The US stock indices traded higher on Friday. By closing the stock market Dow Jones (US30) gained 1.27% (+2.69% for the week), and S&P 500 (US500) added 1.73% (+2.99% for the week). The NASDAQ Technology Index (US100) jumped by 2.09% (+2.70% for the week).

The University of Michigan index for August 2022 rose to 55.1 from 52.5. According to the report, the US inflation is expected to be 5% by year-end (5.2% previously), with the 5-year inflation rate rising from 2.9% to 3.0%. Other data showed that US import prices declined in July for the first time in seven months due to lower fuel and non-fuel costs.

Mary Daly, president of the Federal Reserve Bank of San Francisco, said Thursday that she is open to another 75 basis point increase in September. At the moment, traders estimate there is about a 42.5% chance of a 75-basis-point Fed rate hike in September and a 57.5% chance of a 50-basis-point hike.

Equity markets in Europe were mostly up on Friday. German DAX (DE30) gained 0.74% (+0.67% for the week), French CAC 40 (FR40) added 0.14% (+0.67% for the week), Spanish IBEX 35 (ES35) gained 0.24% (+2.17% for the week), British FTSE 100 (UK100) rose by 0.47% (+0.82% for the week).

In France, inflation rose to 6.8% year-over-year, while in Spain, consumer prices reached 10.8% (y/y), the highest level since 1984. Europe is digging deeper into the energy crisis, and the high inflation rate only exacerbates an already huge number of problems. Commerzbank expects a recession in the Eurozone as a baseline scenario.

The UK’s economic outlook is deteriorating rapidly. While the labor market remains resilient, there is a high probability that UK consumer inflation could reach double digits this week. The Bank of England has already warned that inflation could reach 13% this year (expected to peak in October 2022) while the economy enters five quarters of recession.

In Germany, low water levels on the Rhine, Germany’s commercial artery, have disrupted shipping and increased transportation costs more than fivefold.

Poland’s Foreign Ministry announced that it is joining Finland, Estonia, Latvia, and Denmark to impose a Europe-wide ban on tourist visas for Russians.

The EU and 42 countries issued a statement calling on Russia to immediately withdraw troops from the territory of the Zaporizhya nuclear power plant and Ukraine.

Asian markets traded higher last week. Japan’s Nikkei 225 (JP225) gained 2.26%, Hong Kong’s Hang Seng (HK50) added 0.55%, and Australia’s S&P/ASX 200 (AU200) rose by 0.24%. At the opening session on Monday, the Japanese indices jumped over 1% on the background of the GDP growth in the last quarter. Chinese indices, on the contrary, declined as data on industrial production and retail sales failed to meet economists’ expectations. Against this backdrop, China’s Central Bank unexpectedly cut key lending rates on Monday.

Chinese leader Xi Jinping plans to meet with US President Joe Biden on his first overseas trip in nearly three years, which is scheduled for November this year.

Japanese Prime Minister Fumio Kishida on Monday instructed officials to develop an additional package of steps by early September to ease consumers’ pain from rising wheat and energy import prices amid Russia’s war in Ukraine.

In the commodities market futures on lumber (+22.85%), cotton (+12.96%), natural gas (+8.88%), gasoline (+6.74%), coffee (+6. 49%), silver (+5%), soybeans (+4.65%), palladium (+4.34%), corn (+4.3%), platinum (+4.19%), sugar (+3.96%), wheat (+3.71%), copper (+3.59%), Brent oil (+3.26%), and WTI oil (+3.22%) showed the biggest growth over the week. Orange juice futures (-0.68%) showed the biggest drop.

S&P 500 (F) (US500) 4,280.15 +72.88 (+1.73%)

Dow Jones (US30) 33,761.05 +424.38 (+1.27%)

DAX (DE40) 13,795.85 +101.34 (+0.74%)

FTSE 100 (UK100) 7,500.89 +34.98 (+0.47%)

USD Index 105.67 +0.58 (+0.56%)

Important events for today:

– Japan GDP (q/q) at 02:50 (GMT+3);

– China Industrial Production (m/m) at 05:00 (GMT+3);

– China Unemployment Rate (m/m) at 05:00 (GMT+3);

– China Retail Sales (m/m) at 05:00 (GMT+3);

– Japan Industrial Production (m/m) at 07:30 (GMT+3);

– US NY Empire State Manufacturing Index (m/m) at 15:30 (GMT+3);

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

The FBI recovered confidential and top-secret items from Mar-a-Lago during its Aug. 8, 2022, search of the estate – pointing to former President Donald Trump’s potential violation of several federal laws.

A Florida federal judge – the same one who issued the warrant to search Trump’s estate – ordered on Aug. 12, 2022, that the document be made public – along with an inventory of items seized during the FBI’s raid.

The unsealed documents seem to indicate that the U.S. Department of Justice believes Trump may have violated the Espionage Act, as well as other criminal laws relating to the handling of public records.

Clark Cunningham, Georgia State University legal scholar and an expert on search warrants, explains how this new information connects to possible criminal wrongdoing by the former president.

These laws were potentially violated

The released warrant authorized the FBI to search for evidence that Trump has violated three key laws.

First, there is the Espionage Act, which applies to possession of information related to the national defense that could be used to harm the U.S. or aid a foreign adversary. This law applies to someone who, like Trump, initially had lawful possession of such information but who, after their time in office ended, refuses to return it to the government.

Then, there is obstruction of justice, which includes concealing documents to obstruct a federal investigation.

Finally, there is the Public Records statute, which prohibits someone entrusted with a public record from “concealing” that document.

What’s in the inventory

The inventory of items taken by the FBI from Mar-a-Lago apparently shows Trump may have violated these laws in a number of different ways.

The inventory shows that FBI agents seized documents designated “SCI,” which refers to Sensitive Compartmented Information. In simple terms, this is classified information that comes from intelligence sources – and must be handled only within secured government locations.

Because this kind of sensitive information can reveal both methods and procedures for collecting intelligence – including the identity of undercover agents in hostile countries – the presence of such materials at Mar-a-Lago may be a violation of the Espionage Act, if Trump was willfully retaining this information after the government demanded its return.

