Argentina is the 4th largest producer and exporter of corn in the world. Paraguay grows not much corn, but it takes the 11th place in its exports to the world. The US Department of Agriculture (USDA) reported that US corn exports totaled 477 million bushels over the past week. This is 1.2 million bushels more than a week earlier and 14 million bushels more than the same week last year. Japan purchased 39% of US corn exports last week. Other major buyers were Mexico, South Korea and Colombia. Note that according to the CFTC, the volume of net short positions for corn has peaked since April 2019. This happened because at the end of April this year, corn quotes fell to a minimum since 2009. Now they are trying to correct upward. If market players have to close short positions, this could trigger a speculative price increase.

GBPUSD is trading around its highest levels in a month, having briefly breached the 1.25 psychological level.

Sterling, along with the rest of its G10 peers, has been able to take advantage of the waning US Dollar at the onset of June as they try to pare back their year-to-date losses. Even with its recent rally, the Pound remains over 5.8 percent weaker against the Greenback compared to the start of the year.

UK and EU negotiators are resuming talks today to try and reach a post-Brexit trade deal. If both London and Brussels fail to come to an agreement, at least to extend the transition period beyond 2020, then such a scenario raises the prospects of a hard-Brexit at the onset of the new year. Hence, any development surrounding these June talks could trigger bouts of volatility in Sterling.

The Pound’s outlook remains bearish overall, considering the possibility that the Bank of England could adopt negative interest rates, potentially by February 2021. A no-deal Brexit, coupled with negative UK interest rates, could see GBPUSD plummeting.

For the time being, traders are looking past such concerns and focusing instead on the UK economy’s post-pandemic recovery. The government is set to announce an economic stimulus package next month, which is expected to help mitigate the economic damage from the coronavirus outbreak. Such optimism is curbing the pessimism surrounding Sterling, with Pound-Dollar one-month 25 Delta risk reversals showing that traders have grown less bearish on GBPUSD since March.

From a technical perspective, GBPUSD appears to have more room to run to the upside, with the currency pair yet to venture into ‘overbought’ territory, judging by the 14-day relative strength index. Sterling’s next advance against the Greenback may be capped below the 1.265 line, as was the case on two separate attempts in April. It remains to be seen whether GBPUSD has enough momentum to actually breach that 1.265 resistance level over the short-term, although I’m fairly certain the Dollar will have a major say about that.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The U.S. faces the prospect of a Japan-like deflation.

Let’s begin with a brief review of Japan.

Here’s a chart and commentary from the 2020 edition of Robert Prechter’s Conquer the Crash:

Japan had one of the strongest economies in the entire world, growing at a 9% rate for 20 years up to 1973, and then a pretty strong rate of about 4.5% through 1994. From there, it’;s averaged about 1%. …

Economic growth in the United States today is weaker than Japan’s was in 1989 when its bull market ended. The U.S. economy is dramatically weak relative to the amount of central-bank inflating.

Speaking of the U.S., here’s a May 18 headline and sub-headline from Bloomberg:

America Is Becoming Japan, Not in a Good Way

The country could be on the brink of its own deflationary era.

Bloomberg referred to this prospect as the “Japanification” of the U.S.

But, getting back to that phrase “deflationary era” – what would that look like? What is deflation?

Well, many people erroneously believe that deflation simply means “falling prices.” Yet, it goes well beyond that.

Let’s return to the 2020 edition of Conquer the Crash for a fuller explanation:

A deflationary crash is characterized in part by a persistent, sustained, deep, general decline in people’s desire and ability to lend and borrow. A depression is characterized in part by a persistent, sustained, deep, general decline in production. … Because both credit and production support prices for financial assets, their prices fall in a deflationary depression. As asset prices fall, people lose wealth, which reduces their ability to offer credit, service debt and support production.

Well, the U.S. has already experienced falling asset prices. Consider oil and other commodities, as well as the stock market – which, despite the recent rally, is still well off the highs.

