By Daniel Flaim, Managing Director, North America Interest Rate Derivatives

New York, New York | May 18, 2023 – It is officially the end of the line for LIBOR. After some 30+ years as “the world’s most important number,” and the last six years on an extended farewell tour, the London Interbank Offered Rate will officially be retired as a benchmark for U.S. dollar swaps transactions. CME Group completed its conversion to the Secured Overnight Financing Rate (SOFR) as the standard benchmark reference for over-the-counter (OTC) derivatives trades in April and LCH will complete its conversion containing U.S. dollar LIBOR vs. fixed interest rate swaps on May 20. By June, roughly $60 trillion in U.S. dollar contracts will be secured to SOFR.

Regulators first announced plans to phase out LIBOR in 2017, ushering in a protracted death march that saw the slow-but-steady migration away from the decades-old benchmark. Ultimately, the Alternative Reference Rates Committee (ARRC) selected SOFR as the overnight benchmark rate to use in certain new U.S. dollar derivatives and financial contracts, and the financial industry—including regulators, central banks, trading venues and other market participants—have spent the last several years getting ready for the transition.

Over the course of that multi-year migration, we’ve learned some important lessons:

Big and complicated problems can be solved when the industry sets its collective mind to something. This transition was no small feat but market participants and regulators quickly rallied together to organize and coordinate efforts ahead of upcoming target deadlines. The end result was a relatively smooth process thanks to solid preparation, decisive action and regular communications.

January 2022 was the moment of reckoning. Migration away from LIBOR was slow and steady before taking a drastic turn ahead of the January 2022 deadline for no new LIBOR origination. By February 2022, SOFR trading on Tradeweb made up 72% of all new risk, and across our business approximately 96% of our most active clients globally trading USD swaps were using SOFR.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

This playbook can be utilized elsewhere. We have been pleased to see that the insights and lessons learned from the U.S. dollar LIBOR transition have already extended beyond our markets and into non-LIBOR jurisdictions, further illustrating the permanent impact this movement has had on our global markets.

Why LIBOR Was So Entrenched

Getting there was no small achievement. LIBOR didn’t earn its reputation as “the world’s most important number” for nothing. As the benchmark evolved over the last three decades, it’s been sliced and diced into multiple durations and both backward-looking and forward-looking rates that are used for everything from projecting market expectations for the cost of borrowing to the underlying benchmark for U.S. dollar swaps contracts. Financial technology also grew up around LIBOR, with virtually every piece of financial services software and nearly every financial model incorporating some link to the benchmark.

Thankfully, due to close collaboration between industry stakeholders including trading platforms, dealers and clients, clearinghouses and operators of order management systems, over the course of the transition period, this final step in the migration from LIBOR to SOFR in the swaps market is anticipated to be a smooth one.

