Shares of Cassava Sciences traded 70% higher after the firm provided updates from its Phase 2b study of PTI-125 for use in treating Alzheimer’ disease.

Clinical-stage biotechnology company Cassava Sciences Inc. (SAVA:NASDAQ), which focuses on neurodegenerative diseases including Alzheimer’s disease, today announced that “its management is scheduled to present at the Jefferies Virtual Healthcare Conference today, June 3, 2020, at 3:00 p.m. EST.”

The firm provided an update that included discussion pertaining to “recently announced top-line results of a Phase 2b randomized, placebo-controlled study of PTI-125 in patients with Alzheimer’s disease.” The company stated that it feels that “high variability in levels of biomarkers over 28 days in placebo-treated patients, and other possible factors, may drive a reassessment of overall results for its Phase 2b study.”

The company’s President & CEO Remi Barbier commented, “We think it’s worth reflecting on what can be learned from our Phase 2b study by closely examining the clinical data, methods used to generate the data and drug effects on cognition…These on-going analyses may teach us how to move forward with our drug development plans for PTI-125 in Alzheimer’s disease.”

Cassava Sciences listed some of the key elements to its strategy to better understand the overall outcome of the Phase 2b study of PTI-125. The firm plans to re-analyze cerebrospinal samples from all study participants, analyze lymphocyte & plasma samples from all study participants and evaluate the effects of PTI-125 on cognition. The company indicated that it expects to announce the results of these analyses in H2/20.

The firm explained that PTI-125 is its lead therapeutic product candidate for the treatment of Alzheimer’s disease. According to the company, “PTI-125 is a proprietary, small molecule (oral) drug that restores the normal shape and function of altered filamin A, a scaffolding protein, in the brain.”

The company noted that “Alzheimer’s disease is a progressive brain disorder that destroys memory and thinking skills and that presently, there are no drug therapies to halt Alzheimer’s disease or to reverse its course.” The firm reported that there are approximately 5.8 million people in the U.S. who are currently living with Alzheimer’s disease.

Cassava Sciences Inc. is a clinical-stage biopharmaceutical company based in Austin, Tex. The company focuses its efforts on detecting and treating neurodegenerative diseases, such as Alzheimer’s disease. The firm stated that “it has combined state-of-the-art technology with new insights in neurobiology to develop novel solutions for Alzheimer’s disease, and owns worldwide development and commercial rights to its research programs in Alzheimer’s disease, and related technology, without royalty obligations to any third-party.” The firm mentioned that is also working on developing an investigational diagnostic called SavaDx in order to detect Alzheimer’s disease with a simple blood test.

Cassava Sciences started off the day with a market capitalization of around $50.6 million with approximately 24.78 million shares outstanding and a short interest of about 10.00%. SAVA shares opened nearly 17% higher today at $2.38 (+$0.34, +16.67%) over yesterday’s $2.04 closing price. The stock has traded today between $2.26 and $3.90 per share and is currently trading at $3.48 (+$1.44, +70.59%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Revive Therapeutics is focused on infectious diseases as well as treatments using psilocybin-based formulations.

Revive Therapeutics Ltd. (RVV:TSX.V; RVVTF:OTCMKTS), a company that focuses on repurposing drugs for infectious diseases and rare disorders, is preparing to submit to the U.S. Food and Drug Administration (FDA) an Investigational New Drug (IND) application for a Phase 3 confirmatory trial to evaluate Bucillamine in patients with mild to moderate Covid-19.

The drug has a long history, having been used in Japan and South Korea for over 30 years for rheumatoid arthritis. Revive has a clinical history with the drug, repurposing it to conduct a Phase 2 trial in the United States in 2015 for acute gout flares and cystinuria, a form of kidney stones. While it never went to market, Revive possesses substantial data on its safety and efficacy.

“Bucillamine as an agent has a lot of strength in terms of anti-inflammatory advantages,” Michael Frank, chairman and CEO of Revive Therapeutics, told Streetwise Reports. “From its long use in Japan and South Korea, it has a lot of good history, and good safety and efficacy background. Additionally, from our Phase 2 study for gout, we had a lot of data to support its safety as well as its inflammation treatment properties.”

Earlier this year, with the advent of the Covid-19 pandemic, Revive looked at Bucillamine again. “There’s a lot of data to support that Bucillamine is much more powerful as an anti-inflammatory. It can help restore glutathione, which is an amino acid in the body that can help reduce inflammation. Bucillamine has a strong indication of possibly treating symptoms like lung inflammation caused by infectious diseases from specific strains of influenza, H1N1 and coronavirus, namely Covid-19,” Frank explained.

Revive in April filed a pre-investigational new drug meeting request with the FDA for Bucillamine for the treatment of Covid-19 to proceed to a Phase 2 clinical study. The FDA recommended that the company submit its IND for a Phase 3 confirmatory trial.

The basis of the clinical study will analyze if “Bucillamine has the potential, via restoration of glutathione activity and other anti-inflammatory activity, to lessen the negative consequences of SARS-CoV2 infection in the lungs and to help treat Covid-19 manifestation,” Frank stated.

“The FDA agreed that Revive could rely on its data included in its previous IND with Bucillamine for gout to support the Covid-19 Phase 3 trial and, therefore, the company did not have to perform any Phase 1 or Phase 2 clinical studies,” the company reported.

“Because of our history with Bucillamine, and that Bucillamine has been around 30 years and it’s been effective in South Korea and Japan treating rheumatoid arthritis, and because of the data, we were asked to provide an IND to go directly to a Phase 3 triala much bigger trial,” Frank said.

“FDA’s support in advising Revive to move directly into a Phase 3 confirmatory trial provides an acknowledgment for the potential of Bucillamine in the treatment of Covid-19,’ noted Frank. “Entering into a Phase 3 study is a major milestone for the company, and we are excited to unlock the full potential of Bucillamine not only for this virus but also for other infectious diseases that we will investigate in the future.”

Revive has also stated that it intends to conduct a clinical study of Bucillamine in Covid-19 patients in Canada and today announced that it has submitted a Pre-Clinical Trial Application (Pre-CTA) to Health Canada and will have its Pre-CTA meeting with Health Canada this week.

“Unlike many micro caps in Canada and in the United States, getting to Phase 3 trial is a substantial plateau, and that’s what sets us apart,” Frank added.

Revive is also actively investigating psilocybin-based therapeutics. The firm, which acquired Psilocin Pharma Corp., is investigating “novel oral dosage forms of psilocybin, such as oral dissolvable thin films or tablets, based on the company’s wholly owned patent-pending psilocybin formulations and its exclusive licensed drug delivery technology from the Wisconsin Alumni Research Foundation.”

“We are expanding our psilocybin-based pharmaceutical portfolio with unique oral dosage and drug delivery forms that will target and have the potential to treat diseases and disorders currently not investigated with psychedelic compounds,” Frank said. “We are combining our robust intellectual property portfolio in both psychedelic formulations and our drug delivery technology which is unique within the industry, and leveraging our research partnership with the University of Wisconsin-Madison to establish a specialty portfolio of psilocybin-based pharmaceuticals that we can advance to clinical trials and partnerships with other life sciences companies.”

The company is targeting rare diseases, mental health and addiction with the psilocybin formulations.

Revive has approximately 189 million shares outstanding, 267 million fully diluted.

