There’s a lot going on in the markets at present as traders and investors try and get their heads round the various competing forces. Brent crude is rising for a sixth straight day and is making three-year highs through $80. The global energy crisis is a key focus which may only get worse as we head into winter.

Demand is outstripping supply as the gas crunch spreads around the globe, propelling prices to new parabolic peaks. The lack of natural gas is forcing a switch to oil as an alternative for power generation. The global economic recovery is also seeing more demand in general, with a pickup in airline traffic depleting low oil inventories.

Brent crude has surged past the year-to-date high made in July at $77.46. The May 2018 top sits at $80.47 ahead of the October 2018 mark at $86.60. Prices are overbought on the daily RSI and have cut through the upper band of the Keltner channel so a pullback may be in order soon.

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Bond yields ripping higher, fuelling the dollar

Having seemingly not paid too much attention to the Fed’s hawkish shift last week, markets are hitting bond markets hard, which means yields are flying north. The widely watched 10-year US Treasury yields hit 1.51% and the shorter end five-year yield touched levels last seen in February 2020.

Notably, this is pushing USD/JPY higher, with JPY also suffering as a large energy importer.

Buyers took out the August high yesterday at 110.80 and now have their eyes on this year’s top at 111.659. A break through here could see a push towards 112.25.

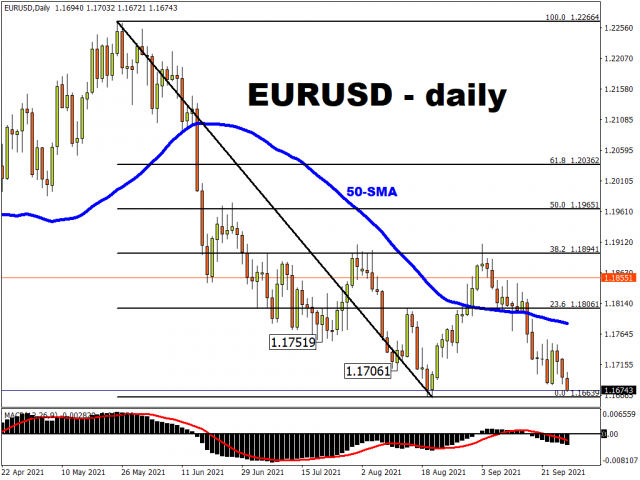

The dollar looks to now be breaking higher on the DXY, with the year-to-date high at 93.72 now within sight. EUR/USD is similarly looking towards major levels, with 1.16639 key support. The energy crisis and shortages mean the backdrop is fragile which is also helping the greenback.

ECB Sintra symposium

The ECB conference at Sintra kicks off today. This has delivered some historic shifts in ECB policy in the past – recall President Mario Draghi’s uber dovish comments in 2019.

Nothing of that magnitude is expected this week but eurozone inflation numbers at 13-year highs released on Friday should sharpen the minds, or at least the hawks’ talons.

Does the ECB still view inflation as “transitory”? And will we get any hints on how the emergency bond buying programme (PEPP) will end next March?

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- Geopolitical and macroeconomic conditions continue to pressure market sentiment Jul 20, 2026

- USD/JPY Poised to Continue Gains as Expensive Oil and Lack of Support Weigh on Yen Jul 20, 2026

- COT Metals Charts: Weekly Speculator Bets led by Copper & Steel Jul 18, 2026

- COT Bonds Charts: Weekly Speculator Bets led by 2-Year, SOFR 3M & 5-Year Bonds Jul 18, 2026

- COT Energy Charts: Weekly Speculator Bets led by Brent Oil & Heating Oil Jul 18, 2026

- COT Soft Commodities Charts: Weekly Speculator Bets led by Wheat, Corn & Soybean Meal Jul 18, 2026

- The Bank of Canada kept its interest rate unchanged. Platinum prices reached a three‑week high Jul 16, 2026

- Stock indices rose after the release of US inflation data. China’s GDP slowed sharply Jul 15, 2026

- GBP/USD Awaits Political News: What Will Happen Next Jul 15, 2026

- USD/JPY Holds at Highs: Pressure Lingers on Yen Jul 14, 2026