Investors across the globe have been injected with a renewed dose of confidence towards risk as governments relax lockdown measures and first human trial results raise hopes for a coronavirus vaccine.

The mood across Asian markets is quite encouraging and this positive vibe should support European shares later this morning. However, questions should be raised over the sustainability of the current rally and return in risk sentiment given how US-China trade tensions have made an unwelcome return. Concerns remain elevated over slowing global growth despite countries easing lockdown measures while fears rise around a second wave of coronavirus infections.

Global equity bulls may be in the driving seat for now, but bears are lurking around the corner waiting for another opportunity to pounce.

King Dollar to maintain grip on iron throne

The mighty Dollar should reign supreme this week despite the semblance of stability enveloping financial markets.

Although investors are clearly hopeful over economies re-opening after an extended lockdown period, global macroeconomic conditions remain depressing while renewed trade tensions are bound to hit sentiment. As risk aversion makes a return and market players rush towards safety, one of the first destinations is likely to be the Dollar.

Looking at the technical picture, the Dollar Index is experiencing a technical correction on the daily charts with prices trading below 99.50. Sustained weakness below this level may give way towards 99.00. Should this level prove to be reliable support, prices could rebound back towards 99.50 and 101.00.

Another day, same old story for Pound

The path ahead for the British Pound is filled with many obstacles and dead ends as fears over a no-deal Brexit return to the scene.

One can’t help but feel a familiar sense of déjà vu as the UK government prepares for its final round of talks scheduled in June to try and avert a no-deal Brexit outcome. To rub salt into the wound, economic data from the United Kingdom remains discouraging with the number of people claiming unemployment benefits soaring to 2.097 million in April.

With the fundamentals not in favour of the Pound, it may be only a matter of time till the technical paint a similar picture. The GBPUSD is under pressure on the daily charts and may trend lower if prices break below 1.2200. Sustained weakness below this level could open the doors towards 1.2000.

Euro eyes 1.10 but upside capped by fundamentals

Where the Euro concludes this week will be heavily influenced by the pending Purchasing Managers Index data scheduled for release over the coming days.

A disappointing set of economic data may put an end to the current rally with 1.1000 acting as a ceiling. Looking at the technical picture, the EURUSD remains a wide range on the daily charts with support at 1.0770 and resistance 1.1000. Expect the currency pair to find comfort within these levels until a decisive breakout is achieved.

Commodity spotlight – Gold

Gold should remain in fashion despite stock markets rising and economies easing lockdown measures.

The precious metal remains supported by global growth fears, lower interest rates across the globe and fears around a second wave of coronavirus outbreak. Gold is trading at levels not seen in more than 7 years above $1430 and has gained over 14% year-to-date. A solid daily close above $1430 may pave the way back towards $1765 and $1770. Alternatively, sustained weakness below $1720 could open the doors back towards $1700.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Improving ZEW economic sentiment for Germany bullish for EURUSD

The ZEW Indicator of Economic Sentiment for Germany recorded an increase for the second time: it rose to 51 points after edging up to 28.2 in April, when an increase to 30 was expected. Readings above 0.0 indicate optimism, below indicate pessimism. This is bullish for EURUSD.

Global equities are gaining today as worries about a second wave of coronavirus cases were offset by reports drug maker Moderna has recorded positive, early results from first human trial of its experimental Covid-19 vaccine. Treasury Secretary Mnuchin and Federal Reserve Chair Powell are expected to testify before the Senate Banking Committee on what further aid is required for the economy amid calls to extend the $660 billion Paycheck Protection Program.

Forex news

Currency Pair

Change

EUR USD

+0.17%

GBP USD

+0.38%

USD JPY

+0.1%

AUD USD

+0.47%

The Dollar weakening continues today ahead of housing starts and building permits reports due later today. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, fell 0.8% Monday. GBP/USD joined EUR/USD’s continued climbing Monday with both pairs higher currently. AUD/USD joined USD/JPY’s continuing climbing yesterday and both pairs are up currently.

Stock Market news

Indices

Change

Dow Jones Index

+0.1%

Nikkei Index

+1.69%

Hang Seng Index

-0.33%

Australian Stock Index

-1.14%

Futures on three main US stock indexes are gaining currently after ending sharply higher Monday as Fed chair Powell reiterated that the central bank would use its “full range of tools tool” to aid the economy. President Trump said an extension of the $660 billion Paycheck Protection Program “should be easy.” Walmart, JP Morgan and Home Depot are among companies reporting quarterly results today while more states are reopening economies and California relaxes reopening rules. Stock indexes in US rallied on Monday: the three main US stock indexes posted gains ranging from 2.4% to 3.9%. European stock indexes are rising currently after sharp gains Monday. German Chancellor Merkel and French President Macron announced a 500 billion euro ($545 billion) debt-backed plan to provide grants, rather than loans, for “the most affected sectors and regions based on EU budget programs and in line with European priorities.” Asian indexes are mostly higher today. Hong Kong’s Hang Seng Index is leading advancers with 2.2% gain despite Nasdaq plans to toughen rules that could make it harder for Chinese companies to list on its exchange.

Commodity Market news

Commodities

Change

Brent Crude Oil

-1.54%

WTI Crude

-1.29%

Brent is edging lower today. Oil prices rallied on Monday against the background of report crude oil production from seven major US shale plays is forecast to decline by 197,000 barrels a day in June to 7.822 million barrels a day, according to the Energy Information Administration. The US oil benchmark West Texas Intermediate (WTI) futures jumped Monday: July WTI gained 7.2% but is falling currently. July Brent crude climbed 7.1% to $34.83 a barrel.

Gold Market News

Metals

Change

Gold

-0.07%

Gold prices are rebounding today. June gold lost 1.3% to $1734.40 an ounce on Monday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Given the widespread COVID-19 induced downturn, I struggled with the outlook for copper. I feared that like stock markets in March, the copper price might collapse. That didn’t happen. Either due to producer discipline or governments halting operations, a fair amount of world supply has been curtailed indefinitely.

It may turn out that COVID-19 has as big an impact on supply as it does on demand. Copper is trading at US$2.35/lb, ~14% below its average price in 2019. So, not the end of the world.

