Asian markets are in the green this morning, following the swing higher in both European and US shares yesterday which rose sharply between 1.5% and 3%. Despite some less positive news around another Chinese property developer, risk sentiment remains fairly optimistic. The dollar is stuck on the side lines at present, as more risk-sensitive commodity currencies claw back losses and safe havens get offered. Next week’s FOMC meeting is a clear risk event for the greenback, with downside against the euro and yen expected to be limited.

Glass half full approach

Investors are holding on to anecdotal evidence above Omicron’s limited impact on public health and therefore the wider economy.

High cash levels are being put to work and investors are chasing riskier assets.

But real concerns still remain about the new variant as new lab data showed that the protection from the Pfizer vaccine is likely reduced 20-40-fold. There are many question marks about if Omicron is better able to evade vaccine and infection-induced immunity, though markets appear to be focusing on the micro, individual risk rather than the wider, macro threat to society. If more people get infected, there is a higher risk that more people on an absolute level may still get admitted to hospital. It’s probably best to leave this to the scientists and medical professions!

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Bank of Canada meeting in focus

With fears easing over the new variant, traders are keeping one eye on calendar risk events. The Bank of Canada meeting later today should see rates kept unchanged at 0.25%. But the focus will be on the bank’s assessment of the current risks around the Omicron variant. Policymakers are appearing to have different takes on the impact on economies. The upbeat messages from the Fed and yesterday’s RBA meeting contrasts with recent BoE comments which were more cautious.

Having announced the end of QE at its last meeting, the booming labour market and GDP, sky-high inflation and a thriving housing market in Canada would normally see a hawkish response from BoC policymakers.

The market is pricing in around five rate hikes next year, with some economist seeing the first move in January. A more cautious stance by Governor Macklem, with economic forecasts not due until the new year, would upset this outlook and see selling in CAD.

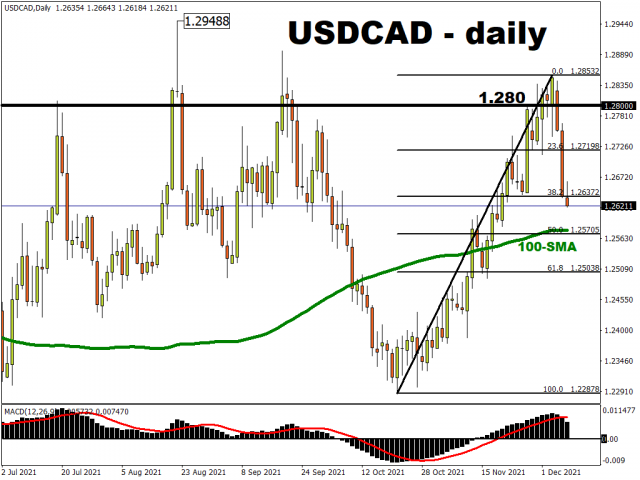

Loonie enjoying risk and oil rally

Commodity currencies have recovered some of their recent losses this week on the rebound in risk and oil prices. USD/CAD had been in a bull channel after six solid weeks of gains. But the last few sessions have seen a sharp reversal with summertime resistance above 1.28 again doing a job. The 50% retracement of the October/December dollar rise will offer support at 1.2570. The 100-day SMA sits just above here. Resistance is in the high 1.27s and the barrier around 1.28.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- The Central Bank of Mexico kept its interest rate unchanged. Iran plans to introduce strict bans for US and Israeli vessels in the Strait of Hormuz Aug 7, 2026

- USD/JPY Holds Firm: Yen Loses Some Support Aug 7, 2026

- Australian trade balance returned to positive territory Aug 6, 2026

- Results in Line for Most Reporting Companies Aug 5, 2026

- Stock indices continue to break records. Oil is falling amid intensified diplomatic dialogue between the US and Iran Aug 5, 2026

- USD/JPY Holds Steady After Intervention: Outlook Remains Uncertain Aug 5, 2026

- EUR/USD: Busy Week Ahead Aug 3, 2026

- Positive sentiment in the AI sector supported stock indices. Oil prices remain volatile Aug 3, 2026

- The Tech‑heavy NASDAQ Index jumped by more than 3.3%. The offshore yuan is trading at its highest level since 2023 Jul 31, 2026

- USD/JPY After Volatility: Multiple Events in One Day Jul 31, 2026