By Lukman Otunuga Research Analyst, ForexTime

It was a tense week filled with anticipation as investors awaited the U.S. Federal Reserve meeting for clues on future monetary policy.

Despite the quiet start, global stocks hit record highs on Monday as equity bulls drew strength from the transitory inflation narrative. Looking at currency markets, the Euro wobbled above 1.21 while the Dollar Index struggled for direction as market players adopted a defensive approach.

In the United Kingdom, UK Prime Minister Boris Johnson delayed lifting the remaining Covid-19 restrictions until Monday 19th July. We questioned whether this would negatively impact the UK’s economic recovery from the pandemic?

On Tuesday, caution enveloped financial markets even after Wall Street closed at record highs overnight. Ahead of the Fed meeting, attention was directed towards the US retail sales and Producer Price Index (PPI) data. Interestingly, US retail sales declined 1.3% month-over-month in May, reversing from the 0.9% rise witnessed in the previous month while PPI climbed 6.6% on an annual basis.

Our trade of the week was gold which remained shaky ahead of the Fed meeting. The past few days were rough and rocky for precious metal after bulls struggled to build on the momentum beyond the psychological $1900 level. We expected gold to remain highly sensitive to the post-FOMC price movements, especially if there were wild movements in Treasury yields and the dollar.

Free Reports:

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

The wait was nearly over on Wednesday morning.

Investors who were craving for some action and volatility had their wishes fulfilled on Wednesday evening after the Fed dished out a hawkish surprise. Although the central bank kept its policy rates unchanged, it moved up its planned interest rate hikes while raising growth and inflation forecasts. This sent shockwaves across financial markets, turbocharging the Dollar, lifting Treasury yields while dragging US stocks lower.

‘Markets Extra’ Podcast: Fed discos to taper-town!

Digging deeper, the Fed signalled two interest rate hikes by the end of 2023 (from zero in the prior meeting) and opened the debate on when it may be appropriate to start tapering. Growth was estimated to expand 7% this year, up from 6.5% in March’s projection. In regards to Inflation, headline and core PCE are expected to reach 3.4% and 3% in 2021, up from previous estimates of 2.4% and 2.2%.

After being bullied by G10 currencies over the past few months, it may be time for the Dollar to strike back with a vengeance. It has appreciated against every single major currency this week while the Dollar Index (DXY) has gained over 1.8%.

Looking at the technical picture, the DXY has turned bullish on the daily timeframe. A strong weekly close above 92.00 could signal further upside next week. However, a technical pullback towards the 200-day SMA could remain a possibility before bulls strike again.

It was an awful week for the EURUSD as king Dollar was crowned by the Fed. A weekly close below 1.1900 may send prices towards 1.1800 and possibly lower this month.

We saw a similar picture with the GBPUSD. It collapsed like a house of cards with prices trading around 1.3800 as of writing.

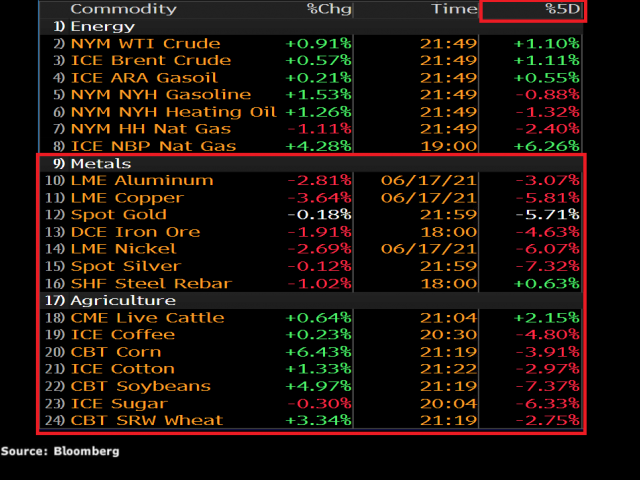

In the commodities arena, gold was a sorry sight to behold. The precious metal stood little chance against a hawkish Federal Reserve and this was reflected in the sharp selloff on Wednesday evening. The toxic combination of an appreciating Dollar, rising bond yields, and prospects of higher interest rates dealt a crippling blow to zero-yielding gold. The precious metal has shed over 5.7% this week and is trading below $1770 as of writing.

Looking at the technical picture, prices are heavily bearish on the daily charts with sustained weakness below $1800 opening the doors to $1750 and possibly lower this month.

Interestingly, the 10-year Treasury yield surrendered its post-Fed meeting gains to trade around 1.46% as of writing. This could be linked to the heavy sell-off in commodities amid actions by China to crackdown on inflation.

Falling commodities tend to lead to higher bond prices, resulting in lower bond yields.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Speculator Bets led by Silver, Gold & Platinum Mar 7, 2026

- COT Bonds Charts: Speculator Bets led by 10-Year Bonds & Fed Funds Mar 7, 2026

- COT Energy Charts: Speculator Bets led by Brent Oil & Heating Oil Mar 7, 2026

- COT Soft Commodities Charts: Speculator Bets led by Corn & Soybean Meal Mar 7, 2026

- Investors run to safe-haven assets amid Middle East escalation Mar 6, 2026

- EUR/USD Under Pressure: Middle East Risks Outweigh All Else Mar 6, 2026

- Bitcoin shows resilience to Middle East events. Oil market stabilizes Mar 5, 2026

- GBP/USD: Market Not Expecting BoE Rate Cut in March Mar 5, 2026

- Brent headed for $100? Mar 4, 2026

- Global stock indices continue sell-off due to Middle East conflict Mar 4, 2026