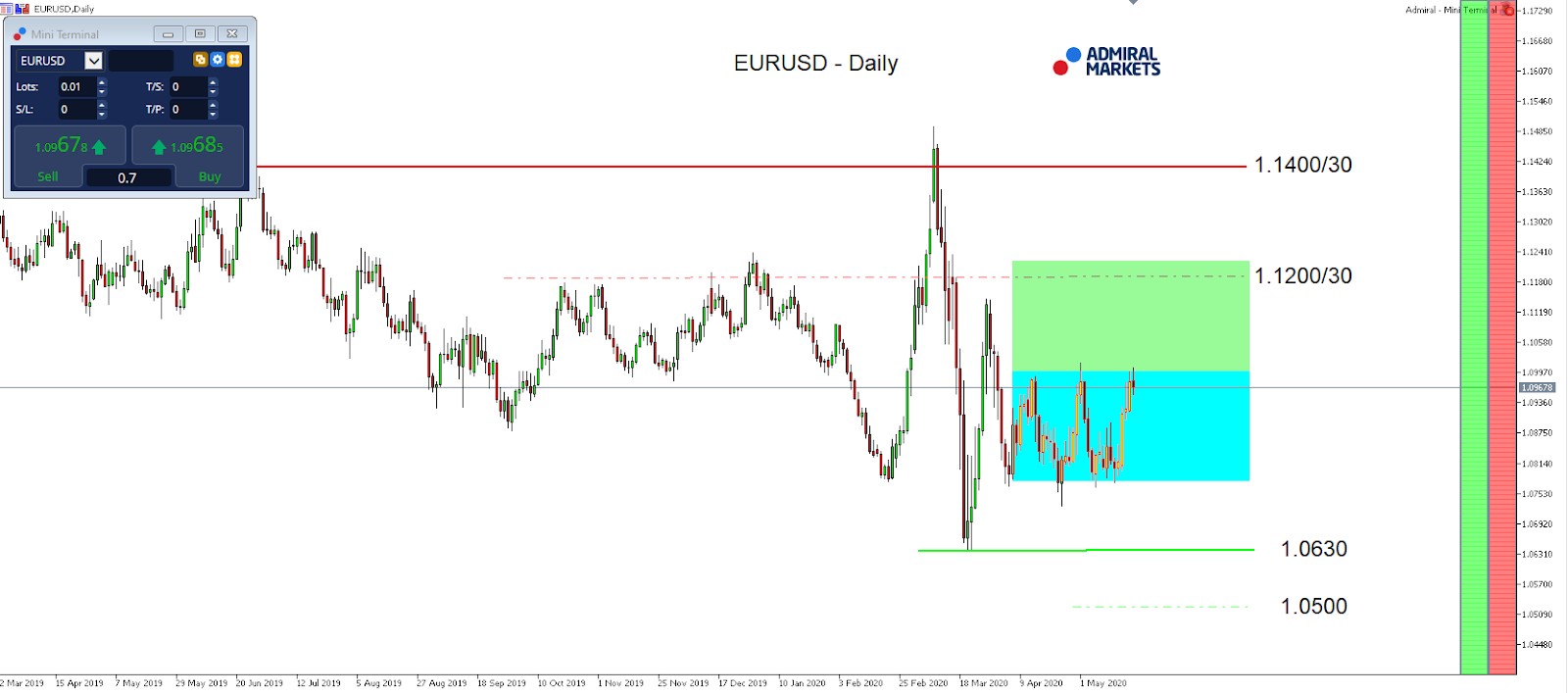

While the economic calendar is quite thin for the weekly close, and market participants may expect forex volatility to be subdued in expectation of the upcoming US bank holiday next Monday, the EUR/USD faces an extremely interesting short-term resistance zone around 1.1000.

In fact, a break higher, with a dynamic stint and quick follow through as high as 1.1200, became likely over the last few days. Because, on Monday, Germany and France’s Merkel and Macron proposed a 500 billion EU recovery fund that would offer grants to the European Union regions and sectors hit hardest by the coronavirus pandemic.

Indeed, one could see this as a first step towards a transfer union and in addition with the massive monetary stimulus from the ECB, recent Euro bullishness with further gains comes with no big surprise.

In addition to that, we see the US dollar staying under consistent pressure, and while we expect European yields to continue to rise, a sustainable drop in 10-year US Treasury yields below 0.60% is likely, too, resulting in a further narrowing of the yield differential between EU and US bonds, favouring gains in the EUR/USD.