Plus, and most importantly, there’s been a credit market contraction and slackening production.

In April, manufacturing output declined 6.3%, according to the Federal Reserve. Moreover, industrial production dropped 5.4% and Q1 GDP fell 4.6%. The Q2 GDP number could show a much bigger drop. Current estimates range from a decline of 25% to 40%.

Also in April, the Credit Managers’ Index from the National Association of Credit Management slid 8.3 points. That’s after a drop of 7.2 in March.

Other deflationary pressures are also in place. As examples, producer prices have been sluggish, and according to the Atlanta Fed’s U.S. wage growth tracker, wage growth peaked at 3.9% in July 2019 and fell to 3.3% in April 2020.

There’s only been two major deflationary depressions in U.S. history. The first one extended from 1835 to 1843. The second one – known as “The Great Depression” – followed the 1929 stock market crash and stretched into 1933.

As you may know, other nations also suffered through the Great Depression.

Is another deflationary depression on our doorstep?

Get a 2020 Foresight and learn about 5 Market Trends 99% of Investors Will Miss, which is a 1-week, 5-insight series pulled directly from our flagship Financial Forecast Service.

It’s premium, subscriber-level content — 100% free to you when you join Club EWI. Membership is also free.

You get our latest forecasts for U.S. stocks, the economy, gold and more.

This article was syndicated by Elliott Wave International and was originally published under the headline Deflation: Why the “Japanification” of the U.S. Looms Largey. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

Global markets are mixed today as President Trump said he was “dispatching thousands and thousands of heavily armed soldiers” to US cities facing protests that erupted after the death of a black man in police custody “if a city or state refuses to take the actions necessary to defend the life and property of their residents.” Global equities advanced yesterday buoyed by moderate US response – just threats and no tariffs – to China’s move to adopt new law restricting Hong Kong’s self-government.

Forex news

Currency Pair

Change

EUR USD

+0.02%

GBP USD

+1.76%

USD JPY

-0.12%

The Dollar weakening has halted today . The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, lost 0.5% Monday despite the Institute for Supply Management report which showed its manufacturing index rose to 43.1 in May from an 11-year low of 41.5 in April . Both GBP/USD and EUR/USD accelerated climbing Monday as Markit’s Manufacturing Purchasing Managers’ Index (PMI) for the euro zone rose to 39.4 in May from 33.4 in previous month. Pound is higher currently against the dollar while euro is down. USD/JPY reversed its climb yesterday while AUD/USD continued rising with the dynamics reversed for both pairs currently.

Stock Market news

Indices

Change

Dow Jones Index

+0.51%

Nikkei Index

+1.33%

Hang Seng Index

+0.49%

Australian Stock Index

+0.52%

Futures on three main US stock indexes are mixed currently. Stock indexes in US ended higher Monday supported by data showing manufacturing sector contraction slowed in May: the three main US stock indexes posted gains ranging from 0.4% to 0.7%. President Trump told US governors to get tougher on protesters amid outrage sparked by the death of a black man while he was in police custody. European stock indexes are rising currently after a rebound on Monday led by travel and leisure shares. Asian indexes are higher currently led by Nikkei . Chinese stocks are rising amid reports China’s government ordered to halt US soybean purchases.

Commodity Market news

Commodities

Change

Brent Crude Oil

+0.47%

WTI Crude

+0.26%

Brent is extending gains today. Oil prices ended higher on Monday against the background of report Russia and members of the Organization of the Petroleum Exporting Countries and allies, a group known as OPEC+, were considering an agreement to extend current output cuts by one or two months. The US oil benchmark West Texas Intermediate (WTI) lost 0.1% Monday. August Brent crude climbed 1.3% to $35.44 a barrel on Monday in thin trading due to market holidays for Germany, Switzerland, Denmark and Norway .

