By Cem Soner, Bangor University

Is the tide finally turning for Turkey? Three months after the re-election of Recep Tayyip Erdoğan for his third term as president, which many feared would lead to economic chaos, ratings agency Moody’s has indicated that Turkey’s credit rating is on course for an upgrade.

Since the election, Erdoğan has installed a new economic team with a commitment to reintroduce conventional monetary policies after years of a more singular approach. This has yielded some early positive results, with June recording the first current account surplus in 18 months – meaning more money came into the country than went out (mostly due to tourism and lower energy imports).

Meanwhile, Turkey’s stock market has been attracting surging interest from foreign investors, and the cost of insuring against the risk of the government defaulting on its debts has sharply declined. So what’s going on?

The mess

When Erdoğan won the May election, contrary to the opinion polls, it extended his tenure as prime minister and then president to almost 20 years. This five-year term is likely to be his last, due to his deteriorating health and constitutional constraints. Thanks to the economic debacle that he created himself, it is also likely to be his most challenging.

There are two pillars to Erdoğanomics: the “unorthodox” view that high interest rates cause inflation rather than the other way around, and a fixation on keeping rates as low as possible. It became much easier for him to implement after becoming executive president in 2018, which gave him much more power.

Free Reports:

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

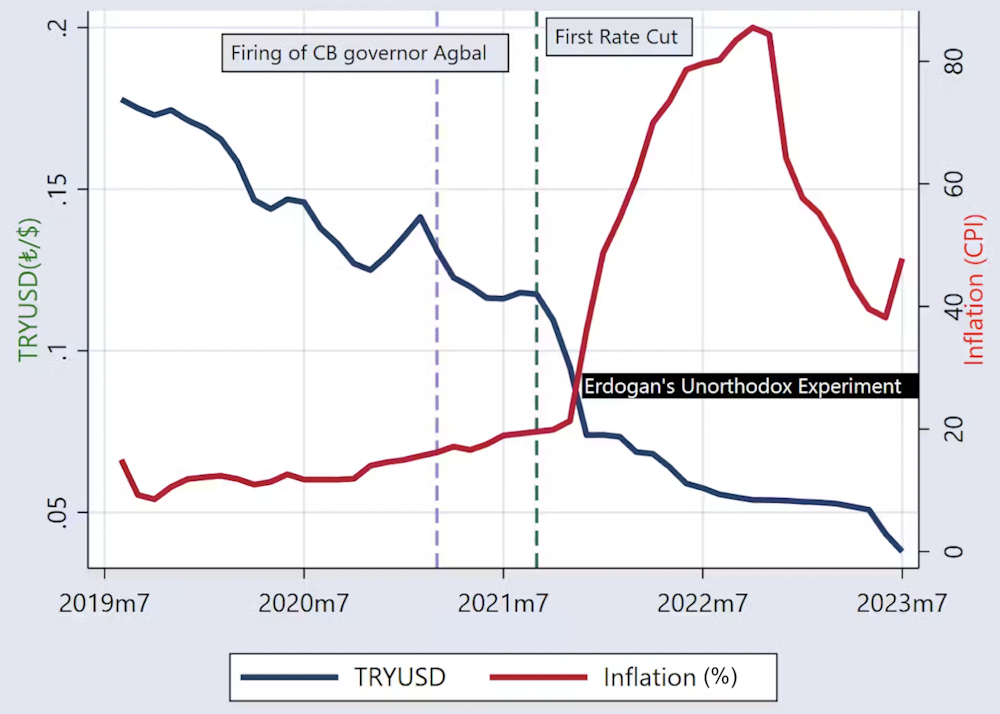

Central bank governors who have disagreed with Erdoğan’s agenda have been shown the door, most notably Naci Ağbal, who was sacked in March in 2021 after only four months in office. It was the next governor, Şahap Kavcıoğlu, a former MP in the ruling party and columnist in a pro-Erdoğan newspaper, who put Erdoğanomics into overdrive. Turkey experimented with aggressively cutting rates at a time when inflation was already close to 20% and most central banks were tightening.

Official inflation skyrocketed to over 80% and the lira plummeted, forcing the central bank to sell substantial foreign exchange reserves to try and shore up the currency. The current account deficit widened to a record level in January and the earthquake in February further worsened the situation.

