As it now is clearly holding above 1,700 USD, the outlook for Gold is strongly bullish. Nevertheless, bulls are now obligated to “deliver” if they want to avoid a deeper short-term correction.

“Deliver” in this context means nothing more than: “push the precious metal above 1,770 USD to new yearly highs”. If they fail to do so, the still given bearish divergence in the RSI(14) on a daily time-frame could play out and result in a test of the short-term trend-support around 1,660 USD.

Nevertheless, mid-term our take for the yellow metal stays clearly bullish and we expect rather than later a stint to the all-time high around 1,920 USD.

One potential driver for such a move could be a sustainable drop in 10-year US Treasury yields below 0.60% which seems, in our opinion, only a question of time.

One trigger could be today’s release of the ADP employment report. While private businesses in the US fired 20.2 million workers in April, today’s numbers are expected only at 9 million lost jobs for May.

Still, any print which comes in worse than the expectation and above 10 million could trigger a next wave of risk-off, bringing US yields under pressure again and driver the precious metal significantly higher with bringing 1,770 USD into our focus.

On the other hand, any positive surprise with a print of less than 9 million fired workers could push Gold again below 1,700 USD:

Source: Admiral Markets MT5 with MT5-SE Add-on Gold Daily chart (between March 4, 2019, to June 2, 2020). Accessed: June 2, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of Gold fell by 10.4%, in 2016, it increased by 8.1%, in 2017, it increased by 13.1%, in 2018, it fell by 1.6%, in 2019, it increased by 18.9%, meaning that after five years, it was up by 28%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks

The Dollar was trampled by most currencies on Wednesday as rising optimism around a quick economic recovery from the coronavirus pandemic boosted appetite for risk.

Safe-haven assets like the Japanese Yen and Gold fell out of favour while the Dollar Index (DXY) tumbled to its lowest level since early March below 97.40. As the market mood improves on recovery hopes, appetite for the Greenback may fall consequently dragging the DXY lower.

Focusing on the technicals, prices are under pressure on the daily charts as there have been consistently lower lows and lower highs. The Index is trading below the 20 Simple Moving Average while the Moving Average Convergence Divergence points to further downside. Sustained weakness below 97.80 may encourage a decline towards 96.25 and 95.00 in the medium to longer term.

Alternatively, a breakout back above 97.80 could trigger a rebound towards 98.50 and 99.00.

Euro rallies towards multi-month high

The Euro jumped to levels not seen in almost three months on hopes policymakers will offer a lifeline to the weakest economies in the Eurozone.

Expect the Euro to push higher in the short term, especially if the Dollar continues to weaken amid the risk-on mood. Looking at the charts, the EURUSD is bullish on the daily timeframe. The strong daily close above 1.1150 may open the doors towards 1.1280 and 1.1360, respectively.

Should prices sink back below 1.1150, the currency pair may target 1.1090.

GBPUSD breakout setup in play

A weakening Dollar has instilled Pound bulls with enough inspiration to break above 1.2500.

The question remains whether the upside momentum is strong enough for prices to break above the 1.2800 level.

Given how the Pound remains gripped by Brexit uncertainty and growth concerns, the fundamentals are not in favour of a stronger currency. However, a broadly weaker Dollar could create an opportunity for prices to push above 1.2800 and beyond.

Looking at the technical, the currency pair remains in a wide range on the daily charts. A strong daily close above 1.2650 may trigger a jump towards 1.2800. If this resistance level gives way, the next key point will be around 1.2900. On the other hand, a breakdown below 1.2500 could open a path back towards 1.2350.

EURJPY bulls are unstoppable….

The EURJPY has jumped over 250 pips since the start of this week thanks to an appreciating Euro and broadly weaker Japanese Yen.

Prices are heavily bullish on the daily charts with a solid breakout above 122.00 seen opening a path towards 122.90.

Commodity spotlight – Gold

As the market mood brightens on recovery hopes, buying sentiment towards safe-haven assets like Gold are set to fall. The precious metal could weaken towards $1680 if the $1710 level proves to be unreliable support. Alternatively, a rebound from $1710 is seen opening the doors back towards $1760.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Global downturn is easing as governments began to ease the tough coronavirus-led lockdown measures. While factory activity still contracted globally in May, contraction slowed as evidenced by purchasing managers indexes for Europe, US and China. Thus, Markit’s Manufacturing Purchasing Managers’ Index (PMI) for the euro zone rose to 39.4 in May from 33.4 in previous month. The US Institute for Supply Management report showed its manufacturing index rose to 43.1 in May from an 11-year low of 41.5 in April. China’s official manufacturing purchasing managers index and the private Caixin manufacturing purchasing managers index both showed factory activity still expanding in May. And China’s services sector returned to growth last month for the first time since January: the Caixin/Markit services Purchasing Managers’ Index (PMI) rose to 55.0 in May from 44.4 in April, hitting the highest level since late 2010. Readings above 50 indicate growth, below 50 indicate contraction. Improving economic data are bearish for gold prices.

Brent Oil has breached the psychologically important $40/bbl mark, and is trading at its highest levels in nearly three months. Brent’s current prices are another clear risk-on signal to the markets, with Asian equities climbing while regional currencies are advancing against the US Dollar today. US and European stock futures are also gaining at the time of writing.

OPEC+ is reportedly close to extending its current supply cuts programme by one month. Under the existing deal, which was sealed on April 12, the alliance of major Oil producers agreed to lower output according to the following schedule:

9.7 million barrels per day: May and June

7.6 million barrels per day: July through end-2020

5.6 million barrels per day: 2021 until April 2022

According to latest media reports, OPEC+ is now preparing to keep its output cuts of 9.7 million barrels until the end of July, before easing up.

Recall that even after the historic deal was announced over the Easter weekend, Brent continued to drop by over 30 percent through late April. This was because, despite the planned OPEC+ output cuts, global demand was seen flailing in the wake of the coronavirus crisis.

Since April 27, as more major economies have reopened, Brent has embarked on a stunning rally of about 76 percent. The proposed output cut extension is appearing to have the desired effect on Oil prices this time around because it comes at a time when worldwide demand for Oil appears to be recovering. US crude stockpiles are set to register four consecutive weeks of declines, pending confirmation later today by official US government data.

Even though $40/bbl Brent is a notable milestone amid the current market environment, it needs to climb another 50 percent before it can return to the $60 handle that we saw at the onset of 2020. Oil’s path for a sustained recovery may be threatened by a second wave of lockdowns or a return of US shale. The longer term outlook could remain dampened if international travel is disrupted for many years to come, as the world adjusts to the “new normal”. Even as Oil bulls enjoy their fortunes since end-April and risk appetite gathers momentum, the downside risks could yet pull the plug on the party.

With the expected OPEC+ output cut extension already mostly priced in, efforts to rebalance global Oil markets must endure and the global economy must show further signs of normalising before Oil prices can claim significantly more gains past $40.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

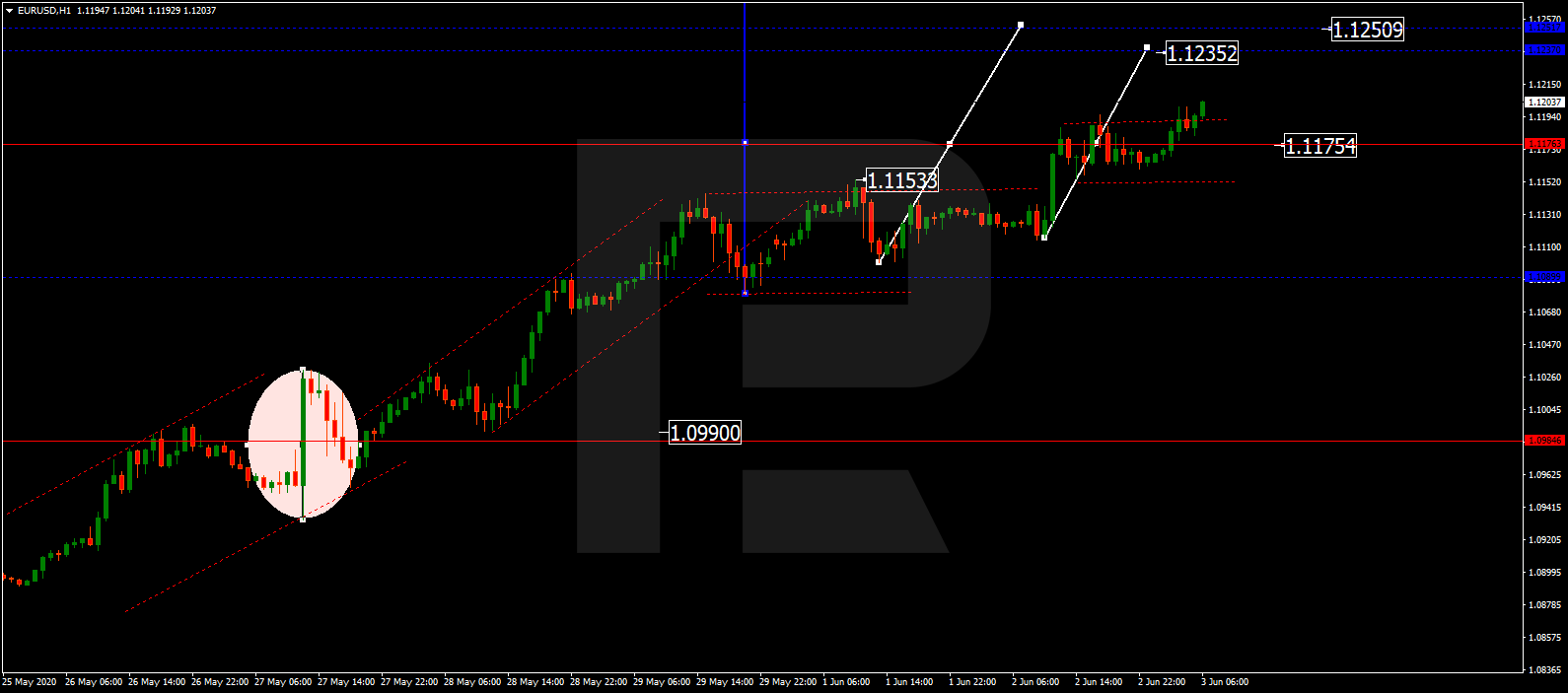

After breaking the consolidation range to the upside, EURUSD is expected to continue growing towards 1.1237 or even 1.1250. Today, the pair may reach the former level and then start a new correction towards 1.1175. Later, the market may resume trading upwards with the target at 1.1250.

