by JustForex

Preliminary data in the PMI report from IHS Markit showed a slowdown in the German manufacturing sector to 57 in January, the lowest in 4 months. The numbers turned out to be slightly lower than the forecasts of 57.5 but they still indicate a steady increase. The industrial production index remained in the positive zone, although it fell to a five-month low, as the volume of orders decreased. Meanwhile, the number of export orders has increased. The decline in employment was the lowest since June 2019 and price pressures have increased. The assessments of the future economic situation were marked as positive ones.

The service sector continues to suffer the most. This index in Germany fell to 46.8. And while the data is slightly higher than the forecasted one, they can’t be called optimistic. This is the 4th consecutive month of falling amid tightening coronavirus controls. Inflation remained unchanged, but employment rose. Business expectations have also improved.

In France, the service sector declined the most, to 46.5. Slight acceleration of growth in the manufacturing sector couldn’t save the situation. The composite index continued to fall for the fifth month in a row. Also, just as in Germany, there is an increase in workplaces, which is associated with the optimistic sentiment of companies for the next 12 months.

Meanwhile, the coronavirus continues to weigh on economic expectations in the UK. Earlier this week, the government envisioned easing measures in mid-March. It looks like the outlook turned out to be bleaker. When Boris Johnson was asked about the likelihood of extending the quarantine until the summer, he didn’t exclude this.

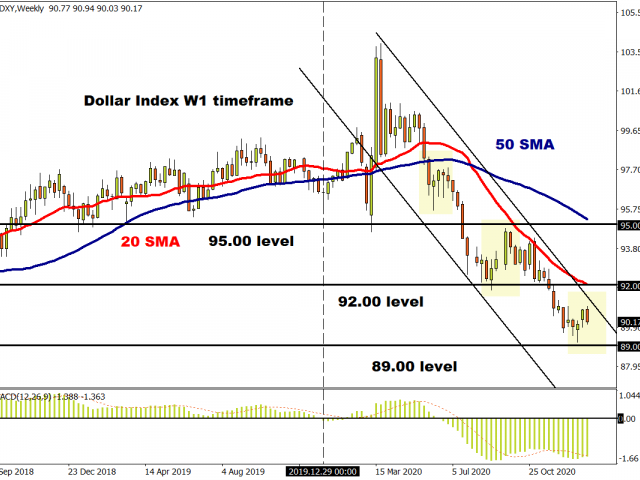

The stock market has ignored the data on the expansion of quarantine in Europe so far. The indices dropped only slightly during the Asian session, which doesn’t look like something serious. The dollar index has stabilized near 90.00.

Main market quotes:

S&P 500 (F) 3,823.88 -22.12 (-0.58%)

Dow Jones 31,176.01 -12.37 (-0.04%)

DAX 13,795.00 -111.67 (-0.80%)

FTSE 100 6,684.25 -31.17 (-0.46%)

USD Index 90.175 +0.048 (+0.05%)

- – New Zealand CPI (QoQ) (4 qtr.) at 00:45 (GMT+2);

- – Australia Retail Sales (MoM) at 03:30 (GMT+2);

- – UK Retail Sales (MoM) at 10:00 (GMT+2);

- – Germany Manufacturing PMI (Jan) at 11:30 (GMT+2);

- – Eurozone Manufacturing PMI (Jan) at 12:00 (GMT+2);

- – UK Services PMI (Jan) at 12:30 (GMT+2).

by JustForex

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.