Investors faced up to a worrying shift in gears by central banks last week as policymakers in Europe either set the groundwork for a tightening in monetary policy or voted for stronger rate rises earlier than many expected. Tightening monetary conditions will be a key driver for 2022 and how risky assets deal with this new era of rising interest rates and reduced liquidity.

Prognostications over the next policy moves by major central banks will serve as the framework for interpreting the following economic events over the coming days:

Monday, February 7

- China markets reopen after Lunar New Year

- CNH: China January Caixin services and composite PMIs

- EUR: Germany December industrial production

Tuesday, February 8

Wednesday, February 9

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

- EUR: Germany December external trade

- GBP: BOE Chief Economist Huw Pill speech

- US crude: EIA crude oil inventory report

- USD: Cleveland Fed President Loretta Mester speech

- Disney earnings

- Uber earnings

Thursday, February 10

- EUR: European Commission’s updated economic forecasts

- GBP: BOE Governor Andrew Bailey speech

- USD: US January consumer price index

- Twitter earnings

- Coca-Cola earnings

- PepsiCo earnings

Friday, February 11

- GBP: UK 4Q GDP and external trade, December industrial production

- EUR: Germany January consumer price index

- USD: US February consumer sentiment

US CPI to grab the headlines

All eyes will be on the US inflation data released on Thursday. Headline CPI is expected to hit 7.3% year-on-year, the highest rate since February 1982. The core rate, which excludes volatile food and energy components, is forecast to touch 5.9%, a level last seen in October 1982. The impact of higher oil prices will be key, with the trend for higher rental costs and auto production restraints likely to continue in January. The key issue is whether these sources of upward price pressures will be sustained over the medium-term. Even if they are not, solid consumer demand and labour market tightness could keep inflation sticky for some time.

Of course, weaker than expected readings would raise hopes that inflation has plateaued. This would be good news for US stock markets, but not so much for the dollar and Treasury yields which would come off their recent highs made after the surprisingly good NFP report released on Friday.

Dollar slide held up by support

The dollar index fell sharply last week from 18-month highs as the ECB moved away from its ultra-accommodative policy stance. Fed officials had also recently calmed fears that a 50-point rate hike was on the cards at its next meeting in March, though the odds for this more than doubled on Friday to around 36% after the solid labour market data. This will add to the ammunition for the Fed hawks, with the fall in Omicron infections meaning there are hopes of a substantial rebound in activity from the second quarter.

The 100-day simple moving average and long-term trendline support from the May 2021 lows acted as support to the greenback last week. Another strong inflation print should encourage more buyers, with some analysts expecting even higher prices in the next few months due to the extreme worker shortage.

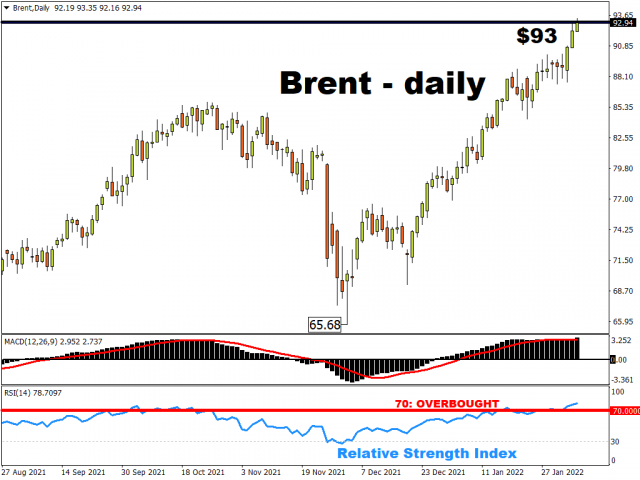

Oil advances to new cycle highs

Last week’s OPEC+ meeting offered little relief to the market, with traders now talking about $100 oil. It was the seventh straight weekly price gain and Brent has risen over 20% this year. As widely expected, the group agreed to a further output increase of 400k barrels per day for March. But the concern is that whilst the cartel may announce production increases, what the market sees is much smaller in reality.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Speculator Bets led by Silver, Gold & Platinum Mar 7, 2026

- COT Bonds Charts: Speculator Bets led by 10-Year Bonds & Fed Funds Mar 7, 2026

- COT Energy Charts: Speculator Bets led by Brent Oil & Heating Oil Mar 7, 2026

- COT Soft Commodities Charts: Speculator Bets led by Corn & Soybean Meal Mar 7, 2026

- Investors run to safe-haven assets amid Middle East escalation Mar 6, 2026

- EUR/USD Under Pressure: Middle East Risks Outweigh All Else Mar 6, 2026

- Bitcoin shows resilience to Middle East events. Oil market stabilizes Mar 5, 2026

- GBP/USD: Market Not Expecting BoE Rate Cut in March Mar 5, 2026

- Brent headed for $100? Mar 4, 2026

- Global stock indices continue sell-off due to Middle East conflict Mar 4, 2026