Orderly Transition to a New Standard

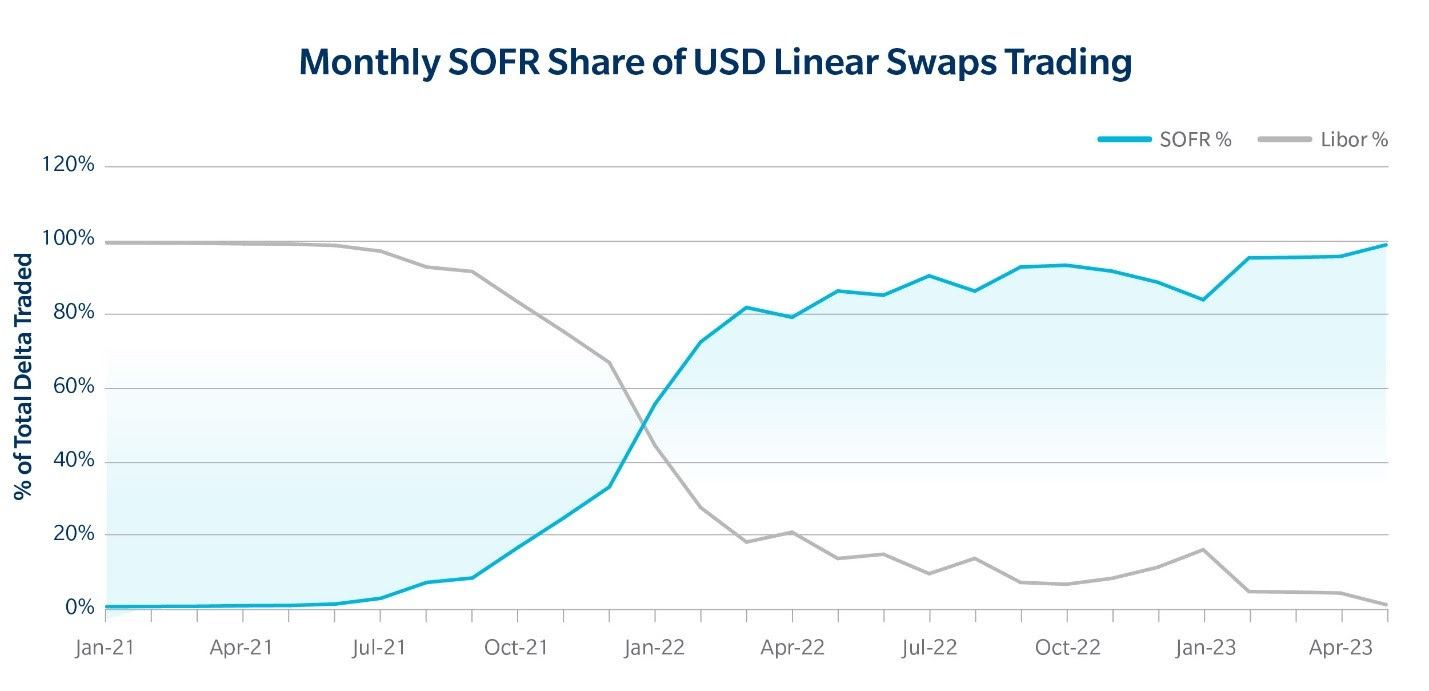

In fact, much of the heavy lifting has already been done. As indicated in the chart below, the percentage of new U.S. dollar swaps trades benchmarked to SOFR and executed on the Tradeweb platform started to trend upward in August of 2021. That date followed the Commodity Futures Trading Commission’s (CFTC) Market Risk Advisory Committee (MRAC) SOFR First recommendation, which introduced a phased approach to the SOFR transition. In the following months, SOFR trading activity on the Tradeweb platform increased as clients began to offset their existing U.S. dollar LIBOR risk, with new SOFR activity reaching parity with LIBOR by January 2022, in response to the upcoming deadline which imposed restrictions on new use of U.S. dollar LIBOR. By February 2022, trading volume benchmarked to SOFR on the Tradeweb platform increased over 50% versus the previous month. In 2022 alone, we had nearly $21 trillion traded in SOFR on the platform.

Source: TW SEF, % of Delta, excluding basis and inflation swaps

Together, the steady forward march toward SOFR adoption for new trades, along with the industry’s diligent efforts to smooth the migration of existing contracts benchmarked to LIBOR, has helped pave the way for an incredibly orderly transition.

Following the success of the LIBOR transition in the U.S. dollar market, we’ve seen similar work being done in non-LIBOR jurisdictions, including Canada. Led by the Canadian Alternative Reference Rate Committee (CARR), Canada is shifting away from the benchmark Canadian Dollar Offered Rate (CDOR) to Canadian Overnight Repo Rate Average (CORRA) as the key Canadian interest rate benchmark. Globally, the LIBOR transition has served as a shining example of industry collaboration overcoming institutional inertia and debunking the myth that things need to be done a certain way just because that’s how they’ve always been done.

It took six years and there was no shortage of doubt and concern along the way, but the transition that the New York Federal Reserve called “arguably one of the most significant and complex challenges that financial markets will ever confront,” is about to be complete. It should come as a cause for celebration to the countless market participants who weren’t afraid to tweak the process, experiment with new standards and collaborate with peers to transform and modernize critical market infrastructure.

Now, as a result of this effort by so many parties, our markets are running smoothly and efficiently and we have proven once again how resilient and innovative our industry can be when we set our sights on a common goal. For our part at Tradeweb, we look forward to continuing to refine our workflows along with the some of the most accurate and timely pricing and reference data available to ensure our clients are operating in a transparent, efficient marketplace.

About Tradeweb Markets

Tradeweb Markets Inc. (Nasdaq: TW) is a leading, global operator of electronic marketplaces for rates, credit, equities and money markets. Founded in 1996, Tradeweb provides access to markets, data and analytics, electronic trading, straight-through-processing and reporting for more than 40 products to clients in the institutional, wholesale and retail markets. Advanced technologies developed by Tradeweb enhance price discovery, order execution and trade workflows while allowing for greater scale and helping to reduce risks in client trading operations. Tradeweb serves approximately 2,500 clients in more than 65 countries. On average, Tradeweb facilitated more than $1.1 trillion in notional value traded per day over the past four quarters. For more information, please go to www.tradeweb.com.

Forward-Looking Statements

This release contains forward-looking statements within the meaning of the federal securities laws. Statements related to, among other things, our outlook and future performance, the industry and markets in which we operate, our expectations, beliefs, plans, strategies, objectives, prospects and assumptions and future events are forward-looking statements. We have based these forward-looking statements on our current expectations, assumptions, estimates and projections. While we believe these expectations, assumptions, estimates and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond our control. These and other important factors, including those discussed under the heading “Risk Factors” in documents of Tradeweb Markets Inc. on file with or furnished to the SEC, may cause our actual results, performance or achievements to differ materially from those expressed or implied by these forward-looking statements. Given these risks and uncertainties, you are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements contained in this release are not guarantees of future performance and our actual results of operations, financial condition or liquidity, and the development of the industry and markets in which we operate, may differ materially from the forward-looking statements contained in this release. In addition, even if our results of operations, financial condition or liquidity, and events in the industry and markets in which we operate, are consistent with the forward-looking statements contained in this release, they may not be predictive of results or developments in future periods. Any forward-looking statement that we make in this release speaks only as of the date of such statement. Except as required by law, we do not undertake any obligation to update or revise, or to publicly announce any update or revision to, any of the forward-looking statements, whether as a result of new information, future events or otherwise, after the date of this release.

- Investors run to safe-haven assets amid Middle East escalation Mar 6, 2026

- EUR/USD Under Pressure: Middle East Risks Outweigh All Else Mar 6, 2026

- Bitcoin shows resilience to Middle East events. Oil market stabilizes Mar 5, 2026

- GBP/USD: Market Not Expecting BoE Rate Cut in March Mar 5, 2026

- Brent headed for $100? Mar 4, 2026

- Global stock indices continue sell-off due to Middle East conflict Mar 4, 2026

- USD/JPY to Quickly Return to Growth: Momentum Favours the US Dollar Mar 4, 2026

- European equities plunge amid Persian Gulf military conflict Mar 3, 2026

- Gold Rallies for Fifth Day, With External Risks Mounting Mar 3, 2026

- Iran Crisis: A Dangerous Turning Point Mar 2, 2026