By Han Tan Chief Market Analyst at Exinity Group, ForexTime

The first Friday of every month brings the highly-anticipated US nonfarm payrolls data. Here are some of the other potential market-moving events scheduled for the first trading week of August:

Monday, August 2

- Manufacturing PMIs for China, Eurozone, UK, US

- US ISM manufacturing

Tuesday, August 3

- RBA policy decision

- Eurozone PPI

- Alibaba earnings

Wednesday, August 4

- Eurozone retail sales

- Composite/services PMIs for China, Eurozone, UK, US

- EIA crude oil inventory report

Thursday, August 5

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

- BOE rate decision

- Germany factory orders

- US initial jobless claims

Friday, August 6

- Germany industrial production

- US nonfarm payrolls

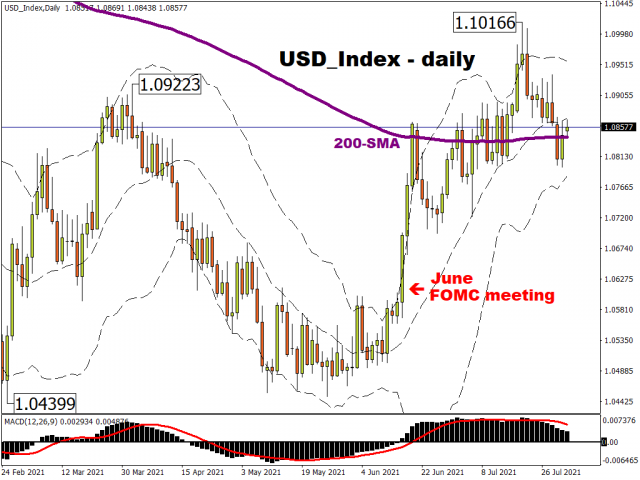

For the US nonfarm payrolls print that’s due on 6 August, markets are forecasting that 900,000 jobs were added last month. Anything higher than 850,000 would be the highest NFP print since August 2020 and would score a third consecutive month of faster jobs growth.

A larger-than-expected July jobs increase (think closer to one million jobs added) could translate into more upside for the equally-weighted US dollar index, and put it on a path back towards its year-to-date high.

Otherwise, a lacklustre print this Friday could ensure that this dollar index remains below its 200-day simple moving average for a while longer and pare more of its gains since the hawkish surprise at the June FOMC meeting.

Markets still guided by Fed’s tapering predictions

Arguably, the biggest theme in play across global financial markets right now is the predictions over the Fed’s tapering.

Considering the robust US economic recovery, the US central bank is expected to ease up on its bond purchases that have supported financial markets since the pandemic. Exactly when the Fed will embark on such a process, at what pace (how quickly it will unwind its bond purchases), and under what economic conditions – all those remain vague at this point in time.

What we do know is that, following last week’s July FOMC meeting, the Fed reiterated that it wants to see “substantial further progress” in the ongoing US economic recovery before it will taper. However, it remains unknown exactly what constitutes “substantial” enough for the Fed.

Conflicting tapering cues within FOMC and markets

This past Friday (30 July), Fed Governor Lael Brainard reminded global investors that the US jobs market is still a long way off from pre-pandemic levels. She highlighted the “shortfall of 6.8 million jobs” that needs to be restored before the Fed tapers.

On the other hand, there was the famed hawk, Federal Reserve Bank of St. Louis President James Bullard, who also on Friday expressed his desire for the tapering to begin this fall and wrapped up by March 2022. Most economists expect the tapering to only commence next year.

Amidst all these conflicting views, it remains to be seen how the forthcoming economic data guides, not just the consensus within the FOMC, but also investors’ predictions for when the tapering will actually commence.

‘Markets Extra’ podcast: Confused by the Fed? So were markets.

More gains for stocks likely until tapering draws closer

As long as the Fed’s ultra-accommodative stance remains intact, that should allow for more upside for US equities in the interim. The S&P 500 is striving to carve out a sustainable presence above the psychologically-important 4400 mark, a feat made more achievable considering that bond yields have been relatively subdued of late.

However, a stellar US jobs report this Friday would shorten the runway for equity bulls, as an NFP print that far exceeds the media forecast (900k) would ramp up markets expectations that the Fed would have to ditch its dovish stance sooner rather than later.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- Your Bourse and FXPRIMUS Bring 24/7 Synthetic Indices to the Global Broker Market Jun 16, 2026

- Institutional investors continue to reduce their presence in metals Jun 16, 2026

- USDJPY Driven by Emotions: Bank of Japan Raises Rate to Highest Level Since 1995 Jun 16, 2026

- The United States and Iran have signed a peace agreement – oil has fallen to 80 dollars per barrel. Jun 15, 2026

- EURUSD Ahead of the New Week: Expecting High Volatility Jun 15, 2026

- COT Metals Charts: Speculator Bets led by Steel Jun 14, 2026

- COT Bonds Charts: Speculator Bets led by 2-Year Bonds & Ultra 10-Year Bonds Jun 14, 2026

- COT Energy Charts: Speculator Bets led by Brent Oil Jun 14, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led lower by Corn and Soybean Meal Jun 14, 2026

- Today investors’ focus is directed at the historic IPO of SpaceX Jun 12, 2026