By Han Tan Market Analyst, ForexTime

As we get ready to enter the second half of the year, here are the major events over the coming days that carry enough weight to influence various asset classes:

Monday, June 28

- Fed speak: New York Fed President John Williams

- European Commission’s summer economic forecasts

Tuesday, June 29

- Fed speak: Richmond Fed President Thomas Barkin

- ECB President Christine Lagarde speech

- Germany CPI

- Eurozone economic confidence

- US consumer confidence

Wednesday, June 30

- UK GDP

- Germany unemployment

- Eurozone CPI

- US ADP jobs

Thursday, July 1

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

- China Caixin manufacturing PMI

- OPEC+ meeting

- BOE Governor Andrew Bailey speech

- Eurozone unemployment

- Manufacturing PMI: US, Eurozone, UK

Friday, July 2

- ECB President Christine Lagarde speech

- Eurozone PPI

- US nonfarm payrolls

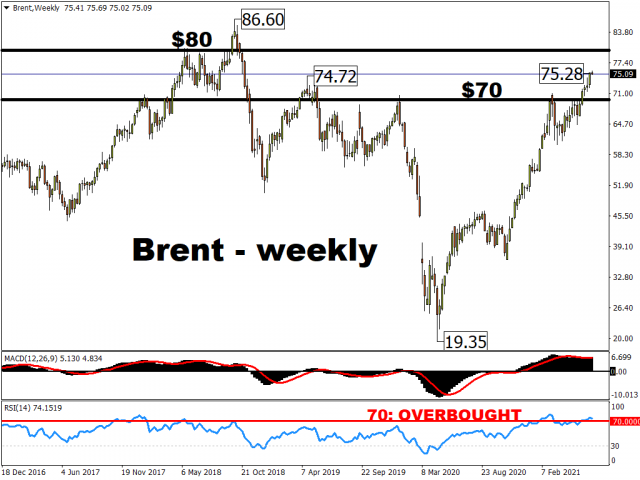

Commodities spotlight: Brent oil

OPEC+ is set to make another key decision on 1 July: whether or not to pump out more oil in August.

Analysts surveyed by Bloomberg expect the cartel to raise their collective output levels by another 550,000 barrels per day (bpd) in August. However, even such a hike is expected to leave global markets in a deficit, which could translate into more upside for oil prices.

As things stand, Brent prices are trading at their highest levels since October 2018. However, judging by its relative strength index, which has crossed the 70 mark to indicate overbought levels, Brent appears ripe for an adjustment in the near-term. Such a pullback would then clear some of the froth to pave the way higher for Brent oil.

However, the uncertainty over the US-Iran nuclear talks still looms over Thursday’s meeting. A US-Iran nuclear deal could see Iran resuming oil exports and upsetting the cartel’s supply plans. It remains to be seen how OPEC+ continues restoring its supplies into the world while taking into account this wildcard.

Still, come Thursday, a smaller-than-expected output hike of fewer than 550,000 barrels per day in August could send Brent prices even higher and closer to the psychologically-important $80/bbl mark.

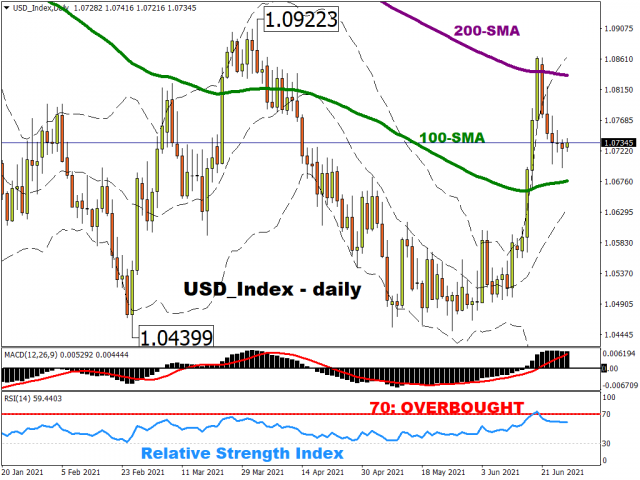

Strike three for US nonfarm payrolls?

The US nonfarm payrolls has disappointed markets for the past two straight months. As things stand, economists are forecasting 700,000 jobs were added in the US labour market this month. If so, that would the highest NFP print in three months, since the March figures.

In the leadup to that tier-1 economic release, this USD index, which is an equally-weighted index comprising 6 major currency pairs, has settled into a more “normal” conditions since pulling back from overbought levels.

However, another lackluster NFP print could give the Fed more runway before having to ease up on its asset purchases, which could prompt the greenback to unwind more of its recent gains and test its 100-day simple moving average (SMA) as the next support level.

Still, the greenback could be jolted by another US jobs shocker this Friday.

A June hiring surge in the US could ramp up expectations for the Fed’s tapering once more. Such a narrative could call upon this USD index’s 200-day SMA as a key resistance level once more.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- The US Tech sector hit by sell‑off. Oil prices decline on renewed negotiations Jul 28, 2026

- Gold Declines, Focus on Fed and Falling Oil Prices Jul 28, 2026

- This week will be one of the most crowded for central‑bank meetings Jul 27, 2026

- EUR/USD Ahead of a Key Week: Holding Near Lows Jul 27, 2026

- COT Metals Charts: Weekly Speculator Changes led by Copper Jul 26, 2026

- COT Bonds Charts: Speculator Bets led by SOFR 3-Months & 5-Year Bonds Jul 26, 2026

- COT Energy Charts: Weekly Speculator Bets led by WTI Crude & Natural Gas Jul 26, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Corn & Soybeans Jul 26, 2026

- The US introduces new import tariffs for 60 countries. Brent crude surpasses $100 per barrel Jul 24, 2026

- USD/JPY Breaks Records: Nothing Slows the Yen’s Decline Jul 24, 2026