By Lukman Otunuga, Research Analyst, ForexTime

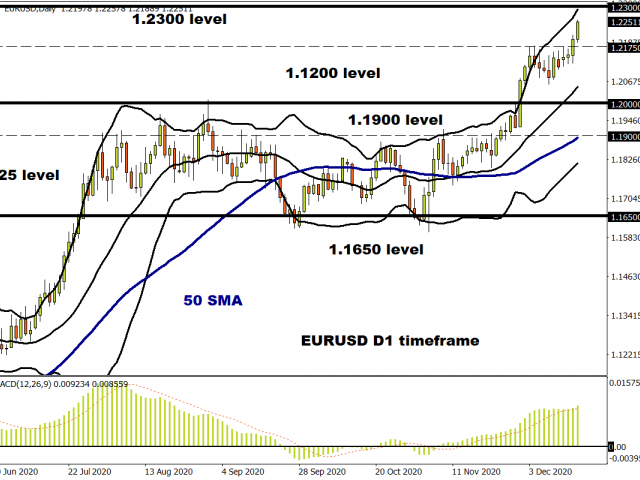

When we look at a number of majors and say there is no obvious resistance ahead, then you know something is up…literally! And so there are key breakouts in nearly every major currency pair today as King Dollar wilts and slides through the 90 level in DXY for the first time since early 2018.

Where to look for the big moves? The Euro has pushed through 1.22 to new highs, cable powered past 1.36, USD/JPY went through 103 and the Aussie surged above 0.76.

When the downtrend is strong and you have a pause in price action, history tells us that compression of trading ranges leads to expansion and a move in line with the dominant long-term trend. Last night’s FOMC meeting didn’t exactly help the greenback either as it disappointed those looking for an increase in bond buying and a focus on long-end bond buying. Fed policy has still to translate into negative real rates and as the odds of US fiscal stimulus rise, so there is more downside for the Dollar. The weekly initial jobless claims numbers have also kicked the bulls whilst down, rising for a second week and way above expectations.

Free Reports:

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Wait-and-see BoE

The Bank of England meeting came and went earlier today with measures and rates left unchanged. There was no mention of negative interest rates as the MPC, like the rest of us, wait anxiously for any white smoke and agreement around a Brexit deal from Brussels. The bank stands ready to act should the need arise, but having increased bond buying at its last meeting, is watching events closely with bank staff estimating that UK GDP will contract by a little over 1% in Q4 of this year.

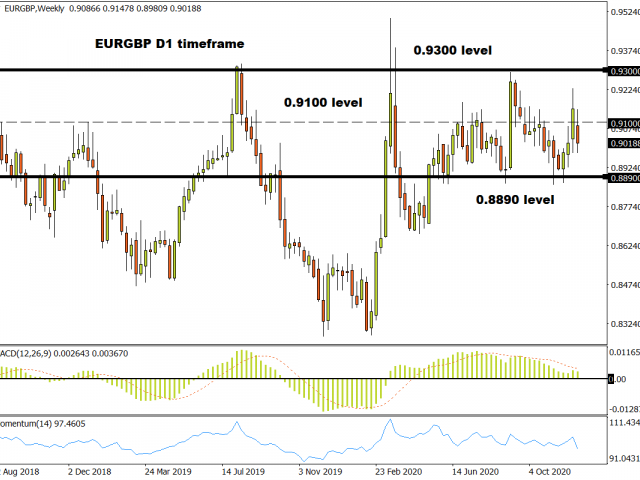

Of course, Brexit is the driver of sterling and GBP has pulled back from its earlier gains. EUR/GBP has been held up a few times at an important Fib level around 0.8990 this month. Do current levels indicate a lot of the good news is factored in already?

Job gains fuel the Aussie

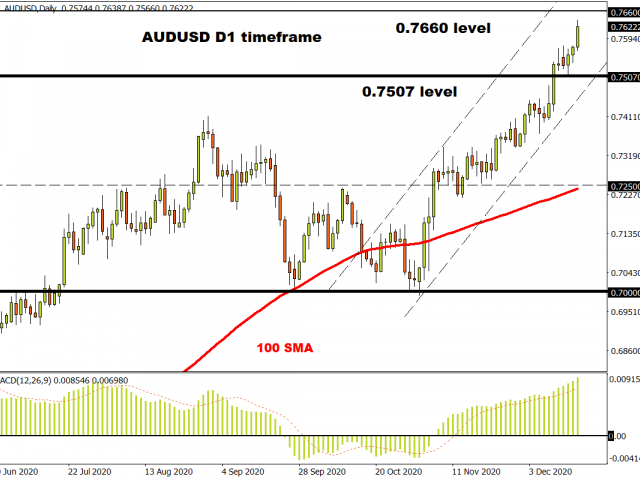

Overnight jobs data down under came in much better than expected, in stark contrast to this afternoon’s figures from the US. A stellar +90k print in November beat expectations of a gain of 50k, following an equally impressive rise in October, while the jobless rate eased to 6.8%. This data simply adds further evidence that Australia is on the road to recovery, having slipped to its first recession in three decades earlier in the year.

AUD/USD has been on a tear, surging for a seventh straight week since the start of November. We are printing levels not seen since June 2018 and momentum indicators are now just touching overbought levels on the weekly chart while the daily is heavily overbought. Bulls would need to see prices below this week’s low of 0.7507 to pull back from their euphoria.

Global reflation is the name of the game with the Aussie, and iron ore especially has boosted AUD as it amounts to over a third of the country’s exports. The China industrial rebound underpinned by vaccine rollouts should keep the uptrend going, although any more QE from the RBA as the bank endeavours to lift wages may see some temporary setbacks for the Aussie.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- EUR/USD: Busy Week Ahead Aug 3, 2026

- Positive sentiment in the AI sector supported stock indices. Oil prices remain volatile Aug 3, 2026

- The Tech‑heavy NASDAQ Index jumped by more than 3.3%. The offshore yuan is trading at its highest level since 2023 Jul 31, 2026

- USD/JPY After Volatility: Multiple Events in One Day Jul 31, 2026

- The US indices sell off amid renewed US-Iran clashes. Oil jumps by 7% Jul 30, 2026

- USD/JPY Temporary in Equilibrium: Multiple Factors in Focus Jul 30, 2026

- GBP/USD at Month’s Lows: The Outlook Remains Weak Jul 29, 2026

- Crude oil falls below $80 per barrel. Australia sees inflation slowdown Jul 29, 2026

- The US Tech sector hit by sell‑off. Oil prices decline on renewed negotiations Jul 28, 2026

- Gold Declines, Focus on Fed and Falling Oil Prices Jul 28, 2026