Turkish inflation and the falling lira

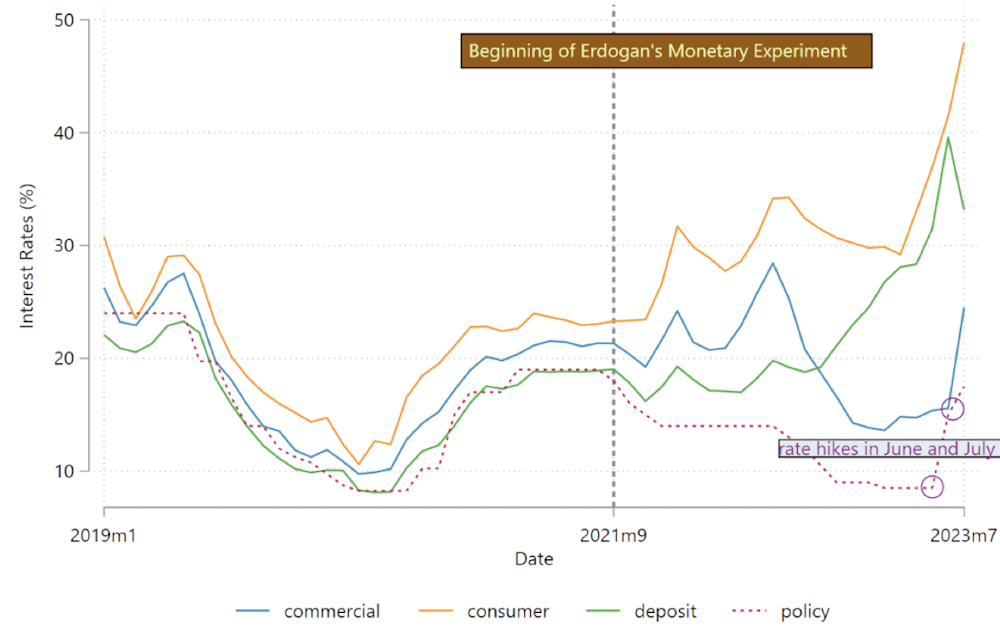

This all happened despite the fact that the authorities struggled to impose their interest rate cuts on the wider economy. Whereas normally high-street interest rates move in line with the central bank rate, Turkish banks responded to the central-bank rate cut by increasing rates on consumer and business loans and savings accounts, signalling they didn’t think the central bank’s policy was sustainable. Loan rates for businesses only later came down after the state-owned banks received a capital boost in the run-up to the election.

The interest rate divergence

A new approach?

The president has now taken a different path. He has appointed former investment banker Mehmet Şimşek as finance minister. Şimşek is respected by the markets due to a previous successful stint managing Turkey’s economy between 2007 and 2018. He has vowed to return to rational economic policies, announcing: “We will prioritise macro financial stability.”

Another reversal signal has been the appointment of Hafize Gaye Erkan as the first female governor of Turkey’s central bank. She too comes from investment banking, having formerly been managing director at Goldman Sachs and co-CEO of First Republic Bank in the US. She has no central banking experience, but markets nonetheless welcomed her appointment. She has an outstanding resume compared to her predecessor, Kavcıoğlu.

Erkan hiked rates on June 22 from 8.5% to 15%, the highest in nearly two years. The accompanying press release expressed a clear view that this is the way to reduce inflation.

The lira has nevertheless kept losing value, while annual inflation rose from 38% to 48% in July. But along with the other improvements I mentioned at the beginning, there has also been a slight improvement in foreign exchange reserves, indicating that the central bank is under less pressure to defend the currency.

In July, the markets were further reassured by the appointments of high-profile economists as new deputy governors for the central bank. This further decreased Turkey’s credit risk. On July 20, the bank hiked interest rates again, to 17.5%.

{kind=link}

What next

Raising interest rates may have side effects. Turkey has one of the world’s highest percentages of “zombie firms” that have only been able to stay afloat because of low borrowing costs, so there could well be bankruptcies. Also, we know from the recent US banking failures that rate hikes inflict significant stress on banks by reducing the value of their bond portfolios.

Turkey’s banks are obviously not new to life under Erdoğan. They have some fine management teams and effective risk-management practices that are used to weathering the country’s economic storms. All the same, they look vulnerable because they hold low-yielding government bonds that could be impaired by aggressive rate hikes – particularly since they are denominated in lira, which creates exposure to further currency collapses. The government could alleviate this concern by swapping these bonds in exchange for new high-yielding ones.

The bigger question is whether we’re really seeing the end of Erdoğanomics or just a lull. We can’t rule out a repeat of 2021, when Ağbal was installed as central bank governor despite his orthodox economic views, then removed shortly after. Erdoğan has already put Şahap Kavcıoğlu, his biddable governor from 2021-23, in charge of Turkey’s banking watchdog, which doesn’t suggest a total break from the past and has confused markets.

The danger is that Erdoğan won’t allow interest rate hikes in the run-up to the local elections in March 2024. On the other hand, voters in cities such as Istanbul and Ankara have been severely affected by inflation. They overwhelmingly voted against Erdoğan in the presidential election, having already handed metropolitan control to the opposition in 2019.

To regain these cities, Erdoğan must tame inflation and alleviate the cost of living crisis. He may also be motivated by a desire to hand a better economy to his preferred successor (likely to be either his son or son-in-law), who might not enjoy his levels of popularity.

Whatever happens, much damage has already been done. The nation’s current GDP per capita is US$10,616 (£8,335), well below its peak of US$12,508 in 2013 (albeit it has grown for the past couple of years). Turkey has lost significant numbers of skilled workers to other countries.

Halting this brain drain, or even reversing it, will be crucial for future economic growth. This seems unlikely under Erdoğan’s leadership. Avoiding a financial crisis is only the first step forward.![]()

About the Author:

Cem Soner, Doctoral Researcher in Finance, Bangor University

This article is republished from The Conversation under a Creative Commons license. Read the original article.

- COT Metals Charts: Speculator Bets led by Silver, Gold & Platinum Mar 7, 2026

- COT Bonds Charts: Speculator Bets led by 10-Year Bonds & Fed Funds Mar 7, 2026

- COT Energy Charts: Speculator Bets led by Brent Oil & Heating Oil Mar 7, 2026

- COT Soft Commodities Charts: Speculator Bets led by Corn & Soybean Meal Mar 7, 2026

- Investors run to safe-haven assets amid Middle East escalation Mar 6, 2026

- EUR/USD Under Pressure: Middle East Risks Outweigh All Else Mar 6, 2026

- Bitcoin shows resilience to Middle East events. Oil market stabilizes Mar 5, 2026

- GBP/USD: Market Not Expecting BoE Rate Cut in March Mar 5, 2026

- Brent headed for $100? Mar 4, 2026

- Global stock indices continue sell-off due to Middle East conflict Mar 4, 2026