Disclosure: 1) Patrice Fusillo compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Revive Therapeutics. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Revive Therapeutics, a company mentioned in this article.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

In light of pandemic conditions, government reactions and the impacts of both on financial markets, Mercenary Geologist Mickey Fulp describes his investment strategy to Maurice Jackson of Proven and Probable.

Maurice Jackson: Joining us for conversation is Mickey Fulp, the world-renowned Mercenary Geologist.

I want to speak to you today about the mainstream financial news networks and the narratives that they’re pushing on both sides of the aisle, respectively. And of course, depending on the news program, the blame is always cast on the political adversaries and never, to anyone’s surprise, are they accepting blame for championing and implementing policies that have created the U.S. financial pandemic. . .it just seems to be skipping over most people’s radar, as we’re all focusing our efforts right now on COVID-19. When you look at the U.S. financial pandemic, just how bad is the U.S. economy, and did it begin with COVID-19?

Mickey Fulp: Well, there were certainly financial stresses before spawning of this flu bug in Wuhan, China. Long live frothy stock markets that were overdue for a correction, burgeoning trade, and budget deficits. And I think most importantly, American outsourcing and our dependence on China for fundamental supply chains.

But there’s little doubt in my mind that this economy was booming despite some underlying structural weaknesses, and the collapse, in my opinion, was due to draconian government overreaction in response to the immediate crisis.

So no doubt, this is a very bad, deadly flu for the elderly and the unhealthy, which would include people who are morbidly obese, diabetics, smokers, those with cardiovascular disease, those with other immune system disorders, and especially so for people living in communal conditions. But I think it’s nothing more than that. I mean, look at the facts. Fifty percent of deaths have incurred in nursing homes. And if you add people who are over 65 who are not imprisoned in nursing homes, it’s up to 75%.

I can give an example in New Mexico. Sixty-five percent of the deaths in New Mexico, which are now over 200, are on the Navajo reservation where all of the conditions that I listed above exist. So, my question is, why was the entire state quarantined and creating an economic collapse? And I think it’s a nanny state protectionism that is morphed into controlism. And it has progressed in my opinion, to socio-fascism.

Maurice Jackson: If the U.S. financial pandemic didn’t begin with COVID-19, does it end with COVID-19?

Mickey Fulp: Well, I think it really did begin with COVID-19, given some underlying conditions, which was a stock market way overdue for a correction, and budget and trade deficits, but certainly won’t end there. And the reason is, government actions have wrought major economic damage and, in my opinion, have forever changed our country. We have unemployment now at Depression-era levels, small businesses devastated and exponential increases in the money supply as tax receipts exponentially decrease. We will never recover from this! I saw something the other day: Mark Cuban refers to what’s coming as America 2.0, and I don’t welcome that.

Maurice Jackson: When you watch the mainstream media channels, what are some of the propagandas that they seem to be pushing from both sides of the aisle that have you just shaking your head in disbelief?

Mickey Fulp: Well, think about it. Does it seem too good to you, what’s coming? What has been done? This country will never be the same. Sad, but true, that the Wuhan flu is causing the economic collapse. It is government officials, many unelected, deep-state bureaucrats at all levels, locking down a country with blatantly illegal and unconstitutional fiat orders without legislative input, and that’s what’s caused the collapse in my opinion.

Maurice Jackson: A prime example of failing economic policy is the unprecedented inflation of our currency by both parties. What type of impact do you see this having on the general equities short term, and then longer term?

Mickey Fulp: Well, some major corporate equities will do well in nominal dollar terms, and a lot will go bankrupt. The rapid inflation [of the] money supply will cancel, in real dollar terms, many of the gains from the corporate entities, and a lot of those are listed on the NASDAQ. NASDAQ is up 4% this year.

But my main concern would be small business entrepreneurial ventures. And that’s what drives growth in our country. And especially Mom-and-Pop storefronts. A great majority of these businesses will never open, and the jobs that are associated with those mainly service jobs are gone forever.

It just seems wrong that these lockdowns punished small businesses while allowing the big-box corporations to stay open and prosper, like Walmart and Home Depot. Meanwhile, your neighborhood corner stores, churches, bookstores, gun dealers, whatnot, are shut down, while booze and pot stores are deemed essential. That seems wrong to me. And I think a lot of this has been driven by a political agenda.

Maurice Jackson: Germane to equities, let’s shift the focus on a space that you and I love to speculate in. And those are resource stocks. Is this the right time to be in the space?

Mickey Fulp: Well, I think so. This is an opportune time to speculate in resource stocks. And we’ve seen, when things start to emerge from a collapse like thisand we saw it in 2008, and early 2009the first thing that goes up is gold. And if it progresses, then gold stocks follow quite soon after that.

Maurice Jackson: Do you favor the miners in the current environment, or junior miners?

Mickey Fulp: I don’t favor miners. I think mining’s a really tough business. So, my bailiwick is the junior explorers, oftentimes referred to as junior miners. But about one in 10 will ever mine anything. Most of them just mine the stock market. That said, certainly, the gold miners have done well and should continue to do very well, with high prices for gold and very low energy costs.

Even though oil has ralliedit’s still at $34 a barrel nowwe should also look at the juniors. The Toronto Venture Exchange index is up 60% from its low in mid-March. That’s phenomenal. Every day, I watch the value of my junior explorer portfolio increase day after day, and I think I was up 37% in April, and I expect to be up even more than that in a month.

Maurice Jackson: Are there any that have your attention at the moment, and why?

Mickey Fulp: Well, I’m looking at gold companies, gold explorers; I’m looking at copper explorers and developers. A company that I currently cover and covered since, well, actually for three years now, we picked it at $0.65. It closed on Friday at $1.90; it’s been as high as $3.14. It has catalysts coming. That’d be Trilogy Metals Inc. (TMQ:NYSE.MKT; TMQ:TSX).

I also picked up another copper company the other day that was at or near its four-year low. A lot of things have gone up, a lot of stocks have popped, especially in the gold explorer space, but there’s a few that haven’t, and there’s a few copper companies that haven’t.

So being a contrarian, I like to go in and look at stocks that have lagged, because I think what’s coming is going to be good for the resource sector, especially in gold and copper. So, be a contrarian, try to find things that are undervalued and buy them when they’re unloved and unknown, and unwanted, and undervalued.

Mickey Fulp: I am a very early shareholder of Hannan Metals; I participated in the pre-RTO [reverse takeover] financings. It’s an exploration play, going into the Amazon Basin in northeastern Peru. They’re looking for giant, sediment-hosted, copper deposits. It’s frontier, it’s grassroots, it’s early days, but being a very early-on shareholder of that company, I watched it progress from a failed zinc project in Ireland; once that was not going to make it, they quickly shifted focus to this copper play in Peru. And I remain a dedicated shareholder of that company.

Maurice Jackson: Germane to buying opportunities, let’s shift the focus now onto physical precious metals. Mickey, why do you own precious metals?

Mickey Fulp: Well, I own gold mainly, and it’s a hedge and insurance policy against financial mismanagement, which we’ve seen a lot of right now. And Pelosi wants to put another $2 or $3 trillion into that financial mismanagement. Geopolitical calamity is also a reason to own gold and economic collapse.

And so, I think, as I think you and I agree, gold is real money. Silver and platinum are superfluous holdings for me. I have some, but I have them because they make pretty coins and they’re fungible. And at some point, I fully expect to convert a bunch of my silver into gold when the ratio normalizes a bit.