The inventory also refers to numerous “top-secret” documents. Federal law definesthis as “information or material which requires the highest degree of protection” and could threaten national security. The FBI’s discovery of top-secret documents could corroborate The Washington Post’s report that the FBI search included classified documents related to nuclear weapons. The FBI also seized documents designated “secret” and “confidential.”

All told, the FBI removed 27 boxes and other individually listed items, including photographs.

Trump received a federal subpoena in the spring of 2022 to return documents taken from the White House.

So if the inventory includes items that should have been returned in response to the subpoena, but were not, that can be evidence of obstruction of justice and concealment of public records.

A defense that might not hold

Trump has suggested that the FBI may have planted evidence during its search.

However, federal rules about search warrants provide strong protection against such a possibility, by requiring that a government officer present when a search warrant is carried out “prepare and verify an inventory” of property seized in the presence of “another officer” and “the person from whom, or from whose premises, the property was taken.”

The officer must then “give a copy of the warrant and a receipt for the property taken to the person from whom, or from whose premises, the property was taken,” according to these rules.

U.S. Attorney General Merrick Garland said during his Aug. 11 statement about the search that these procedures were followed. “Copies of both the warrant and the FBI property receipt were provided on the day of the search to the former president’s counsel, who was on site during the search,” Garland said.

The federal rules say that if the owner of the premises is not present, another “credible person” can verify the inventory – in this case, the unsealed records confirm that Trump’s attorney, Christine Bobbs, acknowledged receipt of the inventory at 6:19 p.m. on Aug. 8, 2022.

Limited precedent for unsealing these types of documents

It’s relatively rare for a judge to unseal court records of a search warrant, unless an actual criminal prosecution is underway and the record is needed in court.

One other notable exception occurred in December 2016 when a New York federal court issued an unsealing order for the Oct. 30, 2016, search warrant requested by former FBI Director James Comey to investigate emails improperly stored by former Secretary of State Hillary Clinton.

Unlike the Justice Department’s Aug. 12, 2022, order regarding Trump, the unsealing of the Clinton-related warrant included the underlying affidavit. An affidavit is a statement made under oath to the issuing judge to obtain the warrant.

Disclosure of these documents provided the basis for a firestorm of criticism by Clinton allies that there was insufficient evidence to support the FBI’s warrant application.

As explained in a judge’s October 2016 order to make the search warrant for the Clinton investigation public, warrant application proceedings “have historically been highly secretive in nature and closed to the press and public.” In that case, the judge said that in deciding whether to unseal, courts must consider both the government’s interest in not compromising an ongoing criminal investigation and the need to protect the privacy and reputation of the person subject to the search who may never be charged with a crime.

However, for the Mar-a-Lago warrant, both the government and Trump, the subject of the search, consented to the unsealing.

True to his reputation for careful judgment, Garland went by the book in response to an avalanche of attacks from Trump allies demanding transparency about the search. The warrant and inventory have now been released for all to see through a proper court procedure – which Trump publicly endorsed.

Water is the most essential resource for life, for both humans and the crops we consume. Around the world, agriculture accounts for 70% of all freshwater use.

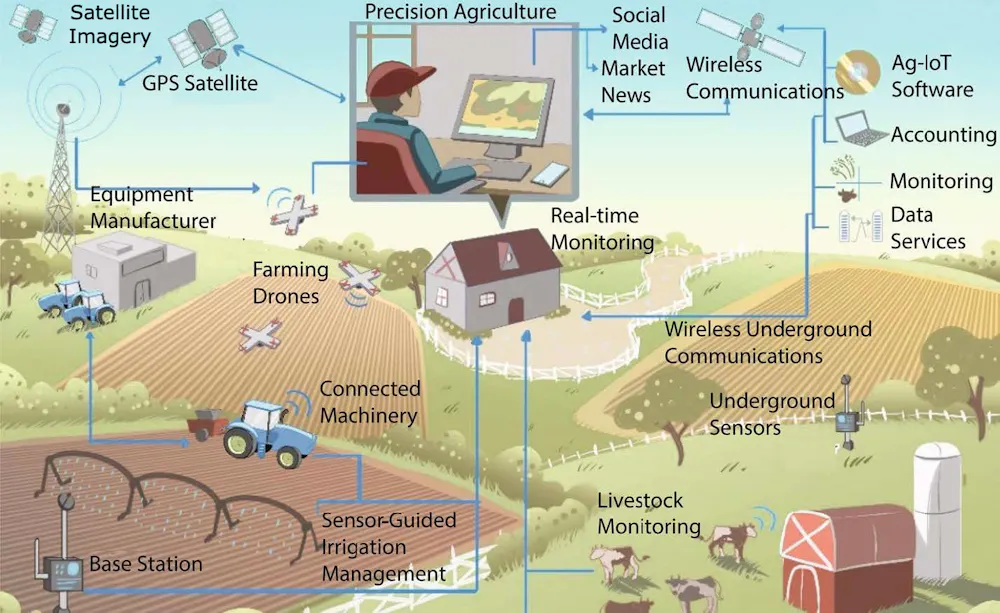

The Internet of Things is a network of objects equipped with sensors so they can receive and transmit data via the internet. Examples include wearable fitness devices, smart home thermostats and self-driving cars.

In agriculture, it involves technologies such as wireless underground communications, subsurface sensing and antennas in soil. These systems help farmers track conditions on their land in real time, and apply water and other inputs such as fertilizer exactly when and where they are needed.

Sensors installed in a corn field. Abdul Salam, CC BY-ND

In particular, monitoring conditions in the soil has great promise for helping farmers use water more efficiently. Sensors can now be wirelessly integrated into irrigation systems to provide real-time awareness of soil moisture levels. Studies suggest that this strategy can reduce water demand for irrigation by anywhere from 20% to 72% without hampering daily operations on crop fields.

What is the Agricultural Internet of Things?

Even in dry places such as the Middle East and North Africa, farming is possible with efficient water management. But extreme weather events driven by climate change are making that harder. Recurrent droughts in the western U.S. over the past 20 years, along with other disasters like wildfires, have caused billions of dollars in crop losses.

Water experts have measured soil moisture to inform water management and irrigation decisions for decades. Automated technologies have largely replaced hand-held soil moisture tools because it is hard to take manual soil moisture readings in production fields in remote locations.

