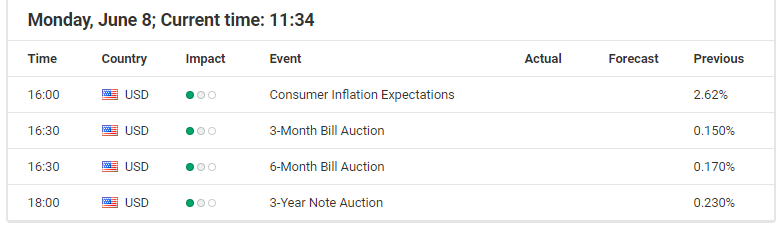

This week – Jun 8 through June 13 – central banks from eight countries or jurisdictions are scheduled to decide on monetary policy: Kazakhstan, United States, Serbia, Ukraine, Moldova, Uganda, Peru and Uzbekistan. Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.

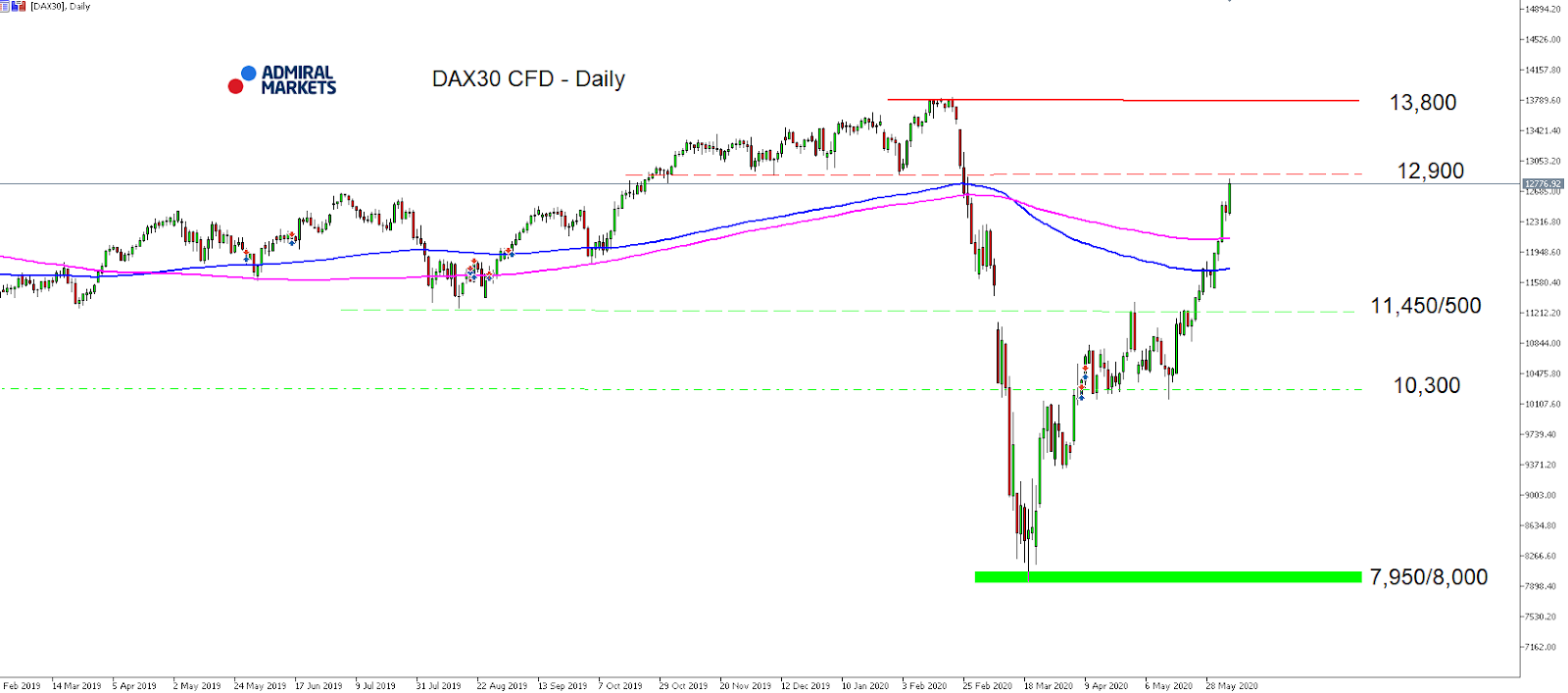

The DAX went parabolic over the last week of trading by gaining further bullish momentum after the German index recaptured the SMA(200) around 12,000/050 points.

At first glance, it seemed quite optimistic to get to see a walk-through on the upside with a push as high as the region around the January lows around 12,850/900 points.

