Source: Ron Struthers (8/7/23)

The long end of the bond market is starting to price in sticky inflation, and Ron Struthers of Struthers’ Stock Reports expects interest rates to rise further. Higher energy prices will start adding to inflation again, adding to the problem. Moderna has broken down on the chart and will be reporting red ink in the next few years. Time to go short.

*Disclaimer: The article is the opinion of Ron Struthers and not of Streetwise Reports. Topics discussed may be controversial to some readers.*

Us old-school analysts remember the days of higher inflation, and the bond market would discount that by wanting higher yields for longer maturities. In this recent bout of inflation, first, the narrative was it was transitory. The next narrative, it would come down with higher interest rates, and then interest rates would drop.

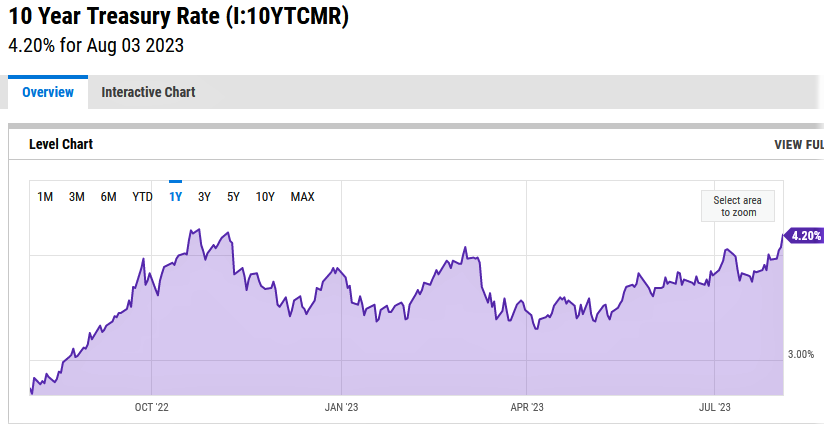

Now headline inflation has fallen to 3.0% YoY, but interest rates are going up, especially at the long end of the bond market. This chart of the 10 Year treasury showed a yield of 4.2% Thursday, and rates are back to the level we saw at last year’s inflation peak.

As you know. I have been commenting for some time that this inflation drop is temporary because of the YoY energy price comparison, and inflation would head back up this fall. It appears the bond market is starting to price in sticky inflation plus supply issues with Bidenomics relentless spending.

Bill Ackman now agrees as the legendary investor is getting ready to cash in on what he says is an imminent repricing of long-term U.S. bonds; he has been preparing for a world where U.S. inflation lingers around 3%.

“If long-term inflation is 3% instead of 2% and history holds, then we could see the 30-year T yield = 3% + 0.5% (the real rate) + 2% (term premium), or 5.5%, and it can happen soon,” he said. “There are many times in history where the bond market reprices the long end of the curve in a matter of weeks, and this seems like one of those times.”

The current yield on a 30-year U.S. Treasury is approximately 4.3%, and it increased after Fitch downgraded the U.S. triple-A credit rating last Tuesday. There has been a lot of news on the U.S. debt downgrade, and no surprise that Biden and his gang blame Trump. Of course, the opposite is true.

According to the non-partisan “market,” the creditworthiness of U.S. Treasury debt improved almost constantly under President Trump and worsened dramatically almost immediately upon President Biden’s inauguration: You can track credit risk via credit default swaps here.

It was understandable that Covid-19 policies of unprecedented stimulus would be short-term, but it has continued under Bidenomics.

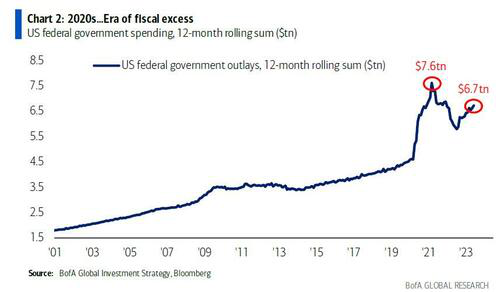

BofA’s Michael Hartnett calls it “The Era Of Fiscal Excess,” and BofA provides this chart below on government spending. The excess will mean higher interest rates.

The Biden Administration does not appear willing to change and fix the problem. They would rather blame Trump. Sadly the market is going to give Bidenomics a very harsh lesson, something that has not happened for a long time. I have been amazed for the past 15 years at how the market has gone along with excess stimulus and QE. It is looking like the day or reckoning is arriving. Interest rates are going much higher, and at the very least, government borrowing will squeeze corporations out of the market.

