GM recalls 38,197 cars for battery control defect

Opel expects cheaper car deals after taking finance in-house

What Is General Motor’s Target Demographic?

GM recalls 38,197 cars for battery control defect

Opel expects cheaper car deals after taking finance in-house

What Is General Motor’s Target Demographic?

By CountingPips.com

The Australian dollar has been on the decline today in Forex trading action ahead of Tuesday’s Reserve Bank of Australia (RBA) policy meeting and interest rate decision. The Aussie has fallen against the US dollar, Japanese yen and the European common currency in foreign exchange trading as data published today showed that Australian retail sales unexpectedly contracted in March by 0.4 percent.

Bloomberg data, based on overnight-index swap rates, shows a 53% chance of an interest rate reduction on Tuesday while large money traders, including possibly George Soros, are rumored to be betting on a rate cut.

The AUD/USD in trading today declined and ended the day near the 1.0251 exchange rate level at the New York close of business. This was a decline of approximately 50 pips on the day. The Australian dollar, meanwhile, showed more modest declines against the Japanese yen and the euro today of approximately 25 pips and 30 pips, respectively.

AUD/USD Support & Resistance Levels:

The AUD/USD currency pair trades right near the 1.0250 exchange level at the current time with a downside support level coming into play at 1.0220. This level has provided support numerous times since February while a close below this level would be the lowest close since the beginning of March. Lower downside targets would bring 1.0200 and then 1.0165 to 1.0150 which would be bringing the pair to the lowest levels of 2013.

Upside targets may be capped at the 1.0300 major resistance level that has been an obstacle in the past and features the weekly pivot point very close by. If the pair can get by that obstacle the 1.0325 to 1.0350 resistance will likely come into play.

AUD/USD Changes & Ranges: Past 6 Weeks

| Date | Pct Change | True Range |

| 2013.03.31 | -0.351 | 0.0142 |

| 2013.04.07 | 1.306 | 0.0234 |

| 2013.04.14 | -2.144 | 0.0255 |

| 2013.04.21 | -0.024 | 0.0118 |

| 2013.04.28 | 0.354 | 0.0163 |

| *2013.05.05 | -0.564 | 0.0089 |

* current week so far

Pivots and Trends Data:

Weekly Pivot Point: 1.0295

Monthly Pivot Point: 1.0390

Linear Regression Indicator Trend / Strength Data:

30-day current trend is BEARISH / Trend strength of -230.4 pips

60-day current trend is BULLISH / Trend strength of 52.9 pips

90-day current trend is BEARISH / Trend strength of -36.1 pips

180-day current trend is BEARISH / Trend strength of -49.7 pips

365-day current trend is BULLISH / Trend strength of 239.6 pips

Article by CountingPips Forex Blog, News & Analysis

The Senate has passed a bill that could end tax-free shopping on the Internet for many shoppers. The Senate voted 69 to 27 Monday to pass the bill, sending it to the House. Some video silent. (May 6)

Attention online shoppers: The days of tax-free shopping on the Internet may be coming to an end. The Senate is scheduled to vote Monday on a bill that would empower states to collect sales taxes from online purchases. (May 6)

Tablets, touchscreen computers to power mobile PC market

Warren Buffett: ‘You have to love something to do well at it’

Opel expects cheaper car deals after taking finance in-house

Warren Buffett: ‘Tough to watch’ Washington gridlock

Berkshire Hathaway’s earnings jump 51 percent

Dow 15,000: ?Sometimes a Bullish Market Is Just a Bullish Market?

Warren Buffett offers advice on investing and life

Buffett’s annual meeting

Buffett says he, Berkshire board in agreement on next CEO

Which way were Large Traders and Hedge Funds leaning the previous week in the Futures Market?

