Global equities advance continues today after China’s Foreign Minister Wang Yi’s warning Sunday that some US officials are pushing relations “to the brink of so-called ‘new Cold War’ “, endangering global peace. Investors’ risk appetite was buoyed by President Trump’s announcement he is “not going to close the country” to prevent the spread of a potential second wave of COVID-19.

Forex news

Currency Pair

Change

EUR USD

-0.07%

GBP USD

-0.63%

USD JPY

+0.01%

The Dollar strengthening continues today . The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, gained 0.3% Friday. GBP/USD and EUR/USD continued falling Friday and are lower currently as German statistics office Destatis confirmed the German economy contracted 2.2% in the first quarter compared with the previous quarter. Data showed Friday UK retail sales fell by a record 18%. USD/JPY joined AUD/USD’s continued sliding on Friday, but has reversed higher currently after news the government was considering a fresh stimulus package worth over $929 billion. Australian dollar’s slide against the dollar is intact.

Stock Market news

Indices

Change

Dow Jones Index

+0.32%

Nikkei Index

+1.85%

Hang Seng Index

-1.16%

Australian Stock Index

+0.83%

US equity markets are closed today for Memorial Day. Stock indexes in US ended essentially unchanged on Friday while recording solid weekly gains: the three main US stock indexes recorded daily returns ranging from -0.03% to +0.4%. European stock indexes are extending gains currently with British markets shut for public holiday. Asian indexes are mostly rising today led by Australia’s All Ordinaries ASX 200 Index, which jumped 2.2%. Chinese stocks are mixed with Hong Kong’s Hang Seng index down after the US Commerce Department on Friday added 33 Chinese companies and other institutions to a blacklist for human rights violations.

Commodity Market news

Commodities

Change

Brent Crude Oil

-1.41%

WTI Crude

+0.21%

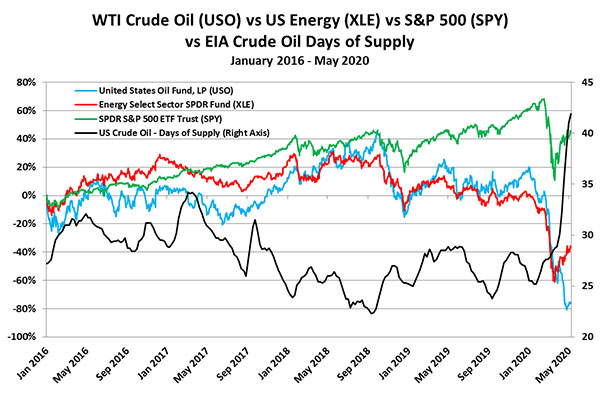

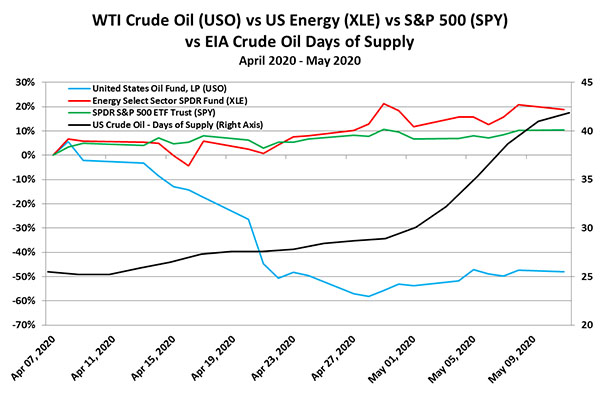

Brent is extending losses today. Oil prices ended lower last session as China’s top economic official said at National People’s Congress on Friday that the country won’t set a growth target for 2020, vowing to spend more to repair economic damage from the coronavirus outbreak. Prices fell despite Baker Hughes report on Friday that the number of active US rigs drilling for oil dropped by 21 to 237 last week, the tenth consecutive drop in a row. The US oil benchmark West Texas Intermediate (WTI) futures ended lower Friday: July WTI fell 2% but is rising currently. July Brent crude closed 2.6% lower at $35.13 a barrel on Friday, booking a 8.1% gain for the week.

Gold Market News

Metals

Change

Gold

-0.38%

Gold prices are retracing lower today. June gold added 0.7% to $1735.50 an ounce on Friday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

– Many stock market investors believe that prices have already bottomed. Numerous banks, brokers and financial firms have issued statements saying as much.

Indeed, the May Elliott Wave Theorist, a monthly publication which has offered analysis of financial and social trends since 1979, noted:

On April 28, Bloomberg interviewed four money managers to answer the question of “Where to Invest $1 Million Right Now.” Cash was not mentioned.

All these professional financial observers might be right in their assessment that the bottom is in for stocks.

Then again, the stock market rise since the March 23 low might be a bear-market rally.

If so, it certainly has “done its job,” meaning, as one of our global analysts put it in Elliott Wave International’s May Global Market Perspective (a monthly publication which covers 40+ worldwide markets):

The job of [the first, big bear-market] rally is to recreate the optimism that existed at the previous highs.

One particular sentiment that the rally has “recreated” is known by the acronym FOMO, which stands for the “fear of missing out.”

A little background: Toward the end of 2019, the FOMO sentiment was prevalent. Indeed, our December 2019 Elliott Wave Financial Forecast (a monthly, U.S.-focused publication which covers stocks, bonds, gold, silver, the U.S. dollar, the economy and more) showed this chart and said:

Last week, the percentage of bulls polled in Investors Intelligence Advisors’ Survey rose to 58.1, a new 13-month extreme. … Last month we talked about the return of FOMO, the fear of missing out on stock gains; its last major outbreak occurred as stocks approached their January 2018 highs. In November, FOMO became far more entrenched. One Bloomberg commentator called it “the age-old fear of missing out” and stated, “The end of the year is coming, when investment managers will be judged on their performance. Those who are behind have an incentive to clamber into the market now, while there is still time.” In our experience, “to clamber” is generally not a sound investment strategy.

As you know, it wasn’t long thereafter that the stock market topped. The major price moves downward were historic.

Even so, the “fear of missing out” sentiment has returned — again.

Here’s an April 7 Bloomberg headline:

FOMO Overwhelms Stock Traders Who Have Begun Ignoring the Risks

Our May Elliott Wave Financial Forecast provides more insight:

According to Google News, the number of articles referencing FOMO and “stock market” increased from 227 in December 2019 to 244 in February 2020, right through the peak in the market. In March, the market’s decline was well established, still the FOMO news count rose to 267.

So, yes, the rally has indeed “recreated” the prior optimism. One might even argue that the level of optimism is now even higher.

So, should investors take the stance that the bottom is in – or, proceed with extreme caution?

Knowledge of the stock market’s Elliott wave pattern will help you to answer that question.

As the Wall Street classic book, Elliott Wave Principle: Key to Market Behavior, by Frost & Prechter, notes:

The primary value of the Wave Principle is that it provides a context for market analysis. This context provides both a basis for disciplined thinking and a perspective on the market’s general position and outlook.

You only need a Club EWI membership, which is also free. Club EWI is the world’s largest educational Elliott wave community and allows you to get Elliott wave insights on investing and trading, the economy and social trends that you will not find anywhere else.

This article was syndicated by Elliott Wave International and was originally published under the headline Why Bear-Market Rallies Are So Tricky. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

Rick Mills of Ahead of the Herd asks if it’s possible to rescue the economy while also making big cuts to greenhouse gas emissions and improving overall health, and discusses one company with a large lithium deposit that could go a long way to providing U.S.-sourced material for batteries.

The pause in industrial activity brought about by the Covid-19 crisis has led us to a fork in the road with respect to the direction we as a society take in fulfilling the twin mandates of suppressing global warming and growing the economy in challenging times.

To some extent these goals are incompatible. In a world that continues to run on fossil fuels, how do policymakers wean countries off oil and gas without wrecking their economies? And from an environmental point of view, how can we continue to drive gas-powered vehicles and heat our homes with natural gas and coal, when we know emissions from these fuels add to greenhouse gases that, left unchecked, will eventually render much of the earth uninhabitable?