In the past decade, wireless data harvesting technologies have begun to provide real-time access to soil moisture data, which makes for better water management decisions. These technologies could also have many advanced IoT applications in public safety, urban infrastructure monitoring and food safety.

The Agricultural Internet of Things is a network of radios, antennas and sensors that gather real-time crop and soil information in the field. To facilitate data collection, these sensors and antennas are interconnected wirelessly with farm equipment. The Ag-IoT is a complete framework that can detect conditions on farmland, suggest actions in response and send commands to farm machinery.

Technologies that together comprise the Agricultural Internet of Things. Abdul Salam/Purdue University, CC BY-ND

Wireless data collection has the potential to help farmers use water much more efficiently, but putting these components in the ground creates challenges. For example, at the Purdue ENT Lab, we have found that when the antennas that transmit sensor data are buried in soil, their operating characteristics change drastically depending on how moist the soil is. My new book, “Signals in the Soil,” explains how this happens.

Abdul Salam takes measurements in a test bed at Purdue University to determine the optimum operating frequency for underground antennas. Abdul Salam, CC BY-ND

Farmers use heavy equipment in fields, so antennas must be buried deep enough to avoid damage. As soil becomes wet, the moisture affects communication between the sensor network and the control system. Water in the soil absorbs signal energy, which weakens the signals that the system sends. Denser soil also blocks signal transmission.

We have developed a theoretical model and an antenna that reduces the soil’s impact on underground communications by changing the operation frequency and system bandwidth. With this antenna, sensors placed in top layers of soil can provide real-time soil condition information to irrigation systems at distances up to 650 feet (200 meters) – longer than two football fields.

Another solution I have developed for improving wireless communication in soil is to use directional antennas to focus signal energy in a desired direction. Antennas that direct energy toward air can also be used for long-range wireless underground communications.

Using software-defined radios to detect soil measurement signals. These radios can adjust their operating frequencies in response to soil moisture changes. In actual operation, the radios are buried in the soil. Abdul Salam, CC BY-ND

What’s next for the Ag-IoT

Cybersecurity is becoming increasingly important for the Ag-IoT as it matures. Networks on farms need advanced security systems to protect the information that they transfer. There’s also a need for solutions that enable researchers and agricultural extension agents to merge information from multiple farms. Aggregating data this way will produce more accurate decisions about issues like water use, while preserving growers’ privacy.

These networks also need to adapt to changing local conditions, such as temperature, rainfall and wind. Seasonal changes and crop growth cycles can temporarily alter operating conditions for Ag-IoT equipment. By using cloud computing and machine learning, scientists can help the Ag-IoT respond to shifts in the environment around it.

Finally, lack of high-speed internet access is still an issue in many rural communities. For example, many researchers have integrated wireless underground sensors with Ag-IoT in center pivot irrigation systems, but farmers without high-speed internet access can’t install this kind of technology.

Integrating satellite-based network connectivity with the Ag-IoT can assist nonconnected farms where broadband connectivity is still unavailable. Researchers are also developing vehicle-mounted and mobile Ag-IoT platforms that use drones. Systems like these can provide continuous connectivity in the field, making digital technologies accessible for more farmers in more places.

US Federal Reserve officials tried to temper expectations for looser policy, and Neel Kashkari said at a conference on Wednesday that the Central Bank is a long way from declaring victory. Kashkari also added that the Central Bank’s proposal to cut interest rates early next year is unrealistic. In an interview with the Financial Times, San Francisco Fed President Mary Daly also warned that it is too early for the US Central Bank to “declare victory” in the fight against inflation. Amid such comments, stock indices fell slightly. At the close of the stock market yesterday, the Dow Jones Index (US30) added 0.08%, while the S&P 500 Index (US500) was down 0.07%. The NASDAQ Technology Index (US100) lost 0.58%.

The slowdown in US inflation may have opened the door for the Federal Reserve to soften the pace of the coming interest rate hikes, but policymakers left no doubt that they will continue to tighten monetary policy until price pressures are fully resolved. At this point, traders of federal funds futures contracts currently estimate a 66% chance of a 50 basis point hike and a 34% chance of a 75 basis point hike in September. Calling inflation “unacceptably high,” Chicago Fed President Charles Evans said he thinks the Fed will probably need to raise the rates to 3.25-3.5% this year and 3.75-4% by the end of next year.

Equity markets in Europe traded yesterday without a single dynamic. German DAX (DE30) decreased by 0.05%, French CAC 40 (FR40) added 0.33%, Spanish IBEX 35 (ES35) gained 0.33%, British FTSE 100 (UK100) was down by 0.55%.

European futures on gas exceeded $2350 per thousand cubic meters. Energy carriers are getting more expensive amid unprecedented heat waves in Europe. High temperatures caused unexpected strain on the region’s power grids, boosting the demand for electricity to power fans and air conditioners. Oil is in increasing demand in this environment as power plants seek alternatives to expensive gas. The International Energy Agency (IEA) raised its forecast for oil demand this year by 380,000 BPD. Normally, the IEA is negative on oil demand, but rising global natural gas prices may encourage more energy consumers to switch to oil for winter heating.

Meanwhile, the Organization of the Petroleum Exporting Countries (OPEC), which usually does its best to boost oil prices, has lowered its forecast for global oil demand growth for 2022. OPEC said it expects oil demand to grow by 3.1 million BPD in 2022, down 260,000 BPD from its previous forecast. Goldman Sachs analysts again forecast an oil price above $130 a barrel by the end of the year.

Gold futures closed lower Thursday as a three-week rally in the precious metal’s prices halted, and investors shifted their attention to the rising US stock market rather than safe-haven assets such as gold and the dollar.

The Latvian Saeima declared Russia a sponsor of terrorism. Earlier, the US Senate passed a resolution urging the State Department to recognize Russia as a state sponsor of terrorism because of the events in Ukraine, Chechnya, Georgia, and Syria. A ban on issuing Schengen visas to all Russians could be part of the seventh package of European sanctions against Russia. EU countries are now discussing the issue.