Maurice Jackson: Which metals are you buying right now? And why?

Mickey Fulp: Yeah, well, the outlook for gold, of course, is bullish with all this money printing. And there are lots of reasons to think gold is going to go up. It’s consolidating right now in the low to mid-$1,700/ounce range.

Silver is very undervalued right now, with a gold-silver ratio still greater than 100. So, you can argue that silver is a very good buy right now, as is platinum compared to gold. . .the idea is that you buy what’s undervalued, and when ratios and valuations tend to normalize, and you sell your silver and platinum and turn it into gold.

For the life of me, I have no idea why anybody would be buying palladium. It’s not shiny and beautiful the way that platinum is. It’s not called white gold, which platinum jewelry is called white gold. And it’s completely overvalued. It went exponential. It’s come back. Right now, it’s high this year was $2,754/ounce, and as we speak today, it’s 1,920, but historically it trades at about a third of what platinum does. And now it’s trading for more than double what platinum does.

So it makes no sense for anybody to buy palladium. And because its prices increased so much back in the daysay a decade or so agothe Chinese, poor Chinese people, would buy it for jewelry because they couldn’t afford gold or platinum. And that’s not the case now. So only 5% of its demand is used for coinage and jewelry, as opposed to 40% for both platinum and silver.

Maurice Jackson: In closing, sir, what keeps you up at night that we don’t know about?

Mickey Fulp: Well, I’m a pretty private person. I’m not sure why I’d tell a bunch of people who I don’t know, something like that, Maurice.

Maurice Jackson: Mr. Fulp, last question: What did I forget to ask?

Mickey Fulp: I don’t rightly know; why don’t you think about it and then asked me next time, Maurice? I’m joking around with you here, but I would like to say, on Memorial Day today, let’s remember those who gave their lives defending the freedoms that the deep-state socio-fascists are now trying to take away from us.

Maurice Jackson: Mickey, for someone reading, where can they find your work?

Mickey Fulp: Twitter @mercenarygeo, with 51,200 followers, and my newsletter, Mercenary Geologist, with over 7,500 subscribers, and this interview will be up as soon as you release it to me, on my website and Twitter.

Maurice Jackson: And as a reminder, I’m a licensed representative for Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio from physical delivery, off-shore depositories and precious metal IRAs. Call me directly at (855) 505-1900, or you may e-mail [email protected].

And finally, please subscribe to provenandprobable.com, where we provide mining insights and bullion sales.

Mickey Fulp, the Mercenary Geologist, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Hannan Metals. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Hannan Metals. Proven and Probable disclosures are listed below. 2) Mickey Fulp: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Hannan Metals, Trilogy Metals. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Trilogy Metals. 3) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 4) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 5) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Steve Palmer, president and chief investment officer of AlphaNorth Asset Management, outlines why he believes Canadian companies on the TSX Venture Index remain good investments in a time of pandemic uncertainty.

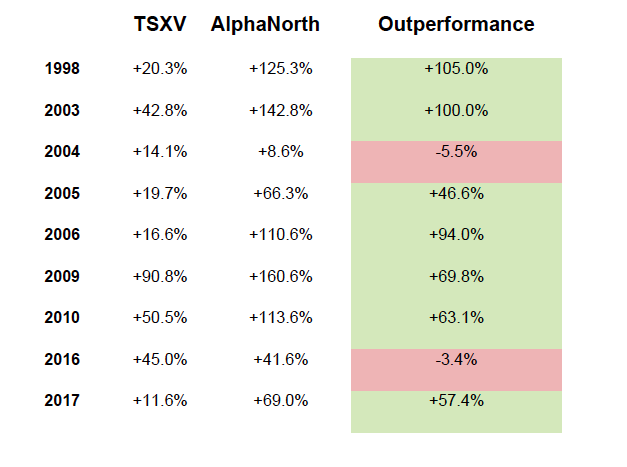

We believe that the COVID-19 lockdown has been a catalyst for the TSX Venture index (TSX.V) to outperform. After a decade of underperforming the major equity indices the TSX.V has led returns from the March equity market lows, gaining 58.9% as compared to 36.3% and 36.6% for the TSX Composite and S&P 500 indexes, respectively. This is likely to continue for reasons outlined in this report.

We do not often write special commentaries. However, when a situation becomes particularly compelling, we are prompted to provide a timely opinion, as we did in our special commentary in February 2016 titled, “Reasons to be Optimistic on Canadian Venture StocksWhat Is Recent Investor Sentiment Implying for Equity Markets?” This opinion piece was very timely and accurate, as the TSX.V was subsequently the best performing diversified equity index worldwide in 2016 increasing by 45% and 12% in 2017. The AlphaNorth Partners Fund, by comparison, returned 42% in 2016 and 69% in 2017.

The Impact of the COVID-19 Lockdown

As the fear regarding the COVID-19 pandemic spread in March, equity indices worldwide crashed. In only a few weeks indices erased substantial wealth. The S&P 500 index declined by 35.4% in just 23 trading days, from an all-time high on Feb. 19 to the low on March 23. Canada’s indices, the TSX and TSX.V, declined in tandem by 37.8% and 44.1%,respectively, over the same period. However, since bottoming in March, these indices have rebounded strongly. The rally is being led by the TSX.V as shown in the following chart.

Why Is COVID-19 a Catalyst for Canadian Small-Cap Outperformance?

In our view, it makes sense that after the initial scramble for cash, the market concluded that many of the companies that comprise the junior market are not as negatively impacted as the large caps. Small-cap companies can more readily adjust costs to survive the recession/depression that we are now in because of the government-imposed lockdowns. For example, one CEO we spoke to recently indicated that he has not been paid for several months. He and others on the management team have made this sacrifice so the company can survive and “get to the other side.” How many CEOs on the TSX Composite are willing to reduce their salary, let alone to zero? That is just not going to happen. These companies will go bankrupt before management in large-cap companies opt for reduced compensation.

Many of the companies in which we have invested have not been negatively impacted by the COVID-19 lockdown and some actually benefit from the situation. These companies are represented in biotech, junior resource (gold, silver, palladium, rare earth metals), e-gaming and technology (artificial intelligence [AI], software, hardware, security).

Many investors have invested in exchange-traded funds (ETFs) and bank-owned, large-cap mutual funds. which pretend to add value through largely investing in the same few stocks. The sector weightings for the TSX 60 index are indicated below as of April 30, 2020, with a brief outline of the challenges that these companies now face.

Financials (33%): The unemployment rate has spiked faster than ever before. Some surveys predict that there will soon be 25% unemployment. Generally, unemployed people do not buy houses, cars and other discretionary items. They redeem investments held at banks to pay bills. This causes default rates to increase. These things all negatively impact the outlook for banks. Recent bank earnings showed year over year average declines of 54%. Will the dividends be safe now that the payout ratios have increased materially?

Materials (13%): This sector is dominated by precious metal companies, which we believe will benefit from the current environment. Whether it is justified or not, an investor consensus that inflation is likely going to emerge as a result of the unprecedented government stimulus will be good for gold. There was strong performance in gold after the Financial Crisis. Gold has recently rallied strongly and we believe that we are in the early days of a similar move.

Energy (15%): Aside from the international price war for this sector, the COVID-19 lockdown will result in significantly reduced travel into the foreseeable future.

