By CountingPips.com

The latest Commitments of Traders (COT) report, released on Friday by the Chicago Mercantile Exchange, showed that futures speculators slightly pared their bets in favor of the euro and the other major currencies against the US dollar. Non-commercial futures positions, those taken by hedge funds and large speculators,were overall net short the US dollar by $29 billion against the other major currencies, down from a total short position of $30.5 billion on October 5th, according to data published by Reuters.

Currency speculators were net long the euro against the U.S. dollar by 41,511 contracts as of October 12th. This is a decline of nearly 7,000 contracts following net long positions of 48,243 contracts on October 5th and breaks a string of five straight weeks of improving positions for the euro.

The COT report is published every Friday by the Chicago Mercantile Exchange (CME) and shows futures positions as of the previous Tuesday. It can be a useful tool for traders to gauge investor sentiment and to look for potential changes in the direction of a currency or commodity. Each currency contract is a quote for that currency directly against the U.S. dollar, where as a net short amount of contracts means that more speculators are betting that currency to fall against the dollar and net long position expect that currency to rise versus the dollar. Open interest is the number of open contracts that have not been closed by a transaction or by delivery.

The British pound sterling had been the last major currency on the short side against the dollar in the CME futures market but in early October the British currency positions changed to a positive net amount of contracts. The euro, Australian dollar, New Zealand dollar, Japanese yen, Canadian dollar, Swiss franc and Mexican peso all continued to have a net positive amount of contracts.

The British pound sterling positions fell slightly to a net of 8,066 contracts after being long on October 5th by 9,403 positions. The latest data interrupts a streak of four straight weeks of improvement for the British pound future positions and brings positions off the best showing for GBP contracts in over a year.

The Japanese yen net long contracts decreased slightly to 48,285 as of October 12th from 49,206 net long contracts reported on October 5th. Yen positions had climbed for two straight weeks after a notable decline on September 21st as many speculators may have decreased their yen long positions due to the Bank of Japan’s currency intervention.

The Canadian dollar positions increased higher for a second straight week to a net total of 43,786 contracts after totaling 42,678 net longs on October 5th and rose to their highest level since May.

Swiss franc long positions declined to 19,947 long contracts as of October 12th after totaling a net of 22,599 long contracts on October 5th. This reverses three straight weeks of increases that brought the Swiss franc positions to their highest level since early in December 2009 when long contracts totaled 24,725.

The Australian dollar positions edged very slightly lower for second straight week after reaching their highest level since April on September 28th. AUD futures contracts declined to a net amount of 67,691 long contracts as of October 12th from 69,036 long contracts on October 5th.

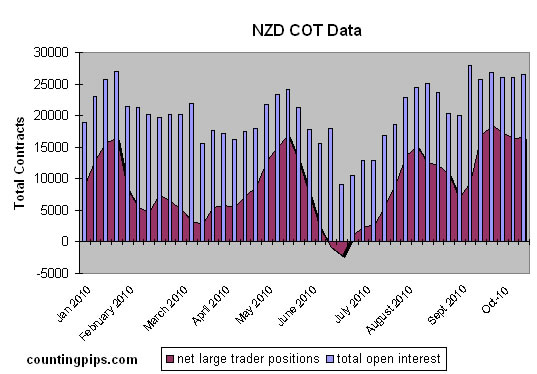

New Zealand dollar futures positions edged slightly higher to a total of 16,573 long contracts after a total of 16,334 long contracts the week before.

Mexican peso long contracts also edged just slightly higher as of October 12th to 86,218 net long positions from 85,764 longs the week prior. Peso positions are at their highest since May and have now risen for five consecutive weeks.

COT Data Summary as of October 12th, 2010

Large Speculators Net Positions vs. the US Dollar

Euro: +41,511 contracts from +48,243 contracts on October 5th

British pound sterling: +8,066 contracts from +9,403 contracts

Australian dollar: +67,691 contracts from +69,036 contracts

Canadian dollar: +43,786 contracts from +42,678 contracts

Japanese yen: +48,285 contracts from +49,206 contracts

Mexican peso: +86,218 contracts from +85,764 contracts

New Zealand dollar: +16,573 contracts from +16,334 contracts

Swiss franc: +19,947 contracts from +22,599 contracts

Go to the Commitment of Traders CME raw futures data

Further COT Resources from around the web:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}