Technically, a break above 1.1000 coincides with a break out of the trading range between 1.0750/0800 and 1.1000 since the beginning of April, resulting in a projected target on the upside around 1.1200/1250:

Source: Admiral Markets MT5 with MT5-SE Add-on EUR/USD Daily chart (between March 22, 2019, to May 21, 2020). Accessed: May 21, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of the EUR/USD fell by 10.2%, in 2016 it fell by 3.2%, in 2017, it increased by 13.92%, 2018, it fell by 4.4%, 2019, it fell by 2.2%, meaning that after five years, it was down by 7.3%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

The Bank of Japan (BOJ) launched a third measure aimed at supporting small and medium-sized firms affected by the spread of the Covid-19 pandemic and extended the duration of all three measures by another 6 months until the end of March 2021. Japan’s central bank noted its existing measures of purchasing commercial paper and corporate bonds, with a maximum amount outstanding of some 20 trillion yen, and the 25 trillion yen Special Funds-Supplying Operations to Facilitate Financing in Response to the Novel Coronavirus. In its statement following an unscheduled policy board meeting that was announced on May 19, the BOJ said it would add a new fund-provisioning measure based on eligible loans from banks based on the government’s 30 trillion yen emergency economic support plan. The total size of these three measures aimed a businesses, which will be known as “the Special Program,” will be about 75 trillion. “By conducting these measures, the Bank will continue to support financing mainly of firms and to maintain stability in financial markets,” BOJ said, reiterating that it is closely monitoring the impact of Covid-19 and “will not hesitate to take additional easing measures if necessary.” Under its new fund-providing measure, BOJ will provide funds at a loan rate of zero percent while a positive interest rate of 0.1 percent will be applied to the outstanding balances of banks’ current accounts that correspond to the amounts of loans provided through this measure. The BOJ’s policy board also affirmed the key elements of its current monetary policy framework known as “yield curve control,” which includes a negative interest rate of 0.1 percent on banks’ excess reserves. It also confirmed decisions taken at its regular meeting in April in which it boosted its asset purchases and scrapped an earlier annual limit of buying 80 trillion yen of Japanese government bonds (JGBs) in favor of buying bonds “without setting an upper limit” so the 10-year yield remains around zero percent. BOJ confirmed it would be buying exchange-traded funds (ETFs) and Japanese real estate investment trusts (J-REITs) to their amounts outstanding increase at an annual pace with the upper limit of some 12 trillion yen and some 180 billion yen, respectively. As far as commercial paper and corporate bonds, BOJ said it would maintain their outstanding amounts at about 2 trillion and 3 trillion yen, respectively. However, BOJ will now undertake additional purchases of both these assets classes until the end of March 2021, as compared with April’s target of September 2020, with the upper limit of 7.5 trillion yen for each asset. In April the additional purchases were raised to the 7.5 trillion from an earlier 1 trillion for each asset. Data released today showed Japan’s consumer price inflation fell to only 0.1 in April from 0.4 percent in the previous two months and is now at the lowest level since November 2016. The drop in inflation is bound to ignite concern that BOJ is losing its fight against deflation. Japan officially fell into recession in the first quarter of this year as its gross domestic product shrank 0.9 percent following a fall of 1.9 percent in the fourth quarter of 2019, the country’s first recession since late 2014. On an annual basis, GDP shrank 2.0 percent in the first quarter after shrinking 0.7 percent in the previous quarter. At its April policy meeting, the BOJ slashed its forecast for growth and inflation. BOJ forecast the economy would shrink between 0.4 percent and 0.1 percent in the 2019 fiscal year, which ended on March 30, down from its January forecast of growth of 0.8 to 0.9 percent. For fiscal 2020, which began on April 1, BOJ forecast the economy would shrink a further 5.0 to 3.0 percent before expanding between 2.8 and 3.9 percent in fiscal 2021. BOJ forecast consumer prices would decline 0.7 to 0.3 percent in the current fiscal 2020 before rising to 0.0 to 0.7 percent in fiscal 2021, well below its 2.0 percent target. www.CentralBankNews.info

Global equities are falling today after a down session on Thursday with US Labor department report showing nearly 40 million Americans have lost their jobs in the last nine weeks. Investors confidence was undermined also by rising US-China tensions as a bipartisan bill was introduced in US Senate that would sanction Chinese officials if they enforce a new national-security law in Hong Kong.

Forex news

Currency Pair

Change

EUR USD

-0.17%

GBP USD

-0.53%

USD JPY

-0.25%

AUD USD

-0.21%

The Dollar strengthening continues today . The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.3% Thursday despite report initial jobless claims jumped another 2.44 million last week. EUR/USD joined GBP/USD’s continued sliding yesterday with both pairs lower currently as data showed euro-zone’s economic activity contracted less drastically in May while UK retail sales fell by a record 18% over year in April. USD/JPY reversed sliding yesterday while AUD/USD turned lower with both pairs down currently.

Stock Market news

Indices

Change

Dow Jones Index

-0.75%

Hang Seng Index

-3.44%

Australian Stock Index

-1.24%

Futures on three main US stock indexes are in the red currently after a pullback Thursday. Earnings season is nearing the end with another batch of companies including John Deere, Hang Seng Bank and Fujifilm Holdings reporting quarterly results today. Stock indexes gave back part of previous session gains on Thursday led by technology shares: the three main US stock indexes recorded losses ranging from 0.4% to 1.0%. European stock indexes are falling today after ending solidly lower Thursday led by bank stocks. Asian indexes are falling today after reports China is planning to impose new national security legislation on Hong Kong. Heng Seng sank 5.7%.