Asian markets were trading up yesterday. Japan’s Nikkei 225 (JP225) was not trading due to the bank holiday, Hong Kong’s Hang Seng (HK50) added 2.40%, while Australia’s S&P/ASX 200 (AU200) ended the day up by 1.12%. But Asian stocks started declining at the open on Friday amid a new blockage in China. China’s economy is still reeling from a series of economically devastating quarantine restrictions imposed earlier this year, and investors are wary of further such measures. Quarantine in a major commodity center such as Yiwu could cause further problems for China’s industrial sector, which unexpectedly contracted in July.

S&P 500 (F) (US500) 4,207.27 −2.97 (−0.071%)

Dow Jones (US30) 33,336.67 +27.16 (+0.082%)

DAX (DE40) 13,694.51 −6.42 (−0.047%)

FTSE 100 (UK100) 7,465.91 −41.20 (−0.55%)

USD Index 105.19 −0.01 (−0.01%)

Important events for today:

– UK GDP (m/m) at 09:00 (GMT+3);

– UK Industrial Production (m/m) at 09:00 (GMT+3);

– Eurozone Industrial Production (m/m) at 12:00 (GMT+3);

– US Michigan Consumer Sentiment (m/m) at 17:00 (GMT+3).

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

The Research Brief is a short take about interesting academic work.

The big idea

Women in statistics classes do better academically than men over a semester despite having more negative attitudes regarding their own abilities, according to our recent study in the Journal of Statistics and Data Science Education.

Using data from more than 100 male and female students from multiple statistics classes, my colleagueand I assessed gender differences in grades over the course of a semester. As part of the study, students also answered surveys at the start and end of the semester that measured six different things: their fear of statistics teachers in general; their thoughts about the usefulness of statistics; their perceptions of their own mathematical ability; their anxiety in taking tests; their anxiety in interpreting statistics; and their fear of asking for help.

Overall, we found that students with more negative perceptions of their own mathematical ability had lower grades over the course of the semester. What’s even more interesting are the gender differences that emerged.

Even though men and women scored similarly on exams at the start of the semester, women finished the semester with almost 10% higher final exam grades. This was the case even though women had significantly worse attitudes about their mathematical abilities at the start of the semester than their male counterparts.

At the beginning of the semester specifically, women were more likely to rate their mathematical abilities as lower than men in the class and report more anxiety toward exams and toward interpreting statistical findings. However, each of these self-assessments improved over the course of the semester such that women’s attitudes didn’t differ from men’s by the end.

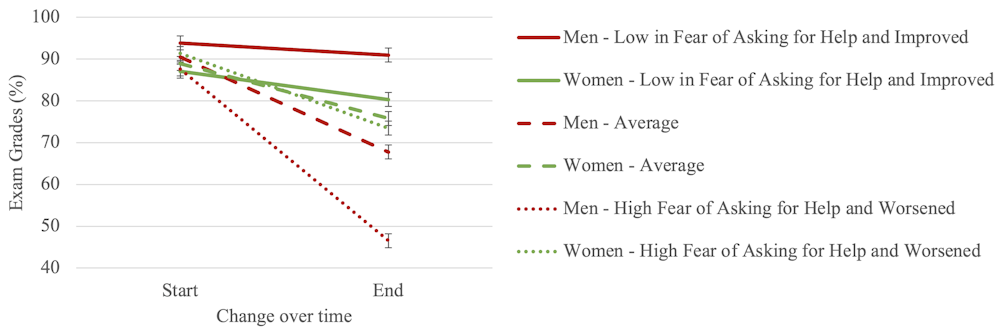

Meanwhile, the grades of male students who reported fear of statistics teachers or fear of asking for help decreased more sharply over the course of the semester. For men whose attitudes improved during the semester, grades also improved – though not as much as women’s grades improved.

Figure reflecting the effect of fear of asking for help and its change over time among women and men. Average grades decreased overall across the semester, likely because of coursework getting more challenging over time. Jonathan Santo, Author provided

The results from our study, in line with others, bolster the notion that women have the potential to do as well as men, and even better, in STEM fields, such as statistics. We contend that women would benefit from additional mentoring to encourage them as they begin pursuing STEM-related education.

Undergraduate students at the University of Nebraska Omaha collaborate on a group assignment for a STEM course. Derrick Nero, University of Nebraska Omaha, CC BY-NC-ND

What still isn’t known

The evidence above provides hints at some of the causes of the gender discrepancy in perceived ability. However, there is much we still don’t know.

For example, why did the attitudes of the women in our study improve over time? Was it based on their confidence in their abilities as their grades improved, or did their statistics teachers influence their perception of their own abilities over time?

More research is needed to understand exactly how women differed from men in their attitudes over the course of the school semester, among other questions. In particular, we’d like to disentangle exactly which classroom or instructor factors can lead to better attitudes among students, ultimately translating to better grades.

Speaker Nancy Pelosi’s visit to Taiwan has elicited a strong response from China: three days of simulated attack on Taiwan with further drills announced, plus a withdrawal from critical ongoing conversations with the US on climate change and the military.

This strong reaction was predictable. President Xi had earlier warned President Biden not “to play with fire”. Of course, if Pelosi’s visit hadn’t gone ahead, the Biden administration would have faced a strong reaction from both parties in Congress for not standing up to China’s threat to Taiwan or human rights issues regarding Tibet and Xinjiang, not to mention Hong Kong.

So where does it leave trade between the world’s two leading powers?

How business trumped ideology

Consider the not-too-distant past. The US supported the Republic of China against Japan in the Pacific war of 1941-45. When the Chinese leadership fled to Taiwan in 1949 following the victory of Mao Zedong’s communists in the Chinese civil war, Washington continued to recognise the exiled regime as China’s legitimate government, blocking the People’s Republic of China (PRC) from joining the United Nations.

This shifted in 1972 following President Nixon’s historic visit to China (in a move to isolate the Soviets). The US now recognised the PRC as China’s sole government and accepted its One China policy. It downgraded its Taiwan relations to merely informal, while affirming a peaceful settlement to the mainland communists’ claim that this was a breakaway province that had to be assimilated.

President Richard Nixon meeting Chairman Mao Zedong in Peking (Beijing) in 1972. manhhai, CC BY-SA

This opened US-China trade, ending a US trade embargo in place since the 1940s. Economic ties proliferated in the 1980s under Mao’s eventual successor, Deng Xiaoping, helping the Chinese economy to multiply while the US enjoyed lower consumer prices and a stronger stock market.

