Market narratives are everywhere at present with competing cross currents hitting traders from all sides. The global energy crisis, supply chain disruptions and the China Evergrande story roll on with central banks perhaps the main actors among all of this. How will they respond and which currencies and markets will be affected the most? The dollar looks well set, buoyed by energy independence and tighter Fed policy soon. Other energy exporting currencies with similarly hawkish polciymakers also look good.

Data points beaten by higher bond yields

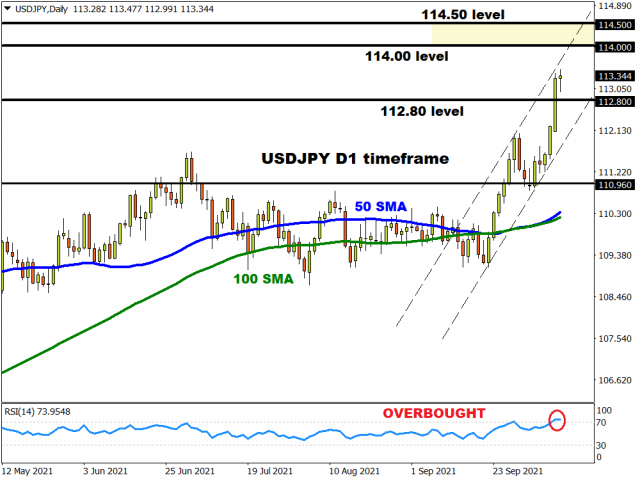

Many seasoned traders say that the bond market leads all other markets. In that sense, the breakout in yields to new cycle highs tells us that the November Fed taper is a done deal. More than that, we saw yen capitulation at a time when there is still some uncertainty over the growth and risk outlook, which would ordinarily lead investors to seek safe havens.

Ahead of the US CPI and Fed minutes tomorrow, USD/JPY broke to new cycle highs yesterday and the highest level since December 2018 on the back of rising bond yields. The move looks decisive (on the weekly chart especially) with the next area of resistance around 114-114.50 The latter zone served as resistance on numerous occasions back in 2017 and 2018. The major is overbought on the daily RSI which means we should expect a pullback in some fashion soon. Support sits around 112.80.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Solid UK Jobs Data keeps alive BoE rate hike expectations

Money markets went into overdrive yesterday, and none more so than the sterling market. A 25 basis point hike by the Bank of England is now fully priced in for December this year, with some 8 basis points for next month. Notably, this morning’s UK employment figures did not spike higher as many feared, despite the end of the furlough scheme. And August average wage growth came in on the high side.

This means there is not much to push back on this fairly aggressive rate hike pricing. The high inflation story contrasts with multiple economic tailwinds (fuel, energy and food shortages, Brexit) that are expected to hit the UK in the coming months. The rise in GBP/USD stalled yesterday at 1.3673 and we are back into the range trading around 1.36. The July low at 1.3571 offers the next line of support while the 50-day moving average looms above at 1.3725.

US Q3 Earnings Season is upon us

We also have the small matter of the third quarter earnings season to digest too! In the current landscape of elevated equity valuations and record high profit margins, it may pay to be on our guard for a bout of upcoming profit warnings. These results will be all about increasing input costs and how they are driving margin pressures. We might also see more evidence of how physical and digital companies’ performance is diverging.

Banks are first up with results this week form JP Morgan Chase giving us a good handle of the broader (investment) banking environment, while Bank of America will show us a picture of domestic loan demand. Key will be talk on inflation and the outlook for interest rates, and how customers are being impacted.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026

- Oil prices jumped 4% amid a new wave of escalation between the US and Iran Jul 13, 2026

- EUR/USD: US Inflation Will Determine Everything Jul 13, 2026