Gold Market News

Metals

Change

Gold

-0.03%

Gold prices are extending losses today. August gold lost 0.1% to $1750.30 an ounce on Monday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Liberia’s central bank lowered its monetary policy rate by 500 basis points to 25.00 percent, saying this rate cut was indicative of its success in reducing inflation to an average of less than 25 percent in the first quarter of this year from slightly over 30 percent in October 2019. It is the first rate cut by the Central Bank of Liberia (CBL) since it set the standing deposit facility rate (SDF) at 30 percent on Nov. 30, 2019 after transitioning to an interest rate-based monetary policy framework from exchange rate targeting in July 2019. In a statement issued May 29 following a meeting of the bank’s board of governors on May 28, the bank’s board of governors also decided to continue issuing shorter tenor instruments of 2 weeks, 1 and 3 months, at an interest rate of 25 percent. Liberia’s economy, which contracted 2.5 percent in 2019 due to an underperformance of non-mining sectors, is expected to be weighed down further by the COVID-19 pandemic while inflation is seen falling further to 19 percent in the second quarter of this year. In November, 209, when CBL tightened its monetary policy and set the key rate at 30 percent, it also lowered the Liberian dollar reserve requirement to 15 percent from 25 percent and raised the U.S. dollar requirement to 15 percent from 10 percent. The Liberian dollar is currently trading at 198.6 to the U.S. dollar, down 5.4 percent this year. CBL switched to an interest rate policy framework from an exchange rate targeting framework at a time of low inflow of foreign exchange. An exchange rate framework requires major holdings of foreign exchange that can be used to defend the exchange rate. Under the new monetary policy framework, CBL will use medium-term interest rates to transmit monetary policy decisions to control inflation and bring down the high prices of goods and services, especially food, which significantly affects poor people, something CBL in November said it was not happy with. CBL also said then the success of the new framework will require the development of financial markets that are currently at a low level. In November last year Liberia’s president, George Weah, named J. Aloysius Tarlue executive governor of CBL after Nathanial Patray retired as executive governor in October that year after he initiated several major reforms, including the development of the new monetary policy framework, strengthening the foreign exchange auction system and developing a financial inclusion strategy. Tarlue was tasked with restructuring the central bank to tackle the country’s economy as it relates to price, exchange rate and financial stability. The policy framework adopted in July will help prepare CBL to move toward inflation targeting, a policy that would be consistent with the convergency criteria of the monetary union of the Economic Community of West African States (ECOWAS). ECOWAS is a regional political and economic union of 15 west African countries and includes the West African Economic and Monetary Union (WAMU), which use the CFA franc that is pegged to the euro. Last year ECOWAS agreed to rename the CFA franc the eco and eight of these countries, mostly former French colonies and grouped in Wamu, plan to adopt the eco as a single currency under the auspices of the Central Bank of West African States (BCEAO).

– Every election year over the past five US Presidential election cycles has presented a unique set of price rotation events. Particularly evident in strongly contested US Presidential candidate battles where the voters are consumed with pre-election rhetoric. The 2007-08 election cycle was, in our opinion, very similar to the current market cycle in terms of consumer sentiment and economic function. The 2015-16 election cycle was less similar – yet still important for our researchers.

The economic conditions of the US economy and the global economy were vastly different prior to each US Presidential election cycle and continue to evolve throughout the current 2020 election cycle. Yet, our researchers believe the correlation of price volatility and rotation combined with the distraction for consumers as the election process occupies the hearts and minds of almost everyone across the globe takes a toll on the markets. Prior to almost any US Presidential, price volatility and trends tend to become much more exaggerated and extended.

We’ve published research articles about this technical setup/pattern that occurs in the markets nearly 8 to 15+ months before the US Presidential election cycle before. The basic theory of the setup/pattern is as follows…

_ 12+ months prior to the election date, the parties consolidate around specific candidates where the first battles of the US presidential election cycle conclude.

_ Over the next 12 months, the battle between the selected candidates becomes more heated and aggressive as voters are pushed information and disinformation related to their decisions.

