By Lukman Otunuga Research Analyst, ForexTime

Despite a disappointing non-manufacturing Chinese PMI reading, Asian bourses are holding up today with eyes on US jobs data and the latest Eurozone inflation print. The Chinese composite PMI unexpectedly fell from 54.2 to 52.9 earlier this morning with details showing a stabilisation of the manufacturing gauge but a setback in the non-manufacturing reading. New restrictive measures in Gaundong to contain a regional Covid outbreak are mainly responsible for this with waning external demand contrasting with rising domestic orders.

Risk mood improved

Markets took comfort in Moderna saying that its vaccine is effective against the Delta variant of the virus with the S&P500 marginally higher and closing at all-time highs. The tech-laden Nasdaq also notched another record peak rising for a sixth day in seven with Facebook pulling back after hitting the magical $1 trillion market cap level. Also adding to more positive sentiment was the US Consumer confidence which jumped with a bounce both in expectations and the current situation.

The dollar went bid breaking out of its recent range and is heading towards the post-Fed highs.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

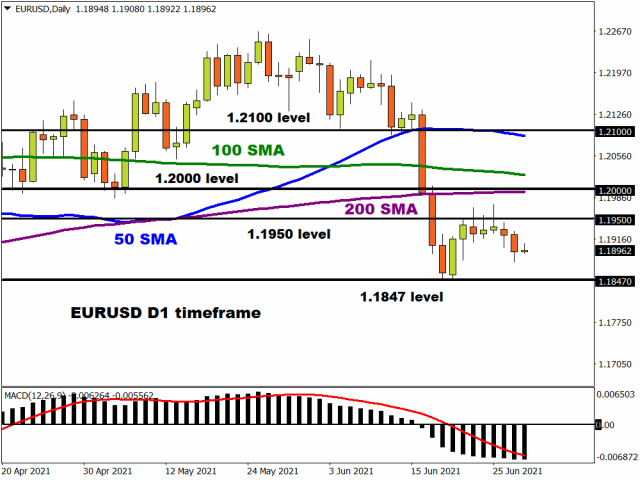

In EUR/USD, this means we are trading below 1.19 again with eyes on the recent cycle lows at 1.1847.

With the monthly US labour market report out on Friday, focus will be on US ADP data today which will be monitored for any signs that private sector hiring has quickened. Although not a great predictor of the NFP headline number, a big beat or miss today can cause near-term volatility. Expectations are for a punchy 600k reading with many analysts hopeful that jobs data comes in strong going forward.

Eurozone inflation subdued

Consensus expects headline and core Eurozone inflation prints to remain relatively subdued at 1.9% y/y and 0.9% y/y respectively when the data is released this morning. Country figures already pointed to a slowdown and these are fairly tame readings compared to those elsewhere. With the outlook remaining muted, the ECB will continue to be one of the last remaining dovish central banks on the block.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026

- Oil prices jumped 4% amid a new wave of escalation between the US and Iran Jul 13, 2026

- EUR/USD: US Inflation Will Determine Everything Jul 13, 2026