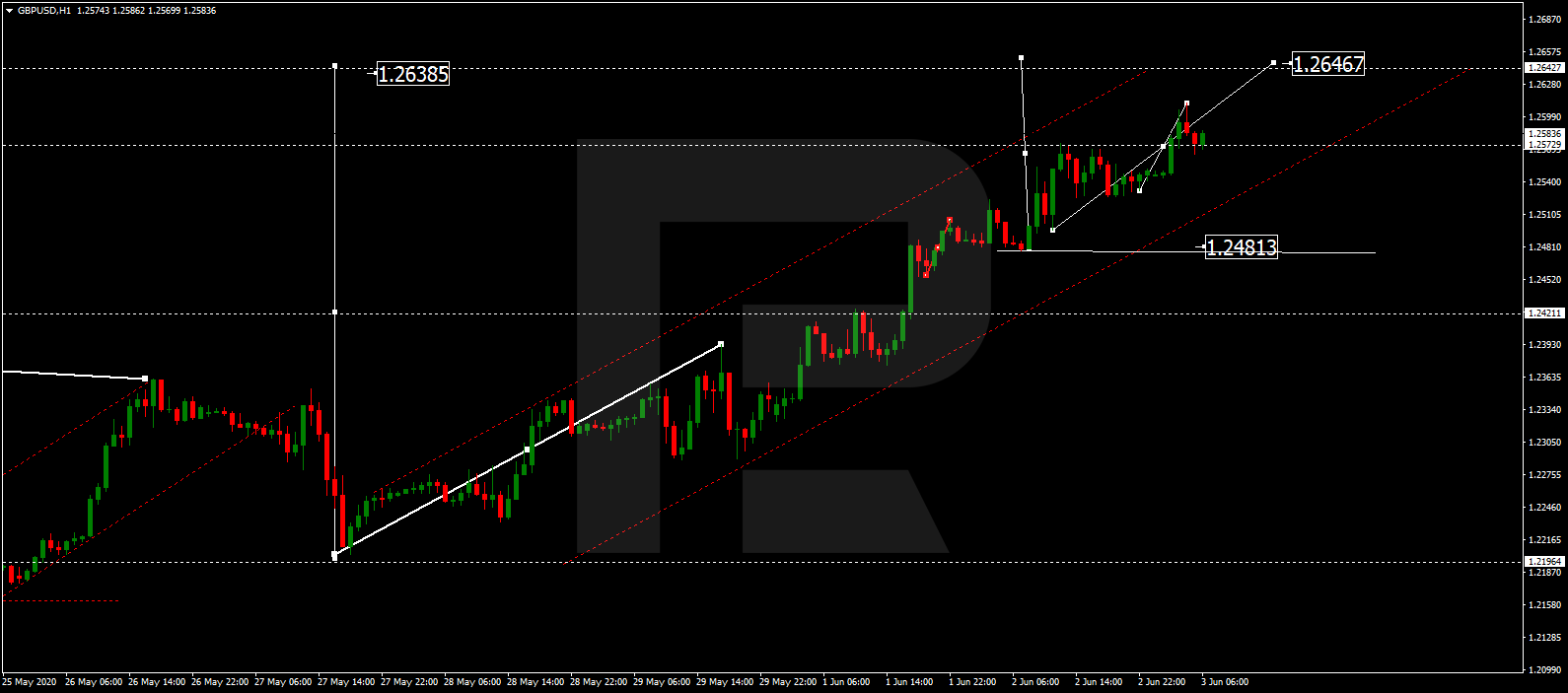

GBPUSD, “Great Britain Pound vs US Dollar”

GBPUSD is still trading upwards. Possibly, the pair may extend the current wave up to 1.2646. After that, the instrument may start a new decline with the target at 1.2481.

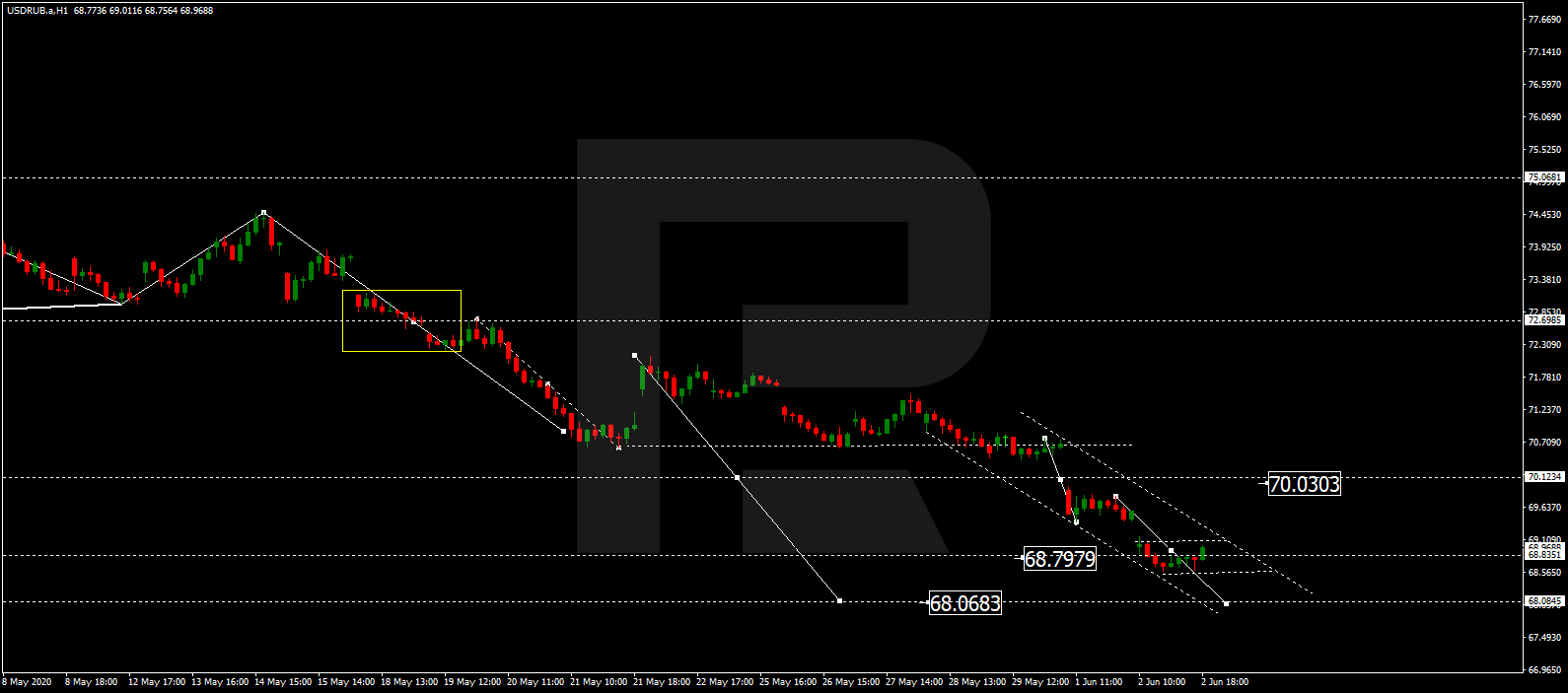

USDRUB, “US Dollar vs Russian Ruble”

After finishing the descending wave at 68.80, USDRUB is expected to consolidate around this level. Later, the market may break this range to the downside to reach 68.00 and then start another correction with the target at 70.70.