Commodity Market news

Commodities

Change

Brent Crude Oil

-5.91%

WTI Crude

-7.02%

Brent is pulling back today. Oil prices edged higher yesterday after the Energy Information Administration report Wednesday crude inventories at the storage hub in Cushing, Oklahoma, fell by about 5.5 million barrels for the week. The US oil benchmark West Texas Intermediate (WTI) futures ended higher yesterday: June WTI gained 1.3% but is lower currently. July Brent crude closed 0.9% higher at $36.06 a barrel on Thursday.

Gold Market News

Metals

Change

Silver

+0.6%

Gold prices are recovering today. June gold lost 1.7% to $1721.90 an ounce on Thursday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Shares of Surface Oncology set a new 52-week high price after the company reported that it is partnering with Merck & Co. in an immuno-oncology study of SRF617, targeting CD39 in combination with KEYTRUDA® (pembrolizumab) in solid tumor patients.

Clinical-stage immuno-oncology company Surface Oncology Inc. (SURF:NASDAQ), which is engaged in developing next-generation immunotherapies targeting the tumor microenvironment, announced today that “it has entered into a clinical trial collaboration with Merck & Co. Inc. (MRK:NYSE), known as MSD outside the U.S. and Canada, through a subsidiary, to evaluate the safety and efficacy of combining Surface’s SRF617, an investigational antibody therapy targeting CD39, with Merck’s KEYTRUDA® (pembrolizumab), the first anti-PD-1 therapy approved in the United States.”

The company further stated that “this combination will be studied as a component of the first-in-human Phase 1/1b study of SRF617 and will be evaluated in patients with solid tumors, with a focus on patients with gastric cancer and those who have developed resistance to checkpoint inhibition.”

The company explained that “SRF617 inhibits CD39, an enzyme critical both to the breakdown of adenosine triphosphate and the production of adenosine and that a substantial body of research supports a role for CD39 in allowing cancer to evade immune responses.” The firm claimed that “the combination of SRF617 and KEYTRUDA has the potential to overcome this barrier to immune system activation and promote anti-tumor immunity.”

Surface Oncology’s Chief Medical Officer Robert Ross, M.D., commented, “Surface is committed to delivering truly breakthrough therapies that can transform treatment for people with cancer. This collaboration with Merck will add an important dimension to our clinical program for SRF617, and allow us to more rapidly assess its potential.”

“We have demonstrated in preclinical studies that the inhibition of CD39 results in substantial activation of both the innate and adaptive arms of the immune system. Encouragingly, we also found that activation is heightened in combination with anti-PD-1 treatment and that this combinatory approach has the potential to overcome anti-PD-1 resistance,” Dr. Ross added.

In a separate news release, Surface Oncology reported today that “it has raised gross proceeds of approximately $28.9 million through its At-the-Market, or ATM, facility with participation based on interest received from EcoR1 Capital LLC, Venrock Healthcare Capital Partners, BVF Partners L.P. and RS Investments, a Victory Capital investment franchise.” The company indicated that it sold approximately 10.9 million common shares at the current market price at the time of $2.66 per share. The firm noted that this transaction exhausted the balance on the $30 million ATM facility.

The company advised that this additional funding will serve to strengthen its balance sheet and the proceed will be used for working capital and other general corporate purposes and to advance its drug pipeline. Specifically, it will help fund the clinical development of SRF617 which is targeting CD39, SRF388 that is targeting IL-27) and the advancement of SRF813 which is targeting CD112R, also known as PVRIG.

Merck & Co., Inc. is headquartered in Kenilworth, N.J., and is one of the world’s largest global healthcare companies with a market cap of around $196 billion. The company provides healthcare services and develops, manufactures and markets animal health products, biologic therapies, prescription medicines and vaccines worldwide.

Surface Oncology is an immuno-oncology company based in Cambridge, Mass. The company is developing next-generation antibody therapies for applications on the tumor microenvironment. The firm stated that “its novel cancer immunotherapies are designed to achieve a clinically meaningful and sustained anti-tumor response and may be used alone or in combination with other therapies.”

Surface Oncology started off the day with a market capitalization of around $75.3 million with approximately 28.32 million shares outstanding. SURF shares opened more than 37% higher today at $3.65 (+$0.99, +37.22%) over yesterday’s $2.66 closing price. The stock has traded today between $3.21 and $4.40 per share and is currently trading at $3.81 (+$1.15, +43.23%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Daré Bioscience’s study, its prospects and the indication’s U.S. market opportunity are discussed in a ROTH Capital Partners report.

In a May 15 research note, ROTH Capital Partners analyst Yasmeen Rahimi reviewed why the outlook is positive for Daré Bioscience Inc.’s (DARE:NASDAQ) DARE-BV1, a treatment candidate for bacterial vaginosis.

Rahimi outlined the next steps for DARE-BV1.

This biopharmaceutical firm based in San Diego, Calif., intends to launch a pivotal Phase 3 trial of DARE-BV1 in July, aiming to highlight it as a firstline treatment option. Topline study data should be available by year-end 2020. Due to the fast track status of DARE-BV1, Daré only needs to complete one Phase 3 study before filing a new drug application for it with the U.S. Food and Drug Administration.

The study will involve 250 women with bacterial vaginosis who will be assessed at their day 2130 visit. The endpoint is clinical cure rate, measured using Amsel criteria.