I came to terms with Dr. Copper by learning that massive, multi-year, global stimulus packages are in the works. In total, probably US$10 or US$20 trillion over the next few years. Much of it will go to copper-intensive infrastructure projects. Furthermore, growing end market demand from the electrification of transportation remains in place.

But enough about copper, today’s gold price is a BIGGER story, currently at US$1,740/oz, 25% above its average price in 2019. New discoveries that contain meaningful gold values will be handsomely rewarded.

In particular, discoveries in globally significant jurisdictions, made by world-class teams, on projects with tremendous blue-sky potential could generate substantial share price gains. With this in mind, I circle back to a small copper & gold story that has all the ingredients for an exciting discovery.

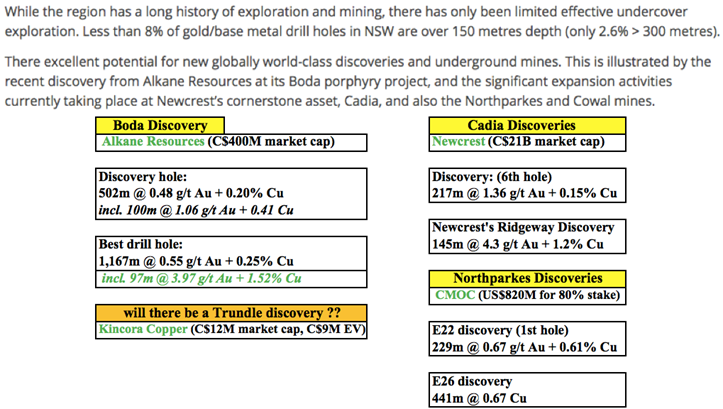

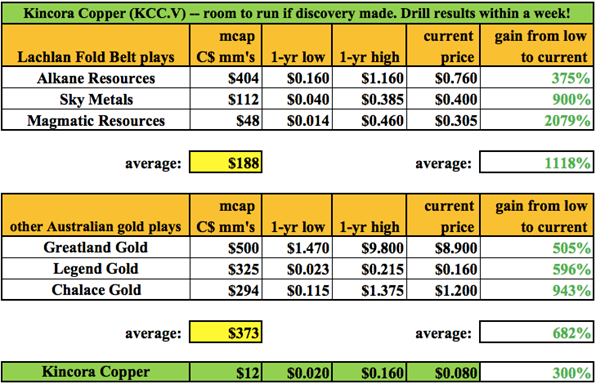

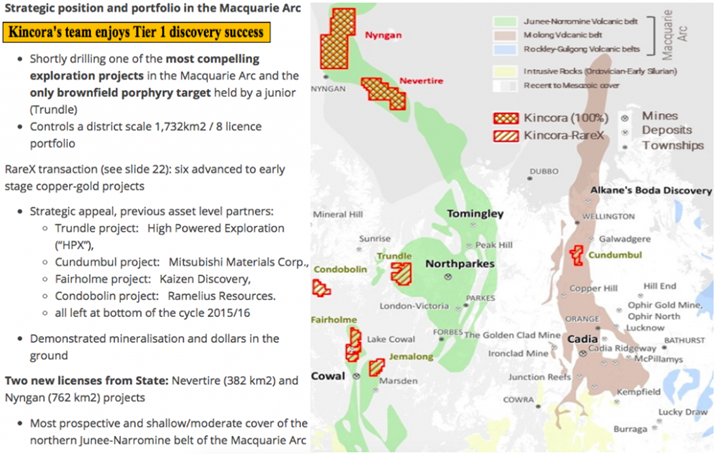

Could Kincora Copper Ltd. (KCC:TSX.V) be the comeback resource junior of the year? After a disappointing drill program in Mongolia, management switched gears, jumping on a compelling opportunity in Australia, just before new discoveries were made all around them. The company is currently drilling its Trundle project in New South Wales (NSW).

It’s worth noting that Trundle is the only brownfield project in the area controlled by a listed junior. Kincora’s enterprise value {market cap (C$12 million) + debt (zero) cash (C$3 million) = C$9 million/US$6.4 million.

Trundle is in an exploration hotspotthe Macquarie Arc (MA) of the Lachlan Fold Belt (LFB). The MA hosts major porphyry deposits, including Newcrest Mining’s company-maker, underpinning it becoming Australia’s largest gold miner, Cadia {913k ounces gold (2019) at AISC of US$ 132/oz net of credits}; Evolution Mining’s flagship Cowal project {251.5k ounces gold (2019) at AISC of ~US$ 675/oz}; China Molybdenum’s (CMOC) copper-gold Northparkes {~240k Au Eq ounces/year}; and Alkane Resources’ Boda {discovery hole: 502 m at 0.48 g/t Au + 0.2% Cu}.

Kincora controls a district-scale 1,732 sq km land position in a few key belts within the MA. Management’s first press release on its Australian activities was on November 21st. Since then, gold is up ~24% to over AUD$ 2,700/oz.a record price. There’s also been significant drill program successes by peer LFB juniors {most notably, Alkane Resources, but also Sky Metals and Magmatic Resources}.

Alkane reported a blockbuster intercept at its Boda project; 96.8m @ 4 g/t Au + 1.52% Cu (~5.4 g/t Au Eq) from 768-meter depth. It also has a 3035k ounce/year producing gold mine and a market cap of ~C$400million. Alkane has the financial ability to aggressively drill out the Boda deposit. A follow-up second phase drill program leading to a maiden resource would be great news for Alkane and neighboring peers including Kincora Copper.

Sky Metals, with a market cap of ~$110 million, has two tin-tungsten-silver projects and two gold projects in the LFB. Its gold discovery really got the share price moving. Sky has some good intercepts, but nothing like Alkane’s.

Magmatic Resources has a market cap of ~$50 million. It has land holdings in the LFB totaling 1,054 sq km vs. 1,732 sq km controlled by Kincora, and is a “nearlogy” exploration play to Alkane’s Boda, as Kincora is to CMOC’s Northparkes. Due in part to Alkane’s success, Magmatic had one of the largest percentage gains of any gold junior on the planet. From 2c to 46c over six months, and recently back to 31c.