This came, despite social unrest in the US, and a very dark fundamental picture for the US economy as well as the European economy. The combination of an EU commission proposal of a 750 Billion-Euro fiscal stimulus package with 500 billion Euro in grants and 250 billion in loans for European Union regions as a first step toward a transfer union, the German governing coalition agreeing on an additional €130bn economic stimulus package which will see e.g. value-added tax rate cut from 19% to 16% and an ECB which boosted the size of its PEPP program on Thursday to 1.35 trillion Euros with being set to run through at least the end of June 2021, the DAX30 took off on the upside.

While the stock market has obviously completely decoupled from the real economy, given the German index’ with valuation at a Price-Earnings-Ratio of around 20, its highest level since the New Economy at 2000, the bullish performance is also a warning sign for ‘bears’.

Whatever driver the DAX30 currently finds, it is a clear bullish one, even though the technical mode on the upside seems very extended.

In fact, the first clear signs of a bearish divergence in the RSI(14) on H1 point to at least a short-term correction, a push back below 12,000 points activate a first target around 11,800/850 points and becomes likely with a break below 12,300/350 points.

Above 12,300/350 points the focus and target on the upside remains on the January lows around 12,850/900 points.

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Hourly chart (between May 19, 2020, to June 5, 2020). Accessed: June 5, 2020, at 10:00pm GMT

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Daily chart (between February 20, 2019, to June 5, 2020). Accessed: June 5, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of the DAX30 CFD increased by 9.56%, in 2016, it increased by 6.87%, in 2017, it increased by 12.51%, in 2018, it fell by 18.26%, in 2019, it increased by 26.44% meaning that after five years, it was up by 34.2%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks

– The disastrous failure of the Trump administration to contain COVID-19 will result in catastrophic 2nd quarter data. As a result, Trump is risking his re-election on domestic unrest, fatal geopolitics and a global depression.

The cold reality is that the Trump administration learned about the virus already on January 3, when CDC Director Dr. Robert R. Redfield informed Secretary of Health Alex Azar that China had discovered a new coronavirus. Yet no mobilization was initiated until toward late March (see my report here):

Indeed, the Trump White House missed three opportunities to contain the virus outbreak; in January (between CDC alert and WHO’s international emergency), the 1st quarter (between the WHO emergency and the pandemic alert) and the 2nd quarter (since social distancing began 6-8 weeks late and inadequately).

Instead of virus mobilization in early January, a long debate began within the White House over “what to tell to the American public,” while Azar and Secretary of State Mike Pompeo began repeated attacks against China. The consequent economic carnage is evident in the 2nd quarter free-fall (Table).

Table Human Costs and Economic Damage of the Pandemic

Human

Costs

Q4 2019 (#)

Q1 2020

(#)

Q2 2020

(#)

Cumulative Cases

China:

US

1

0

China:

US:

82,500

140,600

China:

US:

85,000

2.3 million+

Economic Damage

Q4 2019 (%)

Q1 2020

(%)

Q2 2020

(%)

GDP

Growth

China:

US:

6.0%

2.1%

China:

US:

-6.8%

-4.8%

China:

US:

3% to 4%

-38% to -45%

Source: WHO, IMF, Goldman Sachs, Morgan Stanley, Difference Group.

At the end of June, the US is likely to have more than 2.3 million cumulative cases and over 130,000 deaths. In the 1st quarter, US annual GDP growth contracted (-4.8%) but the real carnage will ensue with the 2nd quarter plunge (-38% to -45%), as I projected in April and major US investment banks have warned. The Atlanta Fed’s model expects a -52% plunge, however.

To survive its pandemic and economic failures, the Trump White House has initiated a series of measures in a hybrid war against China. In the absence of timely countervailing actions, these measures have potential to undermine global economic prospects in the short term and the promise of the Asian Century over time.

Southeast Asia will not remain immune to such headwinds.

From Chinagate to hybrid China Wars

As the Trump White House has targeted China as a its re-election scapegoat, the early victims include US-Sino high-level bilateral dialogue, trade and investment relations, US treasuries, military relations and destabilization in East Asia.

High-Level Dialogues. Undermining decades of US-Sino bilateral progress, President Trump has let US-Sino high-level economic, law enforcement and cultural dialogues freeze since fall 2017; the diplomatic and security dialogue since fall 2018.

Trade. Trade tensions are re-escalating. After the Phase-I deal, China is obliged to buy $200 billion in additional US imports over two years on top of pre-trade war purchase levels. The truce would require 18% annual import growth from the US, which is challenging to China amid Trump protectionism and dire global prospects.

Investment. Before the trade wars, US investment to China averaged $15 billion per year, whereas Chinese investment in the US soared to $45 billion. US investment to China has persisted, but Chinese investment in the US has been forced to plunge to $5 billion. Thanks to Trump decoupling, over a decade of progress has been reversed. Nevertheless, seven of ten US companies do not plan to leave China.

