By JustMarkets

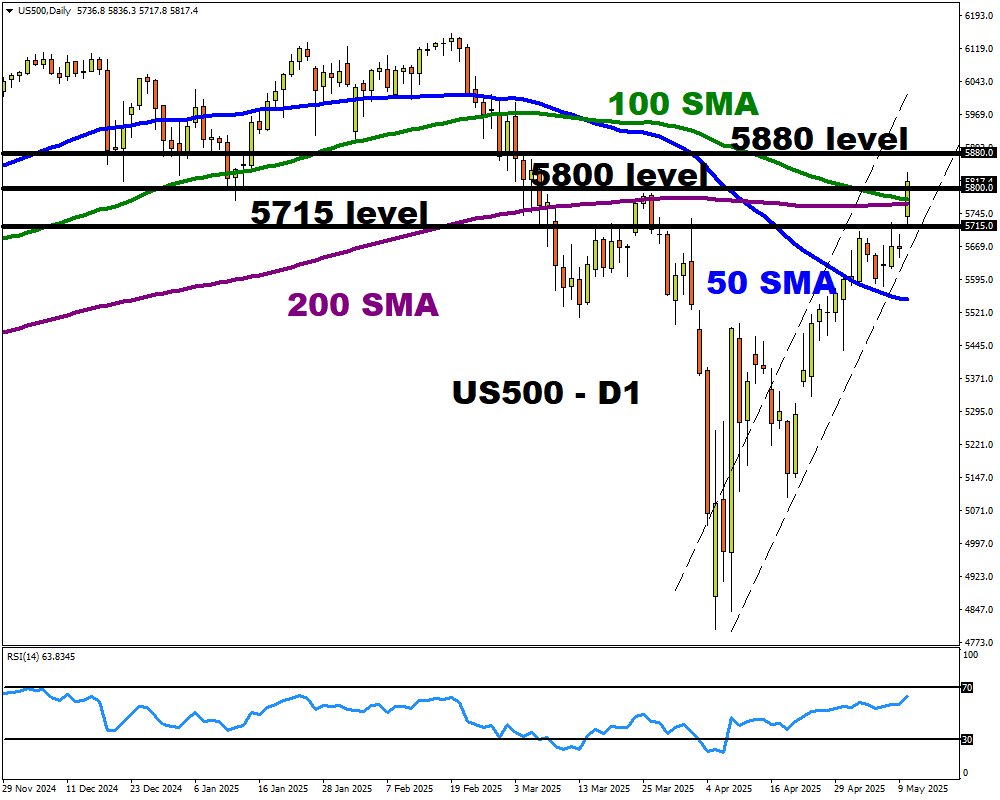

At the end of Monday, the Dow Jones Index (US30) was up 0.32%. The S&P 500 Index (US500) added 0.09%. The Nasdaq Technology Index (US100) closed higher by 0.09%. Surprisingly, markets digested positively the downgrade of the US credit rating by Moody’s to Aa1. Treasury Secretary Scott Bessent downplayed the move and urged trading partners to engage during the 90-day tariff pause.

The Mexican peso rose to 19.40 per dollar, nearing a seven-month peak of 19.38 reached on May 14, as Moody’s downgrade of the US sovereign debt rating to Aa1 on May 16 and rising bets on an imminent Federal Reserve rate cut reduced the dollar’s appeal. The Bank of Mexico’s unanimous 50 basis point rate cut to 8.50% on May 15 amid core and core inflation at 3.9% and Q1 GDP growth of just 0.2% drove down yields in Mexico, but a weaker dollar largely supported the peso’s rise.

The Canadian dollar is holding near 1.40 per dollar, remaining near the one-month low of 1.398 hit on May 14, amid US dollar softness offsetting dovish expectations for the Bank of Canada. However, longs remain constrained by expectations of a dovish Bank of Canada rate after disappointing April jobs growth and a rise in the unemployment rate to 6.9% fueled speculation of a rate cut in June, dampening investor appetite for Canadian assets. Canada’s inflation report will be released today, where the same reading as last month is expected.

Equity markets in Europe were mostly up on Monday. Germany’s DAX (DE40) was up 0.70%. France’s CAC 40 (FR40) closed down 0.04%, Spain’s IBEX35 (ES35) gained 0.25%, and the UK’s FTSE 100 (UK100) closed higher 0.17%. The positive sentiment was boosted by a landmark agreement between the UK and the European Union, which calls for closer cooperation in key areas such as energy, trade, defense, travel, and fisheries. The Eurozone’s annual inflation rate for April 2025 was confirmed at 2.2%, just above the European Central Bank’s target of 2.0%.

The US natural gas (XNG/USD) prices fell more than 6% to below $3.10/MMBtu, the lowest since April 25, and extended last week’s decline of more than 12%, driven by weaker near-term demand and lower LNG exports. Warmer-than-normal weather in late May is expected to curb heating demand.

Asian markets were mostly falling yesterday. Japan’s Nikkei 225 (JP225) fell by 0.68%, China’s FTSE China A50 (CHA50) lost 0.42%, Hong Kong’s Hang Seng (HK50) decreased by 0.05%, and Australia’s ASX 200 (AU200) was negative 0.58%.

The People’s Bank of China (PBOC) cut key lending rates to a record low during its May meeting, matching market expectations and marking the first cut since October. The move followed wide-ranging monetary easing measures announced by Beijing earlier this month to support a sluggish economy and mitigate the potential impact of ongoing trade tensions with the US. The one-year prime rate (LPR), the benchmark for most corporate and household loans, was cut by 10 basis points to 3.0%, while the five-year LPR, which determines mortgage rates, was cut by the same amount to 3.5%. The offshore yuan fell to around 7.22 per dollar, posting a third straight session of losses and hitting a one-week low.

The Australian dollar slipped to $0.643 on Tuesday, rebounding from the previous session’s gains, after the Reserve Bank of Australia cut its key interest rate by 25 bps, as expected, and signaled that risks to the economy were diminishing. Policymakers noted that data for the March quarter confirmed further easing in inflation and pointed to reduced upside risks to inflation. Updated expectations indicated that core inflation is likely to remain near the middle of the 2-3% target range. The RBA also pointed to developments in global trade as a potential impediment to growth, which strengthened the case for additional rate cuts and put pressure on the Australian dollar.

S&P 500 (US500) 5,963.60 +5.22 (+0.09%)

Dow Jones (US30) 42,792.07 +137.33 (+0.32%)

DAX (DE40) 23,934.98 +167.55 (+0.70%)

FTSE 100 (UK100) 8,699.31 +14.75 (+0.17%)

USD Index 100.36 -0.73 (-0.73%)

News feed for: 2025.05.20

- China PBoC Loan Prime Rate at 04:15 (GMT+3);

- Australia RBA Interest Rate Decision at 07:00 (GMT+3);

- Australia RBA Monetary Policy Statement at 07:00 (GMT+3);

- Australia RBA Press Conference at 08:30 (GMT+3);

- Canada Consumer Price Index (m/m) at 15:30 (GMT+3).

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.