Sky Metals and Magmatic Resources, with an average market cap of ~$75 million, are reasonable comps to Kincora’s $12 million pre-discovery valuation. All three are pre-maiden resource or confirmation of an economic discovery hole. Other exploration success stories in Australia, such as Greatland Gold, Legend Mining and Chalice Gold, also demonstrate the power of new discoveries. There’s plenty of run room if management hits pay dirt. A drilling update is expected within a week or so.

There are fewer than two dozen gold/copper (or copper/gold) juniors that have flagship projects in NSW. All but three are Australian-listed. Kincora Copper (TSX-V: KCC) is a good way for North American investors to gain exposure to the LFB.

Kincora has ~$3 million in cash, strong drill targets, (derived from robust prior exploration efforts, plus new studies) and a tremendous management/technical team plus advisors. In addition to the tireless efforts since 2012 of Kincora’s CEO Sam Spring {full bio here}, three additional world-class team members are actively involved, Independent Director & Chairman of the Technical Committee John Holliday, Senior VP Exploration Peter Leaman and Chairman Cameron McRae.

John Holliday has >30 years’ experience in exploration, mostly with BHP and Newcrest Mining, including as chief geoscientist and general manager. He has been working with Kincora since 2015. John has a successful track record in global gold-copper exploration, discovery and evaluation. He was a principal discoverer of the Tier-1 Cadia gold-copper porphyry and Marsden copper-gold porphyry in the LFB, and a geological advisor on the acquisition of many significant projects. {full bio here}

Peter Leaman has >40 years’ experience in exploration, mostly with BHP and PanAust Ltd., where he was regional exploration manager for SE Asia. He’s a hands on, target-orientated leader responsible for project generation and managing exploration programs, resulting in notable discoveries including the Tier 1 Reko Diq porphyry Cu/Au deposit, Crater Mountain epithermal Au/Ag and the Mt. Bini (Kodu) porphyry Cu/Au deposits in Papua New Guinea, among others. {full bio here}

Cameron McRae is a very seasoned mining executive. He had a 28-year career with Rio Tinto and in Mongolia was president of Oyu Tolgoi and Rio Tinto’s country director. McRae led the construction and start-up of the US$6 billin Oyu Tolgoi copper mine and was responsible for safety, strategy, operations and growth initiatives. He has led successful greenfield and brownfield projects, has deep commercial/M&A experience and has sat on numerous exploration and technical committees. {full bio here}

Truly a tremendous team with direct experience, in the right place, at the right time, especially for a company with such a modest enterprise value. As of April 22nd, phase 1 drilling at Trundle has commenced. This phase includes a six hole/~3,800-meter (~630 meters/hole) program, testing three large mineralized zones at greater depths.

The company expects this program to be “high impact, value-add drilling,” as Trundle has “excellent potential for new high-grade porphyry & skarn copper-gold discoveries.”

Regarding the drill program, John Holliday and Peter Leaman commented,

“Modern systematic exploration at Trundle has utilized industry leading IP surveys, including HPX’s proprietary Typhoon system, and magnetic modeling which has been insufficiently followed up by drilling. Existing significant drill intersections support vectoring to very compelling targets at existing mineralized systems within a brownfield environment to Northparkes, Australia’s second largest porphyry mine where five deposits are defined.”

Trundle is 30 km west of CMOC’s Northparkes copper-gold project, Australia’s second largest porphyry mine (behind Newcrest’s Cadia, also in the Macquarie Arc). CMOC acquired an 80% interest in Northparkes in 2013 for US$820 million and has since expanded production and extended the mine life.

Historically an important agricultural hub, substantially increased mining activity in the region has led to favorable infrastructure improvements (power, roads, rail, etc.. This will likely continue as iron ore giant Fortescue Metals ($34 billion market cap) has secured property, including parcels adjacent to Kincora’s southern border of Trundle. Newmont, Gold Fields and Freeport-McMoRan are also exploring in the LFB.

The Trundle project hosts extensive evidence of porphyry and skarn-style copper-gold mineralization across 12.5 km strike length and shares some geological features with Northparkes and Cadia. Results of surface geological mapping, geochemistry, magnetic, gravity and IP coverage, coupled with structural and basement rock interpretations, have been promising.

Past drilling totaled 2,208 holes for 61,146 meters. Only limited modern exploration and very little deep drilling into basement rocks has been done. Importantly, over 92% of historical drilling has been to <50 meters in depth. Just 11 holes have been >300m (~0.5% of total holes drilled). Where the first hole is being drilled, the average drill hole depth is only 28 meters.

Shallow intercepts not followed up on include: [60m @ 0.54g/t Au from 1m], [56m @ 0.88g/t Au + 0.35% Cu from 34m, incl. 2m @ 20g/t Au + 7% Cu & 81g/t Ag from 64m depth], [39m @ 0.55 g/t Au + 0.14% Cu from surface], [35m @ 0.55 g/t Au + 0.25% Cu from 12m], [51m @ 0.58 g/t Au + 0.14% Cu from 33m], [58m @ 0.44 g/t Au + 0.17% Cu from 22m, including 4m @ 1.19g/t Au + 0.41% Cu from 28m]. Note: at spot Au prices, the avgerage grade of 0.6 g/t = nearly $50/tonne, which is good for these shallow depths. Additional high-grade hits, like the 2m @ 20g/t Au (with 7% Cu) would gain a lot of attention in the currently hot gold market.

Deeper core drilling has commenced at the Trundle Park zone on the southern end of the property. Management sees real potential for higher-grade porphyry and skarn copper-gold discoveries. Prior activities intersected, “high-grade localized zones, within a large lower-grade magnetite skarn, similar in style to the Big Cadia skarn, and peripheral to the Cadia porphyry copper-gold deposits.”

Kincora is drilling three fences to test known mineralized porphyry targets analogous to the five identified deposits at Northparkes. Existing intercepts support vectoring to compelling drill targets at the existing systems. No drilling has taken place at the project since 2015, while the Mordialloc target hasn’t seen drilling since 2008.

No drilling has yet tested below the zones, where geophysics and re-logging of historical data has indicated proximity to a porphyry source. Despite a lot of smoke, the potential source has yet to be found.