Subsequently, Daré intends to take 219 patients from the Phase 3 study who experienced a cure of their bacterial vaginosis, whether from DARE-BV1 or metronidazole, and evaluate them in an extension study. They will not get further treatment but will be assessed at both 30 and 60 days after enrollment in this add-on study for duration of treatment response and thus, potential recurrence.

Rahimi explained that Daré’s existing data on DARE-BV1 “is setting up the Phase 3 study for success.” Results from a prior proof of concept study showed that one administration of DARE-BV1 resulted in an 86% clinical cure rate (and 57% bacteriological, or Nugent, cure rate and 57% therapeutic cure rate) at the first post treatment follow-up on day 714. Further, 92% of the women with a clinical cure at that day 714 visit did not show a recurrence of vaginosis at their second visit on day 2130.

Also, the cure rate from the placebo in previous studies was low, at 510%. This means that “there is an excellent chance that the proof of concept results can translate into a larger study, especially since the treatment cure rates would be compared to a low placebo rate, which would show a clear treatment benefit,” noted Rahimi.

She indicated that Daré has the funding needed for this Phase 3 bacterial vaginosis program and for advancing other clinical assets. This is due to the recent purchase agreement the company signed, which can yield up to $15 million for the biopharma over three years. “This transaction grants Daré security and stability, especially during the uncertainty caused by the COVID-19 pandemic,” Rahimi added.

Rahimi highlighted that bacterial vaginosis is an undervalued market opportunity in the U.S. and explained why. With bacterial vaginosis being highly prevalent and the most common cause of vaginitis in U.S. women, the market size in the United States is 21 million. Additionally, the recurrence rate is high, as high as 6080%, within three to four months after the initial infection. As such, a great unmet need exists for a bacterial vaginosis treatment that prevents recurrence.

Finally, Rahimi purported that Daré’s partnership with Health Decisions “can leverage the clinical research organization’s (CRO’s) expertise in women’s health to accelerate clinical development and cut costs. The CRO has extensive expertise with women’s health assets, especially those related to contraception and fertility. In contraception, for example, Health Decisions has executed 40-plus clinical studies. That company “is the perfect match for Daré and will be key for the clinical execution and advancement of assets in Daré’s women’s health pipeline,” the analyst commented.

ROTH has a Buy rating and a $4 per share price target on Daré, the stock of which is now trading at about $1.05 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Disclosures from ROTH Capital Partners, Daré Bioscience Inc., Company Note, May 15, 2020

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Within the last twelve months, ROTH has received compensation for investment banking services from Daré Bioscience, Inc.

ROTH makes a market in shares of Daré Bioscience, Inc. and as such, buys and sells from customers on a principal basis.

Shares of Daré Bioscience, Inc. may be subject to the Securities and Exchange Commission’s Penny Stock Rules, which may set forth sales practice requirements for certain low-priced securities.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

Money manager Adrian Day reviews developments at three gold and silver companies in his portfolio.

Vista Gold Corp. (VGZ:NYSE.MKT; VGZ:TSX, US$0.807) continues to advance the Mt. Todd project in Northern Territories, Australia, as it monetizes non-core assets to maintain a healthy balance sheet without dilution. As it awaits its final permit, the improvements at Mt. Todd are now incremental, with the most significant boost coming from the gold price itself; the project, one of the largest undeveloped gold projects in the world, is highly sensitive to the gold price.

To illustrate that sensitivity, the project’s NPV at a $1,700 gold price (and a 5% discount rate) has virtually doubled to $1.6 billion from last year’s pre-feasibility which used $1,350, and the internal rate of return jumped from 23.4% to 30%. An independent benchmarking study completed in March confirmed Vista’s numbers and assumptions in its pre-feasibility.

Vista sells non-core assets to focus on Mt. Todd

The latest sale is half its royalty on the Awak Mas project in Indonesia, being advanced by an Australia company. This put $2.4 million into the treasury, bringing total cash and cash equivalents to $5.6 million. The company has the right to buy the remainder of the royalty a year from now; if they do not, then Vista can look to sell it elsewhere. Vista also holds 6.2 million shares of Midas Gold, worth approximately $2.8 million today, and it continues to seek a buyer for a used mine it owns. The company says it has sufficient cash for to cover all expenses for the next year. At present, company executives are unable to travel to the project, though senior staff was already onsite before the travel restrictions were introduced.

Looking to realize value from project

Vista is extremely undervalued. The two main risks are whether they will be able to continue monetizing assets to avoid a dilutive equity raise, and whether they will be able to negotiate a successful transaction for the project, obtaining value for long-time shareholders without scuppering a deal by asking too much. It’s a delicate line to walk, but one that a higher gold price perhaps makes easier.

The gap between value and market price ($81 million) is so great that Vista is a buy. It tends to be a volatile stock, however, so there is no need to chase it. The stock has recovered all its March loss when it hit a 37 cents low.