Industrials (11%): In this sector, several airlines will struggle not to go bankrupt in the current social distancing environment. Other constituents are closely tied to GDP [gross domestic product] growth and will also struggle.

Technology (9%): This sector is dominated by the 60% weighting in Shopify Inc. (SHOP:NYSE). The company will benefit from the current environment. However, the shares trades at an astounding price to earnings multiple of 1,174! The shares have recently vaulted past Royal Bank (RY:NYSE) to become Canada’s largest company. If history is any guide, this often does not end well; previous examples of new market darlings that have achieved this honor include Nortel Networks in 2000, which subsequently went bankrupt, and Valeant Pharmaceuticals, which remains down more than 90 %from its 2015 peak and short honor as Canada’s most valuable company. Research in Motion, now BlackBerry Ltd. (BB:NYSE), briefly achieved this title in 2007 before declining 96%. Further strong gains from this sector are unlikely.

Communications (7%): A recent Globe and Mail headline, “Telecom growth on hold as pandemic coos demand,” says it all. The telecommunications companies have steady operations, but it remains to be seen how much consumers and businesses will cut back on services. Revenue forecasts have been reduced due to the recession reflecting negative growth. These businesses already offer pricing pressure as a result of the commodity nature of their products.

Utilities (3%): Do not expect stellar returns from this sector, particularly if we enter a period of rising interest rates. These are utilities after all, offering lower risk business models. However, valuations are tied to fixed income returns, which are now close to zero. As interest rates rise, utilities will need to offer more attractive yields to compete for investor capital, thus share prices will be under pressure.

Consumer Staples (5%), Consumer Discretionary (4%) and Real Estate (0.3%): These sectors will likely have mixed results over the short to medium term. Generally, staples will do well, while discretionary spending will decline due to the recession and high unemployment. Overall, these sectors are too small to move the needle for the TSX overall return.

Healthcare (1%): Unfortunately, this is the smallest weighting and comprised of companies that we do not even believe qualify as healthcare: cannabis. We have been negative on the cannabis sector for some time and we have not been surprised to watch it blow up in grand fashion.

Other factors that have contributed positively to large-cap equity performance in recent years have been share buybacks. Many of these programs will now be on hold over the short to medium term.

COVID-19 Impact on AlphaNorth Partners Fund

Many of our investments in the Fund have not been negatively impacted from the COVID-19 pandemic. Several companies have benefited because of the situation. Although the COVID-19 lockdown has severely impacted many businesses, we are continuing to add opportunities which are minimally impacted or stand to benefit. Fortuitously, many of our investments prior to the crisis already fit this category, and after the initial undiscriminating sell-off, have rebounded strongly. We had minimal exposure to the Energy sector, which has suffered the most devastation. Our largest sector weighting has been Life Sciences, which overall has benefited during this period.

Current Positioning of the AlphaNorth Partners Fund

We have maintained a diversified portfolio with a focus on Life Sciences (ex-cannabis), Technology and Precious Metals. These sectors have been largely unaffected by the COVID-19 crisis and many companies have benefited from the current environment. We have committed to several private placements in the coming weeks which will add 5% to our precious metals weighting.

The Importance of Warrants

Unlike the majority of Canadian investors, particularly the institutions that have survived and participate in the small-cap sector, we are not warrant clippers. Our investment strategy is to maximize investment returns as opposed to minimizing risk. Where the majority of Canadian investors are quick to monetize the value of warrants, we are often are the last to exercise. Instead, we let our profits run if a company is continuing to execute, the valuation is reasonable and the technicals indicate continued strength. The majority of our warrant positions are acquired at no cost as part of private placements. Our current portfolio has approximately 55% warrant coverage.

We value warrants conservatively at intrinsic value. Unless warrants are “in the money,” they receive zero value. In previous bull markets our warrant portfolio has contributed significantly to returns. Investors get zero leverage from warrants investing in ETFs and minimal warrant exposure, if any, in mutual funds.

Conclusion and Outlook

We believe that large-cap equities have rebounded too strongly given the major headwinds facing the economy. It is likely that the sharp rebound in large-cap stocks in recent weeks is unjustified by fundamentals. There remains much uncertainty, and there is likely more bad news to come on the economy and corporate front. We believe that large-cap equities will retest the March 2020 lows. Once investors have more clarity in the coming months and the COVID-19 situation dissipates, large-cap equities will regain lost ground.

We believe that we have entered a period of Canadian small-cap outperformance. Canadian small-cap equities have taken over as the market leaders after a long period of underperformance. This is primarily a result of the numerous companies that are not significantly impacted by the COVID-19 lockdown, while the majority of large-cap companies face material challenges because of it. Years in which the TSX.V has outperformed, the AlphaNorth Partners Fund has been atop performing fund.

The following performance data is for years in which the Canadian small cap market returns were greater than 10%.*

Steve Palmer is a Founding Partner, President and Chief Investment Officer of AlphaNorth Asset Management and currently manages the award-winning AlphaNorth Partners Fund, AlphaNorth Growth Fund and AlphaNorth Resource Fund. Prior to founding AlphaNorth in 2007, Palmer was employed as Vice President at one of the world’s largest financial institutions, where he managed equity assets of approximately CA$350M. Palmer managed a pooled fund, which focused on Canadian small-capitalization companies, from its inception to August 2007, achieving returns of 35.8% annualized over a nine-year period, which ranked it No. 1 in performance by a major fund ranking service in its small-cap, pooled-fund category. Palmer earned a bachelor’s degree in economics from the University of Western Ontario and is a Chartered Financial Analyst.

Disclosure: 1) Statements and opinions expressed are the opinions of Steve Palmer/AlphaNorth and not of Streetwise Reports or its officers. Steve Palmer/AlphaNorth is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Steve Palmer/AlphaNorth was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. AlphaNorth disclosures are below. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

AlphaNorth disclosures: Data prior to 2009 used the BMO Small-Cap Index and institutional small-cap pooled fund managed by Steve Palmer and Joey Javier. 2009 and subsequent data uses TSX.V and AlphaNorth Partners Fund returns. The information contained in this document is not a solicitation to sell any investment products offered by AlphaNorth Asset Management. The information contained herein is for discussion purposes only. Please refer to the Offering Memorandum for complete details of any investment products offered by AlphaNorth Asset Management. There is no guarantee of performance and past performance is not indicative of future results. Returns are presented for Class A shares on an annualized basis except where noted and stated net of all fees. The inception date is December 1, 2007, for the fund. Returns prior to 2007 are based on growth of investment in institutional small cap pooled fund from inception August 1, 1998, to August 1, 2007, and growth of investment in AlphaNorth Partners Fund Inc. from inception December 1, 2007, to the current NAV.

The Research Brief is a short take about interesting academic work.