CEO Spring sums things up,

“With previous drill results, existing untested geophysical surveying and being in a brownfield environment, there’s a strong argument that we have comparable, if not a bit more, smoke at Trundle than Alkane had before its breakthrough drill results at Boda. Boda is the best greenfield discovery in the belt in over 20 years and, before the pull back in the market because of COVID-19, was the catalyst for approximately A$400 million being added to Alkane’s market cap in this rising gold price environment“.

While there are no guarantees when it comes to high-impact exploration of Tier 1 assets, Kincora Copper (TSX-V: KCC) has the foundation for success and a cheap valuation, providing investors an interesting risk-adjusted return opportunity.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Kincora Copper, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Kincora Copper are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Kincora Copper was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Newmont Goldcorp, a company mentioned in this article.

Shares of Allogene Therapeutics traded higher and reached a new 52-week high price after the company reported initial results from its Phase 1 relapsed/refractory non-Hodgkin lymphoma trial.

Clinical-stage biotechnology company Allogene Therapeutics Inc. (ALLO:NASDAQ), which develops allogeneic CAR T (AlloCAR T) therapies for cancer together with its partner independent international pharmaceutical company Servier, announced “the release of the abstract related to an upcoming oral presentation at the American Society of Clinical Oncology (ASCO) Annual Meeting.” The company stated that it will present the first data from its Phase 1 dose escalation ALPHA study of ALLO-501 in relapsed/refractory non-Hodgkin lymphoma (NHL) at the virtual meeting. The firm advised that the study is evaluating Allogene’s ALLO-647, an anti-CD52 monoclonal antibody (mAb), as a part of its differentiated lymphodepletion regimen.

The company’s EVP of R&D and Chief Medical Officer Rafael G. Amado, M.D., commented, “As we look ahead to the end of the month to the virtual ASCO meeting, we are excited to present initial clinical data from our first-in-human study of ALLO-501 and ALLO-647…These findings will provide an early glimpse into the potential of our AlloCAR T pipeline and ALLO-647 based lymphodepletion strategy, which we believe will be foundational in driving the future success and broad applicability of AlloCAR T therapies.”

The company advised that the ASCO abstract includes the initial data for the first nine subject patients treated with escalating doses of ALLO-501 and lower dose ALLO-647 and noted that no dose limiting toxicities or graft-vs-host disease was observed in the preliminary results.

The firm explained that its virtual presentation to the ASCO will include data on 11 patients across ALLO-501 cell dose cohorts and lower dose ALLO-647 patients and will also include those patients treated with ALLO-501 and the higher dose ALLO-647. The company indicated that it is continuing to enroll patients in the Phase 1 ALPHA study with higher dose ALLO-647 in an effort to optimize lymphodepletion.

Allogene advised that the Phase 1 trial is designed to assess the safety and tolerability at increasing dose levels of ALLO-501 and ALLO-647 in patients with relapsed/refractory diffuse large B-cell lymphoma and follicular lymphoma.

The company stated that “it expects to initiate enrollment in ALPHA2, a Phase 1 trial with abbreviated dose escalation of ALLO-501A, in Q2/20 and noted that ALLO-501A is the next generation of ALLO-501, which eliminates the rituximab recognition domains, and it is intended for Phase 2 development.”

Allogene reported that “its AlloCAR T programs utilize Cellectis technologies and that ALLO-501 is an anti-CD19 allogeneic CAR T (AlloCAR T) therapy being jointly developed under a collaboration agreement between Servier and Allogene based on an exclusive license granted by Cellectis to Servier.”

Allogene Therapeutics is a clinical-stage biotechnology company based in South San Francisco, Calif., that is engaged in developing allogeneic chimeric antigen receptor T cell (AlloCAR T) therapies for cancer. The firm mentioned it is building “a pipeline of “off-the-shelf” CAR T cell therapy candidates with the goal of delivering readily available cell therapy on-demand, more reliably, and at greater scale to more patients.”

Servier is an international pharmaceutical company headquarters in Suresnes, France. The company stated that it employs 22,000 people globally in 149 countries and posted total revenues of 4.6 billion euros in 2019. The firm reported that it invests 25% of its total revenues on average in research and development and focuses its efforts in the areas of cardiovascular, immune-inflammatory and neurodegenerative diseases, cancer and diabetes and additionally is active in commercializing high-quality generic drugs.

Allogene Therapeutics began the day with a market capitalization of around $3.9 billion with approximately 125.3 million shares outstanding and a short interest of about 10.5%. ALLO shares opened 17% higher today at $36.34 (+$9.32, +17.30%) over yesterday’s $30.98 closing price and reached a new 52-week high price this morning of $41.74. The stock has traded today between $35.77 and $41.74 per share and is currently trading at $40.98 (+$10.01, +32.30%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

The Gold Anti-Trust Action Committee (GATA) today asked the U.S. Commodity Futures Trading Commission (CFTC) whether it has ever audited the gold reported to it by the New York Commodities Exchange as being eligible or registered for sale and delivery on the exchange.

In a letter to commission Chairman Heath P. Tarbert, Chris Powell and Harvey Organ wrote:

“Recent turmoil in the gold markets in the United States and the United Kingdom has raised questions about the integrity of certain market participants, including the New York Commodities Exchange (Comex) and the London Bullion Market Association.”

The letter asked:

“– Has your commission ever audited the gold kept in Comex-approved vaults and reported to the commission as registered or eligible for sale and delivery?

“– If such audits have been conducted, when and what did they find?

“– Who conducted these audits?

“– Were these audits ever made public? If so, when and how? May we see them?

“– Are future audits planned? If so, when and who will conduct them?”

In recent years, GATA has put similar critical questions to the CFTC without getting answers. Several of those questions have been pressed by U.S. Rep. Alex X. Mooney, R-West Virginia, but the commission has evaded his inquiries too.

Especially avoided lately by the commission are whether it is is aware of futures market trading by the U.S. government, its agents, and other governments, and whether it has jurisdiction over manipulative trading by the U.S. government.

While the commission refuses to answer whether it is aware of futures trading by governments, filings by CME Group, operator of the New York Commodities Exchange, with the CFTC and the U.S. Securities and Exchange Commission show that CME Group provides special discounts to governments and central banks for surreptitious futures trading.