Fortuna nearly there on new project, but at lower output

Fortuna Silver Mines Inc. (FSM:NYSE; FVI:TSX; FVI:BVL; F4S:FSE, US$3.96) is to commence production at Lindero on a reduced operating plan, given the travel restrictions in place in Argentina. The new plan will get cash flow starting sooner than waiting to complete the original plan, but at the cost of lower recoveries. Recoveries are estimated at about 50% initially (down from a planned 80%), with the ore placed on the leach pad to generate more gold over the life of the mine. It is estimated that ultimately 1020% of the gold could be lost. Cash cost will be under $700. The circuit for the revised operational plan is fully installed and ore can now be placed on the leach pad by July.

To proceed now a difficult decision

The equipment required for the tertiary phase of the original plan, already on site, are sensitive and require vendor personnel on site in the initial phase to make adjustments and fix problems. Without these key personnel on sitenormal in the start-up phase of a major new operationit was considered too risky to put the ore through the entire circuit. Once the restrictions are lifted, however, Lindero will be able to move to the full three-part circuit and move back to the original mine plan. It is a shame to lose some of the gold, but we appreciate the difficult decision, particularly given that the country’s travel ban is currently extended to September.

Mining has been named an essential activity in Argentina and allowed to resume with an approved health plan in place. Lindero has the go-ahead. But an international travel ban remains in force. Fortunately, the mine’s Australian operations manager was on site when the travel ban was imposed, but other key personnel from both the company and from vendors were not.

Existing mines continue, with their own challenges

Both of the company’s other mines continue to operate, though at San Jose in Mexico there is mining but currently no ore processing; and at Caylloma new health restrictions reduce the amount of activity.

With the additional delays to production, Fortuna decided to raise additional equity. Although cash on hand ($88 million as of end-March) would likely have been sufficient until Lindero was cash-flow positive, the company has always taken a conservative approach to cash, and wanted a cushion. Total remaining funding including working capital is estimated at $75 million to $80 million. The $60 million raised removes any lingering doubts about the financial ability to complete Lindero.

Fortuna remains significantly undervalued relative to other silver companies, and remains one of our top holdings. But given the current difficulties at both existing mines (including lower grades at San Jose, and lower silver recovery and low base metals prices at Caylloma), as well as the ever-present risks of operating in Argentina, we are holding.

Evrim loses partner but advances elsewhere

Evrim Resources Corp. (EVM:TSX.V, 0.325) announced that its partner Newmont had given up its joint venture on the Astro project and relinquished the regional alliance it had with Evrim in the Northwest Territories of Canada. This was not a shock; Newmont’s acquisition of Goldcorp last year has given it plenty to chew on and seen the company relinquish many joint ventures.

Although it would have been good if Newmont had continued, it is part of business for prospect generators that joint venture partners come and go. The positive from this is that Newmont did not abandon the venture for any lack of success, and the property, which includes a 10-kilometer structural corridor with outcropping gold, discovered in a greenfield explorationplus the results of $3.2 million in exploration work reverts to Evrim, which will seek another partner. Given the challenges of the location, it is probably suitable only for a very large company.

Royalty project advances towards cash flow

Meanwhile, First Majestic continues to advance the Ermitaño project on which Evrim holds a 2% royalty with an increased drill activity and larger resource delineated. In the last announcement in April, grade had increased 15% and contained ounces by 345%. It is expected to commence production in the first quarter of 2021. And work continues on other joint ventures, including Evrim’s review of Yamana’s Western U.S. database, which is beginning to yield fruit.

Cash in the bank is well over C$7 million. That plus the value of the Ermitaño royalty means that most of Evrim’s market cap is backed by hard assets. Thus, the downside is very limited, while there remain plenty of opportunities for upside. Evrim is a buy.

Adrian Day, London-born and a graduate of the London School of Economics, heads the money management firm Adrian Day Asset Management, where he manages discretionary accounts in both global and resource areas. Day is also sub-adviser to the EuroPacific Gold Fund (EPGFX). His latest book is “Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks.”

Disclosure: 1) Adrian Day: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Evrim Resources, Altius Minerals, Lara Exploration and Midland Exploration. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Funds controlled by Adrian Day Asset Management hold shares of the following companies mentioned in this article: All. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Vista Gold, Evrim Resources, Midland Exploration, Altius Minerals, Newmont Goldcorp and Lara Exploration, companies mentioned in this article.

The silver market is on the move. In fact, it’s finally moving out ahead of other precious metals and showing some real leadership.

After the panic selling of March briefly brought spot silver below $12/oz, prices have since surged by 50%. That’s an impressive move to take place within the span of just two months.

The question for investors now is whether the recent rally in silver is fleeting or sustainable – whether it’s evidence of extreme market volatility that suggests more danger ahead or the first leg of a much larger bull market to come.

In our view, there is good reason to believe that the March 2020 lows will never be violated and that silver is therefore in a structural bull market.

Last Monday, Money Metals posted “Silver Breakout in Progress” as a market update. We noted, “Silver prices will run into some overhead resistance just above the $16/oz level. Once broken, that technical line on the weekly chart could serve as a springboard for a run toward $19/oz – and ultimately higher.”

The technical clues we presented for an imminent breakout were confirmed that Friday. Silver springboarded to $17/oz. Then yesterday, carryover momentum brought prices up near $18/oz before this morning’s pullback.