The big idea

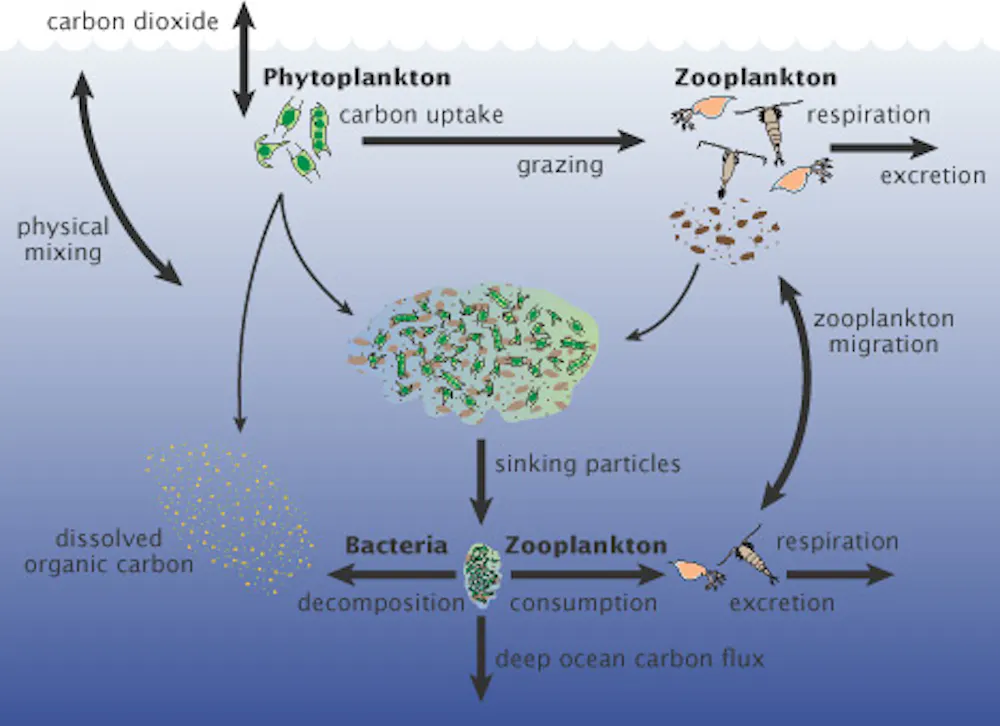

The ocean plays a major role in the global carbon cycle. The driving force comes from tiny plankton that produce organic carbon through photosynthesis, like plants on land.

When plankton die or are consumed, a set of processes known as the biological carbon pump carries sinking particles of carbon from the surface to the deep ocean in a process known as marine snowfall. Naturalist and writer Rachel Carson called it the “most stupendous snowfall on Earth.”

Some of this carbon is consumed by sea life, and a portion is chemically broken down. Much of it is carried to deep waters, where it can remain for hundreds to thousands of years. If the deep oceans didn’t store so much carbon, the Earth would be even warmer than it is today.

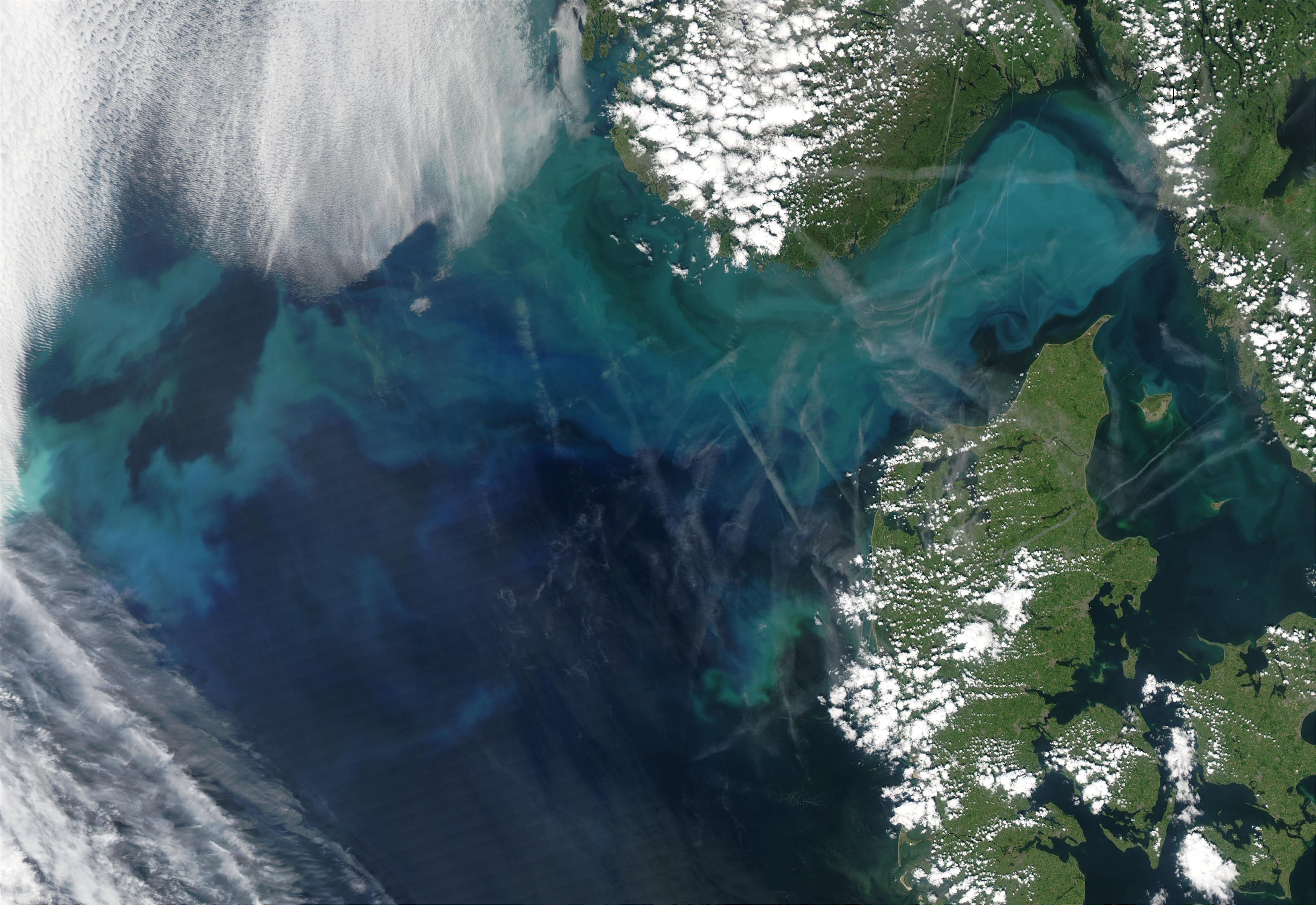

Ocean carbon storage is driven by phytoplankton blooms, like the turquoise swirls visible here in the North Sea and waters off Denmark. NASA

In a recent study, I worked with colleagues from the U.S., Australia and Canada to understand how efficiently the biological pump captures carbon as part of this marine snowfall. Past efforts to answer this question often measured marine snowfall at a set reference depth, such as 450 feet (150 meters). In contrast, we paid closer attention to the depth of something called the euphotic zone. This is the ocean layer close to the surface, where enough light penetrates for photosynthesis to happen.

We accounted more accurately for how deep the euphotic zone extends by using chlorophyll sensors, which indicate the presence of plankton. This approach revealed that the sunlit zone extends farther down in some regions of the ocean than in others. Taking this new information into account, we estimate that the biological pump carries twice as much heat-trapping carbon down from the surface ocean than previously thought.

A recent study shows that scientists have drastically underestimated how efficiently the ocean’s biological pump moves carbon from the surface to deep waters.

Why it matters

The biological pump phenomenon takes place over the entire ocean. That means that even small changes in its efficiency could significantly change atmospheric carbon dioxide levels and, as a result, global climate.