By Jameel Ahmad, Global Head of Currency Strategy and Market Research at FXTM

This market simply doesn’t add up.

Investors are happy to add risk into portfolios with stocks and oil prices cheering this sentiment but at the same time, gold has reached its highest level since October 2012. This is not a relationship that we expect and it is unusual for there to be a limited discussion about it.

Warnings about the risk of a second wave of coronavirus disease infections, the long-term economic damage as well as the loss of economic productivity today is all music to the ears of Gold investors. But, investors are also very excited about vaccine hopes and economies reopening. For better or for worse, this element of risk sentiment questions whether the blast higher in Gold can be sustained.

While there are a lot of reasons for investors to stay positive on Gold, we would require a close above $1750 to receive further encouragement that this rally can last.

Although this rally for stronger risk appetite as well as oil prices suggests that commodity currencies would provide an interesting option to an investor’s portfolio at present. The Australian Dollar has surged by just above 100 pips today and the Daily chart suggests AUDUSD could attempt a further rally. If AUDUSD is able to break above 0.6569 it suggests that the pair will attempt to advance to levels not seen since the first half of March 2020.

(AUDUSD Daily FXTM MT4)

The Canadian Dollar is another commodity currency that looks interesting. USDCAD is 120 pips away from the bottom of a range that has been in play for just over a month. Should USDCAD drop below 1.3848 the pair could attempt to recover losses in the Canadian Dollar that have transpired since the coronavirus was named as a global pandemic.

(USDCAD Daily FXTM MT4)

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Sector expert Michael Ballanger expands on both the latest money market moves and his investment thesis for Getchell Gold.

I was pacing around the house this lovely but cold Friday afternoon (after finally having the water supply restored after our well filed for unemployment benefits), trying desperately to think of a topic to write about in this weekly missive, when it suddenly occurred to me that there is not exactly a great deal of fuel for the fire right now. After we got the “20.5 million unemployed” and a 14.7% unemployment rate at 8:30 a.m., the New York Fed proceeded to do the following:

juice the S&P futures;

slam gold; and

crush VIX futures.

The resulting trading action was about as bizarre as one could ever have imagined, as stocks roared out of the gate and never looked back, going out on the highs with traders saying their prayers while bowing in the direction of the Eccles Building in Washington, D.C. They then laid floral bouquets at the entrance to 133 Liberty Street, in an homage dutifully paid to the portfolio-saving efforts of the New York Fed.

As the four o’clock bell rang and the screens on my three quote monitors settled down to nothingness, I found myself staring blankly at the picture of Federal Reserve Chairman Jerome Powell holding court with the financial media earlier in the week, thinking, “That guy is no economist; he is a former investment banker turned carnival barker pitching the world on Wall Street banking’s vision of the future.”

Despite enjoying one of the most profitable years (thus far) of my forty-plus-year career, I find myself saddened by the events of 2020, not only for the heartbreak and hardships brought on by the pandemic, but alsoand even greater than the loss of life and jobs and wealth it has causedbecause of an even greater tragedy: the final destruction of the free market.

I am hard-pressed to find one market in the world today where prices are determined by the unimpeded and unmanipulated forces of demand and supply. Whether it is the floor of the Chicago Mercantile Exchange or the livestock auctions in Spain or estate sales at Sotheby’s in London, the fruits of our laborthe purchasing power of our savingsis being systematically destroyed.

There is no mechanism anywhere to be found that can undo the damage done by the panicking, terror-stricken elites as they scramble to reboot the global economy. To the masses out there under the age of fifty, they look at the bespectacled Fed chairman, so elegantly attired in the classic grey suit and purple tie, as a grandfatherly figure, uttering words of assurance and encouragement in a manner that would have listeners believe that the Fed has it all under control. In a few months, the virus will have lost its virulence and thanks to the Fed’s actions, citizens of the world will have their lives “back to normal.”

And as I stare at the screen, I cannot help but remember the words of Ben Bernanke: “The Fed does not print money.” And Janet Yellen: “To me, a wise and humane policy is occasionally to let inflation rise even when inflation is running above target.” And, finally, Jerome Powell, who stated last fall, when the repo activities began: “This is not QE” (quantitative easing). After listening to these peoplethese academics (who put their trousers on the same way as do you and I)tell these lies day after day, and year after year, and crisis after crisis, I must tell you that it has me ready to man the pitchforks and torches.

To the youngsters out there reading this, you have to understand that I have listened to this constant drivel since the arrival of the “Maestro” Alan Greenspan in 1987, who pontificated mysteriously for nineteen years as Fed chair while orchestrating two of the most enormous bubbles in U.S. history.

This serial money-printer and the godfather of behavioral finance has received every honor imaginable, including “Knight Commander of the Order of the British Empire,” presumably for his role in navigating the FTSE (Financial Times Stock Exchange) to bubble statusand similar kudos from the French, as well as the highest honor given to any U.S. citizen, the “Presidential Medal of Freedom.” I simply ask, “For what?”

Central banking had a role over time that was best executed in minimalist measures; today it is akin to a drunken meth addict having the keys to Fort Knox. They know no boundaries; there are no limits to their monetary power; and they are bereft of supervision because the elected officials are completely compromised by way of political self-interest.

Imagine that you are a farmer. You live in rural North America, and you have worked the land and fields since a boy, raised a family, educated your children, and now you are sitting on $350,000 of savings looking forward to retirement. You are not a financially sophisticated person; you place your savings into the bank account and hope to live comfortably for the rest of your life.

Then suddenly, without explanation, the cost of living begins to inflate and, through no fault of your own, the wealth you thought you had saved is no longer “wealth.” Some unelected bureaucrat has issued five hundred times as many units of the same currency that you saved, and the purchasing power of your retirement nest-egg has been totally and unmercifully trashed. That unelected bureaucrat arbitrarily determined that the loan books of banks and the stock portfolios of the elite class were of greater importance than the purchasing power of a pool of “money” that represents sixty years of hard work and prudent spending patterns (and an ingrained fear of debt) that was drilled into you by your forefathers.

As I sit here contemplating the future of our North American societies on a Friday evening with a glass of wine in hand, titillating the artistic juices in Hemingway-esque fashion, I ask two questions:

Who gave them the right to debase our money?, and more importantly,

Where is the outrage?