_ The process of the election and the decision-making process for consumers/voters is very stressful and distracts from the normal economic activity for many. This distraction translates into an indecisive market where future expectations (optimism and pessimism) greatly depend on the outcome of the election. Thus, the markets are stuck in a “no man’s land” type of “stasis” waiting for the election event to conclude.

Depending on the events that lead up to the election date, the stock market could be biased towards a bullish trend or a bearish trend which can have a big impact on the pre and post-election outcomes.

S&P 500 Index 2006-09 US Presidential Election Cycle

Lets start by taking a look at the 2006-09 (2008 US election cycle) data/chart. First, we can see the price trend in 2006-07 was moderately bullish within the early election cycle. The first real signs of a crisis in the markets took place in mid-2007 where a deep low price move setup a double-bottom. Near the end of 2007 and into very early 2008, the stock market collapsed below those lows and never really recovered. The real collapse in price began in June 2008 – after a moderate price recovery from the new lows. Price continued to collapse more aggressively just prior to the election date and even after the election was completed.

Yes, we know this collapse was related to the 2008-09 Housing/Credit market crisis and was not related to the directly related to the Presidential election event. Yet, we, as technicians, believe price translates all external factors into a form that we can use to derive future information from. The point we want to try to make is that election cycle years tend to be much more volatile and aggressive.

The pre-election price declines appear to set up a bottom or double-bottom price level 12 to 15+ months prior to the election date. After that completes, the markets may attempt to rally above previous highs at some point, but will likely attempt to retest recent lows 4 to 12 months prior to the election date. As voters/consumers’ attention is consumed by the election process, news and rhetoric, consumers change their habits and become more protective of their assets and future expenses.

The one thing to consider when reviewing this chart is that the uncertainty and indecision in the markets related to the Presidential election cycle were compounded by the collapse of the housing, financial, and credit markets. This event created additional price and economic concerns fairly early in 2008. Additionally, pay attention to the June 2008 change in price trend that sets up a deeper downside price collapse.

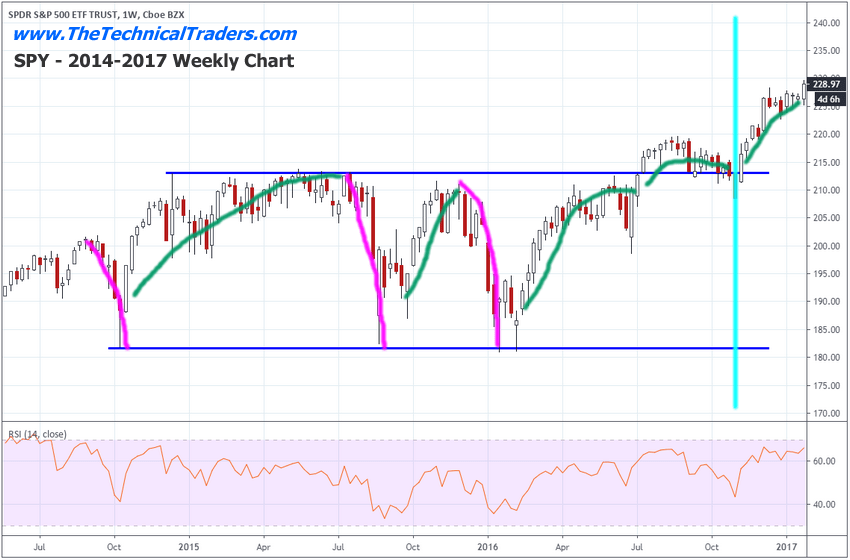

S&P 500 Index 2014-2017 US Presidential Election Cycle

This next chart is the 2014-2017 US Presidential Election cycle and this chart highlights a very different time in US history. There was no massive housing/credit crisis event. There was no massive implosion of the US or global markets taking place throughout this time. There was only a heated battle between two candidates. The chart shows how 2015, nearly 12 months prior to the election date, the market price collapsed twice to complete a double-bottom pattern. This pattern seems to set up prior to election cycles with fairly high consistency.

