By JustForex

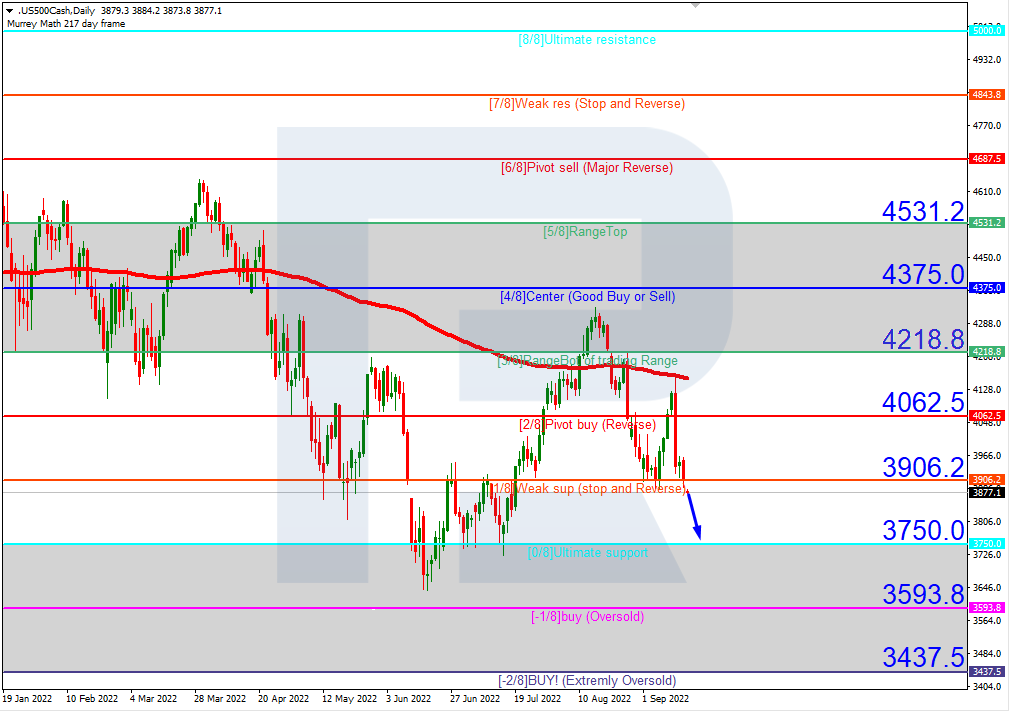

Asset prices around the world fell sharply on Friday as central banks and governments stepped up their fight against inflation. At the close of the stock market on Friday, the Dow Jones Index (US30) decreased by 1.42% (-3.69% for the week) and the S&P 500 Index (US500) fell by 1.72% (-4.07% for the week). Technology index, NASDAQ (US100) lost 0.82% on Friday (-5.92% for the week).

Goldman Sachs strategists Friday lowered their year-end target for the benchmark S&P 500 US stock index to 3600 from 4300. Because monetary policy tends to lag, analysts estimate that the renewed aggressiveness by central banks means the global economy will become even weaker by the middle of next year. The Fed’s latest economic forecasts, released Wednesday along with a massive third straight 75 basis point interest rate hike, show that the Central Bank expects the nation’s unemployment rate to rise to 4.4% next year – up from 3.7% in August. Assuming the labor force remains unchanged, that would mean about 1.2 million people would be out of work. Analysts believe that Fed Chairman Jerome Powell has triggered an emotional bear market phase by endorsing the idea of a recession.

Analysts now dismiss the option that the recession will be short and shallow. Experts are now predicting much tighter monetary policy from central banks and other unintended consequences. The question now is already how deep the recession will be and whether the economy can face any form of financial crisis and a serious global liquidity shock. The US benchmark 10-year Treasury bond yields have reached their highest level in more than 12 years, while German two-year bond yields have exceeded 2% for the first time since late 2008. In the UK, five-year bonds jumped by 50 bps, the biggest one-day jump since late 1991.

Canadian retail sales fell by 2.5% to $61.3 billion in July, the first decline in seven months. Sales fell in 9 of 11 sub-industries, representing 94.5% of retail sales.

Stock markets in Europe were mostly down on Friday. German DAX (DE30) fell by 1.97% (-3.16% for the week), French CAC 40 (FR 40) decreased by 2.28% (-4.39% for the week), Spanish IBEX 35 (ES35) lost 2.46% (-4.68% for the week). British FTSE 100 (UK100) was 1.97% negative (-3.62% for the week).

The manufacturing PMI fell to a low in almost all economies of the region except France. These are clear signs of an impending recession in Europe.

In the UK, recession risks are also rising as the PMI business activity index signals a deepening recession. Companies report that the rising cost of living associated with the energy crisis and growing concerns about the outlook are suppressing demand and reducing output. Renewed supply constraints, soaring energy prices, and the rising cost of imports associated with the weakening pound exacerbate rising price pressures. The British pound and stock indexes fell sharply on Friday after the country’s finance minister announced historic tax cuts and a huge increase in borrowing. Investors are turning away from British bonds amid an expected increase in government debt. According to Bloomberg, analysts expect UK interest rates to reach 5.2% in August 2023, with growing expectations that the Bank of England may raise interest rates by one percentage point at its next meeting in November.

