We got an update on the second part of the Fed’s mandate today in the form of the widely anticipated US CPI data. Admittedly, the central bank’s average inflation target puts more importance on employment but persistent inflation around current levels is certainly a test to the Fed’s transitory narrative, especially at a time when job market fundamentals are improving.

The annual rate of inflation in July has seemingly peaked, printing at 5.4% which was the same reading as the prior month. Core also printed in line on an annualised basis but two-tenths lower than in June, while the 0.3% month-on-month reading was the lowest in four months. The annual comparisons between a lockdown economy and a vibrant re-opening have now passed. But how quickly the figures get back down to around the 2% Fed target area is key for markets.

Will production bottlenecks and labour shortages endure longer than the policymakers at the Fed think?

Demand is certainly outpacing supply at the moment and pricing power is returning to companies. Economists also warn of rising housing costs like rent which lag house price changes and account for a third of the pricing basket.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Dollar sells off post-data

With the market fearing a higher set of inflation figures, bond yields have backed off their highs and the greenback has failed near its recent pivot top amid selling pressure.

Of course, it’s all about the taper debate (September versus December) together with the pace of the taper once it starts. Interestingly, even the in line prints are seeing a negative reaction which suggest that the dollar long trade is crowded.

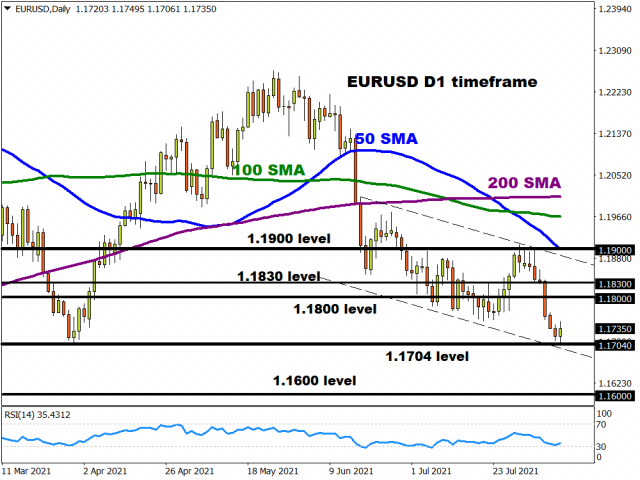

EUR/USD had closed lower for six straight days until today and moved down to test the year-to-date lows at 1.1704. Oversold conditions on the RSI are seeing some buying in the pair, but longer-term the relative position for both central banks is still exceptionally wide.

There is no key support on the charts until the 1.16 area where the September and November 2020 bottoms reside. Prices would need to get back above 1.1751 and then 1.18 to arrest the bearish momentum.

Stocks keep calm and carry on higher…

The major US indices have opened higher with the Dow and S&P500 trading at record intraday highs.

The less scary inflation numbers (it’s all relative!) are supporting investor confidence and the buying of equities. Less hawkish Fed speak recently and the passing of the trillion dollar infrastructure bill is also helping sentiment.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- The Central Bank of Mexico kept its interest rate unchanged. Iran plans to introduce strict bans for US and Israeli vessels in the Strait of Hormuz Aug 7, 2026

- USD/JPY Holds Firm: Yen Loses Some Support Aug 7, 2026

- Australian trade balance returned to positive territory Aug 6, 2026

- Results in Line for Most Reporting Companies Aug 5, 2026

- Stock indices continue to break records. Oil is falling amid intensified diplomatic dialogue between the US and Iran Aug 5, 2026

- USD/JPY Holds Steady After Intervention: Outlook Remains Uncertain Aug 5, 2026

- EUR/USD: Busy Week Ahead Aug 3, 2026

- Positive sentiment in the AI sector supported stock indices. Oil prices remain volatile Aug 3, 2026

- The Tech‑heavy NASDAQ Index jumped by more than 3.3%. The offshore yuan is trading at its highest level since 2023 Jul 31, 2026

- USD/JPY After Volatility: Multiple Events in One Day Jul 31, 2026