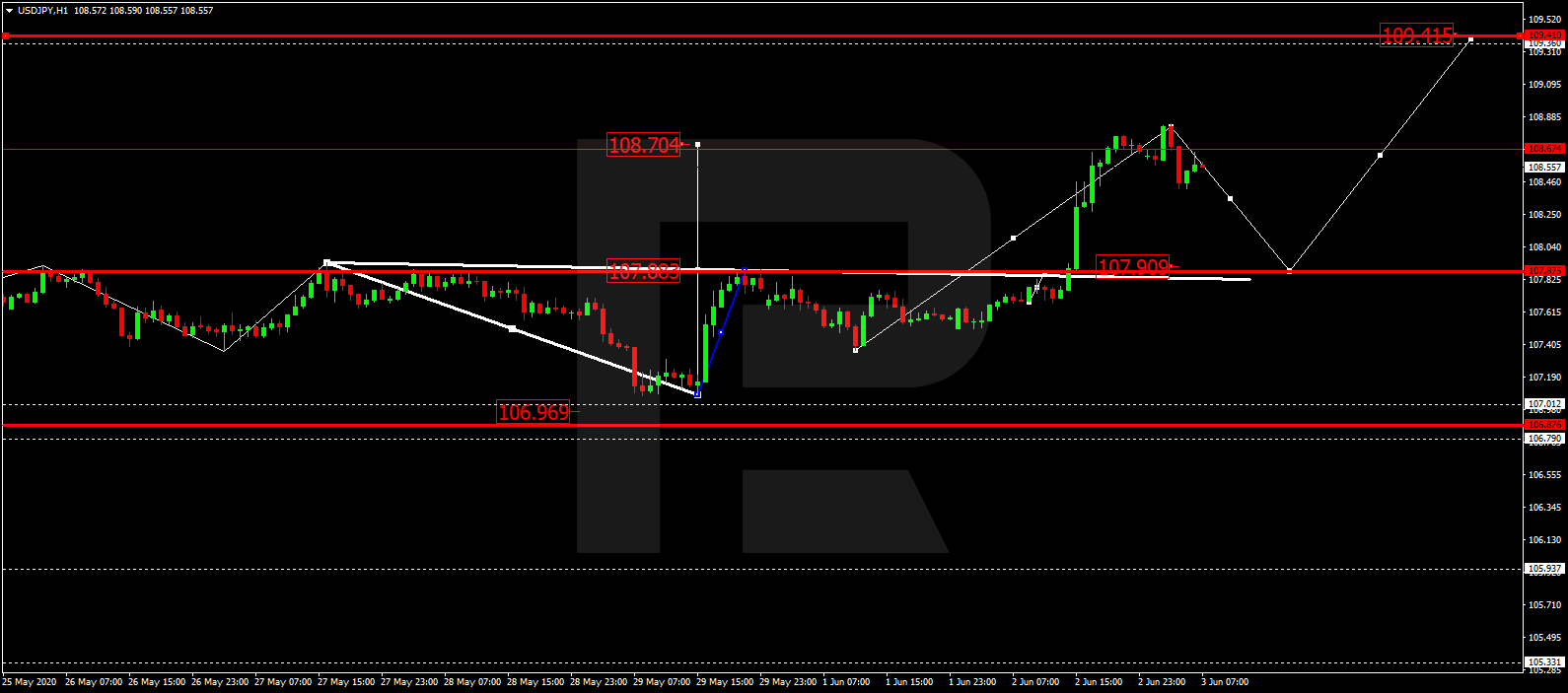

USDJPY, “US Dollar vs Japanese Yen”

After breaking 107.90to the upside, USDJPY has reached 108.70. Today, the pair may correct downwards to return to 107.90 and then form one more ascending structure with the target at 109.41.

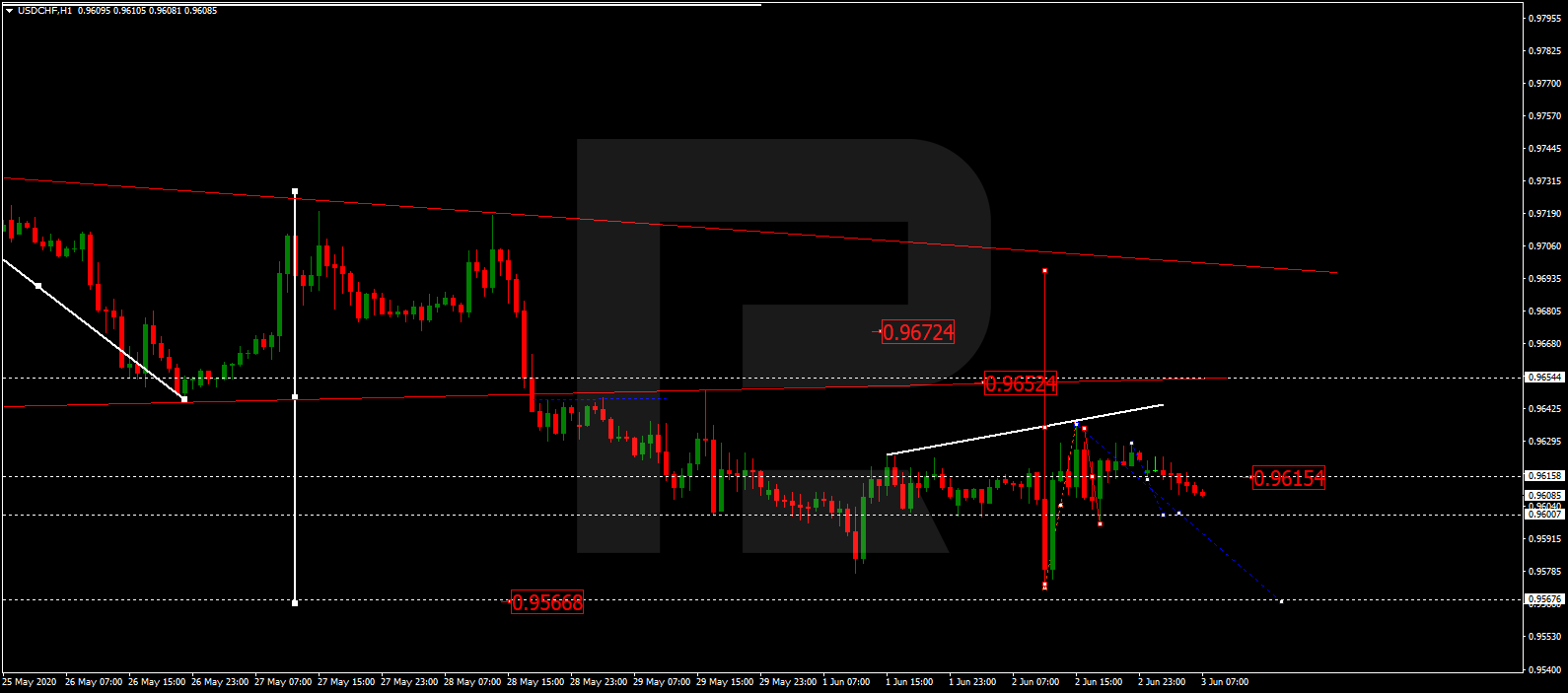

USDCHF, “US Dollar vs Swiss Franc”

USDCHF is still consolidating around 0.9616. If later the price breaks the range to the downside at 0.9600, the market may fall to reach 0.9550; if to the upside at 0.9630 – resume trading upwards with the target at 0.9690.

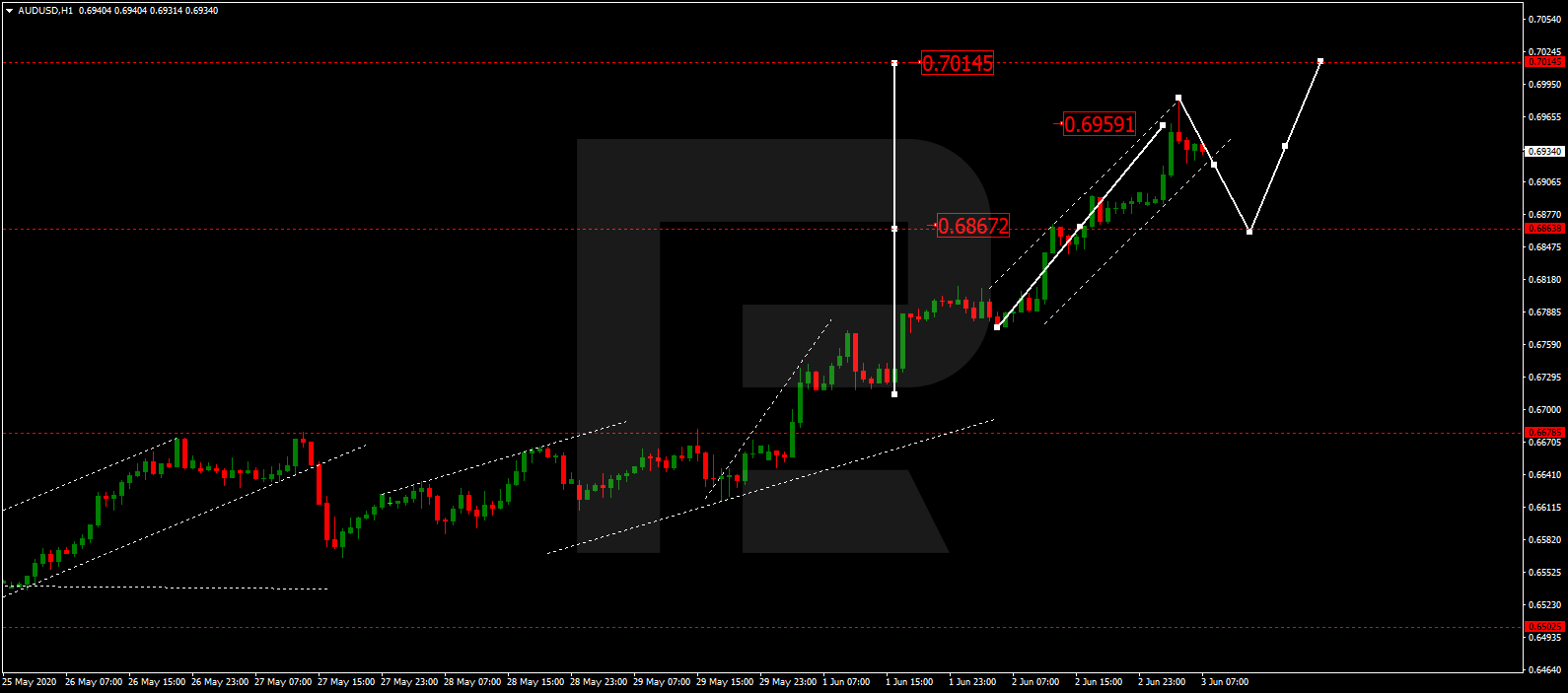

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD trading upwards; it has reached 0.6950 and right now is consolidating below this level. Possibly, the pair may break fall towards 0.6868 and then extend the ascending wave up to 0.7015.