Unexpectedly, the coronavirus has provided a window into a future with fewer carbon emissions. While nobody hoping for a cleaner environment would wish to pair ecological progress with the worst economic slowdown since the Great Depression, the pandemic does show what happens when industrial activity abruptly stops.

As we now know, clearer skies owing to Covid-19 lockdowns have become the silver lining of the global economy coming to a screeching halt in March.

Combine stay at home orders with travel bans, business closures and the fact that demand for oil has fallen off a cliff with economies locked down, and you get global carbon output dipping for the first time since the 2008 financial crisis.

China, the world’s worst polluter, emitted 25% less carbon during a one-month period compared to a year ago, as people were instructed (and in some cases forced) to stay home, factories were shuttered and coal use fell by 40%.

The South China Morning Post reported a significant improvement in China’s air and water quality during the first three months of 2020. Limits on industry and travel upped the number of good air quality days by 11.5% compared with the same time last year in 337 cities across China.

Levels of PM2.5, the smallest and most harmful air pollution particles, dropped 18% between January 20 and April 4. The amount of nitrogen dioxide, a greenhouse gas that causes respiratory problems and cancer, was down 42%.

The country’s water quality was also much improved, shown by reduced phosphorous and ammonia chemicals.

The sharp drop in fossil fuel pollution during the month of April will result in 11,000 fewer deaths in European countries. A study by the Centre for Research on Energy and Clean Air found measures in Europe to contain the spread of coronavirus resulted in a 40% drop in coal-generated power and one-third lower oil consumption.

Madrid saw a 56% drop in the levels of nitrous oxide, a product of burning fuel, with Paris, Milan, Brussels, Belgium and Frankfurt experiencing similar reductions. In New York State, the U.S. epicenter of Covid-19, measures to contain the virus have cut air pollution in half.

So here we are, at a crossroads. In several countries Covid-19 case curves are leveling off, prompting health authorities to gradually lift social distancing restrictions and allow businesses to resume operations. As the re-opening continues, policymakers need to ask themselves: How do we return the economy to pre-virus levels, by getting people working and spending again? Is it possible to rescue the economy while also making big cuts to greenhouse gas emissions and improving our overall health?

The answer to the second question is “yes.” And the way to do it is through a massive “green stimulus” program. We are not talking pie-in-the-sky, no “Green New Deal” schemes costing trillions, espoused by twits and putting governments even deeper in debt, which as we know from a previous article, strangles gross domestic product. No, what we want to see happen is the roll-out of clean and green infrastructure that puts thousands of people to work, restores confidence in heavy industry, while at the same time cleans up the environment and provides renewed hope for a cleaner, safer, sustainable planet for future generations.

It’s something we here at AOTH have been talking about for years, and we’re not alone.

The International Energy Organization’s executive director recently said that turmoil in the oil sector caused by Covid-19 should be seen as an opportunity to embrace green energy. In an interview with Reuters, Faith Birol said lithium-ion batteries and the use of “electrolyzers” to produce hydrogen should be candidates for government subsidies and policy support.

A recent report from Oxford University cited by Oilprice.com concurs the world is at a crucial point in its history, when we either take a step forward in supporting industries that get us to where we need to go in terms of reducing our carbon footprint and cleaning up our environment, or we slide back to a business-as-usual scenario where fossil fuel use continues apace:

Given the scale of spending under consideration, then, there is a once-in-a-generation opportunity to “build back better,” the Oxford report argues. “The recovery packages can either kill these two birds with one stonesetting the global economy on a pathway towards net-zero emissionsor lock us into a fossil system from which it will be nearly impossible to escape,” they warned.

For the United States and China, infrastructure spending is a key piece of the rebuilding puzzle.

U.S. President Trump realizes he needs a strategy for playing through the pandemic, i.e., a means to pull the U.S. up from its bootstraps when, not if, the economy turns around.

It’s likely that Trump stole the idea from the Chinese, who have been touting their own form of blacktop politics as a way of restoring the economy, particularly manufacturing, which has been crushed by the coronavirus.

Beijing is reportedly eyeing a $570 billion infrastructure build-out, not unlike its stimulus package of 2008, to get the economy back on track.

Among the projects that could receive a huge boost in investment, courtesy of a government rescue package, are a $44.2 billion expansion to Shanghai’s urban rail transit system, an intercity railway along the Yangtze River ($34.3B), and eight new metro lines worth $21.7 billion, to be constructed in the virus epicenter city of Wuhan.

Employment creation must obviously be a factor in deciding how to restore crippled economies, given the millions of jobs losses from Covid-19.

The Oxford economists note that construction jobs for renewable energy installation or retrofitting buildings can’t be offshored, and that they are labor-intensivefor every million dollars spent, 7.49 full-time renewable energy jobs are created but only 2.65 jobs in fossil fuels.

Lithium vs hydrogen

If we accept the idea that we need to “go green,” the next question is, which technologies should be supported? Solar and wind are well-developed verticals that will continue to grow, especially as their costs per kilowatt-hour drop relative to natural gas, coal and hydroelectric power, and as renewable energy storage technology keeps improving.

While the biggest obstacle to large-scale energy storage is cost, recent analysis by BloombergNEF found that for applications requiring two hours of energy, lithium-ion batteries are beating natural gas peaker plants on price.

Vehicles are a major source of air pollution. According to the Environmental Defense Fund, the transportation sector is responsible for a quarter of U.S. greenhouse gas emissions. Passenger vehicles produce four times more greenhouse gases than all of domestic aviation.

The electrification of the global transportation system has long been seen as essential to reducing carbon emissions. The two technologies with the capability of delivering vehicles with zero emissions are battery-electric powertrains and hydrogen fuel cells.

An electric vehicle can run on either rechargeable batteries or fuel cells that convert hydrogen into electricity. Both have zero tailpipe emissions, but over the years, cars run on batteries have emerged as the clear winner compared to hydrogen-powered EVs.

There are a few reasons for this. The first is the lack of hydrogen infrastructure. Although fuel cell technology has the advantage of a fast fill-up time, minutes as opposed to the hours-long charge that batteries need, it has proven challenging and expensive to build and support a network of fueling stations that can deliver a highly explosive gas, compressed to 10,000 psi, reliably, quickly and safely.

In California, the only place where hydrogen vehicles can operate as it’s the only state with a (still unreliable) hydrogen fueling network, a goal of 100 hydrogen fueling stations by 2020 has fallen short; as of April 8, the state only had 40. Each station costs around $2 million, making them prohibitively expensive.

Compare that to 18,000 EV charging stations servicing half a million plug-in cars currently traveling on California’s roads.

Also, hydrogen isn’t all that green if the feedstock used to create it is natural gas, which it usually is. Until the electricity is fully renewable, hydrogen vehicles will always have higher CO2 emissions than electric cars.

Finally, the cost per mile favors battery-electric vehicles over hydrogen. Filling a Toyota Mirai or Honda Clarity Fuel Celltwo of only three (the other is the Hyundai Nexo) hydrogen models availablecosts north of $50. Home-charging an electric car on average costs what a gasoline car would if gas sold at $1 a gallon.

The upshot is that BEVs have swamped hydrogen cars. According to The Drive, Despite more than half a century of development, starting in 1966 with GM’s Electrovan, hydrogen fuel-cell cars remain low in volume, expensive to produce, and restricted to sales in the few countries or regions that have built hydrogen fueling stations.

Meanwhile, 10 years after the first modern EVs went on sale, electric cars sell in the low millions a year globallytwo orders of magnitude higher than their hydrogen counterparts.

Since 2010 1.3 million battery-electric and plug-in hybrid vehicles have been sold in the US, compared to around 8,000 hydrogen cars.