Moreover, light penetration varies regionally and seasonally throughout the oceans. It’s key to understand those differences so that ocean scientists can incorporate biological processes into better global climate models.

We also considered another ocean phenomenon that involves the largest animal migration on Earth. It’s called diel vertical migration, and happens around the globe. Every 24 hours, a massive wave of plankton and fish ascend from the twilight zone to feed at night at the surface, then descend back to darker waters in daytime.

Scientists think this process moves a lot of carbon from the surface to deeper waters. Our study suggests that the amount of carbon carried by these daily migrations must also be measured at the same boundary where light disappears, so that scientists can directly compare the marine snowfall to the active migration.

Phytoplankton in the ocean consume carbon dioxide as they photosynthesize. When they are eaten or decompose, some of the carbon they contain falls into the ocean depths via a process called the biological pump. U.S. JGOFS

How we did it

For this study, we reviewed previous research on the biological pump. To compare results, we first determined how deep the sunlit region extended. We found this boundary at the depth where it became too dark to see any more chlorophyll pigments, which mark the presence of marine phytoplankton layers. Across the studies, that depth varied between 100 and 550 feet (30 to 170 meters).

Next, we estimated how much organic carbon sank into deeper waters in these studies, and measured how much remained in particles that sank another 330 feet (100 meters) deeper into the twilight zone. Many creatures live and feed in these deep waters, including fish, squid, worms and jellyfish. Some of them consume sinking carbon particles, reducing the amount of marine snowfall.

Comparing these two numbers gave us an estimate of how efficiently the biological pump was moving carbon into deep waters. The studies that we reviewed produced a wide range of values. Overall, we calculated that the biological pump was capturing twice as much carbon as previous studies that did not take into account the wide range of light penetration depths. Regional patterns also changed: Areas with shallow light penetration accounted for a higher percentage of carbon removal than areas with deeper light penetration.

The ocean twilight zone may hold more life than all of Earth’s fisheries combined, and up to 1 million undiscovered species.

What still isn’t known

Our study reveals that scientists need to use using a more systematic approach to defining the ocean’s vertical boundaries for organic carbon production and loss. This finding is timely, because the international oceanographic community is calling for more and better studies of the biological carbon pump and the ocean twilight zone.

The twilight zone could be profoundly affected if nations seek to develop new midwater fisheries, mine the seafloor for minerals or use it as a dumping ground for waste. Scientists are forming a collaborative effort called the Joint Exploration of the Twilight Zone Ocean Network, or JETZON, to set research priorities, promote new technologies and better coordinate twilight zone studies.

To compare these studies, researchers need a common set of metrics. For the biological carbon pump, we need to better understand how big this flow of carbon is, and how efficiently it is transported into deeper water for long-term storage. These processes will affect how Earth responds to rising greenhouse gas emissions and the warming they cause.

In a move to aid the eurozone, the European Central Bank (ECB) has boosted its pandemic emergency purchase program (PEPP) by a whopping €600 billion to €1.35 trillion.

This monetary policy bazooka comes on top of a €750 billion proposal by the European Commission, adding to a range of strategies in Europe and around the globe to combating the coronavirus menace. With the eurozone economy projected to contract -8.7% this year, every single support offered by the ECB and government will certainly shape the outlook over the coming months.

Why it matters?

Quantitative easing is a monetary policy tool that central banks use to inject money directly into the economy.

It involves large-scale purchases of government debt in the form of bonds which essentially pushes down the interest rates offered on loans. Lower interest rates make it cheaper for households and businesses to borrow which could stimulate consumption.

The million dollar question is whether the €600 billion increase to the PEPP and extension to June 2021 will achieve this goal.

What could go wrong?

Well…it is important to keep in mind that the coronavirus pandemic is a health crisis that may leave a strong psychological impact on consumer behaviour and business sentiment.

It may take more than negative interest rates, QE bazookas and fiscal timebombs to mend confidence back to pre-coronavirus levels.

Another theme to keep a close watch on is inflation. When the markets become too flooded with cash, it can lead to rising consumer prices. However, this could be a good thing for Europe which currently suffers from anaemic inflation levels.

How does this impact the Euro?

Since the idea behind QE is to inject money into markets, the increase in supply should weaken the currency overtime.

However, this may end up boosting attraction towards the Euro instead if lower interest rates stimulate consumption and revive economic growth.

EURUSD Technical outlook

The EURUSD jumped over 150 pips following the ECB’s decision to throw more firepower at COVID-19.

Looking at the technical picture, prices are heavily bullish on the daily charts as there have been consistently higher highs and higher lows. A solid daily close above 1.1360 may open the doors towards 1.1450 in the medium to longer term. Lagging technical indicators like the Moving Average Convergence Divergence (MACD) and 20 Simple Moving Average (SMA) both point to further upside.

Should 1.1360 prove to be reliable resistance, the EURUSD could sink back towards 1.1280.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Of course, there’s been the big collapse in oil prices, plus — just like many other global stock indexes — Russian stocks are well off their highs.

That’s quite in contrast to 2019, when the RTSI index, a U.S. dollar-based index of 50 Russian companies, climbed 29%.

Shortly after registering that performance, Elliott Wave International’s January Global Market Perspective, a monthly publication which covers 40-plus worldwide markets, showed this chart and said:

Complacency toward financial risk stands at unprecedented extremes.

Our global analyst’s comment suggested that a change of trend was afoot, given that extremes in financial markets are akin to a rubber band that is stretched to the breaking point.

Well, here’s an update on the RTSI from the just-published June Global Market Perspective. An EWI global analyst notes:

The RTSI index … did worse than Europe’s broader indexes, losing more than half of its value from February to March. The stunning crash was followed by [a] rally that has since retraced about 50% of the decline.

In addition to stock prices being well off their highs, Russia’s economic output will contract at 6% this year and the jobless number is expected to double.

Plus, in April, the government projected that the budget deficit will hit 4% of GDP.

As the June Global Market Perspective also notes:

Russia’s last financial crisis in 2014-15 also came on the heels of a decline in oil prices, and the crisis culminated on December 15, 2014, when the ruble suddenly plummeted against the euro and dollar. … Russia is entering its current crisis from a much weaker financial position.

So, does this mean that the rally in Russian stocks is nearly over, or might the RTSI index climb the proverbial “wall of worry”?

Well, a March 27 Barron’s headline suggests that investors will eventually be rewarded:

Russia’s Stocks Are a Buy Only for Very Patient Investors

Elliott Wave International’s global analysts provide their own perspective on the big financial picture, yet they are also focused on what’s next for Russia financially and economically — as well as many other worldwide markets.

You see, EWI’s top 5 global experts share their latest forecasts for cryptocurrencies, crude oil, interest rates, deflation, and the futures of the European Union.

The result is a 5-video series (plus, two quick reads) — all in just 13 minutes.

And — you get it free with a fast Club EWI signup. Club EWI membership is also free.