The Treasury published its quarter refunding statement, in which the U.S. boosted the size of its quarterly sale of longer-term debt for the first time in over 2 1/2 years. The bigger-than-expected jump in issuance showcases the rising borrowing needs that contributed to Tuesday’s decision by Fitch Ratings to lower the sovereign U.S. credit rating by one level to AA+.

Fitch said it expects U.S. finances to deteriorate over the next three years, and that’s using old and outdated assumptions. The current and future reality is much worse. It will mean structurally higher yields, and it is only a matter of time before the buyer of last resort, the Fed will be forced to step in with another round of QE.

What will be the next manufactured crisis that the Fed says they have to come to the rescue for?

As you know, I have been watching the US$82 level on oil, and on Friday, the Oil Market broke out with a close at US$82.82, so we have the higher high and now about a +24% move off the US$67 bottom. A new bull market. The coordinated supply-side management of Saudi Arabia and Russia has set oil prices for a sixth weekly gain, with the two OPEC+ heavyweights extending their production and export cuts into September.

I have commented numerous times that I believe that government energy policies to go electric will cause havoc in energy markets and end up with fossil fuel shortages.

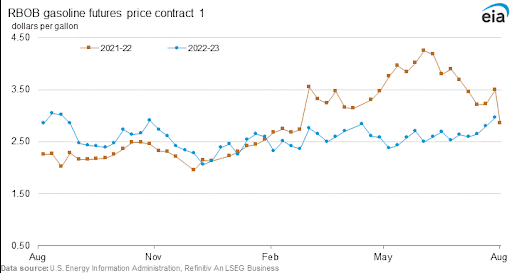

Gasoline inventories have been making new lows, and the next chart on gasoline prices shows new highs this year and are now a little above last August’s prices. And as I have been commenting, energy will soon be adding to inflation again instead of reducing inflation rates. Look out if hurricane season this year hits gulf oil production and refining.

Time to short Moderna again NY:MRNA Recent Price – US$108

We did very well with Moderna Inc. (MRNA:NASDAQ) Put options last January; let’s do it again. The stock broke down on the chart, and their revenues are plummeting with losses taking hold. And vaccine hesitancy continues to rise.

On August 3rd, Moderna reported Q2 results:

- Second quarter 2023 revenues of US$0.3 billion with a net loss of US$1.4 billion and loss per share of US$3.62;

- Covid-19 vaccine sales are now US$2.1 billion for the first half of the year;

- Company expects 2023 COVID-19 vaccine sales of US$6 billion to US$8 billion, dependent on U.S. vaccination rates.

“Second quarter sales were on target, given the seasonal nature of Covid. I am pleased with the progress our U.S. commercial team has made to get new contracts in place for fall 2023. We are on track to deliver 2023 sales between US$6 billion to US$8 billion, depending on Covid vaccination rates in the U.S.,” said Stéphane Bancel, CEO of Moderna. “Our late-stage clinical pipeline is firing on all cylinders with four infectious disease vaccines in Phase 3, including RSV, which was recently submitted to regulators for approval. Our individualized neoantigen therapy is now in Phase 3 for melanoma, and our lead rare disease program for PA is in dose confirmation. We believe that all these products should launch in 2024, 2025, or 2026, and we are continuing to invest in scaling Moderna to bring forward an unprecedented number of innovative mRNA medicines for patients.”

Moderna will be totally reliant on Covid-19 vaccine sales to drive revenues for the next 12 months. I believe they have zero chance of making their US$6 to US$8 billion targets. If they did hit, say mid, way at US$7 billion, it would likely mean no profits. Their cost of sales in Q2 was US$731 million, and the R&D expense was over US$1 billion.

This will likely stay high with their pipeline of development vaccines. General Administration expense was US$332 million in Q2, and this will not likely drop much. Their expenses are running over US$2 billion per quarter, so another US$4 or US$5 billion in sales for the rest of the year will not generate profits.

How long can the stock stay over US$100 with a market cap of around US$40 billion, with mounting losses and no profits in sight?

That said, what if they disappoint as I expect they will?