The bullish mega-trend for silver – fueled by accelerating monetary debasement, declining worldwide mine production, and strong safe-haven demand – is likely just beginning.

At the same time, there are growing signs of shortages in physical silver, at least in some parts of the world. This week, bullion banks have been scrambling big time to find the 1,000-ounce silver bars they need to make near-term delivery commitments on the Comex. This shortage in the U.S. of deliverable silver has caused New York spot silver prices to diverge more than 50 cents above London spot. Such a spread is extremely rare, and arbitrageurs do not seem able to transport enough silver from London to New York to close the gap anytime soon.

None of this means there can’t be sharp pullbacks to come. Silver is a notoriously volatile commodity that seems to specialize in shaking people out (especially leveraged speculators in the futures market).

Although nothing is guaranteed in these wild and often manipulated markets, the blue line shown in the chart above, which had been resistance, will likely now serve as final support in the event of a selloff.

Fundamentally, a silver price below $16/oz is simply not sustainable given that all-in mining costs for the metal currently range into the high teens.

While another bout of irrational panic selling over virus fears is possible should it make a deadly resurgence, the remaining upside potential for silver in the months and years ahead far exceeds its downside risk.

Silver is historically cheap versus just about any other commodity or asset class on the planet.

When measured against gold, silver has never been cheaper – going back through hundreds of years of record-keeping – than it was during the depths of the March selling.

Silver’s unprecedented cheapness versus gold (at one point 1/126th the gold price) gives us further confidence that those extreme lows were anomalous displays of “peak fear” that will never be seen again.

At present the gold:silver ratio comes in right around 100:1. Although still extremely elevated (by normal standards) in favor of gold, silver has been rapidly gaining ground against its pricier counterpart and can be expected to continue closing the gap as the bull market in both metals advances.

With an election coming up and uncertainties surrounding the economy and COVID-19, investor interest in precious metals is likely to remain robust.

A ballooning federal debt and Federal Reserve balance sheet pose serious risks for holders of U.S. dollars.

Fed chairman Jerome Powell recently assured Congress the central bank is “committed to using our full range of tools to support the economy.” They are all “tools” of currency debasement, regardless of what jargon or acronyms monetary planners trot out to describe them.

Granted, safe-haven bullion and ETF buying could taper off in the event that the economic outlook brightens and investor fears recede.

But since more than 50% of silver demand comes from industrial applications, a recovering economy isn’t necessarily a negative for prices – especially when so many other fundamental and technical indicators are now turning bullish.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

By Jameel Ahmad, Global Head of Currency Strategy and Market Research at FXTM

As the old saying goes, if something sounds too good to be true it usually is.

This has unfortunately been the case so far this week for investors when it comes to hope over progress on a coronavirus vaccine. Sadly we do need to brace ourselves for the potential long-haul journey that all will be encountering when it comes to attempting to getting over the mountain with the virus. What this means for investors is that all asset class will remain sensitive to vaccine-related developments. Should the news flow turn positive once again, we can expect that market trends in the direction of stronger stocks, risk appetite and less demand for safe havens can continue. And vice versa if the narrative is not providing a positive picture.

Opportunities that traders could keep an eye on at the moment is the improved buying demand for the Euro across its counterparts. EURGBP and EURJPY are perhaps the more impressive ones. EURJPY is now within 30 pips of the potential high that it could reach as maybe 118.80 as highlighted here.

(EURJPY Daily FXTM MT4)

EURUSD continues to find a potential limit on its advance around 1.10. For a stronger correction in the Eurodollar, it is likely that potential buyers will wait to see whether EURUSD can peek its neck above the waters of 1.10 first. EURGBP also looks appealing with some gas perhaps left in the tank for the pair to point higher. Buyers potentially require a close above 0.90 for today’s daily candlestick for further encouragement on the conviction of this pair.

Elsewhere one of the unlikely winners from some helping hands to support emerging markets has been the South African Rand. USDZAR declined to its lowest level since late March following the central bank cutting interest rates in South Africa once again today. Should USDZAR continue to trend lower, it is possible for the pair to decline to levels not seen since earlier in the same month of March.

(USDZAR Daily FXTM MT4)

While trading volumes and volatility appear slow for major stock markets into the end of week, it might be worth keeping an eye on S&P 500 on the daily charts. This asset has struggled to move above 3000 since early March but price action is suggesting another attempt could be on the way.

(S&P 500 Daily FXTM MT4)

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Shares of Arbutus Biopharma traded higher after the company reported significant and continuous reduction in HBsAg in 12 chronic hepatitis B subjects using 60 mg dosage of its AB-729 drug.

Clinical-stage biopharmaceutical company Arbutus Biopharma Corp. (ABUS:NASDAQ), which is focused on developing a cure for people with chronic hepatitis B virus (HBV) infection, yesterday announced “positive follow-up data from a Phase 1a/1b clinical trial (AB-729-001) in chronic HBV subjects on nucleos(t)ide therapy who received a single subcutaneous injection of 60 mg of AB-729, a proprietary GalNAc delivered RNAi compound.”