Western manufacturing firms either outsourced to Chinese firms or set up operations themselves. They benefited from cheaper production and – for those outsourcing – not having to own factories or deal with labour issues. In turn, the Chinese gained tremendous manufacturing capability.

As China’s middle class grew wealthier, the country became a major target consumer market for US firms such as Apple and GM. The Chinese authorities insisted this was done through local partner firms, transferring technology in the process and further enhancing the nation’s manufacturing know-how.

The growing Chinese threat

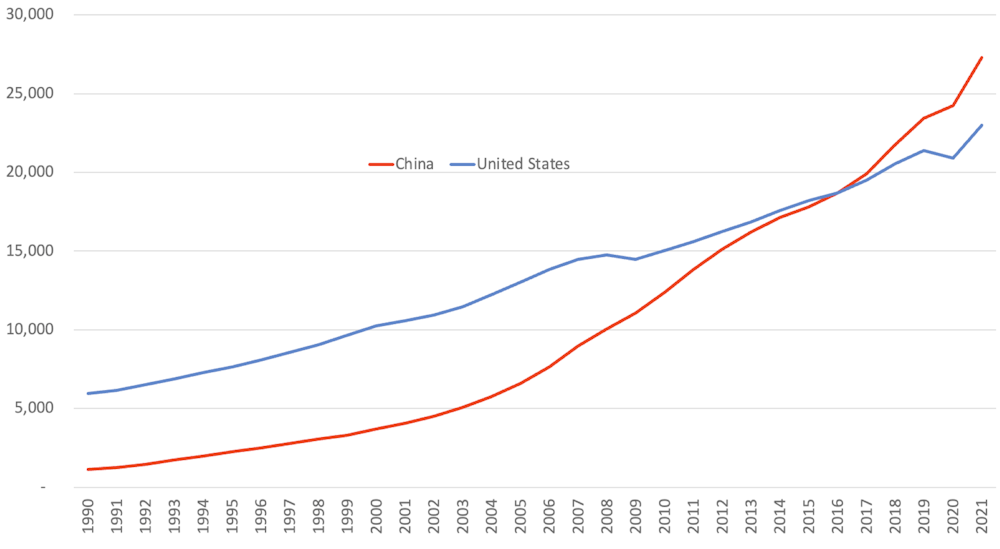

China and the US captured more than half the growth in GDP across the world from 1980 to 2020. US GDP grew nearly five times from US$4.4 trillion (£3.6 trillion) to US$20.9 trillion (£17.3 trillion) in today’s money, while China’s grew from US$310 billion to US$14.7 trillion.

China is now the second largest economy, although the IMF, World Bank and CIA consider it the largest once purchasing power is taken into account (see chart below). The US is still well ahead on per capita income (US$69,231 vs US$12,359 in 2021), though China’s is now that of a “developed” country, having lifted 800 million people out of poverty in the process.

The US has become increasingly concerned about China’s faster economic growth and the fact that the US buys much more from its rival than the other way around. This drove the big decline in US domestic manufacturing that famously helped Donald Trump to win the US presidency.

Chinese and US GDP based on purchasing power parity 1990-2021

World Bank

Equally, the rivalry has extended to other areas as China has sought a leading role on the world stage. Both nations are nuclear powers, although the Chinese military has only 350 nuclear warheads to America’s 5,500.

China has a larger navy, with some 360 battle force ships compared to the US 297, although China’s are mostly smaller – only three aircraft carriers compared to America’s 11, for example. The two countries are also competing in space to bring astronauts to the Moon and establish the first lunar base.

All this has threatened American dominance, while President Xi has also been much more forthright both domestically and internationally than any Chinese leader since Mao. The US has gradually become more hostile, starting with President Obama’s pivot towards other Asian nations in 2016 and then President Trump’s public complaints and eventual sanctioning of China’s “unfair” trade practices.

When President Biden took office in 2021, he began highlighting long-simmering complaints about human rights issues in Xinjiang and the threat to Taiwan (while still endorsing the One China Policy). He also imposed sanctions on certain Chinese companies of a kind not been seen since the Mao-era trade embargo.

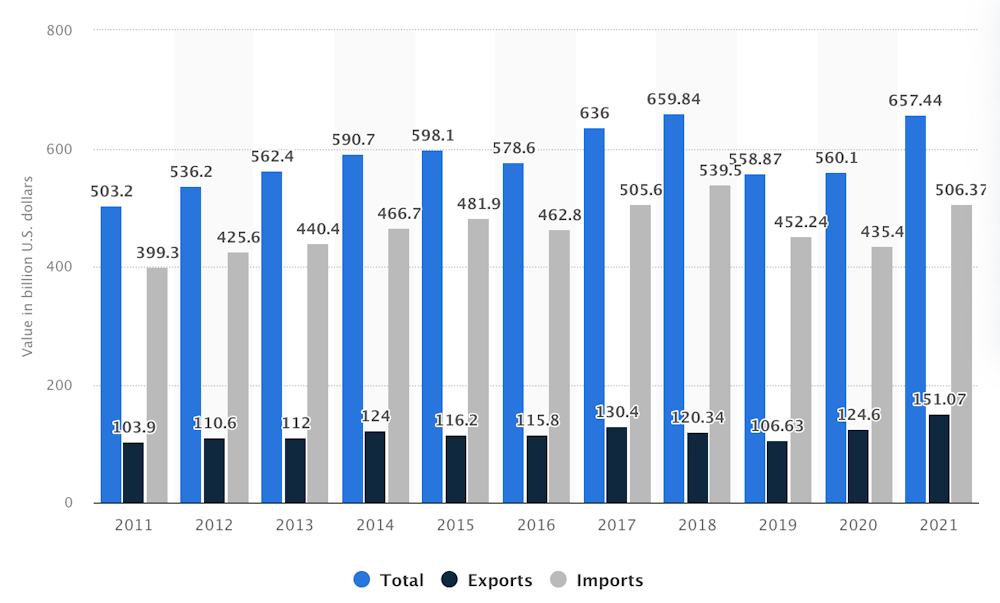

US trade in goods to China 2011-21

Note the US trade in services to China is about one-tenth that of goods. In 2020 the US exported US$40 billion in services to China and imported US$16 billion. Statista

Biden also banned goods from China’s Xinjiang region on the grounds of forced labour in 2022, affecting the purchasing of goods by many western companies. China reportedly moved workers to other parts of the country to enable western companies to keep purchasing.