I recognize that this missive should not be a forum for political dissent, but as a sexagenarian, I have a limited number of years left on the planet to watch this hyperinflationary nightmare unfold. It is my children and their children for whom I fear. These economist-academics at the Fed, the Bank of Canada, the European Central Bank and all across the globe simply have no idea of the outcome of all of this “stimulus” or “assistance” or “payroll protection,” and it is the arrogance with which they address the voting public that gets my wick. They are no smarter than the farmer with the $350,000, and they are no more visionary than you or I, and they are allowed to digitally violate and cheapen a lifetime of conservative behavior. And that’s wrong.

I remain a long-term bull on precious metals, and am currently 50% invested, with emphasis on the junior developers with ounces in the ground. The reason I am is that while there is the potential for a deflationary tsunami arriving from just over the horizon, there is just as much the chance of a supply-shock spike in food and basic staples prices of a hyperinflationary nature.

Not being a central banker, I do not pretend to know for certain the outcome. The central bankers are opting for the former, because the risk to those that own the Fedthe consortium of leviathan banksare infinitely more vulnerable to a deflationary collapse in their loan collateral than the farmer with cash in hand and no debt. Sadly, these central bankers do not care about anything other than the sanctity of the banks’ equity, and that is why Sikorski Steve Mnuchin said, “Nothing is more important than the American economy,” when referring to his priorities concerning the pandemic, which is sad.

Near term, as I wrote at the onset, I fear that the same forces elevating stocks and buying junk bonds and mortgage-backed securities and soon-to-be equity exchange-traded funds (ETFs) are in the process of capping the current advance in gold. Sure, I can see what physical demand is doing in the cash markets and I can appreciate the arguments as to why “it’s different this time,” but last Friday at 8:30 a.m. was too familiar to have been a simple case of too few buyers and too many sellers.

How many times have we seen a great employment report result in a carpet bombing in the Crimex gold pits? I would say that 20.5 million job losses and a 14.7% unemployment rate was anything but “great,” so when every other unemployment “miss” has resulted in a spike in gold, the US$20 gap down with oil, silver and copper all up, was most certainly not “different this time.” It was “more of the same,” and that is why I remain cautious. These are dangerous times, and after a terrific four-month stretch, I will be damned if I am going to let the boys at the New York Fed steal back any of our 2020 profits.

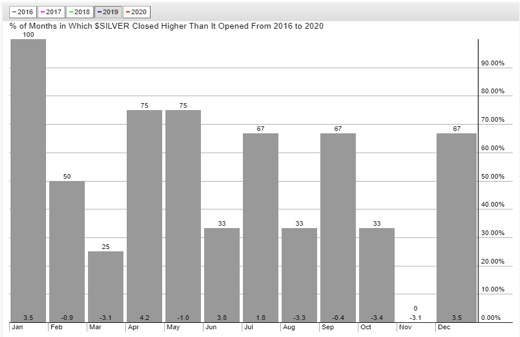

However, I have added to silver for this reason: There could be a scenario where gold simply corrects by trading sideways between now and August (the seasonally strongest month of the year), but where the GSR (gold-silver ratio) normalizes by dropping back to 80 or so. That would be inline with the notion of industrial demand being in charge of the price, rather than its monetary role. Since the White House, the Fed and the Treasury are all spewing the “back to normal” paradigm, silver could be allowed to advance with the economic restart while gold remains capped. It’s a bet and I have tight stops.

Also, because I might be wrong and overly cautious considering the current wave of precious metals enthusiasm, silver is still cheap relative to gold and copper and oil, and remains my personal hedge against a runaway summer move in the metals. Silver seasonality since 2016 is shown below, so while June is tricky, May should give us an edge.

The highlight for the week was the news release by Getchell Gold Corp. (GTCH:CSE), whereby investors were given a glimpse of drill results from Fondaway Canyonactually available in 2017 but not part of the predecessor company’s resource calculation, which came in at 1,069,000 ounces (469,000 Indicated and 600,000 Inferred).

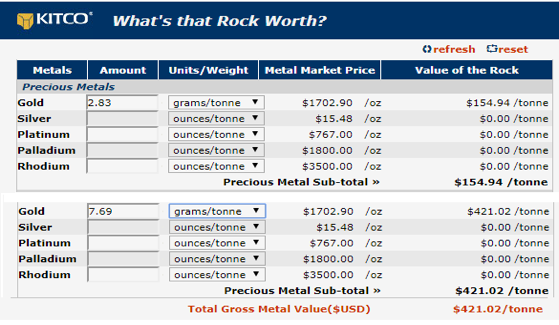

I had gone into SEDAR and searched through the predecessor’s 2017 MD&A (management discussion and analysis), and was blown away by the grade and width of some of these intercepts. I sent subscribers an email alert, and showed them how profitability leverages up with this rising gold price using Detour Gold Corp.’s (DGC:TSX) 2019 Q2 and Q3 MD&As. This open pit operation had a head grade of 0.93 g/t Au with an average sale price of US$1,309/ounce and still earned $16 million sporting a 4.3:1 strip ratio. Getchell’s highlights included “7.69 g/t gold over 9.8 m and 5.28 g/t gold over 7.9 m within a longer interval of 2.83 g/t Au over 65.4 m“.

In the graphic included below, the ore value calculator shows that the long intercept was 65.4 meters of rock valued at US$154.94/tonne, within which they had “bonanza-style” mineralization of 9.8 meters running US$421.02/tonne. These are world-class intercepts and they have most certainly not been factored in by the market when you consider that Getchell is trading at a fully-diluted market cap of ~US$15 million and already has over a million ounces.

The bullish case is presented as follows:

Cipher Research pegs “ounces-in-the-ground” at US$40/ounce with Getchell valued at US$14.2/ounce, implying a lift of 2.81 times current prices.

The current gold resource is understated due to the exclusion of the data released last week from Pack Rat and Colorado (i.e., more ounces).

The new zones are wide open along strike and to depth, which provides tangible blue-sky potential. (i.e., drill hole excitement).