The company’s President and CEO William Collier commented, “These new data further demonstrate the robust activity of AB-729. At week 12, the 60 mg single-dose achieved equivalent reductions in HBsAg as the 180 mg single-dose. We are currently dosing chronic HBV subjects in a multi-dose cohort with 60 mg of AB-729. These data keep us on track for achieving our goal of delivering a combination therapy that includes HBsAg reduction in chronic hepatitis B subjects.”

The firm’s Chief Development Officer Dr. Gaston Picchio remarked, “Importantly, throughout the 12 week period, not only does AB-729 demonstrate robust HBsAg reduction, it does so while remaining generally safe and well tolerated with no abnormal transaminase values in any of the six subjects…We are impressed by both the magnitude and continuous reduction in HBsAg achieved with a single 60 mg dose. We believe that these features could provide a competitive advantage with a low dose and reduced frequency of injections…As we previously announced we are also exploring an additional 90 mg single-dose cohort. We expect data from both the 60 mg multi-dose cohorts as well as week 12 90 mg single-dose data in H2/20.”

The company explained that AB-729-001 is an ongoing first-in-human clinical trial consisting of three parts. Part 1 included three cohorts of randomized healthy subjects, Part 2 enlisted six non-cirrhotic, HBeAg positive or negative, chronic HBV subjects, and Part 3 is studying chronic HBV DNA negative and HBV DNA positive subjects who will receive multi-doses of AB-729 for up to six months.

The company stated on its website that hepatitis B is a potentially life-threatening liver infection caused by HBV, which can cause chronic infection that leads to a higher risk of death from cirrhosis and liver cancer. The firm additionally indicated that the World Health Organization estimates that chronic HBV infection affects 250 million people worldwide.

The firm stated that the COVID-19 situation has resulted in significant disruptions to many businesses and that measures closing businesses and requiring people to stay in their homes raises uncertainty regarding the ability to travel to hospitals in order to participate in clinical trials. The firm stated that “while we have been able to progress with our clinical and pre-clinical activities to date, it is not possible to predict if the COVID-19 pandemic will negatively impact our plans and timelines in the future.”

Arbutus Biopharma is a biopharmaceutical company based in Warminster, Penn. The firm is engaged in discovering, developing and commercializing a cure for people with chronic hepatitis B (HBV) infection. The company stated that it is investigating several drug product candidates that may be combined into a potentially curative regimen for chronic HBV infection.

Arbutus Biopharma has a market capitalization of around $129 million with approximately 68.96 million shares outstanding. ABUS shares opened nearly 44% higher today at $2.69 (+$0.82, +43.85%) over yesterday’s $1.87 closing price. The stock has traded today between $2.28 and $2.69 per share and is currently trading at $2.38 (+$0.51, +27.27%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

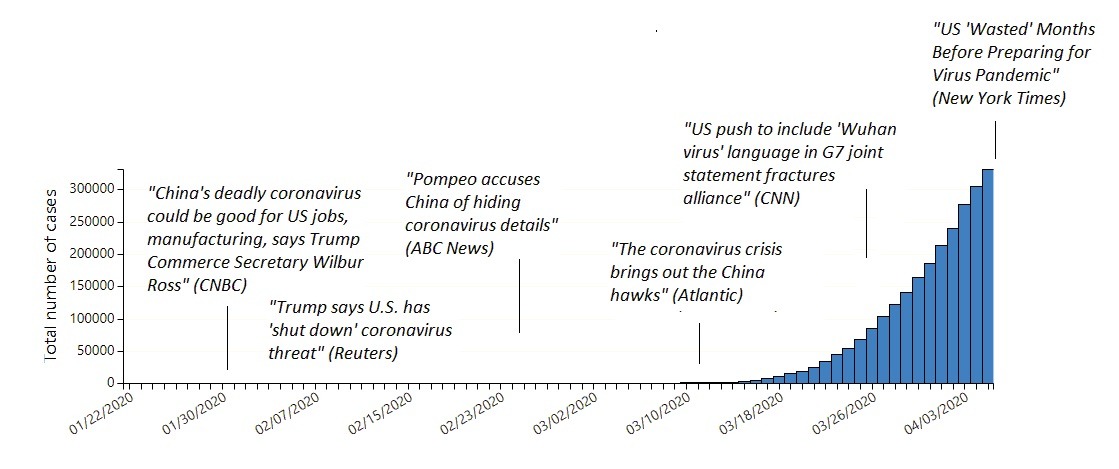

– After the disastrous mishandling of its COVID-19 battle, the Trump White House blames China for the virus, at the cost of American lives and worst contraction since the 1930s.

Ironically, President Trump thanked President Xi for China’s success in the virus battle in late January. But he adopted a very different tone as the White House mishandled the outbreak permitting the virus to spread in America [for the full story, see my COVID-19 report, The Tragedy of Missed Opportunities].

In fact, Trump’s own cabinet took an adversarial stance from the beginning. If the escalation will continue, that stance could result in a new Cold War and the Second Global Depression in the coming years.