Italians are heading to the polls for a national vote that could bring back the country’s first female prime minister and first far-right-led government since the end of World War II. Incumbent President Mario Draghi, who was kicked out in July because of political strife, has agreed to stay as a caretaker.

Gold remains under pressure because of the rising US dollar index and US government bond yields. As long as the US Federal Reserve follows an aggressive tightening policy, precious metals will have no fundamental reason to rise.

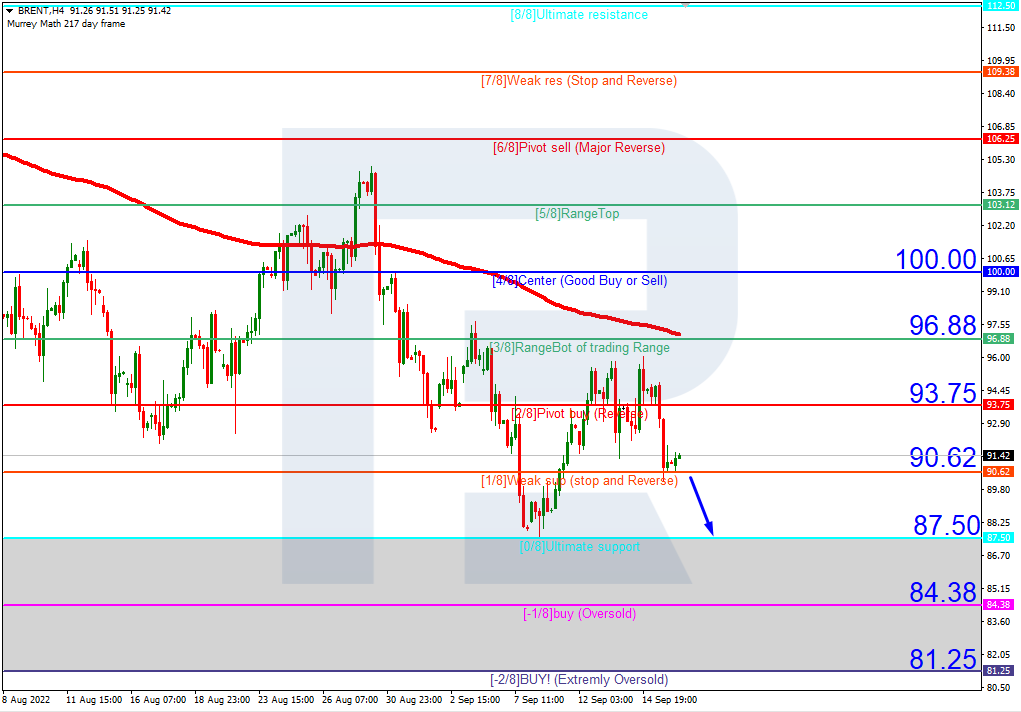

Oil prices fell more than 5% to an eight-month low Friday as the US dollar hit its strongest level in more than two decades and fears that rising interest rates will lead to a recession in major economies, reducing demand for oil. As fears of global growth have turned to panic mode, this will weaken both economic activity and the short-term outlook for oil demand.

Asian markets traded lower last week. Japan’s Nikkei 225 (JP225) decreased by 2.58% for the week, Hong Kong’s Hang Seng (HK50) ended last week down by 4.08%, and Australia’s S&P/ASX 200 (AU200) ended the week in minus 3.92%.

The Chinese yuan finished the trading session at an almost 28-month low as the widening yield gap between the two largest economies in the world continues to put pressure on the Chinese currency.

In the commodities market, futures on orange juice (+6.43%), coffee (+2.32%), and wheat (+2.01%) showed the biggest gains by the end of the week. Natural gas futures (-11.89%), lumber (-9.6%), cotton (-6.8%), WTI oil (-6.29%), platinum (-5.34%), Brent oil (-5.15%), copper (-4.78%), silver (-2.82%) and gold (-1.89%) showed the biggest drop.

S&P 500 (F) (US500) 3,693.23 −64.76 (−1.72%)

Dow Jones (US30) 29,590.41 −486.27 (−1.62%)

DAX (DE40) 12,284.19 −247.44 (−1.97%)

FTSE 100 (UK100) 7,018.60 −140.92 (−1.97%)

USD Index 113.02 +1.67 (+1.50%)

- – Japan Manufacturing PMI (m/m) at 03:30 (GMT+3);

- – Japan Services PMI (m/m) at 03:30 (GMT+3);

- – Japan BoJ Governor Kuroda Speaks at 08:35 (GMT+3);

- – Eurozone German GDP (q/q) at 09:00 (GMT+3);

- – Eurozone German IFO Business Climate (m/m) at 11:00 (GMT+3);

- – Eurozone ECB President Lagarde Speaks at 16:00 (GMT+3);

- – US FOMC Member Mester Speaks at 23:00 (GMT+3).

By JustForex

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.