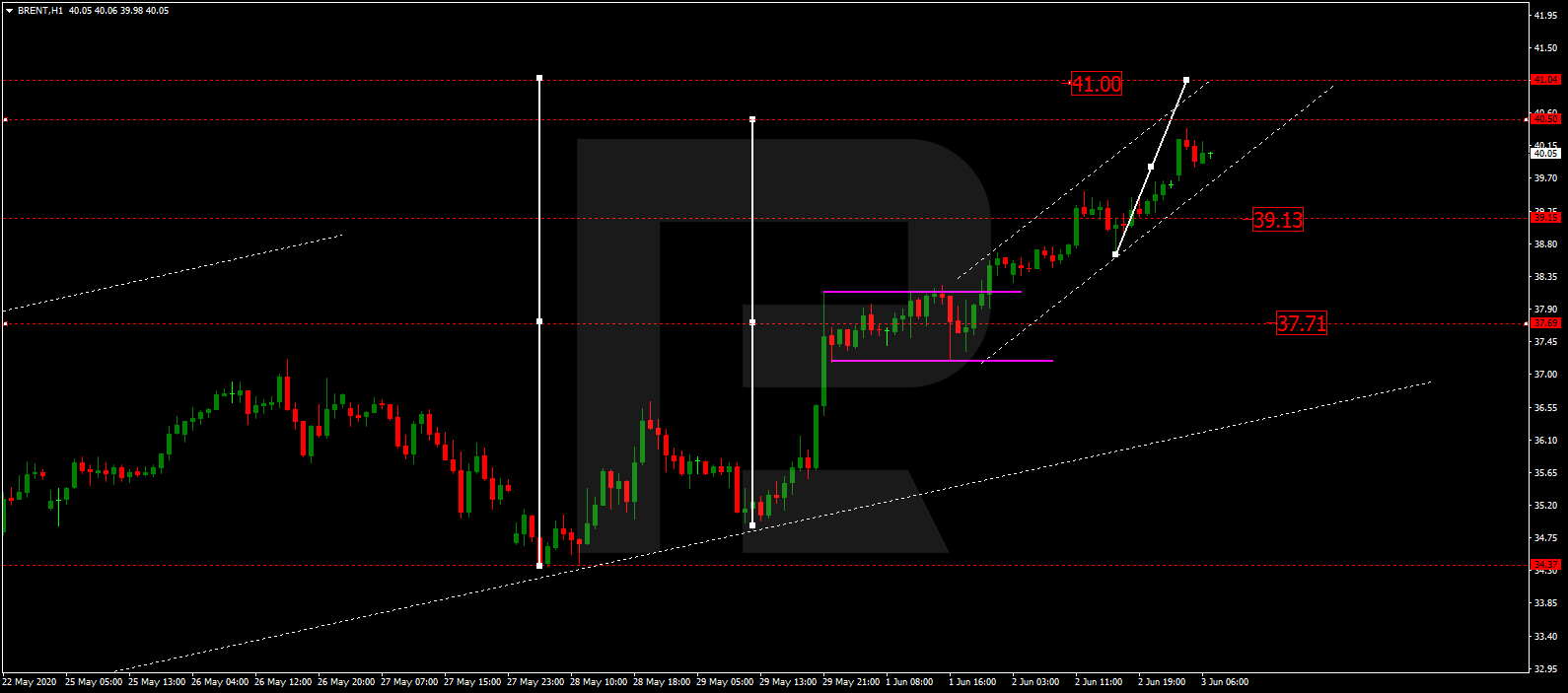

BRENT

After reaching 39.10 and forming a new consolidation range around this level, Brent has broken it to the upside to reach 40.10. Today, the asset is expected to continue growing towards 41.00. After that, the instrument may start consolidating. If later the price breaks the range to the downside, the market may correct with the target at 37.70.

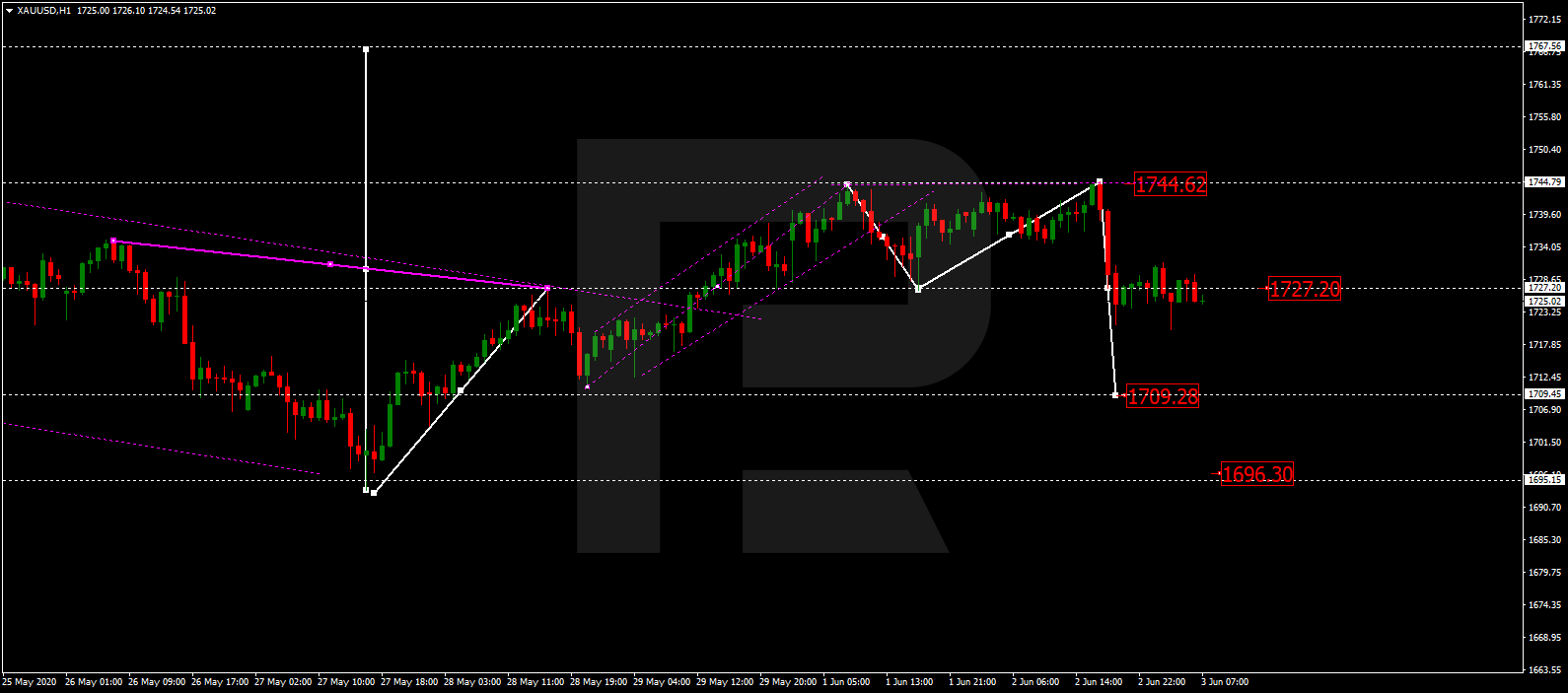

XAUUSD, “Gold vs US Dollar”

After rebounding from 1744.00 downwards, Gold has reached the downside border of the range at 1727.27; right now, it is consolidating around this level. If later the price breaks the range to the downside, the market may resume falling with the target at 1709.20; if to the upside – form one more ascending structure to reach 1744.40.