Bipolarity is back

COVID-19 further increased the distance between the two countries. After China’s zero COVID policy helped to disrupt supply chains and cause product shortages, the Biden administration began calling for reduced dependency on its rival.

US firms have duly been restructuring their supply chains. In June, Apple moved some iPad production from China to Vietnam, albeit also because of growing demand in south-east Asia.

Near-shoring to Mexico is gaining momentum. Apple manufacturers Foxconn and Pegatron are considering producing iPhones for North America in Mexico rather than China to take advantage of lower labour costs and the free-trade agreement between the US and Mexico.

Two global blocs are increasingly emerging, with US treasury secretary Janet Yellen in April calling for “friend-shoring” with trusted partners, dividing countries into friends or foes. The Biden administration announced at the June G7 meeting a new “Partnership for Global Infrastructure and Investment”. Aiming to mobilise US$600 billion in investments over five years, this is an overture to various developing countries already being courted by China under its similar Belt and Road Initiative.

Days earlier, China had hosted the annual BRICS summit, which includes Brazil, Russia, India and South Africa. It welcomed leaders from 13 other countries: Algeria, Argentina, Egypt, Indonesia, Iran, Kazakhstan, Senegal, Uzbekistan, Cambodia, Ethiopia, Fiji, Malaysia and Thailand. Xi urged the summit to build a “global community of security” based on multilateral cooperation. Iran and Argentina have since applied to join the bloc.

We are already seeing what bipolarity will mean for vital components and commodities. In nanochips, the US is leading a “chips 4” pact with Japan, Taiwan and possible South Korea to develop next-generation technologies and manufacturing capacity. China is investing US$1.4 trillion between 2020 and 2025 in a bid to become self-reliant in this technology.

Another big issue is cobalt, which is essential for making lithium batteries for electric vehicles. To secure supply from the Democratic Republic of the Congo, which produces 70% of world reserves, China has navigated Congolese politics, lobbying powerful politicians in mining regions. By 2020, Chinese firms owned or had a stake in 15 of the DRC’s 19 cobalt-producing mines.

As China hoards cobalt supplies, the US seeks alternatives. GM is developing its Ultium battery cell, which needs 70% less cobalt than today’s batteries, while Oak Ridge National Laboratory is developing a battery that doesn’t need the metal at all.

Silver linings

As US-China relations have moved from building bridges in 1972 to building walls in 2022, countries will increasingly be forced to choose sides and companies will have to plan supply chains accordingly. Those seeking to trade in both blocs will need to “divisionalise”, running parallel operations.

American companies wanting to serve Chinese consumers will still need to manufacture in China or other nations within that bloc, while Chinese companies will need to do the same in reverse. Interestingly, Chinese companies have been rapidly buying farmland and agriculture-based companies in the US and elsewhere.

Yet though the new supply chains will almost certainly increase costs for western consumers and dampen China’s growth, there will be benefits. Supply chains should be more resilient to future crises and also more transparent, while reduced transportation (and reliance on Chinese coal) should cut carbon emissions. This should help to meet the UN Sustainable Development Goals on environmental and social sustainability.

The cobalt and nanochips examples also show how the US-China rivalry is catalysing innovation. And importantly, global trade will continue growing as countries depend on each other, even as trade links change.

It will certainly take time to find an equilibrium. It took years for the USSR and US to figure out how to co-exist without getting into direct military conflict. Hillary Clinton wrote in 2011 as Secretary of State that “there is no handbook for the evolving US-China relationship”, and that remains the case today.

At any rate, the businesses that thrive in this new environment will likely be those that plan for a divided world with divisional supply chains. The recent Taiwan row will probably not lead to direct military conflict; rather it will reinforce a trend that has been gathering momentum for a decade or more.

The US stock market rose Wednesday after the release of inflation data for July, which showed that price pressures eased. The overall Consumer Price Index for July was 8.5%, down from the 8.7% expected by economists. Investors now see a 50 basis point rate hike as the most likely scenario for the Federal Reserve’s September meeting. Stock indices jumped sharply on the news, while the dollar index saw its biggest one-day drop in 5 months. As the stock market closed yesterday, the Dow Jones Index (US30) increased by 1.63%, while the S&P 500 Index (US500) added 2.13%. The NASDAQ Technology Index (US100) jumped by 2.89%.

Most of the decline in inflation in July was due to the drop in gasoline prices, which fell by 7.7% for the month. Other categories also saw significant declines, including prices of airline tickets, used cars and trucks, and clothing. On the other hand, some analysts are inclined to think that markets have overreacted positively to the slowdown in inflation because the Fed is still in a cycle of raising rates and will begin cutting the balance sheet next month. Also, according to a new Bloomberg Economics model, inflation in the US now consists of four factors: supply, demand, energy prices, and monetary policy. This model showed that lower energy costs and a tougher Fed stance were the main factors behind the slowdown to 8.5% last month. At the same time, rising demand combined with supply constraints continued to put upward pressure on inflation.

Equity markets in Europe were also up yesterday. Germany’s DAX (DE30) gained 1.23%, France’s CAC 40 (FR40) added 0.52%, Spain’s IBEX 35 (ES35) added 0.49%, and Britain’s FTSE 100 (UK100) closed up by 0.25%.

The US Energy Information Administration reported a second straight week of five million barrels increase in crude oil inventories. But the agency also mentioned that gasoline inventories fell by about five million barrels, which helped offset the bearish sentiment hanging over the market. A lower dollar on the back of slowing inflation led to a rise in oil prices. But there is a vicious circle here that many do not notice. Inflation in the US has slowed due to falling oil and gasoline prices. This caused the dollar index to fall, causing oil prices to rise again. Thus, if the dollar index continues to decline, oil prices will continue to rise, which will have the opposite effect and cause a new acceleration of inflation in the US.