As we progress to the 12 month period just before the election date (highlighted in CYAN), we can see the 2016 election year resulted in a moderate upside price bias after establishing a bottom very early in 2016. Still, there was a decent amount of volatility throughout the year – particularly in June and the 60 days prior to the actual election date.

Remember, other than political drama, this election cycle didn’t include any massive economic crisis events which could have altered the direction of the markets closer to the election date. The deeper double-bottoms set up the price range headed into the election date and the lack of surprise/crisis events prompted a moderate upside price bias leading into the election event.

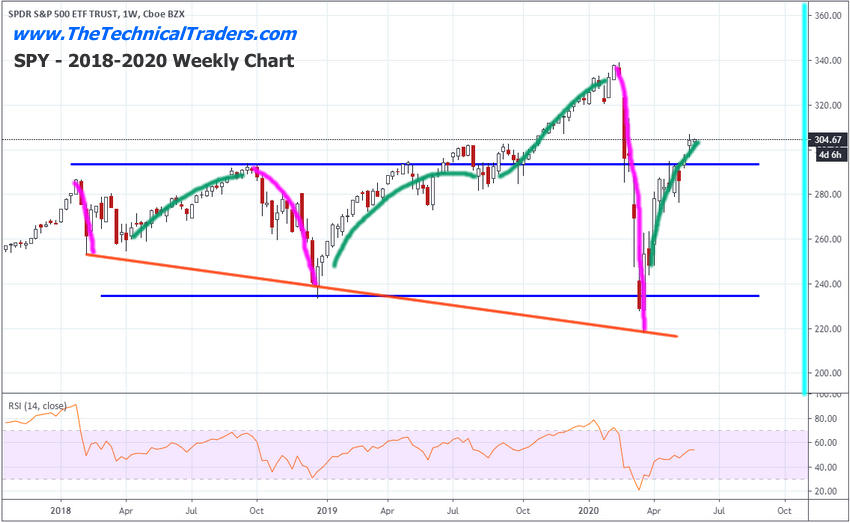

S&P 500 Current 2017-2020 Presidential Election Cycle

Now, we take a look at the current 2017-2020 setup. This time, because of the prior extended rally in the markets from 2017, we’ve seen a series of deeper price lows setups into an expanding bottom/downward sloping price trend. This is somewhat unusual and suggests volatility is excessive at this time in the markets. We’ve also experienced the COVID-19 virus event occur, which is acting like the 2008 housing/financial crisis event.

At this point, heading into early June 2020 and understanding that these Presidential election cycle events typically result in much greater volatility as we get closer to the election date, our research team believes the June through August period could prompt a broad market downside retracement which coincides with Q2 data/expectations. The month of June prior to the election date (Q2) appears to be a very instrumental period for the markets.

The downward sloping lows on this chart suggest a deeper price rotation may occur as the markets move closer to the election date and continue to process the technical and economic data. The uncertainty related to Presidential election cycles is still at play in the markets. Should some type of crisis event unfold in the midst of the final 5 to 6 months prior to the election date, the risk of a downside price event would become much more excessive.