This remains my number one holding in the GGMA 2020 portfolio. The combination of undervalued ounces in the ground and low-risk exploration upside makes Getchell a relatively low-risk, high-reward potential story looking out to the balance of 2020 and beyond. There is more to the story than I have discussed, here but management has done a great job and deserves a nod.

Originally published May 8, 2020.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Getchell Gold. My company has a financial relationship with the following companies referred to in this article: Getchell Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold, a company mentioned in this article.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

McAlinden Research Partners reports that hedge funds that had been shorting natural gas have suddenly developed a strong appetite for natural gas stocks and bonds on the expectation that U.S. oil wells that generate gas as a by-product will close fast enough to make up for the collapse in global natural gas demand.

2019 was such a rough year for natural gas that by the time February 2020 rolled by, hedge funds had built up the largest net short position on record for the sector. Those investors have suddenly developed a strong appetite for natural gas stocks and bonds on the expectation that U.S. oil wells that generate gas as a by-product will close fast enough to make up for the collapse in global natural gas demand. Some Appalachian gas producers are especially well-positioned to benefit from such a prospect.

Global consumption of natural gas is on track to drop by 5% in 2020, according to the International Energy Agency (IEA). While that number sounds harmless, it represents a huge shock to the gas industry which has enjoyed ten years of uninterrupted demand growth, until the COVID-19 lockdowns brought that streak to an end.

Early evidence of the impact has already cropped up in the first quarter data, even though the lockdowns in Europe and the United States were still relatively new. While global demand fell more than 3% in 1Q 2020, demand in the United States dropped 4.5% from a year earlier, dragged down by an 18% decline in residential and commercial demand. For context, the last time U.S. gas demand contracted to this extent was during the Great Depression, when domestic demand tumbled by 13% in 1931 and by 7% in 1932.

Worsening Demand/Supply Imbalance

Although demand has experienced a historic plunge, supply has not been adjusted downward to match that plunge. In fact, the demand/supply imbalance that weighed on natural gas prices last year has only worsened. Natural gas inventories in the United States stood at 2.210 trillion cubic feet on April 24up 783 billion cubic feet from a year ago and 360 billion cubic feet above the five-year average, according to the EIA. In other words, U.S. gas stockpiles are 55% higher than a year ago and 20% higher than the five-year average.

The biggest challenge to adapting output lies in the fact that turning the taps off at typical gas fields isn’t easy. Moreover, those that can be stopped take time and money to restart, says the CFO of InfraStrata Plc, a U.K. firm focused on the development and commercialization of advanced energy infrastructure.

Almost Out of Storage

Back in April, MRP wrote about the sudden wave of oil storage demand that’s been boosting the oil tanker market. It so happens that gas storage sites are also filling up quickly due to growing stockpiles of the commodity. Unless a major change occurs in the near-term, Europe could run out of storage space for its natural gas by July, or even earlier in some markets, according to industry players.

Speculators Flip from Bearish to Bullish

Some investors are already betting that the near-term change will be supply-driven, and that it will originate from the same place that, years ago, seeded the conditions that would eventually grow into today’s natural gas glut. When oil prices plunged into negative territory last month, the US energy industry received a wakeup call. Better to start shutting off money-losing wells, they realized, than to have to pay traders to get rid of the oil.

More than 12% of U.S. gas output is associated gas, extracted as a byproduct of oil drilling. Less oil drilling means less associated gas, which effectively equates to a supply cut. The notion that there may be less shale gas coming from U.S. oil wells this year has prompted the fast money set to reverse their bearish bets on the commodity and its producers. In mid-February, hedge funds and other speculators were piled into the largest net short position on record for natural gas. Now, those same investors are net long for the first time since May 2019.

Beyond April’s 26% Natural Gas Price Surge

Such a dramatic shift in sentiment has helped pushed the price of U.S. natural gas 26% higher in one monthfrom $1.55 per million British thermal units (MMBtu) on April 2nd to $1.96/MMBtu on May 4. Despite those gains, the commodity’s price is still 10% lower than at the start of the year when it was trading at $2.17/MMBtu.

The question some investors are asking is whether these ultra-low prices will compel enough utilities to switch out of alternate power sources into natural gas, triggering a demand-driven price surge in the process. The IEA’s forecasts for 2020 also shed some light on this matter.

As mentioned earlier in this report, the Paris-based agency which advises nations on energy policy estimates that global natural gas consumption will fall by 5% this year. Should the world economy recover faster than anticipated from the COVID-19 disruptions, the overall demand loss could narrow to about 2.7%, which would still mark the first annual drop in natural gas consumption since 2009. Much of the decline is expected to come from power generation.

The IEA has also projected that all sources of energyi.e., oil, coal, natural gas, and nuclearwill see a decline in demand this year, with the exception of renewable energy. That’s because renewables in many countries get first priority to feed electricity into the grid, enabling them to maintain or increase market share when there’s a huge plunge in overall energy demand.

The energy source most at risk of losing market share to natural gas is coal, which is heading for its biggest fall in annual demand (-8.0%) since World War II. The fact that coal’s share in the electricity mix has fallen in India, China, Europe, and parts of the U.S.four regions with large and varied electricity markets implies there is more pain ahead for this commodity. Based on the IEA’s figures, any market share losses to natural gas are not enough to push the latter’s overall growth into positive territory this year. This means, there likely won’t be a demand-driven surge in the price of natural gas, unless the recovery from coronavirus delivers an upside surprise.

How to Invest

Investors can gain exposure to movements in the price of natural gas via the United States Natural Gas Fund, LP (UNG), which holds near-month contracts in natural gas futures. Those looking for exposure to natural gas equities can use the First Trust Natural Gas ETF (FCG) as an investment vehicle. FCG tracks an equal-weighted index of US companies that derive a substantial portion of their revenue from the exploration & production of natural gas.

Given that the world is awash in natural gas, it could take a while for the market to rebalance itself, which means there is limited upside for the UNG in the near-term. Any positive headlines, however, would have a bigger impact on FCG. That’s because natural gas producers have struggled with declining gas prices for 10 years, during which time their stocks have gotten hammered, losing 92% of their value.