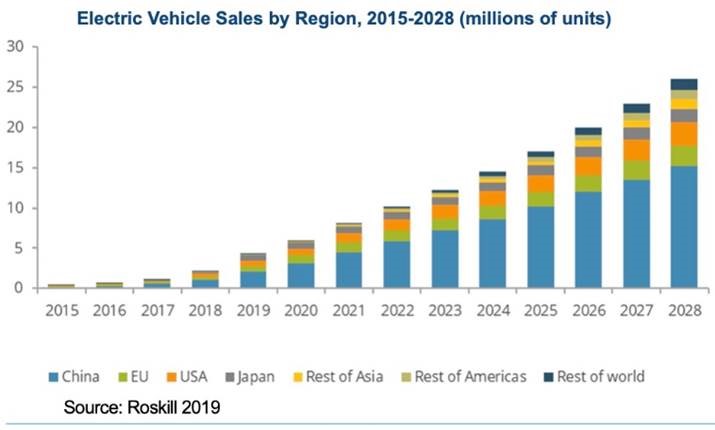

A Reuters analysis shows that automakers are planning on spending a combined $300 billion on electrification in the next decade. Meanwhile more battery factories are being built globally; demand for lithium-ion batteries is forecast to grow at a CAGR of over 13% by 2023.

All of this growth in battery plants and EVs will mean an unprecedented need for the metals that go into them. This includes lithium, cobalt, rare earths, graphite, nickel and copper.

Lithium carbonate and lithium hydroxide are key components of the lithium-ion battery cathode, making it an extremely sought-after battery ingredient.

Lithium, therefore, is expected to see a 29X increase in demand, driven not only by lithium required in EVs batteries, but in consumer electronics like smart phones and power tools, and grid-scale electricity storage.

Yet despite the rosy projections, electric vehicles have a long way to go before they make any kind of a dent in the total vehicle market, which remains dominated by cars, trucks and vans run on gasoline or diesel fuel.

In 2019 sales of plug-in passenger cars achieved a 2.5% market share of new car sales, and while that is up from 2.1% in 2018 and 1.3% in 2017, it means over 97% of global new-car sales were regular vehicles.

The biggest obstacles to higher EV market penetration are resistance to change, range anxiety and price. According to The Drive, 58% of drivers are afraid they will run out of charge while on the road, and another 49% fear the low availability of charging stations.

For many North Americans, sticker shock is a non-starter. While some EV models have come down in price, the lowest-cost Tesla Model 3 in 2019 was $42,900, nearly 19% higher than the national new-car average of $36,115.

Building a better battery

Although electric vehicles have existed as prototypes and with limited commercial production since the 1990s (General Motors’ EV1for a great history watch ‘Who Killed the Electric Car?’), the momentum in the switch from cars equipped with gas and diesel-powered internal combustion engines (ICE) to vehicles powered with lithium-ion batteries started in 2009 by then-President Obama. Obama announced his administration was putting aside $2.4 billion in order for American manufacturers to produce hybrid electric vehicles and battery components.

Of course Tesla was a few years ahead of Obama, forming in 2003 and producing its first model, the all-electric Model S sedan, in 2008.

Electric vehicles have far fewer moving parts than gasoline-powered cars they don’t have mufflers, gas tanks, catalytic converters or ignition systems. There’s also never an oil change or tune-up to worry about. But the clean and green doesn’t end there. Electric drives are more efficient than the drives on ICE cars. They are able to convert more of the available energy to propel the car therefore using less energy to go the same distance. And applying the brakes converts what was wasted energy in the form of heat, to useful energy in the form of electricity to help recharge the car’s batteries.

EV automakers want to know: How can batteries be made cheaply enough to compete with gas-powered vehicles, and with a reasonable range that doesn’t have the driver frantically searching for a charging station in the middle of nowhere?

By 2025 the cost of a large battery pack, say 60 kilowatt-hours with a range of +200 miles, is expected to fall to $100 per kWh or less, which is the point when EV prices would reach parity with gasoline vehicles, notes The Drive.

Achieving price parity is critical. Lower prices would not only give people an incentive to buy their first EV, they would facilitate the green infrastructure build-out we and others have been suggesting could be a way out of the virus-induced economic slump.

Recently Tesla announced plans to introduce a new battery in its Model 3 sedan, in China this year or early next.

Reuters reports the new low-cost, long-life battery is expected to bring the cost of electric vehicles in line with gasoline models, and will allow EV batteries to have second and third lives in the electric power grid.

The batteries designed to last a million miles will rely on low-cobalt and cobalt-free chemistries. The California-based company with “gigafactories” in Nevada and China, is reportedly talking to CATL, the largest electric-vehicle battery maker in the world, about employing CATL’s lithium iron phosphate batteries, which use no cobalt, the most expensive metal in EV batteries.

Prices for these cobalt-free battery packs have fallen below $80 per kilowatt hour, while CATL’s low-cobalt NMC (nickel, manganese, cobalt) battery packs are close to $100/kWh. Comparable low-cobalt batteries being developed by General Motors and Korea’s LG Chem are not expected to reach those levels until 2025.

Tesla is also working on recycling and recovering nickel, cobalt and lithium, and re-purposing lithium batteries in grid storage systems such as the one it built in South Australia in 2017 to capture electricity from nearby wind turbines.

Reuters states,

Taken together, the advances in battery technology, the strategy of expanding the ways in which EV batteries can be used and the manufacturing automation on a huge scale all aim at the same target: Reworking the financial math that until now has made buying an electric car more expensive for most consumers than sticking with carbon-emitting internal combustion vehicles.

US mine–>battery–>EV supply chain

We applaud Tesla and its pioneering, though mercurial CEO, Elon Musk, for being first out of the gate with electric-vehicle technology. Being a first mover in the EV space has made Musk rich beyond his wildest dreams and allowed Tesla the capital to innovate and stay ahead of its competitors.

However, we question Musk’s strategy of rolling out his new batteries in China, which has become the bogeyman of international commerce, and getting into bed with a Chinese company, CATL.

Need we remind readers, the Chinese government undertook pernicious measures to conceal the coronavirus outbreak in Wuhan. They included destruction of virus samples, suppression of information, and delaying lockdown of a city of 11 million, allowing the virus to spread throughout China and worldwide, through airline travel during the Chinese Spring Festival, the largest annual migration of holiday travelers on earth.

The U.S., Australia and all 27 nations of the EU are demanding an investigation into whether the World Health Organization was complicit with China in concealing Covid-19 from the rest of the world for six weeksenough time to prepare a public health response.

Shenanigans like hoarding key medical gear in a near monopoly, then profiting handsomely from sales to desperate buyers, has led to the Trump administration “turbocharging” an initiative to distance itself from China. According to a recent Reuters article, economic destruction and the U.S. coronavirus death toll are driving a government-wide push to move U.S. production and supply chain dependency away from China…

The U.S. wants to create an alliance of “trusted partners” called the Economic Prosperity Network. Participating countries include Australia, India, Japan, New Zealand and Vietnam. Secretary of State Mike Pompeo said the goal is to “prevent something like this from happening again.” (Canada, which refrains from criticizing Beijing due to fear of retaliation, didn’t get an invite.)

Pompeo is referring to how the pandemic exposed China’s tight grip on global supply chains for generic drugs and medical equipment. Although the country accounts for only 13% of active pharmaceutical ingredient (API) makers supplying the US market, it produces many APIs for widely used medicines along with chemicals used to formulate APIs. Often China ships them to India for processing into tablets.

Such medicines include antibiotics, ibuprofen, acetaminophen and heparin, an anticoagulant taken by patients with heart disease.

We like the idea of a network of trading nations who believe in free trade and open borders without harboring secret ambitions to monopolize certain sectors, as China has done with critical minerals, solar power and medical supplies, to name just three.

China has locked up the rare earths market and is the primary player in a number of critical metals markets including lithium, cobalt, graphite, manganese and vanadium.

The Asian superpower imports 98% of its cobalt from the DRC and produces around half of the world’s refined cobalt.

Last year, as part of its trade war strategy, China raised the prospect of restricting exports of rare earths, which are critical to America’s defense, energy electronics and auto sectors, similar to a 2010 Chinese ban on rare earth oxide exports to Japan.

China produces roughly two-thirds of the world’s lithium-ion batteries and controls most of the processing facilities.

Lithium is also among 23 critical metals President Trump has deemed critical to national security; in 2017 Trump signed a bill that would encourage the exploration and development of new U.S. sources of these metals.

According to Benchmark Mineral Intelligence, the U.S. only produces 1% of global lithium supply and 7% of refined lithium chemicals, versus China’s 51%. The country is about 70% dependent on imported lithium.

