By Han Tan, Market Analyst, ForexTime

Markets are pausing for breathe after the positive shocks over the last 24 hours. US stock futures and the Dollar are both mixed while risk-sensitive currencies are broadly stronger on the global recovery story. This means the typical safe-haven CHF and JPY are still struggling, while Gold consolidates yesterday’s losses around a key support level.

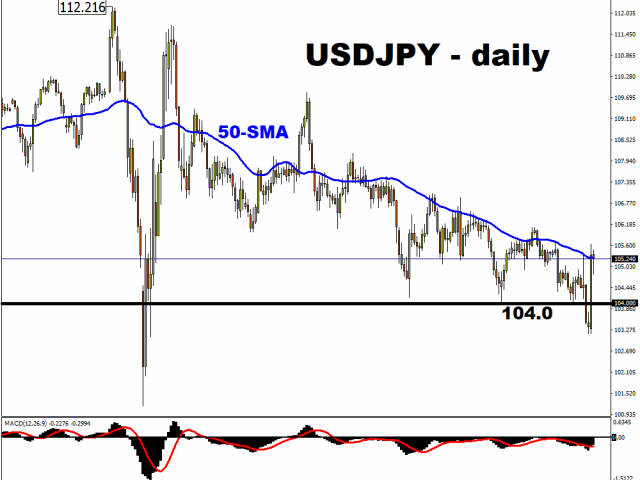

USD/JPY typically has the highest correlation to US yields and many professional traders are now focusing on the magical 1% handle for the benchmark US 10-year. The huge uplift in bond yields around the world yesterday on the ‘vaccine’ moment has potentially shifted the market narrative from a third Covid wave and double-dip recession to vaccination and light at the end of a very dark tunnel.

Higher yields undoubtedly point to economic recovery and more normal times perhaps, but they also hide a dangerous risk and have consequences for both monetary and fiscal policy. Those normal times reduce the need for more easing by central banks and governments which means the new narrative could make it a bumpy road ahead for both bonds and stocks once this early optimism fades. Remember the one about the party and the punch bowl?

Let’s not puncture the good news though, as stock rotation has been something to behold! Yesterday saw the Dow’s biggest outperformance of the Nasdaq since the bursting of the internet bubble in 2000, while bombed-out sectors like banking and energy enjoyed their best days ever, outside of March this year and the GFC in 2008. The many other records scream out loud about extreme positioning and the extraordinary performance of the tech megacaps especially during the pandemic.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Dollar is holding on for now

The US Dollar has bounced off some big levels across the majors in the last few sessions. USD/JPY looked to be settling below 104 before yesterday’s huge move up 1.95 percent. This has propelled the pair firmly back into the range traded during the summer.

Similarly, USD/CHF pierced very strong support around 0.90 before its big vaccine rebound, while USD/CAD is back teetering around the key psychological 1.30 level.

As long as the market continues to expect Fed policy to remain anchored, then investors may be looking to sell Dollar rallies in line with the recovery (and Biden policy mix) cycle, in order to look for higher yielding opportunities elsewhere. But as we said earlier, it’s important we don’t get US 10-year yields exploding through that crucial one percent mark.

Do things come in threes?

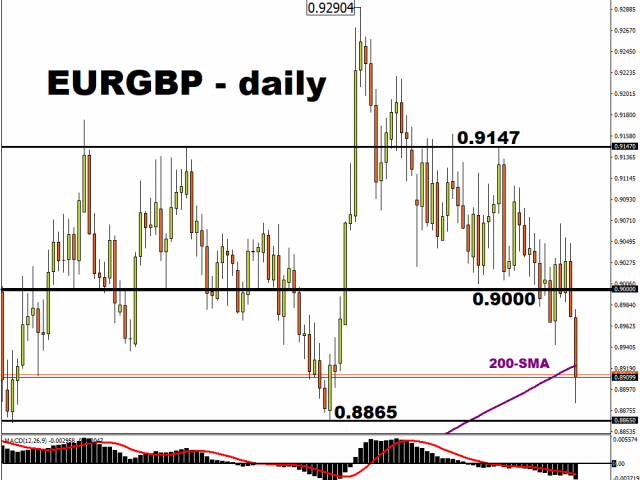

It’s a big week for Brexit with the mid-November de facto deadline in play. GBP is the biggest major outperformer on the day so far, enjoying the news that the House of Lords has rejected the government’s Internal Market Bill. This may ease the path to a trade deal and put the icing on the gateau of the recent positive macro news.

EUR/GBP has broken decisively through cycle support below 0.90 and looks to be heading towards the September and June lows around 0.8860/70. The 200-day Moving Average sits just above at 0.8921.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- Australian trade balance returned to positive territory Aug 6, 2026

- Results in Line for Most Reporting Companies Aug 5, 2026

- Stock indices continue to break records. Oil is falling amid intensified diplomatic dialogue between the US and Iran Aug 5, 2026

- USD/JPY Holds Steady After Intervention: Outlook Remains Uncertain Aug 5, 2026

- EUR/USD: Busy Week Ahead Aug 3, 2026

- Positive sentiment in the AI sector supported stock indices. Oil prices remain volatile Aug 3, 2026

- The Tech‑heavy NASDAQ Index jumped by more than 3.3%. The offshore yuan is trading at its highest level since 2023 Jul 31, 2026

- USD/JPY After Volatility: Multiple Events in One Day Jul 31, 2026

- The US indices sell off amid renewed US-Iran clashes. Oil jumps by 7% Jul 30, 2026

- USD/JPY Temporary in Equilibrium: Multiple Factors in Focus Jul 30, 2026