Source: McAlinden Research (9/6/23)

McAlinden Research shares a deep dive into a market driver with alpha-generating potential.

McAlinden Research shares a deep dive into a market driver with alpha-generating potential.

Last week, the U.S. Federal Trade Commission (FTC) suspended its legal challenge to Amgen Inc. (AMGN:NASDAQ)’s proposed acquisition of Horizon Therapeutics Plc (HZNP:NASDAQ), 2022’s largest deal announcement in the biopharma space. The FTC and Amgen-Horizon then agreed to settle on Friday, clearing the way for the $27.8 billion purchase to close sometime in the fourth quarter.

The FTC notes that, as part of the settlement, attorneys general from six states — California, Illinois, Minnesota, New York, Washington, and Wisconsin — will also dismiss a related federal court preliminary injunction action.

There was significant doubt cast upon the FTC’s case not long after the commission originally filed its suit in May, given its employment of a novel theory that Amgen could eventually bundle its drugs with those it is acquiring from Horizon in negotiations with insurers — therefore entrenching Horizon products’ premiere placement in the market and choking out potential competitors that might be cheaper or more effective. Horizon currently sells two marketed products, Tepezza (teprotumumab) for thyroid eye disease and Krystexxa (pegloticase), a chronic refractory gout treatment.

Since Amgen was quick to agree that they would not bundle their products with Horizon’s, a settlement was the natural conclusion. Further conditions of the agreement between the FTC and the two firms stipulate Amgen will not introduce discount or rebate schemes on their own products that would influence the sale or positioning of Horizon’s drugs.

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

The FTC, which has become more aggressive toward mega-mergers across multiple industries, presented the Amgen-Horizon settlement as a win, but it seems more likely that an ongoing wave of M&A activity among pharmaceutical and biotechnology firms will be bolstered by the sudden conclusion of the suit.

GlobalData’s Deals Database, cited by Pharmaceutical Technology, notes that there were 479 pharma M&A deals announced in Q2 2023, increasing by 18% QoQ in Q2 and 151% YoY. The total value of these deals was $51 billion, decreasing by -30% in Q2, compared with the previous quarter’s total of $72.5 billion. Still, Q2’s pharma industry M&A deal value rose by 77% YoY.

Though fewer deals were signed in the first quarter than in the second, the size of Q1’s deal value was boosted by Pfizer Inc.’s announcement that they would be acquiring massive biotech firm Seagen Inc. in biopharma’s largest deal in almost four years’ time. Pfizer’s offer of $229 per share in cash, a 33% premium on Seagen’s share price at the close preceding the deal becoming public, pushed the total value of the deal to $43 billion.

As MRP has previously noted, Pfizer executives have been among a consortium of biopharma heads that have voiced their desire to increase dealmaking with outside companies. Pfizer has set a goal of adding $25 billion in revenue by 2030 from business development moves, including acquisitions. Those could help the company offset an estimated drop of roughly $17 billion in sales from upcoming patent expirations. Bloomberg notes that Pfizer thinks that sales of Seagen’s four FDA-approved oncology products will exceed $10 billion, about $2 billion more than analysts’ estimates.

The smooth closure of the Pfizer-Seagen tie-up is still beholden to regulators at the FTC, but the recent news on the Amgen-Horizon deal is likely to invigorate confidence among investors that this deal will ultimately receive approval as well.

As of July, the FTC requested more information from Pfizer and Seagan in their review of the deal. Fierce Pharma writes that second requests from the FTC occur in roughly 25% of M&A deals, citing MEDACorp data. The regulator challenges such a transaction 5% — 10% of the time.