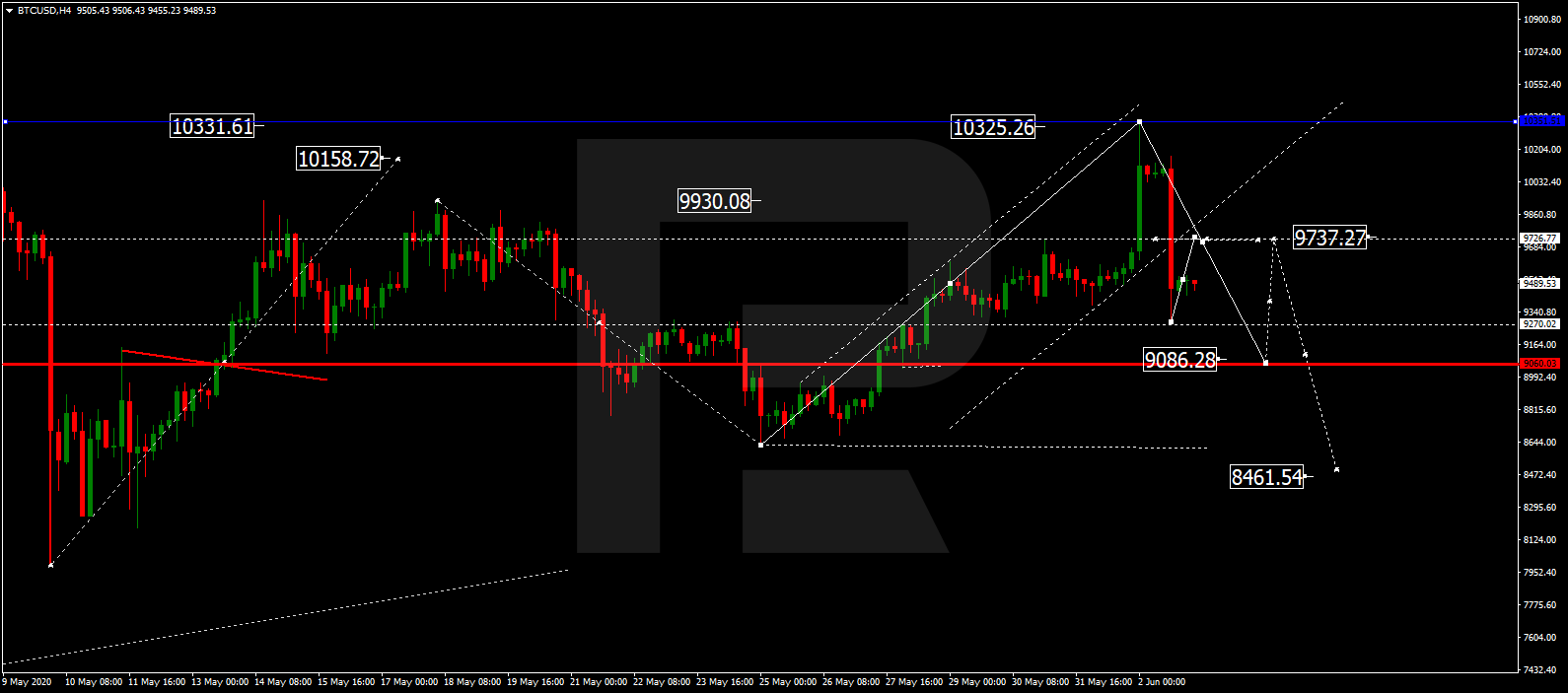

BTCUSD, “Bitcoin vs US Dollar”

After completing the descending structure at 9750.00 and breaking this level downwards, BTCUSD is expected to continue falling towards 9085.00. Later, the market may grow to test 9700.00 from below and then continue the correction with the target at 8500.00.

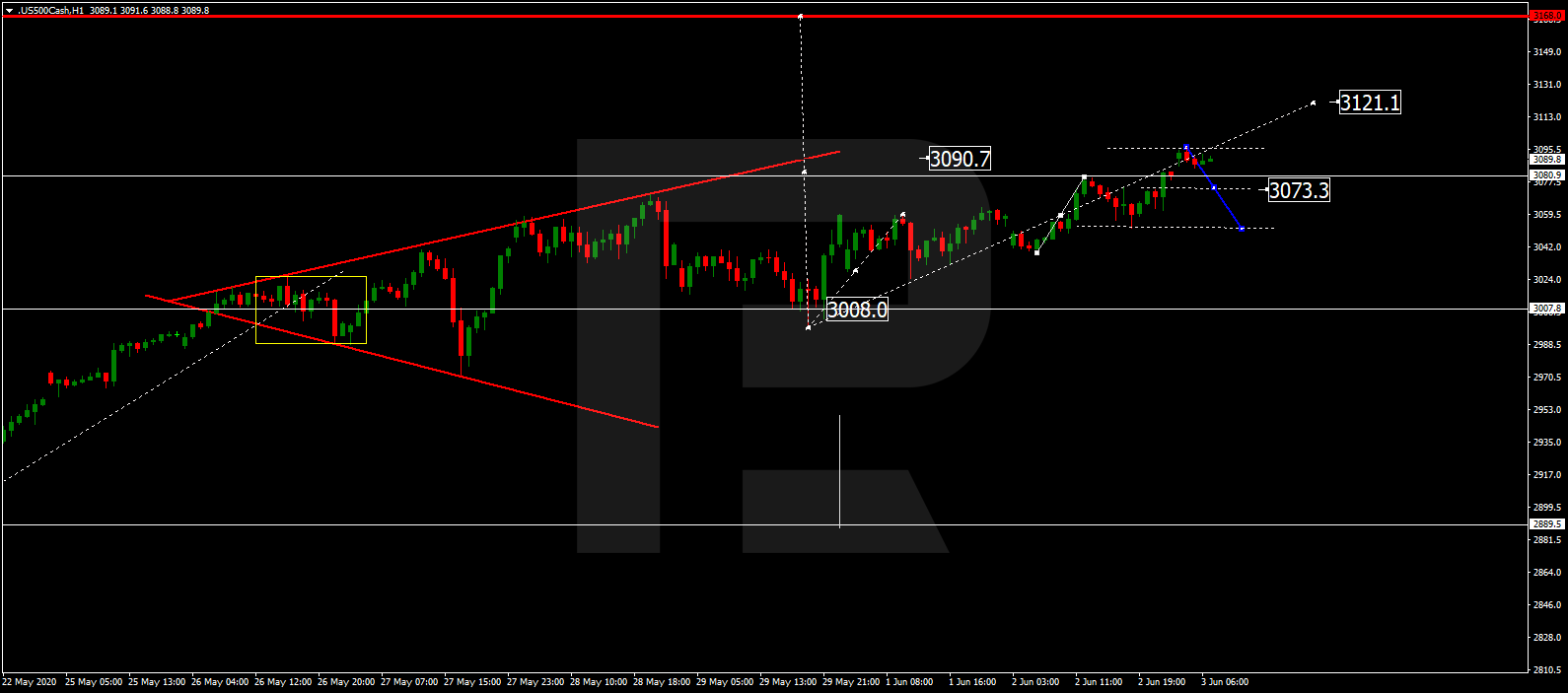

S&P 500

The Index has completed the ascending wave at 3090.5. Today, the asset may correct to reach 3073.6 and then start another growth with the target at 3125.5.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Investor Riley Ireland provides his investment thesis for this explorer with gold properties in Canada.

Investment Highlights:

Strong management with direct ownership

Low market cap of $4,709,629

New gold discovery in New Brunswick on its Grog property

Exploration and drilling in a very active area on their Troilus Property begins imminently

Troilus East exploration and drilling fully funded through investments by Fonds de solidarité FTQ and SIDEX, société en commandite

Troilus East property directly adjacent to Troilus Gold Corp. ($TLG.TO) with a market cap of $103 million

Troilus Gold Corp. ($TLG.TO) has already confirmed 6.4 million ounces (all categories) on its Troilus property and geology suggests the formation could extend to X-Terra’s property

“Undervalued” is a term thrown around a lot these days, especially when it comes to the resource mining sector. Unfortunately, most of these so-called “undervalued” plays are undervalued for a reason and eventually turn out to be nothing more than promotional hype and paper selling. News releases are commonly packed with buzz words like “visible gold” and “high-grade,” which temporarily attracts the attention of retail investors in droves while creating a chart that would compete with Mount Everest. When the hype dies down, investors are left wondering what happened to those supposed high grade and visible gold as the marketing fizzles out along with their investment.

X-Terra Resources Inc. (XTT:TSX.V; XTRRF:OTCMKTS; XTR:FSE) is an undiscovered gem that has made its own discovery recently in New Brunswick. In addition, the company will carry out exploration and drilling in the coming weeks at its Troilus East property, which is right next to Troilus Gold Corp. ($TLG.TO; Market Cap: $103 million). The program is already fully funded through investments by Fonds de solidarité FTQ and SIDEX, société en commandite, so no financing is expected in the foreseeable future.

Strong Management with Direct Ownership

In order to find the winners, or at least a company that gives us the greatest potential for success in the resource mining space, one must look at several factors. Number one, which Rick Rule has stated, is management. In the junior mining space you need solid management and leaders who stand to make exponentially more from their stock and incentive options than from their salary. You need management who puts their own money back into the company and you need management who wants to make a respectable name for themselves in the industry. Behind that management you need a well-oiled experienced machine, and in the resource sector that means geologists with proven track records of profitable discoveries.

X-Terra Resources management and team checks all the boxes. President and CEO Michael Ferreira is as direct as they come, anchored by perseverance, adaptability and risk management, he has been able to lead his team to a new gold discovery through what some may say has been an extremely challenging junior exploration market. A quick glance at the SEDI reports will show that this CEO has a strong history of buying in the open market (sometimes at prices much higher than today’s price) and has continued to do so, even as recently as May 8 (X-Terra’s CFO bought as recently as May 15).

Senior consulting geologist Martin Demers, P. Geo, brings a plethora of experience to the table including a re-discovery of the Casa Berardi mine that was bought out by Hecla Mining ($HL:NYSE) for over $750 million. If you look closer at management’s approach, you’ll notice they do things meticulously and methodically. They have taken their time and use every tool available to help identify the best use of the drills including high resolution heliborne geophysical magnetic survey and 3D mag inversion (VOXI) modelling. This team doesn’t just shoot from the hip. Every step is meticulously planned to ensure drilling will be done as efficiently and cost effective as possible.

Grog Discovery (New Brunswick)

Management might be the #1 thing to consider for a junior mining company, but their properties are also vital to the success. X-Terra recently drilled its New Brunswick properties, the Grog and the Northwest, with surprising and exciting results at their Grog property.

Grog is an epithermal system, which simply put, won’t require high grades to be profitable. Epithermal systems are usually shallow and easily mined as long as there is sufficient size. Example: Equinox Gold’s ($EQX.TO) Mesquite mines M&I resources is 1.9 MOZ @ 0.46 g/t Au. If you take the time to research epithermal mines, you’ll see that most grades are under 0.60 g/t Au. What makes this exciting for Grog is “hole GRG-20-012 identified gold (“Au”) mineralization over a significant width with one interval of 0.41 g/t Au over 36 metres along the hole, which includes 0.46 g/t Au over 31 metres and includes 7.59 g/t Au over 0.6 metres located at a vertical depth of 81 metres under the Grog.” Translation: this is a brand new discovery. And let’s not forget about the higher grade sweetenerthe hydrothermal breccia that highlights two important elements: the confirmation of hydrothermal activity and the potential for bonanza grades within the epithermal system.

