation target is still a long way off.

UK data to add pressure to the BoE

We get the usual mid-month data dump in the UK with signals about labour market strength, the pace of consumer price inflation and retail sales. These are the last official updates before the BoE meeting on 3 February, with CPI expected to rise above the forecast 5% going forward and a labour marker remaining tight.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- The US introduces new import tariffs for 60 countries. Brent crude surpasses $100 per barrel Jul 24, 2026

- USD/JPY Breaks Records: Nothing Slows the Yen’s Decline Jul 24, 2026

- Oil prices reached a 6‑week high. The AUD strengthened on the back of a strong labor‑market report Jul 23, 2026

- EUR/USD Recovers as Dollar Weakens Jul 23, 2026

- Bitcoin rose to $66,000. The New Zealand dollar continues to strengthen Jul 22, 2026

- Inflationary pressure is easing in Canada. In New Zealand, on the contrary, inflation is rising Jul 21, 2026

- GBP/USD Falls After Cabinet Changes Jul 21, 2026

- Geopolitical and macroeconomic conditions continue to pressure market sentiment Jul 20, 2026

- USD/JPY Poised to Continue Gains as Expensive Oil and Lack of Support Weigh on Yen Jul 20, 2026

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026