After yesterday’s slightly disappointing US inflation data release, markets are in wait-and-see mode about how the Fed addresses rising price pressures. Inflation expectations are moving higher which means the world’s most important central bank may struggle to continue arguing that they are well anchored.

The dollar is consolidating yesterday’s selloff while stock markets and bond markets have breathed a collective sigh of relief that inflation didn’t accelerate even further. Value sensitive sectors like materials, industrials and financials outperformed on the day pushing the Dow and S&P500 to fresh record high closes. European bourses had hit multi-year highs yesterday but have opened up mixed so far.

Free Reports:

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

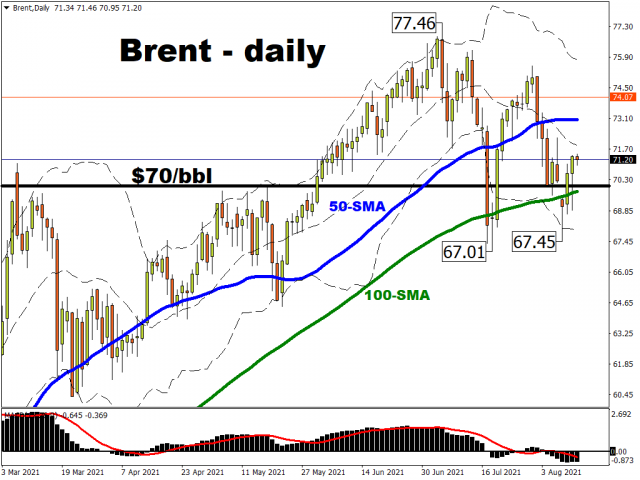

Oil rebounds

It was a volatile day in oil markets with prices moving down towards $69 and then up above $71 on various headlines. The US administration heaped pressure on OPEC and its allies to boost supply to tackle rising gasoline prices. The Biden Presidency wants to see Americans “have access to affordable and reliable energy…at the pump”. Of course interestingly, concerns over rising commodity prices are also being voiced by the Chinese authorities.

The current increase by OPEC+ agreed recently of 400k barrels per day is seemingly not enough. But given the uncertainty around the spread of the Delta variant, it seems unlikely that the Saudis and the oil-producing group will want to increase production just yet. The contradictory nature of Biden policies is also being questioned as it urges greener energy while asking foreign producers to open the taps to lower pump prices.

UK Q2 GDP in line

Hot off the press, second quarter UK GDP has just been released in line with the consensus at 4.8% q/q. Growth is expected to slow again this quarter due to the Delta variant putting the brakes on the economy. But economists hope that the UK should still return to pre-pandemic levels by the end of this year.

With the hawkish noises from the Bank of England last week contrasting heavily with the continued dovish stance of the ECB, EUR/GBP has pushed to new 18-month lows. Prices are now consolidating just below the 0.8471 level and bears expect to see more downside, especially as the ECB engineers a weaker currency. A soft weekly close may start to challenge the 2019 and 2020 lows at 0.8281 and below.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Speculator Bets led by Silver, Gold & Platinum Mar 7, 2026

- COT Bonds Charts: Speculator Bets led by 10-Year Bonds & Fed Funds Mar 7, 2026

- COT Energy Charts: Speculator Bets led by Brent Oil & Heating Oil Mar 7, 2026

- COT Soft Commodities Charts: Speculator Bets led by Corn & Soybean Meal Mar 7, 2026

- Investors run to safe-haven assets amid Middle East escalation Mar 6, 2026

- EUR/USD Under Pressure: Middle East Risks Outweigh All Else Mar 6, 2026

- Bitcoin shows resilience to Middle East events. Oil market stabilizes Mar 5, 2026

- GBP/USD: Market Not Expecting BoE Rate Cut in March Mar 5, 2026

- Brent headed for $100? Mar 4, 2026

- Global stock indices continue sell-off due to Middle East conflict Mar 4, 2026