This is a game changer for the area and it went completely unnoticed by the investing market during this COVID-19 pandemic. The discovery has even captured the attention of CBC (you will have to translate the page for English): https://ici.radio-canada.ca/nouvelle/1701219/or-decouverte-restigouche-mine-exploration. This was virgin undrilled land prior to this drill program and the company managed to hit something significant.Now that the geologists know what mother nature is hiding, they will be able to home in their drill targets with laser focus when they start a second drill program at the Grog. This is the value of the Grog property that retail investors have completely missed as many retail investors do not understand epithermal systems. But the geologist, well funded mining investors, and large mining companies will eventually take notice, if they haven’t already!

Troilus East (Quebec)

The other prized property in X-Terra’s portfolio, which will commence exploration and drilling in the weeks ahead, is the Troilus East Property located on the Frotet-Evans Greenstone Belt situated on the eastern side of the past producing Troilus Gold mine, now owned by Troilus Gold Corp. Last fall, Troilus Gold Corp. published a new mineral resource estimate of 6.47Moz AuEq (all categories) and have continued drilling successfully ever since. Troilus Gold Corp. is currently sitting at a $103 million market cap at the time of writing . X-Terra’s Troilus East property is the second largest land holding in this highly active area and has never been drilled. X-Terra has announced a fully funded summer program to explore and drill this property. This property alone screams value and has incredible potential. If the X-Terra team can prove that Troilus Gold Corp’s mineralized envelopes can be repeated on Troilus East as geology suggests, it could lead to incredible interest from big investors and major players in the sector.

There is more to like about X-Terra Resources from a longer-term perspective, such as their polymetallic Ducran Property and its oil and gas properties in Quebec. However, this article is focused on the current and near-term catalysts of the Grog property in New Brunswick and the Troilus East property in Quebec. Either one of those properties could cause X-Terra’s market cap to climb rapidly beyond its tiny $4.7 million value. The fact the company has its hands on both of these properties, with one essentially de-risked, is remarkable. The Grog discovery going unnoticed by the market in these turbulent times is an incredible opportunity. When you add X-Terra’s upcoming exploration and drilling on Troilus East, with neighboring Troilus Gold Corp. continuing its drilling, and gold prices challenging all time highs, and you have a perfect storm brewing with X-Terra Resources.

Riley Ireland, a seasoned investor who sees value in early stage projects, is financial consultant to Arbutus Point Financial and an options trader.

Disclosure: 1) Riley Ireland: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: X-Terra Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Riley Ireland disclosure below. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: X-Terra Resources. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with X-Terra Resources. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports (including members of their household) own securities of X-Terra Resources, a company mentioned in this article.

Riley Ireland Disclosure: This article expresses my own opinions. I am not receiving compensation for it. I am long XTT stock.

Peter Epstein of Epstein Research profiles an explorer in Colombia with a project on the same prolific gold belt as Buriticá.

The importance of good community relations and avoiding serious outcomes from bad environmental stewardship is paramount. Moreover, in the age of COVID-19 and a 7-year high in the gold price, investors are increasingly interested in countries with abundant mineral resources, that are not among the top producers, countries like Colombia. At the same time, due to COVID-19, local communities will be in need of good, longer-term, high-paying jobs.

Although Colombia remains riskier than the U.S., Canada or Australia, most of the country is considerably less risky than at least three of the world’s top six gold producing countriesChina, Russia and Indonesia. Colombia has a globally significant endowment of potentially mineable metals, yet has been woefully under-explored.

The ability of foreign firms to safely conduct mining activities in Colombia is improving. The newly elected federal government is pro-resource development as a means of accelerating government royalty revenue. For example, it is spearheading a national US$25 billion infrastructure program building roads, highways, bridges and tunnels to improve logistics throughout the Andes.

It doesn’t hurt that giant Zijin Mining recently acquired Canadian junior Continental Gold for US$1.05 billion = ~C$1.5 billion (at today’s C$ exchange rate) in cash (share price tripled in year leading up to takeout) outbidding Newmont Corp. for a truly world-class Colombian asset. Continental discovered and developed Buriticá, one of the highest grade, pre-production projects in the world.

Buriticá had 5.67 million Measured and Indicated ounces at ~11 g/t Au Eq, + 6.46 million Inferred ounces at ~9.2 g/t Au Eq. At US$1,200/oz gold, this project had an after-tax NPV(5%) of US$860 million and an internal rate of return (IRR) of 31.2%, and a whopping US$1.6 billion NPV & 48% IRR at today’s spot price of ~US$1,722/oz. An estimated All-In Sustainable Cost (AISC) of ~US$600/oz places it in the bottom decile of the global cost curve.

Newmont wanted Buriticá. AngloGold Ashanti is active in Colombia. B2Gold has an open pit JV with AngloGold that’s expected to deliver a BFS within nine months. Gran Colombia is the largest underground gold-silver producer in the country (until the Buriticá mine starts later this year). Gold-heavy juniors include; Caldas Gold, Royal Road Minerals, Outcrop Gold, Antioquia Gold, Cordoba Minerals and FenixOro.

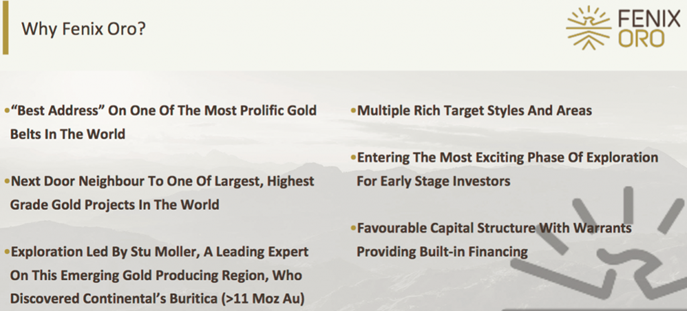

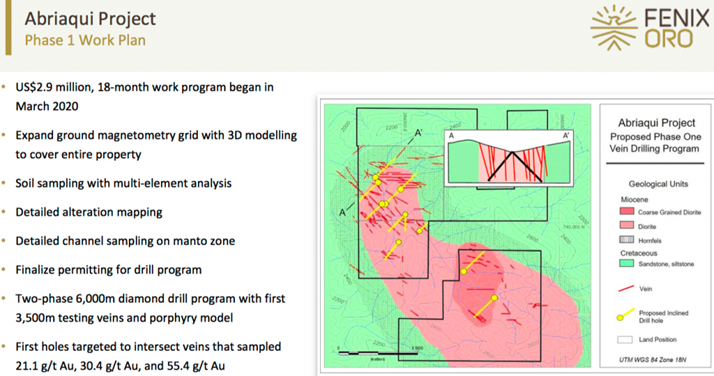

FenixOro Gold Corp. (FENX:CSE) is a company that readers should take a closer look at. Shareholders believe it could be the next Continental Gold, that its Abriaqui project could be another Buriticá. Even if one considers this view an exaggeration (we need to see some drill results), many critical factors suggest the claim is within the realm of possibility.

Led by CEO John Carlesso, a 25-year veteran of the international business world and founder/director of a number of companies. John was VP Corporate Development for Desert Sun Mining when it was acquired by Yamana Gold for $750 million. Over the past 18 years, Mr. Carlesso has focused on LATAM deals.

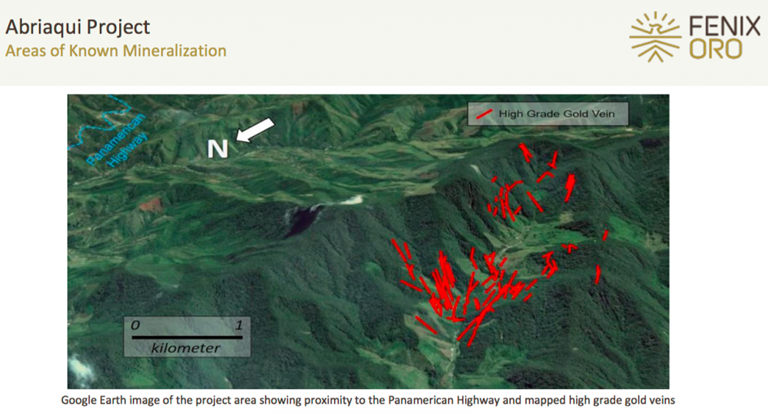

Since 2007, >80 million ounces of gold have been discovered on the 200 km long Middle Cauca gold belt (one of the most prolific in the world) hosting Buriticá and FenixOro’s Abriaqui projects. AngloGold Ashanti has two 20+ million ounce deposits in the belt. Notably, Abriaqui at ~550 hectares is packed into a much smaller footprint than Buriticá at 75,000+ hectares.

How is it possible that Abriaqui could potentially host a multi-million ounce deposit on just a 5 sq km surface footprint? For an answer, I asked newly appointed VP of Exploration (and a director) Stuart Moller (more on him later). He turned me to slide 8 of the May 2020 corporate presentation, explaining that the entirety of Buritica’s resource fits onto roughly one quarter (1/4) of the area of the Abriaqui project. Moller said,

“As shown in the inset of slide 8, the entire Buriticá resource is contained within the 100-hectare red box, shown at the same scale as the Abriaqui map in the figure. Comparing the outcrop area and dense spacing of the Abriaqui veins with Buriticá’s footprint, we believe we have plenty of room for a sizable orebody within our licenses.”