By CountingPips.com

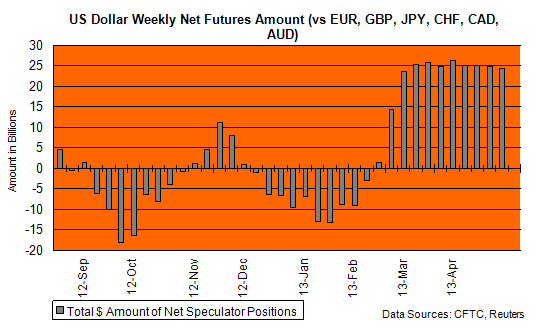

The most recent weekly Commitments of Traders (COT) report, released every Friday by the Commodity Futures Trading Commission (CFTC), showed that large futures traders slightly pulled back on their total bullish bets of the US dollar last week for a second consecutive week.

Non-commercial large futures traders, including hedge funds and large International Monetary Market speculators, totaled an overall US dollar long position of $24.49 billion as of Tuesday April 30th. This was a slight decline from the total long position of $24.94 billion on April 23rd, according to position calculations by Reuters that derives this total by the amount of US dollar positions against the total positions of euro, British pound, Japanese yen, Australian dollar, Canadian dollar and the Swiss franc.

Total US dollar long positions have continued to stay between $23.57 billion and $26.3 billion for the last nine weeks, according to the Reuters calculations. US dollar positions had been in an overall bearish position from November 2012 to February 2012 before turning into a bullish position on February 19th when USD bets equaled $1.481 billion.

What is the COT Report:

The weekly cot report summarizes the total trader positions for open contracts in the futures trading markets. The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

Individual Currencies Large Speculators Positions in Futures:

The individual currency net speculator positions last week saw advances for the euro, Japanese yen, British pound sterling, New Zealand dollar and the Canadian dollar while the Swiss franc, Australian dollar and the Mexican peso all had a declining number of net large trader contracts for the week.

Individual Currency Charts: (Please Click on Chart to Enlarge)

EuroFX: Weekly change of +4,126

EuroFX: Large trader positions for the euro improved last week after showing a decline the previous week. Euro contracts increased to a total net position of -30,149 contracts in the data reported for April 30th following the previous week’s total of -34,275 net contracts on April 23rd.

Last Six Weeks of Large Trader Positions: EURO

| Date | Lg Trader Net | Change |

| 03/26/2013 | -49095 | -4211 |

| 04/02/2013 | -65701 | -16606 |

| 04/09/2013 | -50858 | 14843 |

| 04/16/2013 | -29764 | 21094 |

| 04/23/2013 | -34275 | -4511 |

| 04/30/2013 | -30149 | 4126 |

British Pound Sterling: Weekly change of +1,505

GBP: British pound spec positions improved last week to advance for a third consecutive week and to the best position since March 12th. British pound speculative positions improved last week to a total of -58,607 net contracts on April 23rd following a total of -60,112 net contracts reported for April 16th.

Last Six Weeks of Large Trader Positions: Pound Sterling

| date | Lg Trader Net | Change Weekly |

| 03/26/2013 | -66555 | -5075 |

| 04/02/2013 | -65020 | 1535 |

| 04/09/2013 | -69969 | -4949 |

| 04/16/2013 | -61975 | 7994 |

| 04/23/2013 | -60112 | 1863 |

| 04/30/2013 | -58607 | 1505 |

Japanese Yen: Weekly change of +8,603

JPY: Japanese yen net speculative contracts increased last week for the third consecutive week and to the best level since February 26th. Japanese yen positions increased to a total of -71,127 net contracts on April 30th following a total of -79,730 net short contracts on April 23rd.

Last Six Weeks of Large Trader Positions: Yen

| date | Lg Trader Net | Change Weekly |

| 03/26/2013 | -89149 | -9156 |

| 04/02/2013 | -78171 | 10978 |

| 04/09/2013 | -77697 | 474 |

| 04/16/2013 | -93411 | -15714 |

| 04/23/2013 | -79730 | 13681 |

| 04/30/2013 | -71127 | 8603 |

Swiss Franc: Weekly change of -9,443

CHF: Swiss franc speculator positions declined last week after improving for the previous four consecutive weeks and to the best position since February 12th. Net positions for the Swiss currency futures dropped to a total of -8,264 contracts on April 30th following a total of +1,179 net contracts reported for April 23rd.

