Brent oil has surged by around 56% so far this year. Meanwhile, the benchmark dollar index (DXY) gained 4.77% in the first three quarters of 2021, with the greenback having advanced against all of its G10 peers except for the Canadian dollar during that period.

Will traders find enough reason to push both oil and the buck higher this week?

Markets will be closely monitoring the OPEC+ meeting and the upcoming US nonfarm payrolls report, along with these other scheduled economic events:

Monday, October 4

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

- China markets closed through Thursday

- Brent: OPEC+ decision

- USD: Fed speak – St. Louis Fed President James Bullard

Tuesday, October 5

- AUD: Reserve Bank of Australia policy decision

- JPY: BOJ Governor Haruhiko Kuroda speech

- EUR: Eurozone August PPI

- USD: US September ISM services index

Wednesday, October 6

- NZD: RBNZ rate decision

- EUR: August Eurozone retail sales, Germany factory orders

- USD: September ADP employment change

- US crude: EIA crude oil inventory report

- USD: Fed speak – Kansas City Fed President Esther George

Thursday, October 7

- EUR: Germany August industrial production

- HK stocks: PBOC Governor Yi Gang speaks on “China’s experience with regulating big tech”.

- USD: US initial jobless claims

- USD: Fed speak – New York Fed President John Williams

- EUR: ECB Chief Economist Philip Lane speech

- Tesla annual shareholder meeting

Friday, October 8

- CNH: China September Caixin services and composite PMIs

- EUR: Germany August trade

- CAD: Canada September employment change

- USD: US September nonfarm payrolls

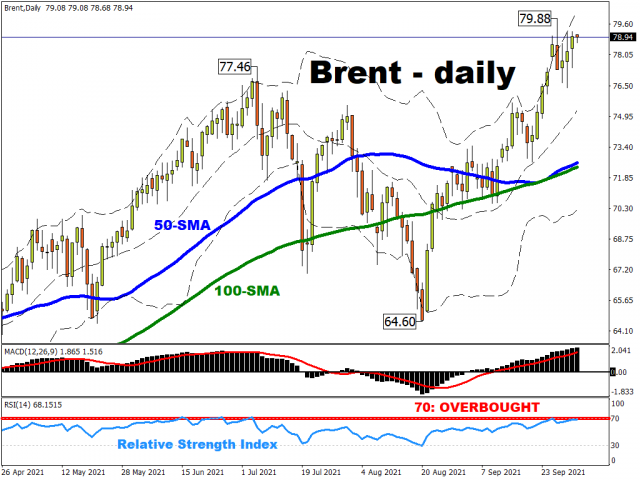

Will OPEC+ give the green light for $80 Brent?

Brent futures have climbed for a sixth consecutive week to trade around its highest levels since 2018. However, as economic principles would have it, higher prices also tend to encourage more supply.

Such will be the dilemma when OPEC+ gathers today (Monday, 4 October) to decide on its collective production levels for November.

As things stand, the alliance has agreed to gradual monthly supply hikes of 400k barrels per day (bpd). However, that is not enough for a world that’s growing increasingly desperate for more oil, especially as the colder winter months approach.

Hence, the alliance of 23 major oil-producing nations may be tempted to take advantage of the higher prices and generate more income by selling more of its supplies to a world that’s craving for it.

Such a surprise move by OPEC+ may, as a knee-jerk reaction, unwind some of the recent gains in oil benchmarks as markets price in the prospects of higher-than-expected supplies.

However, oil bulls are likely to wait for the crucial OPEC+ decision. If the alliance sticks with their current output plan, that should be the green light to push Brent past $80/bbl.

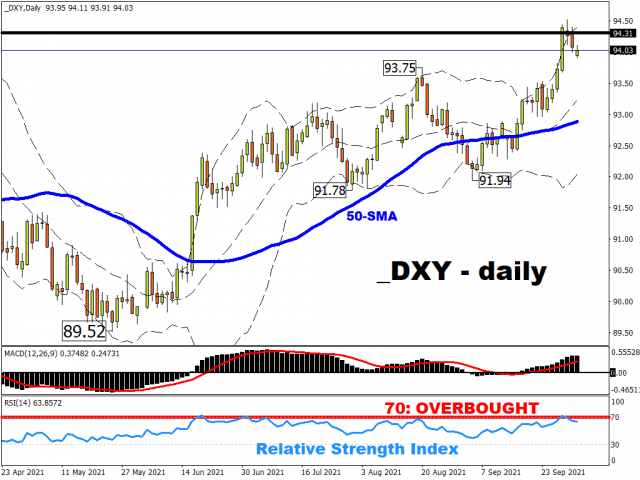

Will the dollar post fresh 2021 highs?

Last week, the benchmark dollar index (DXY) posted a new year-to-date high above the psychologically-important 94 mark. The recent surge in US Treasury yields has lifted the greenback, as markets price in the growing prospects of a US rate hike happening sooner rather than later.

On September 1st, markets had priced in a 77% chance of a Fed rate hike happening by December 2022. Those odds have now gone past 95% – meaning that a hike by end-2022 is now almost fully priced in.

Enter the highly-anticipated US nonfarm payrolls report due this Friday.

As Fed Chair Jerome Powell has made clear recently, further progress in the US jobs markets would essentially give policymakers the green light to start tapering its bond purchases before the year is over (widely expected to commence in November). And with US inflationary pressures already showing signs that it could stay around for longer than expected, more employed Americans could raise demand-side inflationary forces.

Such economic conditions could mean that the policymakers may have to bring forward their rate hike, and such prospects only suggests more upside for the US dollar.

Note that the DXY has eased away from overbought conditions, falling back below its upper Bollinger band and its 14-day relative strength index moderating back below the 70 line. With some of the froth cleared in the dollar index, that should clear the path for more near-term gains, if indeed the US economic data warrants it so.

Of course, we note the typically inverse relationship between oil and the dollar. Hence, all of the factors above should make for an interesting week for oil prices and the US dollar, and whether both can sustain their respective surges of late.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026

- Oil prices jumped 4% amid a new wave of escalation between the US and Iran Jul 13, 2026

- EUR/USD: US Inflation Will Determine Everything Jul 13, 2026