To lessen U.S. lithium dependency will require the building of a mine to battery to EV supply chain in North America.

The first step is to develop new North American lithium mines.

Currently the only U.S. lithium producer is chemicals giant Albemarle. Lithium products from Albemarle’s Silver Peak lithium brine operation in Nevada are sent to its processing plant in North Carolina. This material is then loaded on ships and sent to Asian battery manufacturers, which sell the batteries to EV companies.

It’s curious how several top automakers are planning on, or are already building, electric vehicle plants and facilities without disclosing how they will source their raw materials.

In 2017, Mercedez-Benz announced plans to set up an electric car production facility and battery plant at its existing Tuscaloosa, Alabama, plant. The $1-billion expansion will include a new battery factory near the production site, with the goal of providing batteries for a future electric SUV under the brand EQ. Six sites are planned to produce Mercedes’ EQ electric-vehicle family models, along with a network of eight battery plants.

Korean company SK Innovation has said it will invest US$1.7 billion in the U.S.’ first electric vehicle plant, to serve Volkswagen, in neighboring Georgia. The 9.8 gigawatt-hour-plant would be the first EV battery plant in the United States. SK recently announced a second 10-GWh plant requiring an investment of $1 billion.

GM has rolled out its 2020 Cadillac SUV, built in Spring Hill, Tenn., in a move designed to challenge Tesla.

Tesla’s vulnerability

Last year a Tesla executive said the company is worried about a long-term shortage of nickel, copper and lithium. The number of EVs are expected to multiply in coming years, but they can only progress as fast as the lithium-ion batteries can get built that go into them. In June of 2019, Musk said that in order to ensure Tesla has enough batteries to expand its product line, Tesla might get into mining lithium for itself.

Instead Musk seems to be going out of his way to court China, using its mine-battery-EV supply chain rather than supporting North American companies trying to develop domestic sources of EV raw materials.

Currently Tesla produces nickel-cobalt-aluminum (NCA) batteries with Japanese company Panasonic at its Sparks, Nevada, plant, and buys NMC batteries from LG Chem in China. Nothing local about that.

If Musk thinks his company can lead the world in EV sales by getting its raw materials from China, I’m afraid he is setting himself up for a big fail.

Chinese companies dominate the EV space and will do what they need to do to win market share. While Tesla in December surpassed BYD as the world’s largest electric car maker, without a safe, reliable supply chain, the company is vulnerable to a sudden supply shock that could stop production in its tracks. Case in point: in January the Chinese government temporarily shut down Tesla’s new factory in Shanghai over the coronavirus, delaying production of the Model 3 and denting the company’s first-quarter profits.

The trade war between China and the United States is far from over, in fact it appears to have entered a new phase. This week Trump said he was disappointed with China over its failure to contain the coronavirus and that the worldwide pandemic cast a pall over his trade deal with Beijingdespite a “phase 1” agreement signed in January.

Reuters reports the Trump administration is planning to deploy long-range, ground-launched cruise missiles in the Asia Pacific region, including versions of the Tomahawk cruise missile carried on U.S. warships, and the first new long-range anti-ship missiles in decades. The U.S. Air Force has also begun developing the first hypersonic cruise missile, capable of eluding detection by flying at least five times the speed of sound.

The technology the U.S. intends to deploy to counter China’s missiles uses lithium batteries and rare earth magnets. China controls the market in both.

We have an idea for Elon Musk and Tesla: how about they forget about signing battery deals with China and offtake agreements with Australia, which is a long way from Nevada, and instead look at investing in a lithium mine in the United States?

Three and a half years ago Cypress began prospecting in the Clayton Valley, Nevada, hoping to find a property that could support a lithium carbonate resource to compete with or possibly complement its neighbor, Albemarle’s Silver Peak Mine, whose lithium brine grades are declining.

Its Clayton Valley Lithium Project hosts an indicated resource of 3.835 million tonnes LCE (lithium carbonate equivalent) and an inferred resource of 5.126 million tonnes LCE. The project is ranked among the largest in the world.

Last year Cypress Development Corp. completed the first two phases of a prefeasibility study (PFS), confirming that lithium can be acid-leached and extracted at high recovery rates and successfully separating the lithium-rich claystone ores from the sulfuric acid leachate.

It is a major technical problem to separate ultra-fine clay particles (<5 microns) from a leach solution. Cypress has done it, putting the company at the forefront of lithium clay projects globally.

The U.S. now has a major source of lithium carbonate and lithium hydroxide and potentially a not-inconsiderable amount of rare earths including scandium, a highly prized metal used in aircraft components, for example.

The eagerly awaited prefeasibility study is crucial to moving the project forward, not only for proving that the metallurgical process for separating lithium from clays is commercially viable, but demonstrating that Cypress’ costs are in line with the 2018 preliminary economic assessment (PEA).

Cypress’ vision is to build a mine with the ability to extract whatever oxides they choose, from the processing plant. The project design is based on mining 15,000 tonnes per day to produce 25,000 tonnes per year of LCE.

The end result is that through by-product credits Cypress could shave millions of dollars off of their processing costs, further enriching what we already think is looking to be a very profitable mine.

Cypress is the only lithium junior in North America that has yet to sign an offtake or major financing agreement, despite its project being further advanced than nearby Clayton Valley lithium properties.

Partnering up with Tesla would make sense. Cypress needs a very large buyer for its lithium carbonate and lithium hydroxide end-products, and rare earth oxides needed for permanent magnets that go into EV motors. Tesla has to find a way to bring the cost of batteries down to $100 per kWh, which is the point when EV prices reach parity with gasoline vehicles. Cypress gives them the opportunity to buy their lithium raw materials directly from the mine, cutting out the Asian middlemen. No CATL, no more LG Chem. Surely that would bring down Tesla’s costs of production, allowing them to pass on the savings to EV buyers.

Finally, a U.S. company would have the capability of producing electric vehicles that are affordable to the average American, while also becoming the beach-head for a powerful North American electric-vehicle supply chain that could compete with China, and be independent of its critical minerals.

That would be huge.

There’s no way Silver Peak can produce enough lithium to supply American needs, especially with all of the EV battery and auto production facilities planned.

When you think about the huge amount of ore available to be minedit’s among the largest LCE resources in the worldand the valuable products that will be coming out of the relatively easy processing flow sheet at the end, we believe Cypress may have the most important mine in America in decades.

Cypress has a very important study release coming virtually any daythe Prefeasibility study (PFS) on its Clayton Valley Lithium Project. A positive study result means CYP completes another step on its development path to building a mine.

The project is next to Albemarle’s Silver Peak Mine, Albemarle (NYSE:ALB) is the world’s largest lithium producer. Tesla is the world’s largest EV manufacturer, its gigafactory is just 200km away from CYP’s Clayton Valley Project.

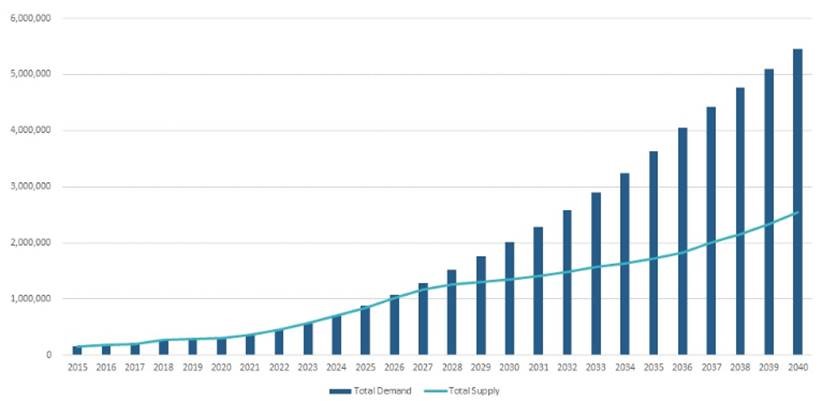

Current annual lithium (LCE) supply is around 360,000 tonnes. Total lithium demand of LCE is expected to reach over 1 million tonnes by 2025 or higher, states S&P Global Platts Analytics.

The United States is about 70% dependent on imported lithium.