Blaming China for Trump’s COVID-19 mishandling

The efforts to exploit the crisis for political purposes began early in the year. On January 30, right after the ‘Phase 1’ trade deal and the national virus emergency in China, Commerce Secretary Wilbur Ross declared the outbreak in China would benefit US manufacturing and bring jobs back to America. He was seconded by Trump’s trade advisor, Peter Navarro, who pledged US tariffs on Chinese imports would not be lifted even if the deadly coronavirus weighs on China’s economy.

Despite the first novel coronavirus cases in the US, both Ross and Navarro apparently presumed the virus would not spread in America.

Between early January and mid-March, the Trump White House’s accusations against China intensified with broad criticism of the administration’s mishandling of the outbreak, particularly as US debate escalated over botched evacuations, faulty test kits and delays in testing, shortages of personal protective equipment (PPE) and additional PPE shortages due to tariff wars, failed responses and associated elevated health risks, inadequate quarantines, failed self-quarantines, premature exits from lockdowns and the list goes on.

That’s when politicized attacks were initiated by Secretary of State Mike Pompeo and Health and Human Services Secretary Alex Azar who blamed China for the U.S. virus crisis. Meanwhile, Trump sought to “talk down” the virus impact in the markets.

When the WHO declared the global emergency on Jan 30, Trump still claimed that “we have it very well under control.” Even in early March, he described the virus as “very mild” and said the infected could get better by “going to work.”

Ironically, as the Trump White House repeatedly labelled the virus a “China virus” or “Wuhan virus,” that fostered a perception that the outbreak would be limited to China, while it was actually exploding in America and Europe.

When these deflection efforts failed to halt public criticism of the administration, the Trump White House began to exploit even reputable media to launder unsubstantiated intelligence meant to ratchet up tensions with China. The hope is that scapegoating – the “Chinagate” – would steer attention away from the Trump administration’s catastrophic disastrous mishandling of the COVID-19 crisis.

That’s why the politicized efforts to re-redefine the COVID-19 as the “China virus” continued into late March (and prevail even today). That’s when the numbers of US virus cases and deaths began to soar.

Use of scapegoats in paranoid politics

Instead of international cooperation to beat the pandemic, the Trump White House and its Republican supporters are on a survival mode. They hope to ensure Trump’s second term. That’s why another critical moment was missed when Pompeo called for COVID-19 to be identified as the “Wuhan virus” at the G7 Summit in late March.

Obviously, European officials resisted the redefinition since the WHO had cautioned against giving the virus a geographic name because of its global nature. But in the process, precious time was missed as US domestic political priorities overrode the urgency for international cooperation against the global pandemic (Figure).

FigureChina as the Scapegoat for U.S. Mishandling of the Pandemic

The purposeful use of projective bashing of targeted scapegoats has a long history in US politics. In the mid-1960s, Richard Hofstadter, the iconic historian of postwar liberal consensus, defined it as a recurring “paranoid style in American politics.”

In the effort to explain away the presence of class, ethnic, and immigration divisions in America, this style projects such divides onto other countries, real or imaginary adversaries, as evidenced by the 1950s McCarthyism, the Trump administration’s controversial ties with the U.S. alt-right movement, and Trump’s personal paranoid style that sparked warnings by leading American psychiatrists and psychologists already three years ago (The Dangerous Case of Donald Trump, 2017).

These views have been echoed by former US ambassador to China Max Baucus, who recently warned that he feared the Trump administration’s rhetoric against China was leading the US into an era “which is similar to Joe McCarthy back when he was red-baiting the State Department, attacking communism.”

Months of missed opportunities

The Trump administration knew about the virus risks already by January 3, when CDC Director Dr. Robert R. Redfield called Secretary of Health Azar, telling him China had discovered a new coronavirus. Azar made sure the National Security Council (NSC) knew about the virus because in early 2017 Trump had eliminated NSC’s global health unit, despite warnings about possible future pandemics.

As the New York Times has reported, the new virus team began daily meetings in the basement of the West Wing, yet no mobilization was initiated. Rather, a long debate began within the White House over “what to tell to the American public,” even as Trump, Pompeo and Azar blamed China for the lack of transparency.

Although the government’s leading scientists and health experts raised the alarm early and pushed for aggressive action, they faced resistance at the White House. Trump didn’t want markets to be spooked by panic. As a result, misguided political priorities continue to override science-based policies stressing public health.

The cult of secrecy in the White House has not eased. In mid-April, Dr Anthony Fauci, a key member of the virus task force, was asked by the CNN, whether earlier mitigation efforts could have saved more lives. Truthfully, he admitted: “If we had right from the very beginning shut everything down, it may have been a little bit different. But there was a lot of pushback about shutting things down back then.” Hours later, Trump retweeted a user who said it was “Time to #FireFauci.”

The recent confrontation between Trump and Fauci about the dangers of a premature exit from the lockdown is still another example of Trump’s political priorities, at the expense of American lives and U.S. economy.

Whatever the ultimate reason for the painfully long delay in the mobilization against the virus in America, the fact remains that, like Hong Kong and Singapore after January 3, the Trump White House could have begun the virus battle proactively.

For almost three months, it chose not to. And when it could no longer could hide its catastrophic mistake, the White House blamed China for the catastrophe.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net