Treasuries. For years, Beijing invested much of its foreign exchange reserves in US assets, particularly US Treasury securities. In another low-probability but high-impact re-election scenario, Republicans are threatening Beijing with unilateral $1.1 trillion debt cancellation, while Democrats hope to de-list Chinese companies from US markets. As a result, Beijing is diversifying investments away from the US, while pumping over $1.4 trillion into the tech sector over to 2025.

Military Relations. Despite political differences, US-China military exchanges used to feature high-level visits, exchanges between defense officials, and functional interactions. According to Pentagon, these engagements have fallen by two-thirds in the Trump era, while bilateral tensions are rapidly escalating in South and East China Sea. Whether accidental or provoked, a conflict is a matter of time.

Special Administrative Regions. Destabilization efforts in Chinese mainland’s proximity have escalated dramatically since 2017.

Unlike previous administrations, the White House, in cooperation with Taiwan’s president Tsai Ing-wen, seeks to undermine decades of “One China” policies. If the past “strategic ambiguity” gives way to force, the geopolitical impact could destabilize East Asia.

Hong Kong. According to Washington, “pro-democracy forces” are threatened in Hong Kong. According to Beijing, cooperation between the White House, Congress, and Tsai government is fueled by a quest for “color revolution.” As Senate Intelligence Committee chair, radical-right Sen. Marco Rubio (R-FL) hopes to exploit the Hong Kong Human Rights and Democracy Actfor regime change in China as he has in Iran, Russia, Venezuela and elsewhere.

Financier of the Trump campaign and Republican conservatives, billionaire casino magnate Sheldon Adelson allowed the CIA to use of his Macau properties for US espionage in the early 2010s. More recently, his Sands Corp. played a critical role in an apparent spying operation targeting Julian Assange, when the CIA came under the control of Mike Pompeo, another Adelson ally.

Before Trump’s Hong Kong declaration,US lawmaker Scott Perry (R-PA), a retired Pennsylvania Army National Guard Brigadier General, has introduced a bill to recognize Tibet as a sovereign country.

From pandemic geopolitics to US debt crisis

In 2003, the Bush administration began its Iraq War under a pretext, presumably to achieve a domino-effect democracy across the Middle East. The consequent nightmare led to still another ‘forever war’ in the region, in which the costs soared to $3 trillion, as estimated by economist Joseph Stiglitz.

Barely two decades later, the Trump administration has initiated what in Beijing looks like a nascent hybrid war to win re-election. The economic costs of complacency, which are misplaced on China and WHO, are estimated at $9 trillion; that’s three times the costs of the Iraq War.

These tragic losses could pale with the imminent new policy mistakes. In what I have termed a Great Power Conflicts scenario, lingering pandemic risks would result in intense trade and technology wars, “hot” geopolitical conflicts and a long, multi-year global depression. This is the current path of the Trump White House, which is predicated on leveraging US economy to the hilt.

US debt has soared to $26 trillion that puts US debt-to-GDP ratio to 120% (at par with that of Italy amid its debt crisis in 2011-12), which the White House and the Fed will soon have to further increase.

Due to the central role of US in the world economy, such economic leverage – coupled with the human costs of the pandemic and deadly geopolitics – is pushing global prospects toward the edge of global depression.

About the Author:

Dr. Steinbock is the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

This is a short version of a commentary published by China-US Focus on June 5, 2020.

And just like that, all seems right in global stock markets.

The record-breaking gains in Friday’s US jobs report have cheered risk assets at the start of the new trading week. Asian equities are pushing higher while US futures are adding to last week’s gains. The Dow Jones appears on course to complete a ‘V’ shape recovery, despite having ventured into overbought territory.

The 2.5 million jobs added in the US last month appears to justify the tremendous gains in equity markets since March, much to the chagrin of economists who had forecasted a drop of 7.5 million jobs for the non-farm payrolls report that was released on June 5. The unemployment rate, which was expected to hit 19 percent in May, actually eased to 13.3 percent from April’s 14.7 percent.

All of a sudden, the market narrative is less concerned about whether the worst of the economic damage is over. Instead, it has pivoted to how quickly the global economy can recover from Covid-19. The broad-based bounce in the jobs market speaks to the resilience of the US economy’s primary growth engine, as well as the efficacy of fiscal and monetary stimulus measures.

The sooner-than-expected recovery also bodes well for the global economy. The post-lockdown return of American workers should drive a rebound in consumption, which has been the US economy’s primary growth engine before the pandemic. As demand levels are restored, suppliers and exporters around the world can hope to resume offering their services and goods to the world’s largest economy, while improving job prospects and economic activity in their respective home countries along the way.

Considering the rosier outlook that markets are indulging in, no surprise that Gold has tumbled and fallen below its 50-day simple moving average while its upward momentum has diminished substantially.