I invite readers to continue reading and to consider the risk-reward proposition here. FENX’s Enterprise Value (EV) [market cap cash + debt] of ~C$14 million is less than 1/100 (< 1%) the size of Continental Gold’s takeout value. Although admittedly an apples to oranges comparison until/unless a significant discovery is made by FenixOro, investors should know in a matter of months, not years, if there’s something exciting that warrants further drilling.

The secret to the blue-sky potential at Abriaqui, and Buriticá’s existing 12M+ Au Eq resource, is the depth and continuity of mineralization across each company’s project areas. The technical team at FenixOro has already traced high-grade gold veins over ~900 meters of vertical extent, from gold outcrops at ~2,800 meters elevation, to workings at ~1,800 meters. Buriticá has greater than 1,200 meters of vertical extent and remains open at depth.

FenixOro’s Abriaqui project is directly on trend, and ~15 km west of Buriticá. Closeology is nice, but there’s a lot more to this story. First and foremost, there’s VP of Exploration/Director Stuart Moller. With 40 years’ experience in international mineral exploration, he held senior roles with Barrick and Pan American Silver.

As VP of Exploration at Continental Gold, Mr. Moller led the team that discovered Buriticá and was in charge of the first 270 drill holes. Few, if any, geologists on the planet are better suited to find the next Buriticá deposit than Mr. Moller. He and his technical team are anxious to conduct the very first meaningful, modern drill program on FenixOro’s property.

Armed with a great team, 40 years’ exploration under his belt and invaluable experience from drilling a giant discovery just 15 km away, Mr. Moller is understandably quite excited and optimistic. At the same time, he’s realistic. He told me that as bullish as he sounds over the phone, one never knows what a deposit holds until you drill it. The time has come to show the world what’s hidden below surface, not just talk about it.

Second, a fully funded [6,000 meters, 1820 holes] phase 1 drill program is expected to start in about two or three months. Unlike giant exploration properties where there can be hundreds of drill holes before a large discovery is made, management expects to identify a lot of mineralization in phase 1. Readers should note, FenixOro has already delineated >100 narrow, high-grade veins.

Readers should note, it’s not just narrow (~30150 cm wide, tightly spaced, several meters apart) high-grade and possibly ultra-high-grade veins (>50 g/t). Equally important is the grade of mineralization between the veins. Investors will get a sense of this from phase 1 drill results starting in late summer or early fall.

Third, the gold price at US$1,722/oz is a spectacular development. Until recently, I never mentioned strength in the gold price as an investment merit. This year is different. I believe gold will stay strong at least through January 2021, due to the economic fallout from COVID-19, global debt-fueled stimulus programs/money printing and U.S. elections. If Trump loses, some fear his departure from office in January could be contentious.

Fourth, not only is Colombia well-endowed with minerals, it’s a low-cost jurisdiction to explore and develop. Fifth, as mentioned, the Colombian government is spending up to US$25 billion on infrastructure projects. A major 4-lane highway, complete with new power lines, from Medellín will come within 4 km of the Abriaqui project, cutting travel time in half to under two hours.

Despite not having drilled yet, a great deal is already known about the Abriaqui project. Over 300 chip or channel samples have been taken with assays of up to 146 g/t gold. More than 15% were >20 g/t gold. Hundreds of soil samples are in the lab awaiting assays. Greater than 100 high-grade veins have been mapped.

We can be reasonably sure that water, labor and power availability will not be a problem. Mr. Moller has lined up a well-known Canadian drill contractor, at very low cost. Community relations are strong. FenixOro has prudently partnered with a third generation local mining cooperative.

As mentioned, strong continuity and upwards of 1,000 meters of vertical extent support the possibility of a large or very large gold deposit. The gold is “free-milling,” as can be seen in the production from small water-driven gravity separation mills on the property.

FenixOro Gold Corp. (CSE: FENX) is fully funded well into next year. Therefore, evidence of something potentially worth much more than the company’s current EV of just C$14 million could come by the fall, well before the need to raise additional equity capital.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about FENIXORO GOLD., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of FENIXORO GOLD CORP. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, FENIXORO GOLD CORP. was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Technical analyst Clive Maund discusses Greenbriar Capital shares’ big ramp up following its agreement with the Puerto Rico Electric Power Authority.

We hit the jackpot with this one, so it was a bit silly of me to say that traders might want to think about taking some money off the table on Friday morningsilly because the Montalva solar energy project deal that Greenbriar Capital Corp. (GRB:TSX.V; GEBRF:OTC) has done with PREPA (Puerto Rico Electric Power Authority) is going to end up being worth about C$10 a share, and I’ve heard it said that it could be a $17 stock. The deal now moves on to final approval by the Puerto Rico Energy Bureau (PREB) and the Puerto Rico Financial Oversight and Management Board (FOMB). This process is expected to last two to three weeks (from now) and should be a mere formality, a rubber stamp job.

We bought the stock back at the perfect entry point 2 weeks ago as it completed a bull Flag, since which time it has accelerated into a vertical ramp on news of the deal being clinched, as you will see on the latest 6-month chart shown above. With this deal being worth approximately C$10 per share it is clear that the stock is probably on its way to this level, however, that said, we can expect to see some jitters and profit taking in the days leading up to the final approval, so we will keep an eye on it and “play it by ear” as this time approaches. Since it is already super critically overbought on its RSI indicator after Friday’s big jump, we can expect it to hit some profit taking “air pockets” from now on, and anyone who wants in or wants to add to positions should do so on any larger intraday dips, but as the date of final approval approaches in a couple of weeks we may look to take profits.

Greenbriar Capital Corp, GRB.V, GEBRF on OTC, closed at C$2.98, $2.15 on 29th May 2020.

Originally posted on CliveMaund.com at 1.15 pm EDT on 31st May 2020.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Clive Maund: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. CliveMaund.com disclosures below. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports (including members of their household) own securities of Greenbriar Capital, a company mentioned in this article.

Charts provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Shares of Myovant Sciences traded 40% higher after the company reported that it has submitted a New Drug Application to the FDA for once-daily relugolix combination tablet for the treatment of women with uterine fibroids.

Healthcare company Myovant Sciences Ltd. (MYOV:NYSE) today announced that “it has submitted a New Drug Application (NDA) to the U.S. Food and Drug Administration (FDA) for its once-daily relugolix combination tablet (relugolix 40 mg, estradiol 1.0 mg, and norethindrone acetate 0.5 mg) for the treatment of women with heavy menstrual bleeding associated with uterine fibroids.”

The company’ CEO Lynn Seely, M.D., commented, “An estimated five million women in the U.S. suffer from symptoms of uterine fibroids, which may include heavy menstrual bleeding, pain, and anemiayet effective non-invasive treatment options are very limited…If approved, we hope to redefine care for these women with relugolix combination tablet, a potential new treatment that demonstrated a predictable and clinically-meaningful reduction in menstrual blood loss while maintaining bone health in the Phase 3 LIBERTY program.”

The company highlighted in the report that “the NDA is supported by positive data from two Phase 3 studies and a long-term extension study, demonstrating sustained reduction in heavy menstrual bleeding while maintaining bone health through one year, and that if approved, relugolix combination tablet would be the first once-daily, oral treatment for women with heavy menstrual bleeding associated with uterine fibroids in the U.S.”

The firm additionally pointed out that this NDA is the third such regulatory application it has submitted this year noting that it filed a Marketing Authorization Application to the European Medicines Agency in uterine fibroids and an NDA in advanced prostate cancer.

The company explained that “uterine fibroids are noncancerous tumors that develop in or on the muscular walls of the uterus and are among the most common reproductive tract tumors in women.” The firm noted that around five million women in the U.S. suffer from symptoms of uterine fibroids.

The company listed that “relugolix is a once-daily, oral gonadotropin-releasing hormone (GnRH) receptor antagonist that reduces ovarian estradiol production, a hormone known to stimulate the growth of uterine fibroids and endometriosis, and testicular testosterone production, a hormone known to stimulate the growth of prostate cancer.”

The company is presently developing a relugolix combination tablet for use by women with uterine fibroids and for women with endometriosis and is also working on a relugolix monotherapy tablet for men with advanced prostate cancer.

Myovant Sciences Ltd. is a clinical-stage biopharmaceutical company focused on developing and commercializing therapies for the treatment of women’s health, prostate cancer and endocrine diseases. The company’s lead product candidate is relugolix, a once-daily, oral GnRH receptor antagonist that binds to and inhibits receptors in the anterior pituitary gland. The company has three late-stage clinical programs for relugolix in uterine fibroids, endometriosis and prostate cancer.

Myovant Sciences began the day with a market capitalization of around $1.1 billion with approximately 89.87 million shares outstanding and a short interest of about 3.5%. MYOV shares opened higher today at $12.54 (+$0.29, +2.36%) over Friday’s $12.25 closing price. The stock has traded today between $12.44 and $19.00 per share and is currently trading at $16.99 (+$4.74, 38.69%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Sector expert Michael Ballanger bemoans the panic-inducing influence of politicians and the influx of “counterfeit currency” from central banks on the money and commodities markets.

One look at the chart of the U.S. financial markets against the backdrop of economic paralysis and suffering, and one is immediately filled with a myriad of emotions. Sympathy for those that have been afflicted by the most recent pandemic; fear for the families whose primary breadwinner is now unemployed; confusion toward the proper course of action going forward; and finally outrage at the abject timidity of our citizens in responding to the orders laid down by these insipid politicians in response to the crisis.