This article was syndicated by Elliott Wave International and was originally published under the headline Russia: How Financial “Complacency” Morphed into “Crisis”. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

The European Central Bank (ECB) almost doubled the size of its pandemic emergency purchase program (PEPP) and extended it by a further six months in response to what it said was an “abrupt drop in economic activity” that is expected to lead to an economic contraction of 8.7 percent in 2020. The central bank for the 19 European countries that share the euro currency boosted the size of its PEPP program by 600 billion euros to 1.350 billion and will now be purchasing assets, such as government or corporate bonds, until at least to the end of June 2021 or “until it judges that the coronavirus crises phase is over.” The massive boost to the ECB’s asset purchases, also known as quantitative easing, comes as the bank’s staff sharply raised its estimate for the drop in economic output and inflation in response to the global measures taken to limit the spread of the Covid-19 pandemic. “Incoming information confirms that the euro area economy is experiencing an unprecedented contraction,” ECB President Christine Lagarde said. While recent data and surveys show some signs of a bottoming-out of the sharp drop in economic activity, Lagarde said the “improvement has so far been tepid compared with the speed at which the indicators plummeted in the preceding two months. The economy of the euro area already shrank 3.8 percent in the first quarter of this year from the fourth quarter of 2019 and containment measures were only in place from mid-March. The latest update of its economic forecasts sees “growth declining at an unprecedented pace in the second quarter of this year, before rebounding again in the second half, crucially helped by the sizable support from fiscal and monetary policy,” Lagarde said. ECB staff expects the euro area economy to shrink 8.7 percent this year, up from the March forecast of growth of 0.8 percent and 2019’s growth of 1.2 percent. Inflation is seen of only 0.3 percent, down from 1.2 percent in 2019 and the March forecast of 1.1 percent, and well below the ECB’s target of close to, but below 2.0 percent. In May inflation is estimated to plunge to only 0.1 percent from 0.3 percent in April. Boosted by its own massive stimulus and other European government measures to support economic activity, such as the German-French proposal for a 500 billion euro virus fund and European Council’s 540 billion euro safety net, the euro area economy is seen bouncing back. Gross domestic product in 2021 is forecast to expand by 5.2 percent and then another 3.3 percent in 2022 while inflation is seen rising to 0.8 percent in 2021 and 1.3 percent in 2022. Given the uncertainty around the length of the pandemic and thus the economic recovery, the ECB also published two alternative projections. In addition to expanding the size and length of its PEPP program, the ECB will also reinvest maturing principal payments from securities purchased until at least the end of 2022. The ECB’s stimulus measures come as its interest rates are already at rock bottom, with the benchmark refinancing rate at 0.0 percent and the lending rate at 0.25 percent since March 2016 and the deposit rate at minus 0.50 percent since September 2019. Lagarde confirmed the ECB’s guidance that it expects to maintain rates “at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.” While the ECB’s PEPP program initially was launched in March, it is also engaged in further stimulus measures, such as its asset purchase program (APP), which will continue purchasing bonds and other securities at a monthly pace of 20 billion euros together with an additional envelope of purchases of 120 billion until the end of this year. The ECB confirmed that it expects to continue with the monthly purchases under APP “for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.” The expansion of PEPP follows the ECB’s cut to the interest rates on its targeted longer-term refinancing operations (TLTRO III) in April when it also launched another program to boost liquidity in the euro area financial system known as PELTRO, or non-targeted pandemic emergency longer-term refinancing operations. In April the ECB had also said it was fully prepared to raise the size of PEPP. The European Central Bank issued the following statement with its policy decisions and an introductory statement by its president, Christine Lagarde:

“At today’s meeting the Governing Council of the ECB took the following monetary policy decisions:

(1) The envelope for the pandemic emergency purchase programme (PEPP) will be increased by €600 billion to a total of €1,350 billion. In response to the pandemic-related downward revision to inflation over the projection horizon, the PEPP expansion will further ease the general monetary policy stance, supporting funding conditions in the real economy, especially for businesses and households. The purchases will continue to be conducted in a flexible manner over time, across asset classes and among jurisdictions. This allows the Governing Council to effectively stave off risks to the smooth transmission of monetary policy.

(2) The horizon for net purchases under the PEPP will be extended to at least the end of June 2021. In any case, the Governing Council will conduct net asset purchases under the PEPP until it judges thatthe coronavirus crisis phase is over.

(3) The maturing principal payments from securities purchased under the PEPP will be reinvested until at least the end of 2022. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary stance.

(4) Net purchases under the asset purchase programme (APP) will continue at a monthly pace of €20 billion, together with the purchases under the additional €120 billion temporary envelope until the end of the year. The Governing Council continues to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.

(5) Reinvestments of the principal payments from maturing securities purchased under the APP will continue, in full, for an extended period of time past the date when the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

(6) The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

The Governing Council continues to stand ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner, in line with its commitment to symmetry.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.’

INTRODUCTORY STATEMENT:

“Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council, which was also attended by the Commission Executive Vice-President, Mr Dombrovskis.

Incoming information confirms that the euro area economy is experiencing an unprecedented contraction. There has been an abrupt drop in economic activity as a result of the coronavirus (COVID-19) pandemic and the measures to contain it. Severe job and income losses and exceptionally elevated uncertainty about the economic outlook have led to a significant fall in consumer spending and investment. While survey data and real-time indicators for economic activity have shown some signs of a bottoming-out alongside the gradual easing of the containment measures, the improvement has so far been tepid compared with the speed at which the indicators plummeted in the preceding two months. The June Eurosystem staff macroeconomic projections see growth declining at an unprecedented pace in the second quarter of this year, before rebounding again in the second half, crucially helped by the sizeable support from fiscal and monetary policy. Nonetheless, the projections entail a substantial downward revision to both the level of economic activity and the inflation outlook over the whole projection horizon, though the baseline is surrounded by an exceptional degree of uncertainty. While headline inflation is suppressed by lower energy prices, price pressures are expected to remain subdued on account of the sharp decline in real GDP and the associated significant increase in economic slack.

In line with its mandate, the Governing Council is determined to ensure the necessary degree of monetary accommodation and a smooth transmission of monetary policy across sectors and countries. Accordingly, we decided on a set of monetary policy measures to support the economy during its gradual reopening and to safeguard medium-term price stability.

First, the Governing Council decided to increase the envelope for the pandemic emergency purchase programme (PEPP) by €600 billion to a total of €1,350 billion. In response to the pandemic-related downward revision to inflation over the projection horizon, the PEPP expansion will further ease the general monetary policy stance, supporting funding conditions in the real economy, especially for businesses and households. The purchases will continue to be conducted in a flexible manner over time, across asset classes and among jurisdictions. This allows us to effectively stave off risks to the smooth transmission of monetary policy.

Second, we decided to extend the horizon for net purchases under the PEPP to at least the end of June 2021. In any case, we will conduct net asset purchases under the PEPP until the Governing Council judges thatthe coronavirus crisis phase is over.

Third, the Governing Council decided to reinvest the maturing principal payments from securities purchased under the PEPP until at least the end of 2022. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

Fourth, net purchases under our asset purchase programme (APP) will continue at a monthly pace of €20 billion, together with the purchases under the additional €120 billion temporary envelope until the end of the year. We continue to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of our policy rates, and to end shortly before we start raising the key ECB interest rates.

Fifth, we intend to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when we start raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Sixth, we decided to keep the key ECB interest rates unchanged. We expect them to remain at their present or lower levels until we have seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within our projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

Together with the substantial monetary policy stimulus already in place, today’s decisions will support liquidity and funding conditions in the economy, help to sustain the flow of credit to households and firms, and contribute to maintaining favourable financing conditions for all sectors and jurisdictions, in order to underpin the recovery of the economy from the coronavirus fallout. At the same time, in the current rapidly evolving economic environment, the Governing Council remains fully committed to doing everything necessary within its mandate to support all citizens of the euro area through this extremely challenging time. This applies first and foremost to our role in ensuring that our monetary policy is transmitted to all parts of the economy and to all jurisdictions in the pursuit of our price stability mandate. The Governing Council, therefore, continues to stand ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner, in line with its commitment to symmetry.