How will the United States, how will Volkswagen, Tesla, Albemarle, GM, Mercedes and SK Innovation obtain enough lithium for the storm of demand that is brewing?

Cypress Development Corp TSX-V:CYP Cdn$0.19 2020.05.16 Shares Outstanding 90,077,001m Market cap Cdn$17,114,630m CYP website

Richard (Rick) Mills, AheadoftheHerd.com, lives on a 160-acre farm in northern British Columbia. Richard’s articles have been published on over 400 websites, including: Wall Street Journal, USA Today, National Post, Lewrockwell, Montreal Gazette, Vancouver Sun, CBSnews, Huffington Post, Beforeitsnews, Londonthenews, Wealthwire, Calgary Herald, Forbes, Dallas News, SGT report, Vantagewire, India Times, Ninemsn, Ib times, Businessweek, Hong Kong Herald, Moneytalks, SeekingAlpha, BusinessInsider, Investing.com, MSN.com and the Association of Mining Analysts.

Disclosures: 1) Rick Mills: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Cypress Development Corp. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company currently has a financial relationship with the following companies mentioned in this article: Cypress Development is an advertiser on Ahead of the Herd. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures/disclaimer below. 2) The following companies mentioned in this article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

Legal Notice/Disclaimer: Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH. Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it. Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified. AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice. AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report. AOTH/Richard Mills is not a registered broker/financial advisor and does not hold any licenses. These are solely personal thoughts and opinions about finance and/or investments no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor. You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments but does suggest consulting your own registered broker/financial advisor with regards to any such transactions.

Lesotho’s central bank lowered its key interest rate for the fourth time this year and slashed its growth forecast for this year to a contraction of 5.7 percent. The Central Bank of Lesotho (CBL) cut its rate by another 50 basis points to 3.75 percent and has now cut the rate 275 points this year following cuts in January and at extraordinary meetings of its monetary policy committee in March and April. Since July 2019, when CBL began its current easing cycle, it has cut the rate 325 basis points. “The rate, set at this level, will ensure that the domestic cost of borrowing and lending will be aligned with the cost of funds elsewhere in the region,” CBL said, lowering its target for the floor of net international reserves to US$530 million from $660 million. “The NIR target remains consistent with the maintance of the exchange rate peg between the loti and the South African rand. CBL’s rate cut was decided at a meeting of its policy committee on May 22, rather than on May 26 as scheduled. On May 21 the South African Reserve Bank (SARB) cut its policy rate by 50 basis points to 3.75 percent, its fourth rate cut this year. Lesotho is surrounded by South Africa and its economy relies on inflows and workers’ remittances. Along with Namibia and Eswatini (former Swaziland), Lesotho is part of the rand monetary area that uses South Africa’s rand as a common currency. In 1980 Lesotho introduced its own currency, the loti, which trades at par with the rand. “The domestic economy has generally been weak,” CBL said, adding measures of economic activity had declined 0.6 percent in March compared with a 0.2 percent decrease in February. The labour market showed a decline in employment in both manufacturing and migration mineworkers, consistent with lower demand for some of the large firms’ products, while government employment had improved slightly, CBL said. “While economic forecasts are likely to change, the economy is expected to contract by 5.7 per cent in 2020 mainly due to COVID-19 infection and control measures,” CBL added. In March CBL forecast growth this year would be lower than its earlier forecast of 2.2 percent and 2021 growth of 4.1 percent. In 2019 Lesotho’s economy grew an estimated 2.6 percent based on strong mining performance and a recovery in textiles. Lesotho’s inflation rate eased to 4.0 percent in March from 4.2 percent in February while gross international reserves rose to 4.7 months of import cover from 4.3 months in the first quarter.

In a Nutshell: The Federal Reserve instituted a policy of unlimited quantitative easing in March 2020 in response to the COVID-19 pandemic, in effect injecting trillions of dollars into the economy. But some analysts believe the consequences of that action may not be limited to stimulus checks and paycheck protection. According to Stefan Gleason, Director of the Sound Money Defense League, the Fed’s pandemic response is only the most recent manifestation of a long-standing inflationary monetary policy enabled by unbacked fiat currency. That’s why Gleason and the Sound Money Defense League advocate for returning to a limited currency backed by gold and silver to preserve the value of money and reward savers.

In March 2020, people in the U.S. began to shelter in place in the wake of the COVID-19 pandemic, and economic activity slowed considerably. The Federal Reserve pledged to put as much new money into the economy as necessary by purchasing government debt and asset-backed securities on the open market.

With that, the Fed effectively created new dollars through the issuance of credit — a process sometimes known as printing money. The Fed’s post-COVID-19 policy of unlimited quantitative easing has made trillions in new dollars available to policymakers to help protect businesses and consumers.

That sounds like a good thing — until it isn’t, according to Stefan Gleason, Director of the Sound Money Defense League.

Gleason’s Sound Money Defense League is the public policy arm of a group of businesses that includes Money Metals Exchange, a national precious metals investment company and news service with more than 500,000 readers and 150,000 customers. It also includes Money Metals Depository and Money Metals Capital Group, a lending agency.

According to Gleason, the Fed’s recent moves differ from long-standing monetary policy only in scale, not in intent. Since the creation of the fiat currency system in 1913, U.S. dollars have leaked value as the size and scope of government has increased.

What’s needed to halt this chronic inflation, Gleason said, is a return to a monetary system in which circulating currency is limited and backed by gold and silver rather than by government fiat.

“The constitution set up a system where gold and silver was the money of our country,” Gleason said. “And as we’ve severed ties with gold, it’s enabled huge deficits and massive growth of government. Gold and silver are the antidotes to that.”

Working to Reform the Legal and Financial Status of Precious Metals

Gleason came to his role as an advocate for the gold standard after more than 15 years of involvement in free-market politics.

“Some of that is pertinent to precious metals,” he said. “Since 1913, the goal of U.S. monetary policy has been to create inflation, which devalues savings through interest rates that are below the rate of inflation and thus basically steal purchasing power.”

The Sound Money Defense League works on the federal and state level in a variety of ways to promote the investment potential of precious metals and clear a path toward the eventual readoption of the gold standard.

Before the Great Depression, the Federal Reserve was required to have enough gold to back 40% of U.S. currency. But bank failures during the Great Depression frightened the public into hoarding gold, making the policy untenable. Soon after taking office in 1933, President Roosevelt ordered all gold coins and gold certificates in denominations of more than $100 turned in for other money, abandoning the gold standard and making possession legal again only in 1975.

The Sound Money Defense League supports legislation calling for an audit of U.S. gold reserves famously held at Fort Knox along with a review of the Federal Reserve itself.

On the state level, the Sound Money Defense League encourages states to remove sales and income taxes from monetary metals, hold precious metals as reserve assets, and take other steps to support sound money.

“At the state level, we also publish the Sound Money Index, which ranks and evaluates every state on its policies relating to precious metals and sound money,” Gleason said. Additional issues concern whether the states operate depositories for precious metals, whether they have laws that harass precious metals dealers and investors, and whether they invest in or hold precious metals in their pension and reserve funds. Wyoming, Texas, and Utah currently lead the index.

“We’re encouraging states to affirm that gold and silver are money as prescribed by Article 1, Section 10 of the U.S. Constitution,” Gleason said.

Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

As we head into this Memorial Day weekend and remember those who have fought for our great country over the years, those who gave their lives – the ultimate sacrifice – to protect the freedoms we enjoy, we thought it appropriate to highlight on this week’s podcast an issue and a man who is fighting for another form of freedom… that being our financial freedom.

Not long ago, I spoke to Larry Parks of the Foundation for Monetary Education. For the past several decades, Larry has tirelessly advocated for sound money and freedom from governmental repression through a deliberate, ongoing campaign of inflation and currency debasement. This corrupt system has also led to widespread debt enslavement while impoverishing many savers and wage-earners across the globe.

We hope you’ll enjoy this interview… and remember that when our liberty hangs in the balance, we must vigorously defend ourselves against those who would take away our freedoms, whether the threat be foreign OR domestic.