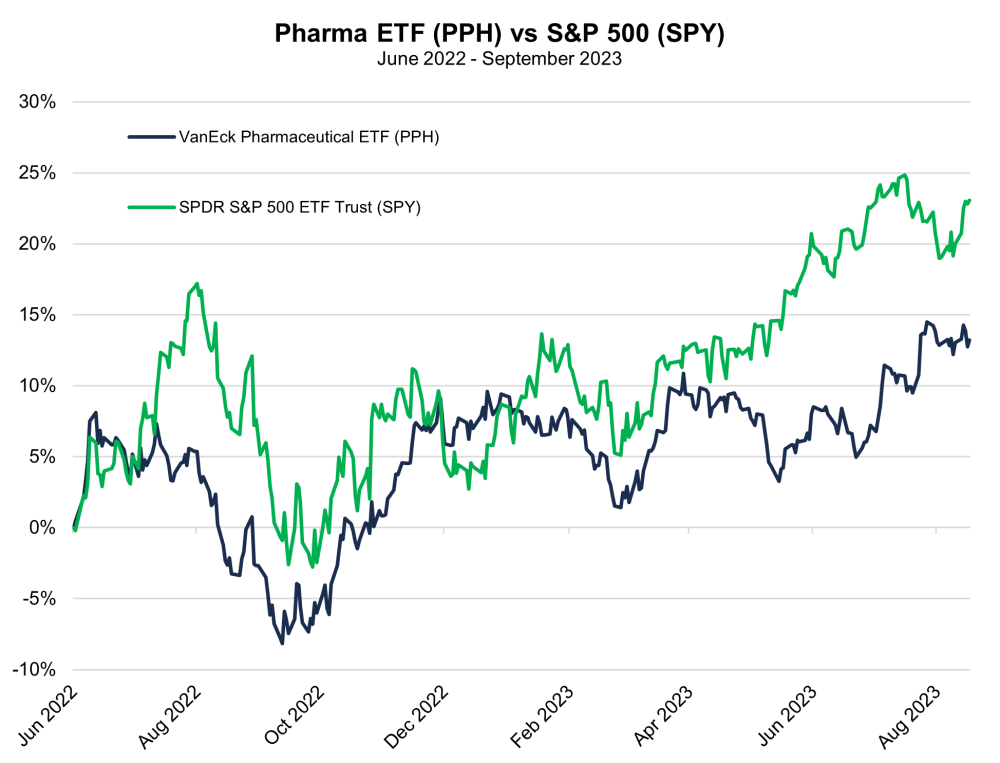

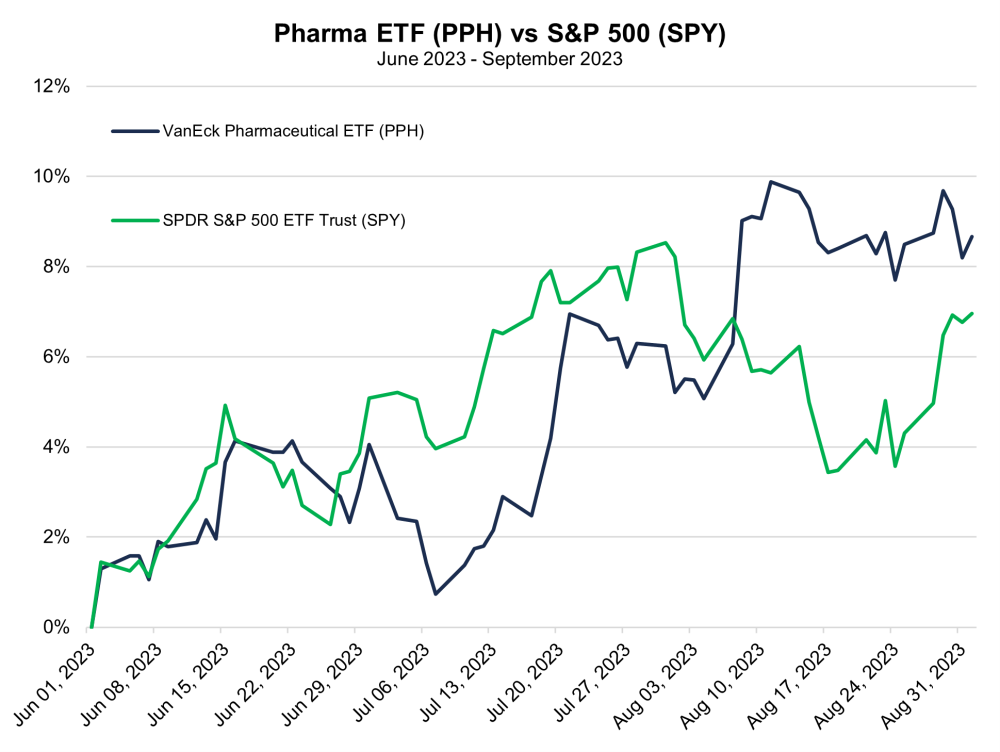

Charts

Important Disclosures:

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

- This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

For additional disclosures, please click here.

McAlinden Research Partners Disclosures

This report has been prepared solely for informational purposes and is not an offer to buy/sell/endorse or a solicitation of an offer to buy/sell/endorse Interests or any other security or instrument or to participate in any trading or investment strategy. No representation or warranty (express or implied) is made or can be given with respect to the sequence, accuracy, completeness, or timeliness of the information in this Report. Unless otherwise noted, all information is sourced from public data.

McAlinden Research Partners is a division of Catalpa Capital Advisors, LLC (CCA), a Registered Investment Advisor. References to specific securities, asset classes and financial markets discussed herein are for illustrative purposes only and should not be interpreted as recommendations to purchase or sell such securities. CCA, MRP, employees and direct affiliates of the firm may or may not own any of the securities mentioned in the report at the time of publication.

- Investors run to safe-haven assets amid Middle East escalation Mar 6, 2026

- EUR/USD Under Pressure: Middle East Risks Outweigh All Else Mar 6, 2026

- Bitcoin shows resilience to Middle East events. Oil market stabilizes Mar 5, 2026

- GBP/USD: Market Not Expecting BoE Rate Cut in March Mar 5, 2026

- Brent headed for $100? Mar 4, 2026

- Global stock indices continue sell-off due to Middle East conflict Mar 4, 2026

- USD/JPY to Quickly Return to Growth: Momentum Favours the US Dollar Mar 4, 2026

- European equities plunge amid Persian Gulf military conflict Mar 3, 2026

- Gold Rallies for Fifth Day, With External Risks Mounting Mar 3, 2026

- Iran Crisis: A Dangerous Turning Point Mar 2, 2026