Gold hit a 5-week high on declining US inflation. Gold has an inverse correlation to the dollar index and government bond yields, which fell sharply yesterday after the CPI data. But it should be noted that usually, in a cycle of monetary tightening through higher interest rates, the national currency and government bond yields rise.

Asian markets traded lower yesterday. Japan’s Nikkei 225 (JP225) decreased by 0.65%, Hong Kong’s Hang Seng (HK50) fell by 1.96%, and Australia’s S&P/ASX 200 (AU200) ended the day down by 0.53%.

The Reserve Bank of New Zealand will likely raise its rate by another 50 basis points in August. Nevertheless, the deteriorating economic picture and rapidly falling home prices suggest that investors may see a downward revision to the interest rate trajectory forecast. As the RBNZ is increasingly seen as a test case for other central banks, global markets will be watching closely for any dovish bias from the bank.

S&P 500 (F) (US500) 4,210.23 +87.76 (+2.13%)

Dow Jones (US30) 33,309.84 +535.43 (+1.63%)

DAX (DE40) 13,700.93 +165.96 (+1.23%)

FTSE 100 (UK100) 7,507.11 +18.96 (+0.25%)

USD Index 106.21 −1.16 (−1.09%)

Important events for today:

– US Producer Price Index (m/m) at 15:30 (GMT+3);

– US Initial Jobless Claims (w/w) at 15:30 (GMT+3);

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

The US stock indices were trading lower yesterday ahead of the inflation data, indicating that investors were probably closing their positions before the important report. At the close of the stock market yesterday, the Dow Jones Index (US30) decreased by 0.18%, and the S&P 500 Index (US500) was down 0.42%. The NASDAQ Technology Index (US100) fell by 1.19%.

The Fed’s balance sheet reduction plan, known as quantitative tightening (QT), will begin in full force in September. The Fed will begin reducing the balance sheet with $95 billion monthly cuts ($60 billion in Treasuries and $35 billion in mortgage-backed securities). But analysts believe the US Central Bank will have to wind down some of its aggressive monetary tightenings as early as next year as it begins cutting rates to fight the economic downturn. Bank of America estimates that if the Fed pauses QT in September 2023, the Treasury will probably have $630 billion less debt for the public in the fiscal year 2024. Fed Chairman Jerome Powell said last month that the Central Bank’s model “Suggests that it could take two to two and a half years” for the balance sheet to come to a “New equilibrium.” The balance sheet more than doubled during the pandemic, to $9 trillion earlier this year, as the Fed again used quantitative easing as a crisis-fighting tool. But there is an alternative view. Some analysts believe the US Fed will have to raise rates to 5% in 2023 and stay at that level because of tight inflation to get room to lower interest rates in 2024 and again resort to increasing the balance sheet by turning on the printing machine.

Micron Technology (MU) projected negative free cash flow in the second quarter due to falling revenue as lower PC and video game sales are expected to impact chip demand. The company’s stock is down more than 4%. Norwegian Cruise Line (NCLH) reported second-quarter results that fell short of Wall Street expectations and provided gloomy forecasts, predicting that occupancy levels won’t return to pre-pandemic levels until next year. Rival Royal Caribbean Cruises (RCL) and Carnival (CCL) are down more than 5%.

Tesla CEO Elon Musk sold $6.9 billion of Tesla stock, citing the high likelihood of a forced deal with Twitter. Musk broke off an April 25 agreement to buy Twitter for $44 billion in early July. Twitter sued Musk to force him to complete the transaction, dismissing his claim that he had been misled about the number of spam accounts on the social media platform. Both parties will appear in court on October 17.

Stock markets in Europe traded flat on Tuesday. Yesterday German DAX (DE30) fell by 1.12%, French CAC 40 (FR40) lost 0.53%, Spanish IBEX 35 (ES35) gained 0.48%, British FTSE 100 (UK100) closed on the plus side by 0.07%.

A famous German aluminum factory is preparing to shut down due to the growing gas crisis in Europe. Costs have doubled this year, causing the plant to idle one week a month to save gas. The price of gas contracts for Europe has nearly tripled since the beginning of the year due to Russia’s invasion of Ukraine, sanctions against Russia, a slowdown in Russian gas supplies through Nord Stream 1, and global market tensions. Germany’s energy regulator is urging companies, the government, and consumers to reduce gas consumption and has asked major firms to submit contingency plans to reduce consumption during the winter further.

Gold prices are strengthening ahead of a key inflation report. Gold is getting support as a safe-haven asset as stock indices decline along with the Dollar Index. Investors expect a decline in the rate of inflation in today’s report. But if the data is worse than expected, the dollar index could get a boost, negatively affecting the prices of precious metals.

Oil prices fell on Tuesday as market participants compared last week’s potential stockpiling in the US with news that exports of some oil via the “Druzhba” pipeline from Russia to Europe, which runs through Ukraine, have been halted. Russian pipeline monopoly Transneft said Ukraine had suspended crude through the pipeline because Western sanctions prevented Moscow from paying transit fees. The news, however, was offset by reports of new progress in nuclear talks with Iran, which could bring 500,000 to one million barrels a day to the market if Tehran frees itself from sanctions imposed on its oil over its suspected nuclear weapons development.

Asian markets traded flat yesterday. Japan’s Nikkei 225 (JP225) fell by 0.88%, Hong Kong’s Hang Seng (HK50) lost 0.21%, and Australia’s S&P/ASX 200 (AU200) was up by 0.13% by the end of the day.

China’s annual Consumer Price Index was slightly lower than expected at 2.7% instead of 2.5%. Meanwhile, the Producer Price Index, which shows the factory inflation rate, fell sharply from 6.1% to 4.2%. The easing of price pressures in China may reflect the sluggish performance of the domestic economy due to continued Covid-19 lockdowns in major commercial centers hampering activity.

S&P 500 (F) (US500) 4,122.47 −17.59 (−0.42%)

Dow Jones (US30) 32,774.41 −58.13 (−0.18%)

DAX (DE40) 13,534.97 −152.72 (−1.12%)

FTSE 100 (UK100) 7,488.15 +5.78 (+0.077%)

USD Index 106.32 −0.12 (−0.11%)

Important events for today:

– Japan Producer Price Index (m/m) at 02:50 (GMT+3);

– China Consumer Price Index (m/m) at 04:30 (GMT+3);

– China Producer Price Index (m/m) at 04:30 (GMT+3);

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

The US stock indices traded mixed on Monday. By the close of trading, the Dow Jones index (US30) increased by 0.09%, while the S&P 500 (US500) decreased by 0.12%. The NASDAQ Technology Index (US100) lost 0.10% yesterday.