Mike Gleason: It is my privilege now to welcome in Lawrence Parks, founder and executive director of the Foundation of the Advancement of Monetary Education. Larry has dedicated much of his life towards the study and promotion of sound money, having author articles that have appeared numerous times in publications like The Economist, The Washington Times, National Review, and The Wall Street Journal just to name a few. He even hosts a weekly TV show that airs on cable networks in the Manhattan area called “The Larry Parks Show”. He is given expert testimony in Washington to the United States Congress on monetary policy. He’s a real champion for sound money, and it’s great to have him on with us today.

Larry thanks for the time and welcome. It’s good to talk to you.

Larry Parks: It’s a pleasure. Thank you for hosting this.

Mike Gleason: Well Larry, to set the stage here briefly give us some background about the Foundation of the Advancement of Monetary Education and what motivated you to take the helm of the organization nearly 25 years ago, let’s start there.

Larry Parks: I had been in the money management business and I had noticed along the way that I was getting severe distortions in the evaluation of the stocks that we used to cover. And I had known about the money issue, I had studied at one point with Murray Rothbard. And it wasn’t my intention right from the very beginning to do this. I tried to get other charities, other think tanks, to pay attention to this and nobody would touch it. Turns out there’s a good reason for that. Somebody suggested to me along the way “Why don’t you do it?” And I ended up doing it.

When we got started, we had all of the work that Committee for Monetary Education and Research did. (They) had several hundred monographs, a couple of which were authored by me. We had all that digitized. The people at The Foundation for Economic Education, that was Harry Stendhal’s at the time. They had all the work of Henry Hazlitt, I don’t know if you remember that name.

He was from The Times. He wrote a book called Common Sense Economics and stuff on gold, made all that stuff. I recruited 30 some odd board of advisers and board members, some of them had world-wide reputations, and we were off and running. And I thought that the gold space, especially the gold companies would sponsor our work but that never happened. It’s very interesting how the people on the other side, on the paper money side were able to co-op just about everybody and promulgate this, what I call this imaginary fake money into society on a worldwide basis. It’s just utterly remarkable they got away with this.

Mike Gleason: Now you’ve made the point that gold is the most important of all the commodities in the world, even more so than oil. Explain why you believe that to be the case if you would please?

Larry Parks: The reason gold is the most important commodity is that gold is the only way to ensure payment. And so the way I like to explain it is that the glue that holds society together is keeping promises. So for example I make up with you I’m going to be available at 3 o’clock today if I don’t keep my promise that hurts the relationship.

But the promises that are most important to society, aside from the promises that we make to family and friends, are the promises to pay. To pay pensions, to pay annuities, to pay savings, to pay rents, whatever. If those promises get broken society unravels. And so, what happens is that people who have promises of payment take pensions for example, pensions are really differed wages, they depend on that promise being kept. And in turn they make promises to other people mindful that they’re going to get paid. If that chain gets broken all of the inter relationships in society down and we’ve seen examples of that from all recorded history. The thing about gold is that gold is the only way to ensure payment over a long period. People think about gold as money they think about going to the grocery store, that’s absurd. Nobody would use gold for day to day transactions. Gold is important for payment into the future. And so, whatever it is that you use as money, say for example you use water, some of that water is going to spill. In the case of gold you have no spillage.

The guy who really put his finger on this the best is a guy named Carl Menger. He’s part of the so-called Austrian School of Economics picked up on Von Mises by Rothbard and others. And what they said was that gold is the sellable, most efficient money. And the way they measure that, and it’s really ingenious, if you look at all the things that could possibly be money and the things that have been money-like salt, cattle, copper, steel, all kinds of stuff- and you line them all up and you offer ever increasing amounts of each into the marketplace, the commodity for which the by sale spread increases the least that’s the most efficient money. And it just so happens that’s gold. No matter where you drop in in history, either in ancient times or Renaissance times, today, say in the 19th century, cross culture, cross time you see people using gold as money when it’s available. So it’s not like someone came down from the heavens and said “Look in China, in the Mideast, in Europe you have to use gold.” Somehow by trial and error they just figured out that gold is the most efficient money. But again it’s the key to holding society together.

Mike Gleason: Our listeners know that the market had chosen gold as the best form of money for thousands of years as you’ve just explained, but it hasn’t been openly used as money in recent decades. Talk about how and why gold was booted out of the world’s monetary system, at least officially.

Larry Parks: Well, what’s happened and this also goes back to ancient times, it was generally the rule of rulers of countries that said what the money was going to be. Best case is when the people themselves decided what the money was going to be, but a lot of times the rulers of those countries got involved with coinage. They put their images on it. They set the standards, but a long time ago people at the top of the heap figured a good way to steal was to debase the coinage. So in Renaissance times, when they started having precious metals as money, they used to clip the coinage. In modern times they figured out with things like factional reserve lending that they could really, in effect, debase the money completely. The problem with gold from that point of view is that gold protects the money.

So, if you have gold you have what you have. The way I like to say there’s no counterparty risk with gold. With everything else you have counterparty risk that somebody will do something that will damage the value of your currency. For example, if I pay you with a check, Mike, you have counterparty risk that the check may not be good. And if I pay you with a dollar, that we call a dollar today which is not a dollar, but what I call a dollar today you have counterparty risk that the issuing authority in our case it’s the banking system, the Federal Reserve and the banks, will depreciating the purchasing power of that money. And they tell you right out that they’re going to do that. The jargon for that is called inflation targeting. And see, you’re always at risk that after some long period you’re not going to have what you think you have, or you’re not going to get paid what you think you’re going to get paid.

However with gold it is what it is. By getting rid of gold they’re able, in effect, to engage in really a massive amount of thievery under the color of law of course where they transfer the wealth of society from the people who earn it — mostly ordinary working people — to the people who are in charge of the monetary system. We’ve developed on this end of the phone data from primary sources in this case the Federal Deposit Insurance Corporation, they have on their website one line for each year going back to 1934 when they got started of all the banking statistics. And up until the last tie to gold was broken, and that was in 1971, the money that went to the banks… and I can send anybody a chart on this if they wish just send me an email larry@larryparks.com… it was a small amount of money. It was a sum number of billions. Since the last tie to gold was broken in 1971 it’s in the trillions. Trillions. In dividends to their shareholders and in trillions in compensation to their employees. That would not be possible with gold.

Also, in the sense of the politicians there’s a very important book that people should take the time to read. It’s called “Fragile By Design” it’s by a Columbia Professor and his partner at, I think University of California by the name Steven Haber. It’s called “Fragile By Design” and they document very nicely that there is, on a world-wide basis what they call a grand bargain between the banking systems and the monetary authorities and banks in effect of paper money. When you have paper money you can have unlimited spending. So a lot of people complain about the deficit, about debt and what not. Well with paper money there is no limit to how much money you can spend. And if you have unlimited spending you get unlimited government. And if you have unlimited government the people in charge have unlimited power, they like that. Gold stands in the way. So, what they’ve done at this end in our country is, even though the Constitution guarantees us promises as gold and silver coin as money they’ve pretty much got gold out of the system and they’ve done it right from the get-go. Right from the time right after the Revolution. There’s a ton of stuff from 19th century where they recognize that gold is antagonistic to the paper money. And of course, the way they get you to use it is they force you to use it with what’s known as legal tender laws. Again another abomination.

Mike Gleason: There was a recent documentary financed and distributed by The Financial Times and in that piece one of their experts says gold is like “shiny pooh”. He goes on to say that “People who like gold are people who like to play with their pooh.” A silly comment to say the least but on a serious note, how do you explain the disdain for golf among financial elites Larry? Because this individuals comments are quite often shared by many.

Larry Parks: I can explain it in four words: gold pays no fees. So the people in the financial world especially on Wall Street, Wall Street is a fee business. So, when people have savings, and a lot of people are concerned, especially people who are at the upper end, they’re concerned about inter-generational wealth transfer, leaving money to their kids. People who retire, who are facing retirement, or plan to retire, they have and issue “How should I allocate my money?” And as far as Wall Street is concerned they want you to allocate it in a way that generates fees for them.

