This coming Friday’s US nonfarm payrolls report will be interpreted within the context of Fed Chair Jerome Powell’s Jackson Hole speech on 27 August. This key jobs report could dictate the US dollar‘s next move, which in turn could roil oil prices as well, with commodity markets also honing their attentions on a crucial OPEC+ decision on its intended supply hikes.

Here are the events that could move global financial markets this week:

Monday, August 30

Tuesday, August 31

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

- JPY: Japan July industrial production and unemployment

- CNH: China August manufacturing and composite PMIs

- NZD: ANZ August business confidence

- EUR: Eurozone August CPI

- CAD: Canada GDP (June, 2Q)

- USD: US August consumer confidence

Wednesday, September 1

- CNH: China August Caixin manufacturing PMI

- Japan, Eurozone, UK, US manufacturing August PMIs

- EUR: Eurozone unemployment

- Brent Oil: OPEC+ decision on production

- US Crude: EIA crude oil inventory report

Thursday, September 2

Friday, September 3

- CNH: China Caixin August services and composite PMIs

- JPY: Japan August services and composite PMIs

- GBP: UK August services and composite PMIs

- EUR: Eurozone July retail sales, August services and composite PMIs

- USD: August US nonfarm payrolls, services and composite PMIs, ISM services index

Tapering now less-feared?

Despite saying he is open to pulling back on the central bank’s asset purchases this year, Powell sought to divorce the idea of tapering as an immediate precursor to a US interest rate hike.

In other words, although the Fed’s tapering may indeed start this year, the rate hike may not follow soon after the tapering ends.

This is because the Fed Chair once again said he wants to see sustained above-target inflation and a broad-based recovery in the jobs market. At Jackson Hole, he sent out a reminder about the 6 million jobs that are still lost since the pandemic, as well as reiterating his belief that the inflation surges may be “transitory”.

That message was heeded by the markets. After Powell’s speech, markets lowered their expectations for a November 2022 US rate hike from 53% to 40.5%. However, they still are forecasting a greater-than-even chance (76.5%) of a pre-Christmas rate hike in December 2022.

And this is where Friday’s jobs report comes in.

Markets are currently expected a figure of 750,000 jobs added last month, which is lower than the June and July figures that were above 900k.

USD bears could breathe a sigh of relief on signs of moderating jobs growth and a stagnant unemployment rate, as those should mean a longer runway before the US interest rate hike. And given the persistent threat of the Delta variant’s spread through the world’s largest economy, that could delay workers’ return to jobs. If this Friday’s jobs data indeed prove to be subdued, that might lower the chances of a sooner-than-later Fed rate hike, while preventing the greenback from surging higher in the interim.

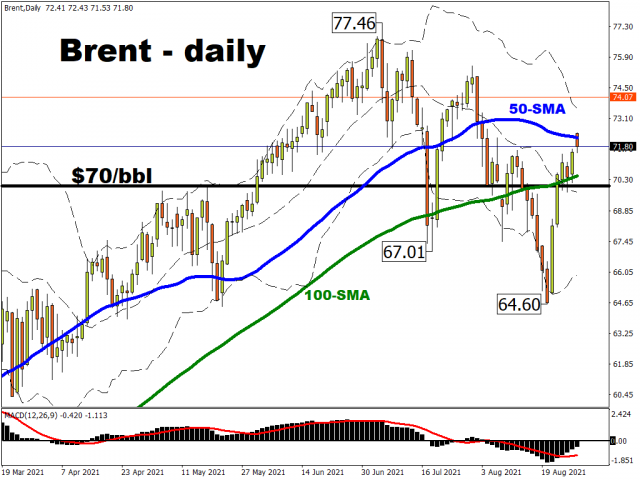

Oil markets await OPEC+ decision

Recall that back in July, OPEC+ agreed to raise output by 400k barrels per day (bpd) starting in August, accompanied by subsequent 400k bpd hikes each ensuing month.

However, since that July decision, the Delta variant’s resurgence in major economies has forced lockdowns once more in countries such as China, Australia, and New Zealand. Hence, it remains to be seen how OPEC+ takes into account these demand-side risks, while ensuring members can claim enough market share to keep them satisfied.

Although oil markets are still expected to tighten through year-end, one doesn’t need to be reminded about how swiftly the Delta variant can alter that outlook.

Should OPEC+ press ahead with its intended supply hikes, that could signal confidence that global demand is robust enough to absorb that incoming supply. Still, if traders and investors don’t share that same optimism, should OPEC+ leave its supply hike plans unchanged, that could prompt Brent oil to unwind recent gains and falter back into the sub-$70/bbl region once more.

Oil markets will also be closely monitoring the impact of Hurricane Ida on US oil supply infrastructure. Signs of tightening supplies, depending on the duration, could spur oil prices higher despite Brent being resisted at its 50-day simple moving average at the time of writing.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026

- Oil prices jumped 4% amid a new wave of escalation between the US and Iran Jul 13, 2026

- EUR/USD: US Inflation Will Determine Everything Jul 13, 2026