It’s a jam-packed week full of important economic data, major G-10 central bank meetings and no doubt, more updates on the Omicron variant.

Here are the key events lined up for this week:

Tuesday:

- JPY: Japan October industrial production (final)

- AUD: Australia consumer and business confidence

- EUR: Eurozone October industrial production

- GBP: UK October unemployment, November jobless claims

- USD: US November producer price index

Wednesday:

- CNY: China November industrial output and retail sales

- GBP: UK November inflation

- USD: Federal Reserve decision and November retail sales

- US crude: EIA weekly US crude oil inventory report

Thursday:

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

- GBP: Bank of England decision and December PMIs

- EUR: European Central Bank decision and December PMIs

- USD: US initial weekly jobless claims, November industrial production, and December PMIs

Friday:

- JPY: Bank of Japan decision

- EUR: Eurozone November inflation (final), Germany November producer prices and December IFO business climate

Although the CBOE Volatility Index (VIX) has fallen back to its long-term average around 20, trading volumes may be thinner than normal as desk take off risk positions ahead of these major risk events and the holiday season. No-one wants to be caught offside on a big position heading into Christmas and illiquid trading sessions!

The FOMC meeting is arguably the most important, but the major policy point has been telegraphed already.

Fed Chair Powell’s recent hawkish message that inflation is more permanent is likely to be confirmed as the FOMC double the speed of the tapering of its bond purchases which means the stimulus should end in March, as opposed to the middle of next year. This should in turn open the door to faster interest rate rises, with consensus seeing at least a two-hike view for next year.

Perhaps more crucially, the market will see the new set of forecasts and “dots” as policymakers update their projections for the Fed Funds rate over the coming years.

Watch out especially for the new terminal rate, essentially the peak interest rate, which will be revised and potentially upgraded.

The ECB has more difficult choices to make, in what was supposed to be a big bang meeting. The current fourth wave of the pandemic, plus the new Omicron variant, will add further pressure to the region’s economy, while headline inflation has continued to accelerate. New staff projections are released, and long-term inflation forecasts will be monitored to see if “team transitory” is still winning the argument. A probable drop back below 2% will support the bank’s patient approach. The hawks will be placated with the phasing out of the emergency QE program as planned in March 2022.

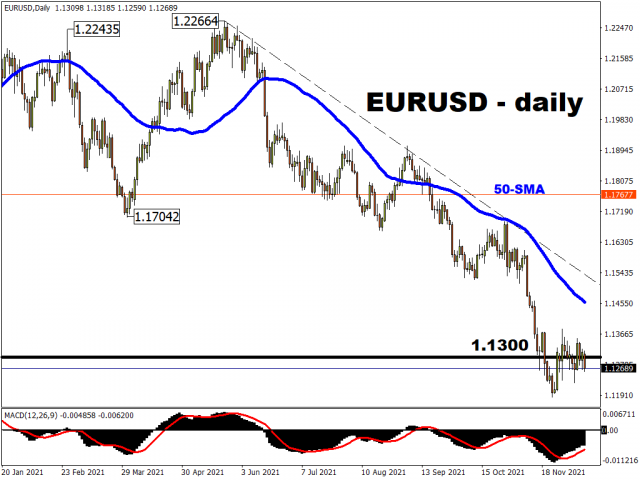

The euro has traded around 1.13 since the end of November. Its failure to make a decent run at the 1.14 level points to the downward trend reasserting itself.

The Bank of England decision is set to be a close call on Thursday, with expectations of a 15bp rate hike tempered by the recent announcement of “Plan B” Covid restrictions. Having let down markets in November by not hiking, the Omicron variant has been added to the mix of uncertainty which policymakers have to deal with. Hawkish rhetoric around inflation has continued from MPC members, with the new variant potentially exacerbating the supply chain recovery.

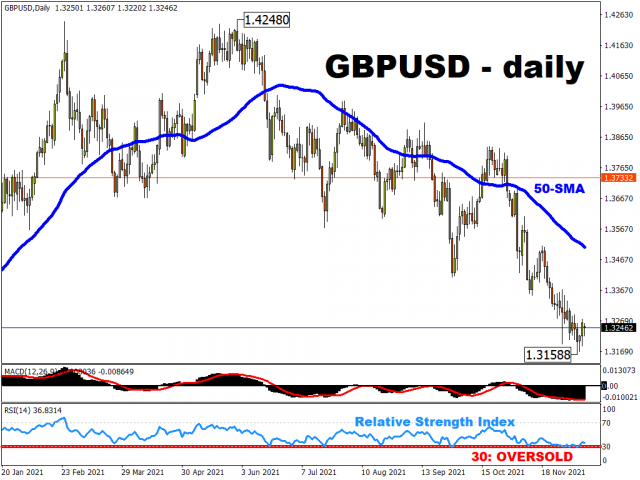

Sterling touched new lows for the year last week at 1.3160 and cable will need to get back above 1.3411 to change the current bearish momentum.

The final major central bank to meet is the Bank of Japan, who will keep policy ultra-easy. There is speculation that policymakers may end some of the pandemic measures before they run off in March.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- The US introduces new import tariffs for 60 countries. Brent crude surpasses $100 per barrel Jul 24, 2026

- USD/JPY Breaks Records: Nothing Slows the Yen’s Decline Jul 24, 2026

- Oil prices reached a 6‑week high. The AUD strengthened on the back of a strong labor‑market report Jul 23, 2026

- EUR/USD Recovers as Dollar Weakens Jul 23, 2026

- Bitcoin rose to $66,000. The New Zealand dollar continues to strengthen Jul 22, 2026

- Inflationary pressure is easing in Canada. In New Zealand, on the contrary, inflation is rising Jul 21, 2026

- GBP/USD Falls After Cabinet Changes Jul 21, 2026

- Geopolitical and macroeconomic conditions continue to pressure market sentiment Jul 20, 2026

- USD/JPY Poised to Continue Gains as Expensive Oil and Lack of Support Weigh on Yen Jul 20, 2026

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026