We get a plethora of data this week, including activity PMIs across the globe and GDP figures from Europe and the US. Geopolitical risks are rising as Russia-Ukraine tensions mount.

The highlight will be the Federal Reserve meeting on 26 January, sandwiched between key economic data releases and tech earnings:

Monday, January 24

Tuesday, January 25

- AUD: Australia 4Q inflation and December business confidence

- IMF updates World Economic Outlook

- Microsoft earnings

Wednesday, January 26

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

- US crude: EIA crude oil inventory report

- USD: Fed rate decision

- CAD: Bank of Canada rate decision

- Tesla earnings

- Intel earnings

Thursday, January 27

- CNH: China December industrial profits

- USD: US weekly initial jobless claims and 4Q GDP

- Apple earnings

Friday, January 28

- NZD: New Zealand January consumer confidence

- EUR: Eurozone January economic confidence, Germany 4Q GDP

- USD: US December PCE deflator, personal income and spending, and consumer sentiment

The FOMC is expected to signal a rate hike in March and the immediate end of its bond buying programme, brought forward from the current mid-March end point.

Markets are now pricing in four Fed hikes of 25bp this year with a good chance that we will see more than two rate hikes in the first half of 2022, or alternatively a 50bp hike. Most notably, bond yields have moved higher with stable to lower inflation expectations, resulting in a sharp move higher in real rates. This has been the key driver of souring risk appetite and will determine market direction going forward, in what is becoming quite an aggressive path for Fed action.

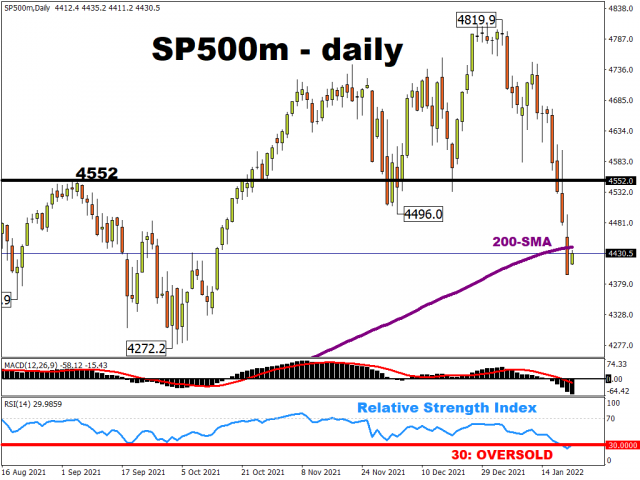

Stock markets brace for tech sector results

Company earnings will be in focus with many investors hoping the releases stop the strong selloff we have seen in tech stocks and the broader US equity markets.

Anxiety over rising US interest rates has seen investors flee global stocks this year with the tech-heavy Nasdaq suffering its biggest slide since the pandemic rocked markets in March 2020.

The broader blue-chip S&P 500 index shed 5.7% last week with more than two-thirds of the companies within the index now in a technical correction – or down at least 10% from their record high – including 149 stocks that have fallen by 20% or more. Some of the world’s biggest companies report in the next fortnight, including Microsoft after the US market closes on Tuesday, Tesla and Intel mid-week and Apple after US markets close Thursday, while Amazon and Facebook release their latest earnings next week.

The pressure is on many of last-year’s high-flying tech companies to refuel investor confidence and stop the contagion from the tech drawdown.

That said, the S&P500 is still higher now than it was in September, even though equities remain richly valued. An alignment of financial markets and conditions with the Fed’s more hawkish rhetoric and outlook has been on the cards for some time.

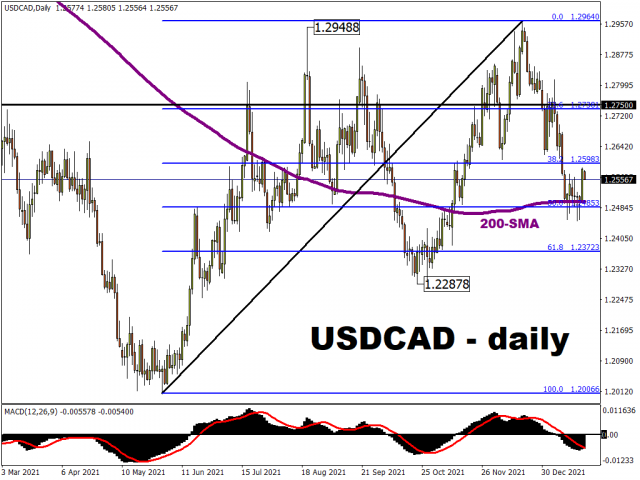

Bank of Canada set to pull the rate hike trigger

Hours before the Fed meeting on Wednesday, policy makers at the BoC are likely to raise interest rates 25bps, with at least three more rate hikes predicted by markets this year. Inflation is at 30-year highs and the economy is at record employment, while Covid restrictions are set to ease at the end of the month.

With some analysts predicting as many as five rate rises in 2022, the Canadian dollar should continue to outperform, especially against those currencies whose central banks are in no rush to tighten monetary policy, like the ECB and BoJ.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Speculator Bets led by Silver, Gold & Platinum Mar 7, 2026

- COT Bonds Charts: Speculator Bets led by 10-Year Bonds & Fed Funds Mar 7, 2026

- COT Energy Charts: Speculator Bets led by Brent Oil & Heating Oil Mar 7, 2026

- COT Soft Commodities Charts: Speculator Bets led by Corn & Soybean Meal Mar 7, 2026

- Investors run to safe-haven assets amid Middle East escalation Mar 6, 2026

- EUR/USD Under Pressure: Middle East Risks Outweigh All Else Mar 6, 2026

- Bitcoin shows resilience to Middle East events. Oil market stabilizes Mar 5, 2026

- GBP/USD: Market Not Expecting BoE Rate Cut in March Mar 5, 2026

- Brent headed for $100? Mar 4, 2026

- Global stock indices continue sell-off due to Middle East conflict Mar 4, 2026