As the welfare of future generations hangs in the balance, its tentativeness the direct result of government ineptitude, I keep asking myself a critical question: “When did the backbone of our people turn to mush?” If someone holding political office had told my grandfather to stop ploughing his fields or tending to his livestock because a sickness was spreading throughout the community, that charlatan would have wound up with buckshot adorning his gluteus maximus. How dare any group of elected bureaucrats ordain the shutdown of an economy? Telling citizens to “stay home” and “avoid contact” was tantamount to telling my grandfather to cease and desist in providing for his family. That he should shutter the ploughs and the reapers and the milking stations, that his sons and daughters need not feed the chickens or slop the hogs because the government was going to “protect them” from harm? Well, not only would promises like that go unheeded by the generations that preceded us; they would be treated with the utmost of distrust and the vilest of response.

The reason that citizens of North America fled Europe and the British Isles to become settlers in the New World was because acceding to government orders and laws and rules and edicts had left them wallowing in a sewer of social and economic slavery while the elites inhabiting the privileged classes prospered. Sadly, over the last century or so, starting around 1934 with the creation of the first U.S. “central bank” (the Federal Reserve), citizens have been purposefully softened by the availability of social safety nets that started innocently and well intentioned in the 1930s, with programs like the Tennessee Valley Authority and later Freddie Mac and Fannie Mae.

But at every sniff of an economic downturn, political responses have grown progressively more rapid and more extreme. With the mainstream media (which is now social media more than print or TV/radio media) providing a wonderful symphony of accompaniment, the political grandstanders have been able to generate a cavalcade of panic, which has provided the perfect cover for clandestine enrichment of the corporate sector, once again, as in 2009, from the public purses on the pretense of economic Armageddon.

Fellow citizens, I ask you: How many times must you be subjected to this moral hazard rot before you arm yourselves with torches and pitchforks and enact change?

Back in late February, when the fear-mongering was just shifting into gear, I was ranting and raving about the REPO operations back in late September and asking why the Fed was bailing out the hedge funds. I was waving the red warning flag long before COVID-19 conveniently arrived on our doorsteps to present a “clear and present danger” to all aspects of Western civilization, to the extent that the U.S. central bank alone has authorized an injection of $10 trillion into the corporate pig trough. That is a pittance when one adds the Bank of Japan (BOJ), the Bank of China (BOC), the European Central Bank (ECB), the People’s Bank of China (PBOC), and all of the other purveyors of counterfeit currency to the mix.

Where was it ever written that an elected official has the right to impair the purchasing power of years of labor and prudence and savings of the average citizen? What gives any politician the right to debase my money, upon which I deserve to rely as I move into retirement?

You must forgive me for sounding like a bitter, disillusioned old man but the events of the New Millennium are growing more and more apocalyptic as the days wear on. Today I read that the CDC (Centers for Disease Control and Prevention) has agreed with the findings of scientists from Yale and John Hopkins, and has determined that the mortality rate for the current pandemic is no different than for any other strain of infectious virus.

In other words, whether or not these political wand wavers ordered work stoppages or not, the same rate of fatalities would have occurred. Whipped up into a media-frenzied print-fest, the Fed and the U.S. Treasury just trashed your savings, your pensions and your Social Security by assuming leadership of a crisis for which not one person was either qualified to assess nor capable of managing. The “clear and present danger” was not the pandemic; it was the politicians and the money changers inhabiting the temple.

Markets

What markets? There are no “markets” anymore. All I see when my quote terminal starts flashing these days is the New York Fed’s omnipotent computer programs whirling away, assigning their desired price objectives to literally everything. Yield curve moving back to inverted? Nopebuy all short-dated bonds until the two-year yield is down. Thirty-year yield moving lower? Nopesell the hell out of the 30-year until we get that yield well above the two-year. Stocks looking a tad weepy? Nopebuy a 500-lot of the E-minis and trigger the algos to the buy side.

And gold! What the hell is it doing at $1,750/ounce? Offer three times annual global production $40 under cash, and we can easily fix that problem, too! Everywhere I look I see criminal interventions making it impossible for me to apply the skills I learned over 40 years to the practice of managing risk.

The near-term outlook for stocks is now locked within the walls of the Eccles Building in Washington; the models that have been constructed have no historical precedent upon which to rely. These economists all disagree on every point except one: credit creation. Since all they really understand is the process of debt application to solve all problems of a fiscal and monetary nature, the pandemic now provides an entirely new bogeyman to be vanquished through monetization. Adding a health crisis to the banking crisis of 2008 and the liquidity crisis of October 2019 (when the REPO ops began in earnest), their models completely and conveniently omitted the underlying systemic cause of disruptionswhich, of course, is debt.

I learned long ago that after periods of sustained credit creation in any society, there comes a moment when the marginal benefit of one additional dollar of debt has zero impact on either gross domestic product (GDP) or money velocity, with the latter more important than the former. The world passed that threshold in 2008, and was beginning the violent and deflationary process of debt destruction when the international banking cartel, led by the Wall Street/Washington ringleaders, held out their hands. After using the MSM (mainstream media) to spread panic throughout the campaign headquarters of the political classes, they secured permission to reverse the debt elimination process through an unprecedented credit creation orgy that papered over the insolvency and illiquidity of the purging process.

Sure enough, the policymakers discovered the impossibility of reversing an exploding debt bubble, and that you can no more assuredly reverse a credit bubble’s popping than you can the direction of the St. Lawrence River. You can divert the flows temporarily, but you can never reverse them.

The first signs of the return of the credit reckoning came last autumn with the “not QE” REPO operations that were all centered around the growing illiquidity in the treasuries markets, which then began to bubble over into corporate high yield. As the size and scale of the REPO actions were escalating wildly as late as February, the debt destruction monster was starting to become an unpopular narrative that was threatening to overshadow the China trade war and talks of impeachment. In an election year, the last thing any Republican could handle was the re-emergence of this credit “hydra.”

Enter the Wuhan pandemic and what arrived in the nick of time was the perfect cover for yet another debt-fueled diversion of the credit reckoningbut this time, unlike 2009, the money-printing bazooka used by Hank Paulson has been replaced by a fifty-megaton nuclear weapon of mass distraction designed to keep the citizenry terrorized and under control.

In past times, the layering of large swaths of counterfeit currency on top of systemic insolvency was done so delicately, and usually with little drama or fanfare. In the ’80s, when the savings and loan industry was buried in bad loans that threatened the big Wall Street counterparties, they deftly and surgically moved the problem “off balance sheet,” which is a polite way of saying that they lifted the corporate governance carpet and with the flick of the broom, swept the rotting remnants of corruption, bribery, and boardroom malfeasance under, never to be seen or spoken of again.

Fast forward to 2020. There are now daily press conferences with the thespian thought-managers front and center, all giving opinions and pronouncements on issues over which they have no control and about which they have no knowledge. To say that I am irked by the arrogance of the self-professed “experts” in espousing forecasts on everything from mortality rates to economic recovery rates is an understatement; these blowhards have zero understanding of, nor ability to predict, anything related to the pandemic. Therefore, they had zero authority to make decisions affecting millions of citizens in countries all over the world. Yet they did, and now we must live with their gambles on how we should live our lives.

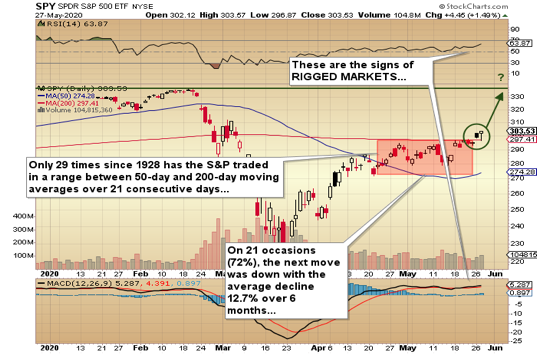

There is only one chart to show, and it is one that depicts the insanity of the day. Thanks to this coordinated orgy of preventative credit expansion, equity markets, led by the S&P 500, have roared back from the abyss. Debt-to-GDP at 140% and forward P/Es (price-to-earnings ratios) in the never-before-seen 24 ranges are today the “new normal,” and not to be feared but rather embraced, because at the end of the day, there can never ever again be bankruptcies of a corporate origin. These might impact the unemployment rate and, more importantly, stocks, and if stocks are in decline, people will be afraid to spend the money they no longer have, and that they lost while providing for their families after the government forced their employers to stop all operations.

I watch riots breaking out in Minneapolis, and now L.A., over yet another racially charged police action causing the death of a citizen, and firmly believe that this is going to become an accelerant to the outrage that is simmering on the back burners in households all across the globe. The SPY looks like it wants to probe higher, and quite possibly test the February pre-COVID highs, but from my perspective, valuations are absurd and joined by risks that are now even higher than I sensed in February, when I urged subscribers to short the SPY at 326.

Will I short the SPY again any time soon? Well, if I am in a Las Vegas casino and I see the pit boss whispering to a croupier about a player on a “roll,” I can promise you that I will not be joining that table any time soon. There are just too many big players who want to see stocks higher, and bonds and gold “controlled,” and until I have certainty that the trillions upon trillions of Fed credit bestowed upon the Wall Street crowd is not aimed at the stock market and Donald Trump’s reelection, I will be happy to keep the bulk of my investible cash exactly thatin cashwith an overweight position in gold and silver junior developers with ounces in the ground and fortunes to be made when the levee finally breaks and the oceans of toxic debt flood the fields.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.