This year, the UK has followed other European countries and is not recommending Covid-19 shots for those under 50. I expect this trend will continue as the risk/reward does not make sense for younger people. As more and more independent studies come out, we find that the risk or adverse events with these shots are much higher than we were led to believe. Also, the effectiveness of the shots is very questionable.

Some examples –

Example One – Eight people who died suddenly after receiving a messenger RNA (mRNA) COVID-19 vaccine died due to a type of vaccine-induced heart inflammation called myocarditis, South Korean authorities said after reviewing the autopsies. The study was published by the European Heart Journal on June 2 and was funded by the South Korean government. Myocarditis wasn’t suspected as a clinical diagnosis or cause of death before the autopsies, researchers said. And another key factor is that, in general, very few autopsies have been done in any country.

Example 2 – A new study released in mid-May indicates the more shots you get, the more you are susceptible to Covid and other diseases because there is harm done to your immune system. Something I and many expert doctors and scientists have been warning about. Now proof is mounting with this independent study that received no external funding, and the scientists indicate no conflict of interest. Of course, it is scientific in nature, but here is most of the abstract that summarizes it.

Increasing evidence has shown that, as with many other vaccines, they do not produce sterilizing immunity, allowing people to suffer frequent re-infections. Additionally, recent investigations have found abnormally high levels of IgG4 in people who were administered two or more injections of the mRNA vaccines. HIV, Malaria, and Pertussis vaccines have also been reported to induce higher-than-normal IgG4 synthesis. It has been suggested that an increase in IgG4 levels could have a protecting role.

However, emerging evidence suggests that the reported increase in IgG4 levels detected after repeated vaccination with the mRNA vaccines may not be a protective mechanism; rather, it constitutes an immune tolerance mechanism to the spike protein that could promote unopposed SARSCoV2 infection and replication by suppressing natural antiviral responses.

Example 3 – A new study recently published in Burns shows a sudden increase in StevensJohnson syndrome (SJS)—a rare and potentially fatal skin disorder. It appears to be triggered by COVID-19, increased vaccination rates, or a lowered threshold (immune response) caused by vaccines or previous infection, according to a large case series. Researchers with the burns unit at Concord Repatriation General Hospital in Australia saw two to four cases of SJS, or toxic epidermal necrolysis, per year prior to COVID-19. In the first six months of 2022 alone, the same burn center observed a seven-fold rise in cases.

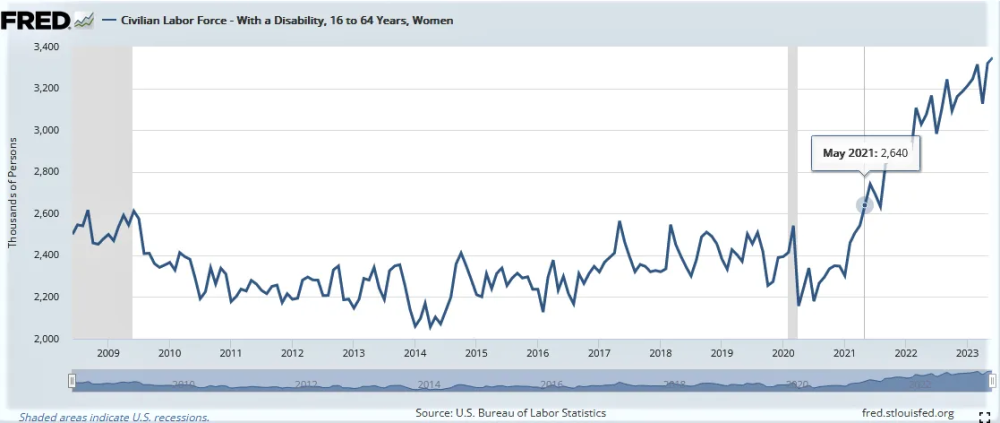

Example 4 – Since the shots, disability numbers have skyrocketed in the Fed’s monthly jobs report.

As of June – there are over 4 million disabled American workers. To put this in a numbers perspective — three standard deviations only happen 0.03% of the time, and what we are seeing here is eight deviations and higher. These are called ‘black swan’ events, which are very very rare.

Market analysts Ed Dowd has been tracking this info and he is challenging the medical institutions that make $billions — to investigate the cause. However, most of us have a very good idea of what the cause is.

Example 5 – Under the Freedom of Information act, documents were released by BioNTech to the European Medicines Agency (EMA) in late June. They reveal tens of thousands of serious adverse events and thousands of deaths among people who received the Pfizer-BioNTech mRNA COVID-19 vaccine.

