Source: Economic Events May 18, 2020 – Admiral Markets’ Forex Calendar

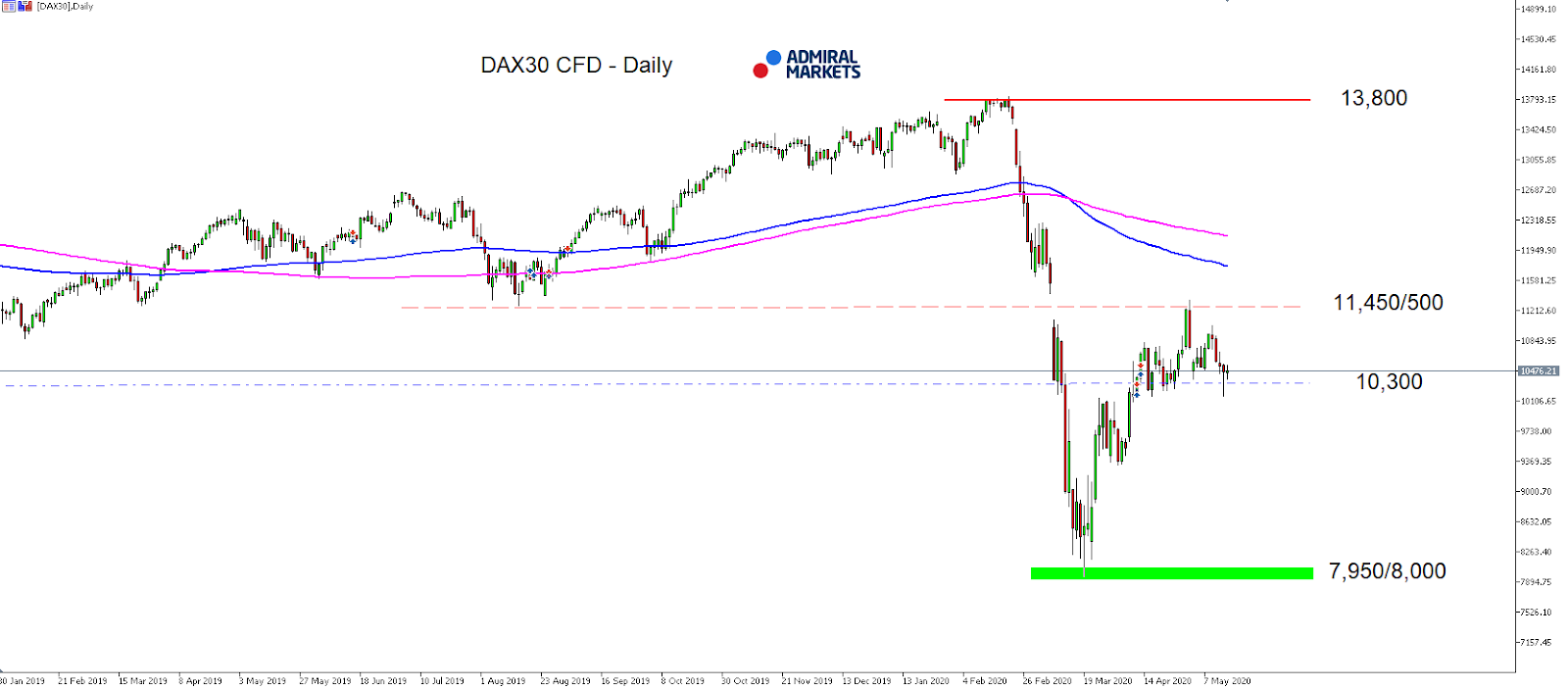

The DAX30 ended last week on a little roller coaster. After a sharp drop last Thursday, where the German index attacked the region around 10,200 points. It can hold that level, thanks to massive support and a sharp bounce in US Equities.

But when carefully looking at the short-term hourly picture, and assessing the sequence of falling highs and lows over the course of last week, the mode remains short-term bearish below 10,700 points.

While we have to wait to see whether there will be a volatile start to the week as there is a thin economic calendar, but we’d still be careful with long engagements. In fact, we’d consider Short engagements more attractive from a risk-reward perspective.

That is especially true after last Wednesday’s comments from Fed chairman Powell, where he noted that the recovery of the US economy may take time to gather momentum.

He could have said that a V-shaped recovery in the US (but also globally) is off the table.

And with expected earnings for the S&P 500 being 28% down from their peak, and 13% below realized earnings (which is way less than during previous recessions and can only be justified by a massive V-shaped recovery in earnings in 2021), US Equities, but also Equities in general including the German DAX, seem to be overvalued, and a next sharper leg lower stays a serious option.

Technically, the DAX30 CFD stays at least neutral as long as we can hold above 10,200 points, but a break lower activates 9,600 points as target on the downside in the days to come:

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Hourly chart (between April 27, 2019, to May 15, 2020). Accessed: May 15, 2020, at 10:00pm GMT

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Daily chart (between January 30, 2019, to May 15, 2020). Accessed: May 15, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of the DAX30 CFD increased by 9.56%, in 2016, it increased by 6.87%, in 2017, it increased by 12.51%, in 2018, it fell by 18.26%, in 2019, it increased by 26.44% meaning that after five years, it was up by 34.2%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

- This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

- Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

- Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

- To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

- Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

- The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

- Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

- The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.