Last Six Weeks of Large Trader Positions: Franc

| date | Lg Trader Net | Change Weekly |

| 03/26/2013 | -12198 | -1202 |

| 04/02/2013 | -12015 | 183 |

| 04/09/2013 | -10014 | 2001 |

| 04/16/2013 | -3253 | 6761 |

| 04/23/2013 | 1179 | 4432 |

| 04/30/2013 | -8264 | -9443 |

Canadian Dollar: Weekly change of +3,831

CAD: Canadian dollar positions improved slightly last week for a second consecutive week after falling to a new low level for 2013 on April 16th. Canadian dollar positions improved to a total of -67,848 contracts as of April 30th following a total of -71,679 net contracts that were reported for April 23rd.

Last Six Weeks of Large Trader Positions: CAD

| date | Lg Trader Net | Change Weekly |

| 03/26/2013 | -62645 | 2686 |

| 04/02/2013 | -64544 | -1899 |

| 04/09/2013 | -71133 | -6589 |

| 04/16/2013 | -75913 | -4780 |

| 04/23/2013 | -71679 | 4234 |

| 04/30/2013 | -67848 | 3831 |

Australian Dollar: Weekly change of -1,023

AUD: The Australian dollar large speculator positions fell slightly again last week to decline for a fifth consecutive week. Aussie speculative futures positions decreased to a total net amount of +30,234 contracts on April 30th after totaling +31,257 net contracts as of April 23rd.

Last Six Weeks of Large Trader Positions: AUD

| date | Lg Trader Net | Change Weekly |

| 03/26/2013 | 85515 | 31460 |

| 04/02/2013 | 83971 | -1544 |

| 04/09/2013 | 77879 | -6092 |

| 04/16/2013 | 53175 | -24704 |

| 04/23/2013 | 31257 | -21918 |

| 04/30/2013 | 30234 | -1023 |

New Zealand Dollar: Weekly change of +1,345

NZD: New Zealand dollar speculator positions rose last week to just under the 2013 high level of April 16th. NZD contracts increased to a total of +29,050 net long contracts as of April 30th following a total of +27,705 net long contracts on April 23rd.

Last Six Weeks of Large Trader Positions: NZD

| date | Lg Trader Net | Change Weekly |

| 03/26/2013 | 16916 | 4439 |

| 04/02/2013 | 18387 | 1471 |

| 04/09/2013 | 25150 | 6763 |

| 04/16/2013 | 30808 | 5658 |

| 04/23/2013 | 27705 | -3103 |

| 04/30/2013 | 29050 | 1345 |

Mexican Peso: Weekly change of -8,360

MXN: Mexican peso speculative contracts decreased lower last week for the second consecutive week. Peso positions declined to a total of +138,551 net speculative positions as of April 30th following a total of +146,911 contracts that were reported for April 23rd.

Last Six Weeks of Large Trader Positions: MXN

| date | Lg Trader Net | Change Weekly |

| 03/26/2013 | 128162 | 18786 |

| 04/02/2013 | 142755 | 14593 |

| 04/09/2013 | 142542 | -213 |

| 04/16/2013 | 151288 | 8746 |

| 04/23/2013 | 146911 | -4377 |

| 04/30/2013 | 138551 | -8360 |

The Commitment of Traders report is published every Friday by the Commodity Futures Trading Commission (CFTC) and shows futures positions data that was reported as of the previous Tuesday (3 days behind).

Each currency contract is a quote for that currency directly against the U.S. dollar, a net short amount of contracts means that more speculators are betting that currency to fall against the dollar and a net long position expect that currency to rise versus the dollar.

(The graphs overlay the forex spot closing price of each Tuesday when COT trader positions are reported for each corresponding spot currency pair.)

See more information and explanation on the weekly COT report from the CFTC website.

Article by CountingPips.com – Forex News & Market Analysis

Buffett says he, Berkshire board in agreement on next CEO

Berkshire Hathaway’s earnings jump 51 percent

Berkshire’s Munger says takeover prices look very high

Berkshire Hathaway’s earnings jump 51 percent

Wall Street sees Fed buying $1.25 trillion of assets in stimulus

Big four U.S. brokerage firms are thriving, not diving: report