Let me now explain our assessment in greater detail, starting with the economic analysis. The latest economic indicators and survey results confirm a sharp contraction of the euro area economy and rapidly deteriorating labour market conditions. The coronavirus pandemic and the necessary containment measures have severely affected both the manufacturing and services sectors, taking a toll on the productive capacity of the euro area economy and on domestic demand. In the first quarter of 2020, when containment measures were only in place from mid-March in most countries, euro area real GDP decreased by 3.8%, quarter on quarter. Information from surveys, high-frequency indicators and incoming hard data all point to a further significant contraction of real GDP in the second quarter. Most recent indicators suggest some bottoming-out of the downturn in May as parts of the economy gradually reopen. Accordingly, euro area activity is expected to rebound in the third quarter as the containment measures are eased further, supported by favourable financing conditions, an expansionary fiscal stance and a resumption in global activity, although the overall speed and scale of the rebound remains highly uncertain.

This assessment is also broadly reflected in the June 2020 Eurosystem staff macroeconomic projections for the euro area. In the baseline scenario of the projections, annual real GDP is expected to fall by 8.7% in 2020 and to rebound by 5.2% in 2021 and by 3.3% in 2022. Compared with the March 2020 ECB staff macroeconomic projections, the outlook for real GDP growth has been revised substantially downwards by 9.5percentage points in 2020 and revised upwards by 3.9percentage points in 2021 and 1.9percentage points in 2022.

Given the exceptional uncertainty currently surrounding the outlook, the projections also include two alternative scenarios, which we will publish on our website following this press conference. In general, the extent of the contraction and the recovery will depend crucially on the duration and the effectiveness of the containment measures, the success of policies to mitigate the adverse impact on incomes and employment, and the extent to which supply capacity and domestic demand are permanently affected. Overall, the Governing Council sees the balance of risks around the baseline projection to the downside.

According to Eurostat’s flash estimate, euro area annual HICP inflation decreased to 0.1% in May, down from 0.3% in April, mainly on account of lower energy price inflation. On the basis of current and futures prices for oil, headline inflation is likely to decline somewhat further over the coming months and to remain subdued until the end of the year. Over the medium term, weaker demand will put downward pressure on inflation, which will be only partially offset by upward pressures related to supply constraints. Market-based indicators of longer-term inflation expectations have remained at depressed levels. While survey-based indicators of inflation expectations have declined over the short and medium term, longer-term expectations have been less affected.

This assessment is also reflected in the June 2020 Eurosystem staff macroeconomic projections for the euro area, which foresee annual HICP inflation in the baseline scenario at 0.3% in 2020, 0.8% in 2021 and 1.3% in 2022. Compared with the March 2020 ECB staff macroeconomic projections, the outlook for HICP inflation has been revised downwards by 0.8percentage points in 2020, 0.6percentage points in 2021 and 0.3percentage points in 2022.

Turning to the monetary analysis, broad money (M3) growth increased to 8.3% in April 2020, from 7.5% in March. Strong money growth reflects bank credit creation, which is driven to a large extent by the acute liquidity needs in the economy. Moreover, high economic uncertainty is triggering a shift towards money holdings for precautionary reasons. In this environment, the narrow monetary aggregate M1, encompassing the most liquid forms of money, continues to be the main contributor to broad money growth.

Developments in loans to the private sector continued to be shaped by the impact of the coronavirus on economic activity. The annual growth rate of loans to non-financial corporations rose further to 6.6% in April 2020, up from 5.5% in March, reflecting firms’ need to finance their ongoing expenditures and working capital in the context of rapidly declining revenues. At the same time, the annual growth rate of loans to households decreased to 3.0% in April, from 3.4% in March, amid consumption constraints due to the containment measures, declining confidence and a deteriorating labour market.

Our policy measures, in particular the very favourable terms for our targeted longer-term refinancing operations (TLTRO III), should encourage banks to extend loans to all private sector entities. Together with the measures adopted by national governments and European institutions, they support ongoing access to financing, including for those most affected by the ramifications of the coronavirus pandemic.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed that an ample degree of monetary accommodation is necessary for the robust convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding fiscal policies, an ambitious and coordinated fiscal stance remains critical, in view of the sharp contraction in the euro area economy. Measures taken should as much as possible be targeted and temporary in nature in response to the pandemic emergency. The three safety nets endorsed by the European Council for workers, businesses and sovereigns, amounting to a package worth €540 billion, provide important funding support in this context. At the same time, the Governing Council urges further strong and timely efforts to prepare and support the recovery. We therefore strongly welcome the European Commission’s proposal for a recovery plan dedicated to supporting the regions and sectors most severely hit by the pandemic, to strengthening the Single Market and to building a lasting and prosperous recovery.”

Waste heat is all around you. On a small scale, if your phone or laptop feels warm, that’s because some of the energy powering the device is being transformed into unwanted heat.

On a larger scale, electric grids, such as high power lines, lose over 5% of their energy in the process of transmission. In an electric power industry that generated more than US$400 billion in 2018, that’s a tremendous amount of wasted money.

Globally, the computer systems of Google, Microsoft, Facebook and others require enormous amounts of energy to power massive cloud servers and data centers. Even more energy, to power water and air cooling systems, is required to offset the heat generated by these computers.

Where does this wasted heat come from? Electrons. These elementary particles of an atom move around and interact with other electrons and atoms. Because they have an electric charge, as they move through a material – like metals, which can easily conduct electricity – they scatter off other atoms and generate heat.

Superconductors are materials that address this problem by allowing energy to flow efficiently through them without generating unwanted heat. They have great potential and many cost-effective applications. They operate magnetically levitated trains, generate magnetic fields for MRI machines and recently have been used to build quantum computers, though a fully operating one does not yet exist.

But superconductors have an essential problem when it comes to other practical applications: They operate at ultra-low temperatures. There are no room-temperature superconductors. That “room-temperature” part is what scientists have been working on for more than a century. Billions of dollars have funded research to solve this problem. Scientists around the world, including me, are trying to understand the physics of superconductors and how they can be enhanced.

Understanding the mechanism

A superconductor is a material, such as a pure metal like aluminum or lead, that when cooled to ultra-low temperatures allows electricity to move through it with absolutely zero resistance. How a material becomes a superconductor at the microscopic level is not a simple question. It took the scientific community 45 years to understand and formulate a successful theory of superconductivity in 1956.

While physicists researched an understanding of the mechanisms of superconductivity, chemists mixed different elements, such as the rare metal niobium and tin, and tried recipes guided by other experiments to discover new and stronger superconductors. There was progress, but mostly incremental.

Simply put, superconductivity occurs when two electrons bind together at low temperatures. They form the building block of superconductors, the Cooper pair. Elementary physics and chemistry tell us that electrons repel each other. This holds true even for a potential superconductor like lead when it is above a certain temperature.

When the temperature falls to a certain point, though, the electrons become more amenable to pairing up. Instead of one electron opposing the other, a kind of “glue” emerges to hold them together.

Keeping matter cool