The European Central Bank has a policy meeting this Thursday, with the euro poised to react to the central bank’s commentary about when it could start winding down its emergency asset purchases. Traders and investors will also be raring to know what Fed officials make of the disappointing August nonfarm payrolls report released last Friday, and whether it could disrupt the Fed’s tapering plans.

Tapering remains a key theme for markets in the coming week filled with these major economic events:

Monday, September 6

- EUR: Germany July factory orders

- US markets closed

- US President Joe Biden to renominate Jerome Powell as Fed Chair this week?

Tuesday, September 7

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

- CNH: China August trade

- AUD: Reserve Bank of Australia policy decision

- EUR: Germany July industrial production and September ZEW survey expectations

- EUR: Eurozone 2Q GDP (final print)

Wednesday, September 8

- CAD: Bank of Canada rate decision

- USD: US July JOLTS job openings

- USD: Fed Beige book

- USD: Fed Speak – Dallas Fed President Robert Kaplan, New York Fed President John Williams

Thursday, September 9

- CNH: China August CPI and PPI

- EUR: Germany July trade

- EUR: European Central Bank rate decision

- USD: US weekly initial jobless claims

- EIA crude oil inventory report

Friday, September 10

- EUR: Germany August CPI (final print)

- GBP: UK July monthly GDP and trade

- CAD: Canada August unemployment

- USD: US August PPI

Will the ECB inch towards tapering?

All eyes will be on ECB President Christine Lagarde, a notable dove, and whether she might warm up to the hawkish tones emanating from within the Governing Council. If so, then the euro could climb higher, noting that the shared currency still holds year-to-date declines against most of its G10 peers.

With the worst of the pandemic now behind the Eurozone economy, the ECB may have to start thinking about reining in its emergency asset purchases, or at least start talking about it as many major central banks have started doing, including the Fed. After all, Eurozone inflation hit 3% in August, its highest in a decade and above the ECB’s 2% target.

However, some ECB officials are still preaching caution, while European Union economy commissioner Paolo Gentiloni just this past weekend warned against a premature tightening of policy, which he labelled would be a “big mistake”. He reiterated the thought that inflationary surges of late would be a “temporary phenomenon”, a similar sentiment expressed across the Atlantic as well.

EURUSD to reflect ECB vs. Fed tapering expectations

Besides pitting the doves against the hawks within the ECB, traders and investors are also comparing the ECB against the Fed in their respective journeys towards tapering.

Recall that as recently as 27 August, Fed Chair Jerome Powell had stated that he was open to throwing his weight behind starting to rein in the US central bank’s own purchases before the end of this year. But those comments came before last Friday’s shockingly low nonfarm payrolls print (235k vs. expected 733k).

The hiring downshift in the US labour market could complicate the Fed’s tapering timeline.

Euro traders will similarly be monitoring the data out of Germany, the EU’s largest economy, over the coming days to see if the ECB might also be given reasons to hold up on the thought of tapering. Note that recent confidence readings for German businesses and consumers came in lower than expected due to disruptions from the Delta variant.

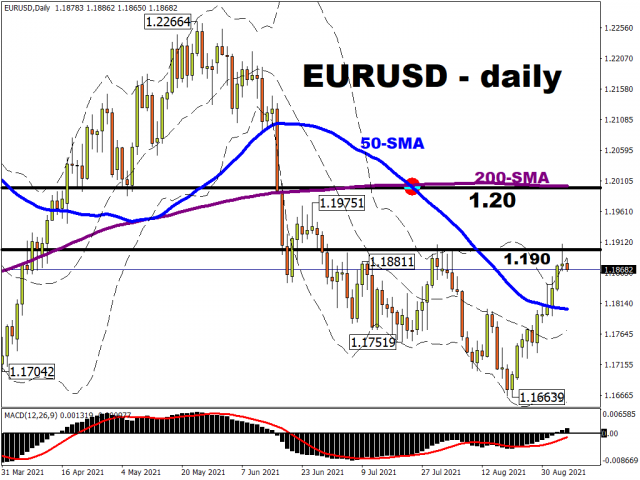

Still, if the ECB is seen to be moving closer to normalizing its policy settings, at a time when the Fed is forced to pause, that could help EURUSD break sustainably above the psychological 1.19 mark, with bulls then potentially eyeing next the late-June high of around 1.1975 as the next resistance level of interest.

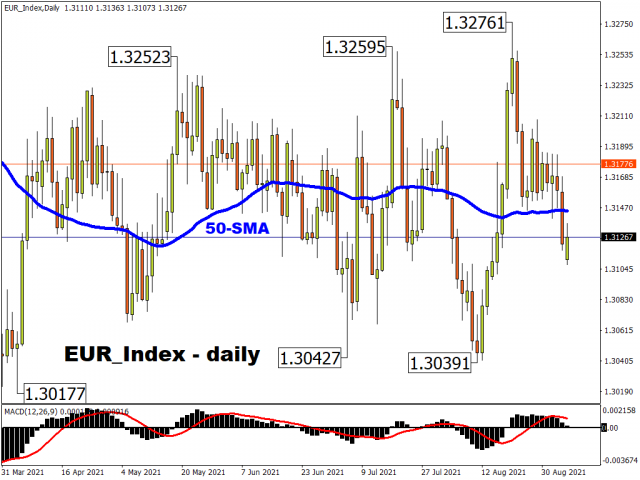

If the euro surges, that should also prompt the benchmark dollar index (DXY) to unwind more of its recent gains, given that the euro accounts for 57.6% of the DXY.

However, if the mid-week speeches from Fed officials sound defiantly hawkish even in the face of last month’s US hiring slump, that should buttress the greenback.

Hence, pay attention to euro this week, which is bound to reflect market expectations on the ECB’s policy outlook.

A surprise hawkish pivot could prompt this equally-weighted euro-index to break to the upside, having been trading sideways since mid-April.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026

- Oil prices jumped 4% amid a new wave of escalation between the US and Iran Jul 13, 2026

- EUR/USD: US Inflation Will Determine Everything Jul 13, 2026