In the case of gold really the best thing that people can do for savings for the future is to buy gold, my favorite are U.S. Gold Eagles, and put them away. But if you do that where are the fees for Wall Street? And so, what they’ve done, it’s really incredible what they’ve gotten away with in the pension business. For example, in defined benefit pension plans in America there are roughly ten trillion dollars’ worth of investible assets. Ten trillion. And no gold. The only gold position that I can identify is the Texas Teachers Retirement System. They have a billion dollar position in physical gold out of roughly one hundred and forty billion dollars of investible assets but in the other ten trillion there’s no gold. And they have roughly something on the order of twenty some odd percent, last I looked around twenty-four or twenty-five percent of these assets in fixed income, these are Government bonds and court bonds, on the theory that people are safer.

In fact, the icon of American investing, that would be Warren Buffett, he said in one of his chairmen letters from his Berkshire Hathaway company followed up with an article in Fortune Magazine that the most unsafe, the most risky assets are currency denominated assets, and he specifically targets bonds. And the reason they’re unsafe and risky, the only risk you have to be concerned about is that at the end of the holding period that you have less purchasing power than when you started. The answer is that things like fixed income, that’s a guaranteed loser.

So how do you explain that you have ten trillion dollars, you have roughly two and half trillion dollars in the most risky most unsafe investment and no allocation to gold. And of course, the answer is, as I’ve said, gold pays no fees. So really what you have here is really cheating people on a massive scale, I mean it’s unbelievable how they’ve gotten away with this. In the last couple years there’s been talk about having these investment advisors having a fiduciary responsibility to their customers, and they defeated that. So basically, the way Wall Street works is that they’re in it for the fees. If the customer gets a good result, that’s a happy accident. So today… and I’ll tell you Mike it’s an incredible scandal, it doesn’t get enough press… there’s one hundred and fifty of these so-called multi-employer pension funds that are on the Department of Labor critical list which is to say they’re bust. And millions of workers are involved, what’s their remedy? What should these people do when they turn 65 or 70, whatever, and they can’t work anymore and their bodies are broken from the work that they used to do and they have no money, how are they supposed to live?

So really what’s happening in the country today is that there is, I perceive, a huge lean towards socialism. My view we are at best two election cycles, maybe one election cycle, away from the country going socialist. I don’t know how many people watched the State of The Union Address by President Trump, but he went out of his way to say in very strong terms he said, “We’re not going to have a socialist country.” Now you never heard any other President say something like that. The fact that he felt compelled to say that, they recognize also that there is this lean towards socialism. That would be an enormous tragedy, we are on the glide path right now to Venezuela.

Mike Gleason: Switching gears here a little bit, you talk to mining executives and you have your finger on the pulse there, so I want to ask you, do you think they believe there is price suppression in the metals’ markets? And as a follow up, if they believe there is – which to us seems hard to deny at this point – why don’t mining executives cry foul? Because it seems as though their companies would be the most impacted. Is it that they just don’t want to call out the very banks that they’re so depended upon for credit, or is it something else? Because the lack of an outcry for mining leaders has always baffled me Larry.

Larry Parks: Well, it’s not only baffling although I’ll give you an explanation for it, but it’s disheartening. These folks have fiduciary responsibility to their shareholders and also to themselves. Except for people like Rob McEwen, very good guy, and Rudi Fronk. Rob McEwen has McEwen Gold, Rudi Fronk at Seabridge. Very few have any kind of material interest in the companies at all. They’re in it for the payroll. In their defense, and it’s not a great defense but it is a defense, they don’t know anything about this business with gold and the monetary system. These guys, I don’t think there’s any women running any of these companies anymore. There was one woman and I think she sold out to Barrick some time ago. I forget her name. But basically, these people went to the Colorado School of Mines or its equivalent. Some of them have accounting degrees and that’s it. Also until recently none of these people were from America. So if you look at all the major gold companies, important gold companies, they were all headed by foreigners. So they don’t know anything about the constitutional issues here in America. Why would they?

So right now you have two. You have this fellow John Thornton who just took over a couple years ago at Barrick Gold. He’s an American. And Gary Goldberg who runs Newmont. But before Thornton took over it was Peter Munk. Peter Munk came from Hungary, grew up in Hungary, educated in Switzerland, considered himself a Canadian. Newmont was Jimmy Goldsmith, a Brit. And all the rest are from other parts of the world. No one knows anything about the provisions, the history and it’s really America that’s lead the way on this, not any other kind of country. There’s all a story to this, and I know we only have a few minutes for this podcast, but back in 1944-45 when the Bretton Woods Conference met really the dye was set there to get gold completely out of the system. Roosevelt did his part in 1933, but after Bretton Woods the idea was that the United States dollar would be convertible into gold for foreign governments and foreign central banks. At that time it was still a felony for Americans to own gold. That’s an interesting question you don’t get an answer to.

What is the public policy justification for making gold ownership in America a felony? I mean where have you seen that question asked in any economics textbook? Basically the guys that run these gold companies they don’t know about this. Why should they? They’re geologists, they’re mining engineers, it’s not part of their study.

Here in America educational system is highly controlled especially at the college level. Nobody gets ahead in economics talking the way I’m talking. The Huffington Post somebody did a study, and it turns out if you want to get ahead in the academy you have to publish. And it turns out that just about all the important economic journals are edited by a president or former employees of the Federal Reserve.

You don’t get ahead. So basically, there’s a lack of knowledge, and gold is denigrated and so those quotes that you gave from that Financial Times, imagine the Financial Times sponsoring, and I think that documentary, it’s called something like, “Dangerous Obsessions”… if you go on YouTube you can search those key words, dangerous obsession… it’s just outrageous that an expert should say it’s like pooh. This is really crazy, but that’s the level that we have now. When you start talking about gold people pigeon hold you. They say “You must be a gold bug” which is a derogatory statement.

Anyway, as far as the guys who run the mines are concerned they’re interested in salaries. They get good salaries. Like I say, very few of them have any skin in the game and that’s it. They don’t know the vocabulary, they don’t know what you’re talking about, they defer to the World Gold Council which is basically the world jewelry council. That’s been a thorn in my side the whole time I’m at this.

Mike Gleason: Yeah that’s I think the conclusion we’ve drawn as well. There’s no great explanation as to why these guys are just sort of completely AWOL when it comes to the suppression schemes. We have had (on our podcast) Keith Neumeyer CEO of First Majestic Silver who is a very outspoken individual when it comes to the manipulation. At least there are some out there that are doing that.

Well Larry, as we begin to close here tell folks how they can get involved or perhaps how they can partner with you in your efforts to help advance sound money policy, other than making a fully tax deductible donation to FAME… which can be done at FAME.org… talk about what people might do to join in the fight to help restore fiscal responsibility and sound money to our nations monetary policy.

Larry Parks: Well the first thing is they’re going to have to invest some of their most valuable resource and that’s their time to learn about this. We have on our website, especially the issues summary. It’s simple to do, there’s a lot of cognitive dissonance here. But we could use introductions, especially introductions to trustees of pension funds. And one of the big opportunities I think to get interest in gold we need to build a constituency for gold in the United States and there is no such constituency today. I think in December it’s a proxy for this, the mint sold something like three thousand gold eagles. That’s nothing. That’s like a tenth of a ton.

To put that into perspective for you, the mines produce about three thousand tons a year and there’s roughly two hundred thousand tons above ground. A tenth of a ton is nothing. You know because you’re in the business people keep denigrating gold. So really the opportunity to build a constituency is to get gold into pension funds.

I know you know about this Mike, I don’t know if your listeners know about it but we just had three bills that went down in flames in Wyoming. Which were going to compel the state of Wyoming… we had about seventeen representatives out of sixty vote in favor of it. But all of these pension funds are naked. And if these pension funds at least had some gold people would start taking an interest in what’s happened here. And what’s happened will not stand the light of day. Like I said this is just out and out thievery, stealing from ordinary people their future payments. It’s not like they come to your house and take what you have, but really we’re on a glide path to Venezuela as I’ve said.

We could use introductions. If the people can’t make a donation refer us to a trustee of a pension fund, any kind of pension fund. And I’m particularly interested in people who run pension funds for organized labor. The reason for that is that organized labor, they employ lobbyists and they have pull. They’re the principle victims so they’re the ones who could really make a difference here.