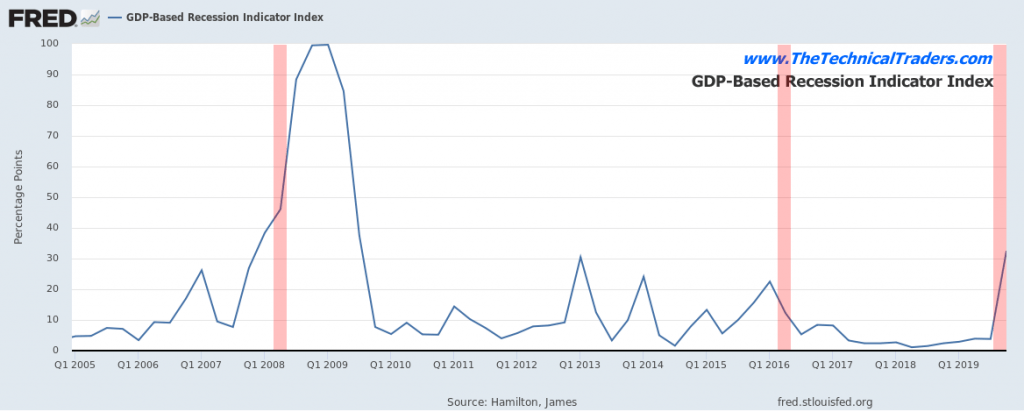

GDP Based Recession Indicator

Currently, the COVID-19 virus event has set up a critical price event headed into the 2020 Presidential election cycle which is somewhat similar to the 2008 election cycle. Pay attention to the GDP Based Recession Indicator chart below. Notice how the 2008 election cycle correlated with a massive increase in the GDP Based Recession Indicator? Now, see how the current GDP Based Recession Indicator has already begun to spike upward? Unlike what happened in 2016 where the GDP Based Recession Indicator stayed below 30, the current level of this indicator suggests a crisis event is beginning to unfold in 2020.

If this crisis event continues, the process where the price will attempt to properly identify risks and valuation levels will likely take place over the next 8 to 12+ months – which is very similar to what happened in 2008 and 2009. Our researchers believe June 2020 could become a critical month for price activity where the future price trends are established.

Concluding Thoughts:

Currently, we are urging our friends and followers to stay overly cautious of this upward price trend in the US stock markets. Even though we have seen the NQ and other sectors rally to near all-time highs, we believe the markets are still excessively volatile and the indecision leading up to a Presidential election cycle could prompt some really big price moves in the future. We are still trading the long side of the market and advising our clients to take very low-risk trades which have been properly sized. This is a traders market where skilled technical traders can find incredible gains.

June through August will likely become critical in regards to the future price trends and will likely determine if the markets continue to push higher or rotate downward as concerns and potential crisis events continue to unfold. Historically, June through August prior to a Presidential election cycle are very important measures of what happens near and after the election event.

I hope you found this informative, and if you would like to get a pre-market video every day before the opening bell, along with my trade alerts. These simple to follow ETF swing trades have our trading accounts sitting at new high water marks yet again this week, not many traders can say that this year. Visit my Active ETF Trading Newsletter.

If you have any type of retirement account and are looking for signals when to own equities, bonds, or cash, be sure to become a member of my Long-Term Investing Signals which we issued a new signal for subscribers.

Ride my coattails as I navigate these financial markets and build wealth while others lose nearly everything they own during the next financial crisis.

Investors have marched into June with a renewed appetite for risk after President Donald Trump’s response to China’s new law reining in Hong Kong was not as bad as initially feared.

It looks like market players are dumping in favour of riskier currencies amid the growing optimism and this continues to be reflected across the G10 space. With the mighty Dollar entering the new trading month clearly on the wrong side of the bed, could weakness be a dominant theme over the next few weeks?

The Dollar Index (DXY) daily chart is certainly worth one thousand words. Prices are under pressure with bearish investors eyeing the 97.80 level. A solid daily close below this point may encourage a decline towards 96.25.

AUDUSD explodes higher with 0.6850 in sight

The Australian Dollar took advantage of a weaker Dollar on Monday as prices rallied towards 0.6800.

A weaker Greenback should inject Aussie bulls with enough inspiration to break above 0.6800 with 0.6850 acting as the next key level of interest. If rally runs out of steam and prices sink back under 0.6700, then the AUDUSD may retrace back towards 0.6550.

USDJPY remains rangebound

Prices are trading near the 108.00 resistance level and could sink back towards 107.00 if the Dollar continues to weaken. A breakdown below 107.00 may trigger a drop towards 105.90.