Tesla (TSLA) added 1%, driving consumer stocks higher as sentiment about electric vehicles was boosted by a new climate bill passed by the US Senate over the weekend. It includes nearly $400 billion over a 10-year period to fund energy-related programs and expand and improve existing tax credits for electric vehicles.

Nvidia Corporation (NVDA) fell more than 8% after the chip maker reported second-quarter revenue of $6.7 billion, well below its estimate of $8.1 billion, with the company lowering its revenue forecast for the third quarter.

In the US, consumer confidence in the housing market fell to its lowest level since 2011 as both prospective buyers and sellers became more pessimistic. According to Fannie Mae’s monthly survey, only 17% of those surveyed in July said it was a good time to buy a home, down from 20% in June.

Stock markets in Europe mostly rose on Monday. Germany’s DAX (DE30) gained 0.84%, France’s CAC 40 (FR40) added 0.80%, Spain’s IBEX 35 (ES35) jumped by 1.28%, and the British FTSE 100 (UK100) closed higher by 0.57% yesterday.

Britain’s largest electricity distributor said that the damages of 280 million pounds sterling from the bankruptcy of energy companies would be shifted to consumers.

Yesterday, the German government spokesman said that Germany faces difficult months, but the country supports Ukraine and sanctions against Russia.

Goldman Sachs analysts said they believe the case for higher oil prices remains strong as the market faces larger shortages than they expected in recent months.

Gold prices maintained their recent gains as volatility in stock markets ahead of this week’s US inflation data boosted demand for the yellow metal. Gold and silver prices are inversely correlated with the dollar index and US government bond yields. Therefore, a decline in the dollar is usually accompanied by a rise in gold prices and vice versa. The focus now is on US consumer price data for July, which will be published on Wednesday. Analysts expect inflation to likely remain at a 40-year high in the coming months, necessitating further monetary tightening by the Fed. An unexpected rise in CPI could push up the dollar index and yields, negatively impacting gold and silver prices.

Asian markets traded flat yesterday. Japan’s Nikkei 225 (JP225) gained 1.26%, Hong Kong’s Hang Seng (HK50) was down by 0.77%, and Australia’s S&P/ASX 200 (AU200) added 0.07%.

Tensions between China and Taiwan eased slightly after China announced the end of military exercises around the island. At the same time, Taiwan’s defense ministry said Chinese planes and ships never entered Taiwan’s territorial waters.

The NAB Australia Business Confidence Index showed that inflationary pressures continue to rise, indicating that inflation has not yet peaked. But business activity remains strong despite global and domestic economic headwinds. Analysts believe the strong economic data will allow the RBA to raise interest rates another 0.5% at its next meeting on September 6.

S&P 500 (F) (US500) 4,140.06 −5.13 (−0.12%)

Dow Jones (US30) 32,832.54 +29.07 (+0.089%)

DAX (DE40) 13,687.69 +113.76 (+0.84%)

FTSE 100 (UK100) 7,482.37 +42.63 (+0.57%)

USD Index 106.41 −0.21 (−0.20%)

Important events for today:

– Australia NAB Business Confidence (m/m) at 04:30 (GMT+3).

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.

Asian shares struggled for direction this morning as concerns about inflation and the outlook for economic growth weighed on sentiment. Overnight, Wall Street’s main indices were mostly flat with a sales warning from Nvidia dragging down the tech sector. In Europe, stocks are expected to open lower due to the growing caution ahead of the US inflation report on Wednesday.

Looking at currencies, king dollar has retreated from recent highs while EUR/USD is trading around the sticky 1.02 level. Gold seems to be waiting for a fresh fundamental spark while oil prices are under pressure as OPEC’s monthly report and EIA data loom.

On the data front, Australian consumer sentiment slumped in August thanks to the horrible combination of soaring inflation, rising interest rates, and gloomy outlook on living costs. This marks the ninth consecutive month that sentiment has stayed negative.

Will US Inflation report spark fireworks?

The main risk event and potential market shaker this week will be the latest US inflation figures published on Wednesday. After accelerating by 9.1% in June, markets are forecasting a cooling in July annual inflation to 8.7%. Should expectations match reality, this could be a breath of fresh air for financial markets and fuel optimism around inflation plateauing. Given how markets remain obsessive and incredibly reactive to any topic relating to rising prices, explosive levels of volatility could be on the cards.

If US consumer prices defy market expectations by rising again, this is likely to reinforce expectations around the Fed hiking rates by another 75 basis points in September. According to Bloomberg, traders are currently pricing in this scenario with around a 74% probability.

Alternatively, if the inflation report meets or misses expectations, this could raise hopes over consumer prices peaking. Such a development could encourage the Fed to step back from its aggressive approach toward hiking rates, which could send the dollar tumbling and Treasury yields declining.

Commodity spotlight – Gold

Gold was able to recover from last Friday’s selloff after the strong jobs report cooled recession fears and fortified expectations for more aggressive Fed rate hikes. Bulls wasted little time in clawing back the post-NFP losses yesterday with prices trading around $1785.50 as of writing.

Although buyers have been in the driving seat for the past three weeks, the pending US CPI report could shift the balance of power between bulls and bears. A strong inflation report could deal zero-yielding gold a heavy blow as aggressive rate hike bets jump. Alternatively, a weak report may provide the precious metal an opportunity to push higher.

Looking at things from a technical perspective, there are a couple of tough resistance levels that bulls may face down the road. The first one is around $1785 where the 50-day SMA resides and $1830, a key point just below the 100 and 200-day Simple Moving Average. If bears end up dominating the scene, prices may sink back towards $1752 and $1724.

Undergraduate students at the University of Nebraska Omaha collaborate on a group assignment for a STEM course.

Undergraduate students at the University of Nebraska Omaha collaborate on a group assignment for a STEM course.