Mike Gleason: Well, it’s certainly been a great honor to speak with you and we greatly enjoyed the conversation. Keep up the great work. You guys are doing fantastic work there. People should go to FAME.org and make a contribution. You’ve just heard from Larry and how he has dedicated a lot of his life to this effort and it’s a very noble one. We certainly appreciate you coming on the Money Metals Podcast, take care Larry.

Larry Parks: A real pleasure, thank you Mike.

Mike Gleason: Well that will do it for this week, thanks again to Larry Parks of the Foundation of the Advancement of Monetary Education for more information visit the website FAME.org and please consider making a contribution to this important and vital cause. Again, you can do that and find out plenty of other information on these topics as well at FAME.org.

And check back here next Friday for our next Weekly Market Wrap Podcast. Until then this has been Mike Gleason with Money Metals Exchange, thanks for listening, and have a great weekend everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

We are now entering the final part of the endgame of the latest fiat experiment and the actions of the Fed and other central banks virtually guarantee that most currencies, including and especially the dollar, will end up totally worthless, just like in the Weimar Republic in Germany in 1923. Needless to say, in such an environment, anything that has real value like gold and silver, will soar in price, and even make intrinsic gains as everyone eventually tries to get aboard the lifeboat.

Massive deflationary forces are already ravaging the economy, with the virus scare acting as a catalyst, and already millions have already lost their jobs and millions more will as the economy comes to a screeching halt. In the face of this the Fed and other central banks have mobilized to try to head off complete collapse and an implosion of the debt markets leading to an interest rate spike, and also to protect and advance the interests of the super wealthy still further. The Fed’s balance sheet is expanding like a supernova that is starting to explode and it is set to expand at an even more rapid rate, made necessary by a severe decline in productivity and serious disruption of global supply chains. The reason that the virus was dispersed when it was is that governments feared that collapsing economies and widespread unemployment and poverty would lead to revolution, so they needed a way to keep the population under tight control, hence the lockdowns as unemployment in the U.S. and elsewhere skyrockets with the virus as an excuse.

All of this means that both gold and silver are set to soar. As pointed out repeatedly by Egon Von Greyerz, it is not so much that gold and silver are gaining in value, but that currencies are losing value due to them growing in quantity exponentially. Gold and silver, whose value is intrinsic and cannot be destroyed, are simply moving to reflect the destruction in the purchasing power of fiat.

The “writing on the wall” was and is the yawning gap between the price of paper and the price of physical gold and silver. Recently it became huge, and given what is going on this gap was certainly not going to be closed by the price of physical gold and silver droppinginstead it would be closed by the price of paper gold and silver taking off higher, and that is what we have been seeing in recent weeks, as the biggest bull market in the Precious Metals sector in history by far gets started. Already, gold has broken out to new highs against most currencies and it is likely to do so before much longer against the dollar, even if a pullback occurs first.

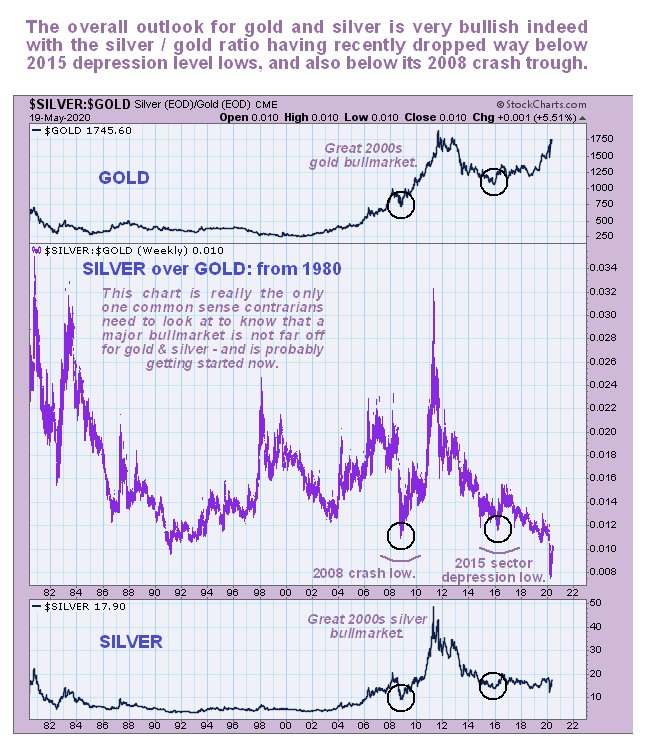

Another factor that we have for a long time now taken as a strong indication of an incubating bull market is the silver-gold ratio which recently reached an incredible low extreme as we can see on its long-term chart going back to 1980 below. Most low extremes on this indicator have coincided with sector bottoms, the most notable examples being at the 2008 crash low and 20152016 sector depression low, which were followed by major sector uptrends. Recently this ratio fell to a freak low which was a sure sign that the sector had hit bottom. Now it is recovering as silver at last starts to join the party. Gold has been rising for some time and is now starting to challenge its dollar highs and it has opened up a huge divergence with silver that will be resolved by a roaring bull market in silver.

Now we will turn to the most interesting very long-term chart for silver, which also goes back to 1980 to allow direct comparison with the silver to gold ratio chart above. The first point to note is that the big rally during the 1st half of 2016 stalled out almost exactly at the resistance at the 2008 highs. But by far the most important point to observe is that the unprecedented massive bull market that is now incubating HAS NOT EVEN OFFICIALLY STARTED YET, AND WON’T UNTIL SILVER BREAKS ABOVE THE KEY RESISTANCE SHOWN ON THE CHART APPROACHING $21. Until that happens reactions are possible, but once this breakout occurs the entire sector is likely to go ballistic.

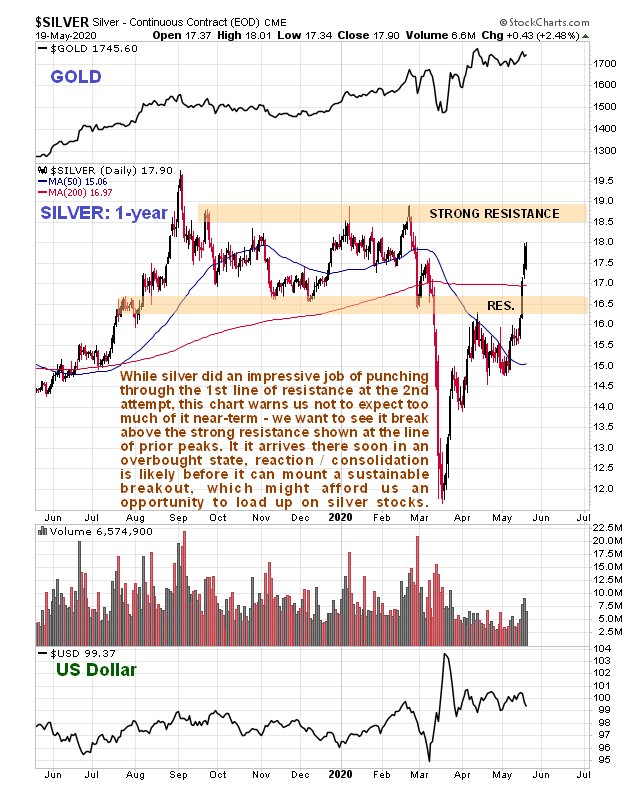

Now we will turn to the 1-year chart for silver to get a feel for what is going on right now. Whilst annotating this chart, I realized that we probably don’t need to panic about getting the silver stocks on board, because the really big action in most of them won’t start until the silver price breaks above the resistance approaching $21 that we looked at on the long-term chart, and on this chart we can see that it first has to contend with a quite strong zone of resistance approaching a line of peaks near to $19. While the current sharp advance looks like it will soon bring it to this resistance, it will arrive there in a very overbought state, which makes it quite likely that it will pause to react/consolidate, and any minor weakness at that juncture would provide us with an opportunity to load up the silver stocks on our list at somewhat better prices.

Originally posted on CliveMaund.com at 8.55 am EDT on 20th May 2020.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.