The documents show that cumulatively, during the clinical trials and post-marketing period up to June 18, 2022, a total of 4,964,106 adverse events were recorded, yes almost 5 million. Among children under age 17, 189 deaths and thousands of serious adverse events were reported. According to an analysis by commentator and author Daniel Horowitz, the percentage of adverse events classified as serious was “well above the standard for safety signals usually pegged at 15%,” and women reported adverse events at three times the rate of men. 60% of cases were reported with either “outcome unknown” or “not recovered,” suggesting many of the injuries “were not transient,” Horowitz said.

Example 6 – I pointed out earlier that a Texas Federal Judge in May ordered the accelerated release from the FDA of the Moderna trial data, requiring all documents to be made public by mid-2025 rather than, as the FDA wanted, over the course of about 23.5 years.

Well, the first 15,000 pages or so of data released by DTR add to the growing body of evidence suggesting that the COVID-19 vaccines may not be as safe as advertised.

The pages also included a rat study on pregnancy and fetuses. The findings of this study are troubling. The mRNA vaccine altered the skeletal variations of the rat fetuses, and the “female pregnancy index” of the vaccinated rats was significantly lower than the control group. I could go on with more examples, but I have no doubt that vaccine hesitancy will continue to rise. Plummeting Trust in the narrative and public health sector.

Zero healthy individuals under the age of 50 have died of COVID-19 in Israel, according to newly released data.

“Zero deceased of 18–49 years of age with no underlying morbidities,” the Israel Ministry of Health (MOH) said in response to a formal request from an attorney. The information was sparked by a freedom of information request filed by attorney Ori Xabi, who has been filing several such requests as he seeks to obtain information from the MOH regarding the COVID-19 pandemic and COVID-19 policies.” That only means that what we were told for three years was not true,” he said.

Big Tech firms were asked to censor COVID-19 information that ended up being true, Meta CEO Mark Zuckerberg has assessed. “Just take some of the stuff around COVID earlier in the pandemic where there were real health implications, but there hadn’t been time to fully vet a bunch of the scientific assumptions,” Zuckerberg, whose company is the parent of Facebook and Instagram, said during a discussion with podcaster Lex Fridman that was released on June 8.

According to a report by the Public Health Agency of Canada (PHAC). The report, based on questionnaires with 2,088 Canadians and 16 focus groups nationwide, noted that less than one quarter (22 percent) of those surveyed said they were more likely to trust federal agencies since the pandemic. I wonder why!

In the U.S., a study conducted by Pew Research found that post-pandemic, there was a smaller percentage of Americans expressing the belief that children should be required to be vaccinated in order to attend schools. In prior studies, 82% had supported vaccine requirements, which fell to approximately 70% in the recent report. The report also found that fewer than half of U.S. adults consider the preventative health benefits of COVID-19 vaccines to be high, with a majority also perceiving the risk of side effects as being at least medium.

Overall, 62% of those questioned believed the COVID-19 vaccines’ benefits did outweigh their risks — though this is far below other childhood vaccines, with MMR vaccines seeing support levels of 88%. Conclusion More and more information becomes available that questions the safety and effectiveness of the shots. What is more troublesome is a lot of this information has to come out with court action. What are they trying to hide? It certainly just causes more distrust by the public and more vaccine hesitancy. I expect Moderna has little chance of meeting its revenue targets with Covid-19 vaccine sales, and any other potential products are at least one or two years away.

According to 24 analyst ratings, the average is overweight, with an average target price of US$182.72. However, the average earnings estimates are all negative for the next three years, around -$4/share. There are only two sell ratings, and given the outlook, there will probably be many downgrades. The technical view on the chart looks quite bearish. The stock fell through support around US$115 goes back over two years, and I see the next target around US$70.

The next earnings report is November 2, so if we go with the November 17 put options, we can catch what I expect will be another negative quarterly report.

I like the November US$115 Put for around US$8.50, and it is about US$7 in the money. You could go for more leverage and go with the November US$105 Put for around US$3.00. It is out of the money, but if the stock drops to my target of US$70 by then, it will have a bigger percentage gain than the November US$115 Put.

Important Disclosures:

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

- This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

For additional disclosures, please click here.

Struthers Resource Stock Report Disclosures

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author’s control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.