The closure of oil wells in the Permian and North Dakota regions could be especially beneficial to gas-focused companies operating in the Appalachians, since they will be able to capture a greater share of the market by default. Some of these companiesincluding EQT Corp (EQT), Range Resources Corp. (RRC), and CNX Resources Corp. (CNX)saw their share prices more than double during the month of April. Those gains helped the FCG deliver a return of +51% last month. There is room for the Appalachian gas stocks to climb higher, since they are rising from a very low base.

This content was delivered to McAlinden Research Partners clients on May 4. To receive all of MRP’s insights in your inbox Monday – Friday, follow this link for a free 30-day trial.

McAlinden Research Partners (MRP) provides independent investment strategy research to investors worldwide. The firm’s mission is to identify alpha-generating investment themes early in their unfolding and bring them to its clients’ attention. MRP’s research process reflects founder Joe McAlinden’s 50 years of experience on Wall Street. The methodologies he developed as chief investment officer of Morgan Stanley Investment Management, where he oversaw more than $400 billion in assets, provide the foundation for the strategy research MRP now brings to hedge funds, pension funds, sovereign wealth funds and other asset managers around the globe.

Disclosure: 1) McAlinden Research Partners disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

McAlinden Research Partners: This report has been prepared solely for informational purposes and is not an offer to buy/sell/endorse or a solicitation of an offer to buy/sell/endorse Interests or any other security or instrument or to participate in any trading or investment strategy. No representation or warranty (express or implied) is made or can be given with respect to the sequence, accuracy, completeness, or timeliness of the information in this Report. Unless otherwise noted, all information is sourced from public data.

McAlinden Research Partners is a division of Catalpa Capital Advisors, LLC (CCA), a Registered Investment Advisor. References to specific securities, asset classes and financial markets discussed herein are for illustrative purposes only and should not be interpreted as recommendations to purchase or sell such securities. CCA, MRP, employees and direct affiliates of the firm may or may not own any of the securities mentioned in the report at the time of publication.

Bob Moriarty of 321gold discusses this company that is exploring a rare earth element project in Canada.

I have been remiss in not doing much in the way of writing about resource opportunities for a couple of reasons. Obviously the Corona virus issue has been at the forefront of most people’s attention. But also I was saying for years that a depression was coming and wise people would prepare in advance.

About the virus. Every day it looks more and more like some sort of scam by Bill Gates, the Deep State and Dr. Fauci representing the interests of big Pharma. Obviously the Chinese were lying about how many people died in China. They sought to understate the number killed. But the US is just as much a liar, in the opposite direction.

I make the point in my books that perfectly ordinary people can figure out what is really going on simply by asking the right questions. As of this morning as I write the Johns Hopkins graphic shows that according to their official numbers, the US represents 31.7% of all the cases in the world. Now since the US only has about 4% of the world’s population, it would be quite impossible for us to have eight times as many infected as the rest of the world per capita.

San Diego reported that 194 of their people died of the virus. It took an honest official to reveal that only 6 of those 194 actually died of the virus. The rest tested positive but died of strokes, heart attacks and other events. Even the CDC admits that their results for those having the virus at death are five times higher than actually being killed by the virus. Donald Trump wants to be the biggest and the best at everything. How the CDC reports deaths and the virus certainly qualifies.

Meanwhile in Texas medical authorities said that a 22-week preemie died of the virus but failed to mention that babies born at 22 weeks never survive. That baby did not die from the virus.

Bill Gates and big Pharma want to tag and bag you with a vaccine that may or may not even work but will put billions of dollars into someone’s pockets. Hopefully his. During the Swine Flu fiasco, the vaccine killed more people than the flu did. There are reports out today that if you have been vaccinated against the ordinary flu you have a 36% higher chance of catching the Corona Virus. Even the CDC admits lying about deaths from the flu to encourage vaccinations.

It’s a stretch to imagine how a worldwide panic over a flu would have any sort of a positive impact on any junior resource stock but actually there is a company that may have just hit the jackpot as a result.

As a direct result of the Chinese literally shutting down their entire economy for a couple of months in response to the Corona Virus, the single source supply chains for nearly everything China produces were utterly broken. For some commodities such as rare earths required for specialty metals and military purposes, it was a giant wake up call.

Now I am not a believer that China or Russia for that matter are enemies of the United States. I believe that the MIC needs monsters to slay to justify the US taxpayers funding half the military expenses in the entire world. But having China as a sole source for anything is stupid and beyond stupid for metals so critical to the functioning of our economy as Rare Earths.

I’ve done articles in the past on Defense Metals. The share price is up 50% in the last six months and still cheap. They have made wonderful progress and Defense Metals Corp. (DEFN:TSX.V; DFMTF:OTCQB; 35D:FSE) just announced on the 13th a major addition to their 43-101 resources at Wicheeda in central British Columbia. The resource showed a 49% increase in tonnage and a 30% increase in average grade. It was economic before and I showed the numbers in the December piece. It is much more economic today.

The US realizes that a safe and secure supply of Rare Earths from outside China is mandatory. The Federal Government has already defined Rare Earths as critical resources. A bill in Congress today calls for changing the tax deductions for mining companies in the US of Rare Earths and creates a $50 million fund to help junior companies out. That’s just in the US but one day soon they will figure out that the US just doesn’t have much in the way of REE but Canada has a bunch.

We are in a depression. I’ve said it was coming for years. As long ago as a year ago I was saying it would start in October. It actually began a month early and became obvious to everyone in March. But the vast majority of people think it is somehow connected with the Corona Virus. It is not. It was coming any way with or without a bad flu season. The Corona Virus just made everything speed up. Now the majority of investors think that as soon as the quarantine ends, the economy recovers. That’s not going to happen any time in the next fifteen years. It is the greatest depression in history because we have the greatest debt load in all of recorded history.

We will have the most massive wealth transfer that has ever taken place from those unprepared to those who are prepared. My readers are prepared and will see rewards such as they have never dreamed possible. We are going to have deflation and hyperinflation at the same time. When the government gets tired of being stupid, we will declare a debt jubilee and go back to honest money. Eighteen months later the economy will recover.

Defense Metals is an advertiser. I have bought shares in the open market and in various private placements. That makes me biased so I request readers do their own due diligence.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Defense Metals. Defense Metals is an advertiser on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: Defense Metals. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Defense Metals, a company mentioned in this article.