This week, investors are set to digest the October retail sales data out of some of the world’s largest economies, alongside these scheduled economic data and corporate earnings releases:

Monday, November 15

- JPY: Japan GDP

- CNH: China October retail sales, industrial production

- GBP: BOE MPC member Jonathan Haskel speech

Tuesday, November 16

- AUD: RBA Governor Philip Lowe speech, RBA meeting minutes

- EUR: Eurozone Q3 GDP

- GBP: UK September unemployment, October jobless claims

- USD: US October retail sales and industrial production

- Walmart Q3 earnings

- Home Depot Q3 earnings

- USD: Fed speak – Richmond Fed President Thomas Barkin, Kansas Fed President Esther George, Atlanta Fed President Raphael Bostic, Philadelphia Fed President Patrick Harker

Wednesday, November 17

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

- JPY: Japan October trade

- EUR: Eurozone October CPI (final)

- GBP: UK October CPI

- Baidu Q3 earnings

- USD: Fed speak – New York Fed President John Williams, San Francisco Fed President Mary Daly

- US crude: EIA weekly US crude oil inventory report

- NVIDIA Q3 earnings

- Lowe’s Q3 earnings

- Target Q3 earnings

Thursday, November 18

Friday, November 19

- JPY: Japan October CPI

- GBP: UK October retail sales, November consumer confidence

- GBP: BOE Chief Economist Huw Pill speech

- CAD: Canada September retail sales

- USD: Fed speak – San Francisco Fed President Mary Daly, Fed Vice Chairman Richard Clarida

Let’s first consider the hard economic data. Markets are forecasting month-on-month retail sales growth of 1.3% for the US and 0.5% for the UK. China’s October retail sales exceeded market expectations this morning, growing 4.9% year-on-year compared to the median estimate of 3.7%.

Should more of these figures come in better-than-expected, then risk sentiment could be emboldened by the fact that consumers worldwide are still able to display enough spending power to preserve the global economic recovery.

On top of that, more clues about the health of spending levels could be derived from the Q3 earnings from household names such as Walmart, JD.com and Alibaba. For the US in particular, retail giants such as Home Depot, Lowe’s, and Target are also due to release their respective financial results from this past quarter, noting that these 3 stocks are also constituents of the S&P 500.

S&P 500 to post new record high?

Note that consumer discretionary stocks have a 12.8% weightage on the S&P 500. Hence, this blue-chip index could be spurred higher if these earnings and retail sales economic data come in better-than-expected, especially if the good news can punch past the swirling concerns surrounding the heightened inflation levels in major economies.

The fear is that, as consumer prices rise, people’s purchasing power is diminished. Should consumption drop, then the global economy could lose one of its main drivers of growth. Persistently higher inflation which chokes the global economic recovery may result in a “stagflation” environment, which would be bad for risk sentiment.

Faced with such risks, stock markets could do with some healthy readings on retail sales and corporate earnings in order for the S&P 500 to post a new record high, which is a mere 0.4% away at the time of writing.

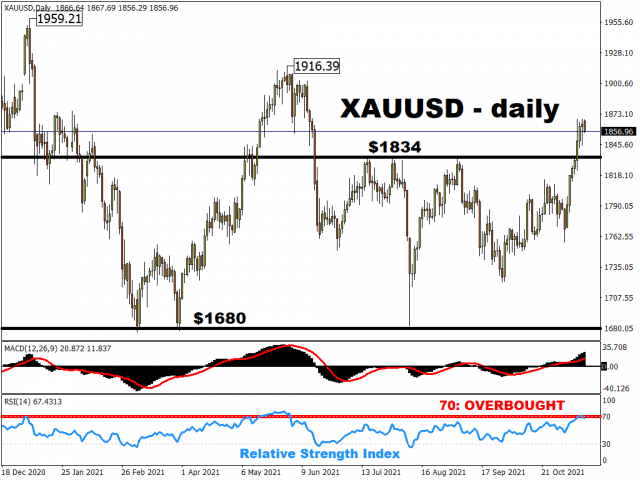

Gold supported by inflation concerns

Bullion has clearly benefitted from these fears surrounding persistently higher inflation, with spot gold trading around its highest levels since June.

Should the retail sales data show that consumption levels are indeed waning as a result of these higher inflation, that could stoke further demand for this safe haven asset which is traditionally seen as a hedge against inflation.

Bullion support is also very reliant on the notion that the Federal Reserve will continue to remain patient before raising US interest rates. Note that gold prices tend to have an inverse relationship with bond yields, which tend to feed off the US monetary policy outlook. Considering the speeches by Fed officials over the coming days, should policymakers show more and more desire to raise interest rates sooner than expected, that in turn could prompt gold to unwind some of its recent gains.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- The Central Bank of Mexico kept its interest rate unchanged. Iran plans to introduce strict bans for US and Israeli vessels in the Strait of Hormuz Aug 7, 2026

- USD/JPY Holds Firm: Yen Loses Some Support Aug 7, 2026

- Australian trade balance returned to positive territory Aug 6, 2026

- Results in Line for Most Reporting Companies Aug 5, 2026

- Stock indices continue to break records. Oil is falling amid intensified diplomatic dialogue between the US and Iran Aug 5, 2026

- USD/JPY Holds Steady After Intervention: Outlook Remains Uncertain Aug 5, 2026

- EUR/USD: Busy Week Ahead Aug 3, 2026

- Positive sentiment in the AI sector supported stock indices. Oil prices remain volatile Aug 3, 2026

- The Tech‑heavy NASDAQ Index jumped by more than 3.3%. The offshore yuan is trading at its highest level since 2023 Jul 31, 2026

- USD/JPY After Volatility: Multiple Events in One Day Jul 31, 2026