USDCAD tumbles below 1.3680

Talk about a way to start the final trading month of Q2.

The USDCAD has tumbled almost 200 pips today and could sink lower thanks to a severely depressed Dollar. Should the Canadian Dollar appreciate on rising Oil prices, the USDCAD may sink lower towards 1.3500.

GBPUSD to break above 1.2500?

Who would have thought the GBPUSD would jump towards 1.2500 as Brexit talks official resume on Tuesday?

While the currency pair could push higher on Dollar weakness, the upside may be limited by uncertainty and fears over the UK economy.

A solid breakout above 1.2500 could trigger a move back towards 1.2650. Should 1.2500 prove to be a reliable resistance, prices may decline back towards 1.2350.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

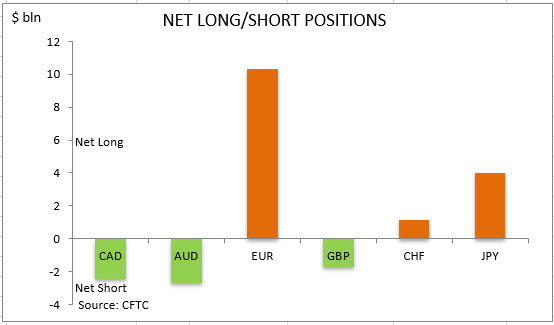

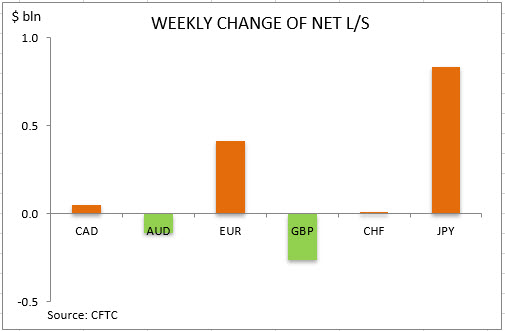

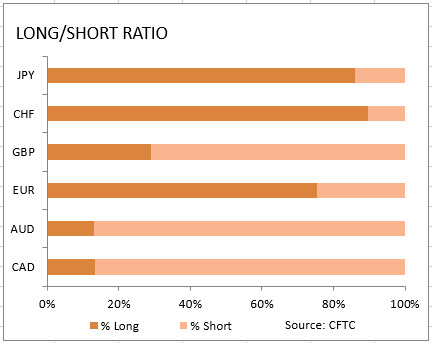

US dollar bearish bets increased to $8.60 billion from $7.67 against the major currencies during the one week period, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to May 26 and released on Friday May 29. The change in overall dollar position was mainly due to significant decrease in bearish bets on Canadian dollar, and increase in bullish bets on Japanese yen and euro as the Japanese government announced it was considering a fresh stimulus package worth over $929 billion while data showed euro-zone’s economic activity contracted less drastically in May. The Pound, Canadian and Australian dollars maintained net short positions against the dollar. The bearish dollar bets rose as minutes of the Fed’s April policy meeting showed officials discussed how to convince markets that interest rates will stay low for a long time. Bearish bets on dollar increased as US Labor department report showed nearly 40 million Americans lost their jobs in the previous nine weeks.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

UK manufacturing PMI for May was revised upward: manufacturing PMI for May was revised up from preliminary reading of 40.6 to 40.7. This is bullish for GBPUSD.

The European Commission also reduced the forecast for wheat exports to 26.5 million tons from 28 million tons. In the World Agricultural Supply and Demand Estimates report for May, the US Department of Agriculture (USDA) wrote that wheat production in the European Union would reach 143 million tons in the 2020/21 season and 28 million tons in exports. As we can see, the expectations of the European Commission are much more frugal now. Note that the forecast for world wheat production this season by the International Grain Council is 766 million tons, which is 2 million tons less than the similar forecast of the USDA. All this can support wheat quotes.