Despite markets acting as if the recession is firmly in the rearview mirror, the road ahead could prove to be a real slog, barring more positive shockers like the ones we witnessed this past Friday. About 21.5 million Americans are still unemployed, while the 13.3 percent unemployment rate still is the highest such reading since the 1940s. It might take many more months, and perhaps even more support measures, to restore the US workforce to pre-pandemic levels. In the interim, global investors will be hoping that there isn’t a second wave of lockdowns in the world’s largest economy.

Yet, Friday’s surprise has once again pointed to the tremendous unpredictability over the investment landscape. The clear winners are the equity bulls who had priced in a “V” shaped recovery, and they are far closer now to being proven right, judging by the latest US non-farm payrolls report. And their bets appear to have been vindicated by the stunning US jobs report.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Global equities are mixed currently after a rally Friday following surprise US jobs report. Unexpected drop in US unemployment rate boosted investors’ risk appetite ahead of the Federal Reserve meeting this week.

Forex news

Currency Pair

Change

EUR USD

-0.32%

GBP USD

+3.31%

USD JPY

-0.11%

The Dollar strengthening has paused today . The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, gained 0.2% Friday as Bureau of Labor Statistics reported US economy regained 2.5 million jobs in May and the unemployment rate fell to 13.3%. GBP/USD continued climbing Friday while EUR/USD fell with the dynamics intact for both pairs currently. AUD/USD and USD/JPY continued climbing on Friday with Australian dollar still higher against the greenback currently. Yen is higher against the dollar currently after Japanese government revised the Q1 GDP upward to 2.2% annualized rate of decline from 3.4% drop in initial estimate.

Stock Market news

Indices

Change

Dow Jones Index

+2.21%

US equity markets are mixed today after ending sharply higher on Friday. Stock indexes rally in US was led by cyclical shares: the three main US stock indexes recorded daily gains ranging from 2.1% to 3.2% while booking weekly gains ranging from 3.3% to 6.8%. European stock indexes are rising currently after jump on Friday. Asian indexes are rising today led by Japan’s Nikkei index which jumped 1.4%.

Commodity Market news

Commodities

Change

Brent Crude Oil

+1.2%

WTI Crude

+1.23%

Brent is edging higher today. Oil prices ended sharply higher last session on reports major oil producers were convening Saturday to discuss plans for extended productions cuts. The US oil benchmark West Texas Intermediate (WTI) futures ended solidly higher Friday: July WTI rose 5.7% and is higher currently. August Brent crude closed 5.8% higher at $42.30 a barrel on Friday. The group of major oil producers known as OPEC+ agreed on Saturday to extend the output curb deal to withdraw almost 10% of global supplies from the market by a third month to end of July.

Gold Market News

Metals

Change

Gold

+0.73%

Gold prices are retracing higher today. August gold fell 2.7% to $1680.40 an ounce on Friday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

The most recent U.S. jobs report, which he believes is bound for revision, has Michael Ballanger musing on how economic policies are reflectedor distortedin the precious metals markets.

I was sitting in my den looking out over the swamperlake tonight when it appeared as though something was flailing around near the shoreline. So I threw on my deck shoes and went for a stroll down to the water to see what all the commotion was about. Now, you must understand that I have been around the Kawartha Lakes since my late teens, having fished for pickerel alongside the Buckhorn Dam in the summer of 1970. Back in the day, the pickerel were so plentiful that we would throw two or three of these two- to three-pound beauties into the live well and then play “catch and release” for the remainder of the day, because you were taught at a very young age that you only take what you need as food and you release anything else so they could grow and make more baby pickerel. At the root of the practice was one remarkably simple fact: Pickerel are the finest-eating freshwater fish in the world and you want to protect them.

So here I am, looking past the weeds and algae in the shallows of western Lake Scugog and what comes lumbering past is the most gawd-ugly creature that I have ever observedan enormous Asian carp that had to be ten pounds. Before I could say “invasive species,” two more appeared, equally as detestable and even larger than the leviathan that first surfaced, after which the fish began to perform a kind of floundering, splashing, mating ritual where they rotated their bodies over and around the female in a manner most foreign to anything I have observed in six decades of angling in the Ontario waterways.

It was at this point in time that I came to an epiphany, the point of the experience that at once provided me with an idea for a topic for tonight’s missive but, more importantly, the sudden realization that any of the natural species that have inhabited these lakes (such as my beloved pickerel) have zero chance of surviving in waters dominated by Asian carp. The sad part is that there are no natural predators to keep carp populations in check, so how the Ministry of Fisheries and Wildlife intends to solve this unnatural distortion is beyond me.

That, my friends is not only sad, but also symptomatic of even greater unnatural distortions in the global capital markets, thanks largely to the insanity of the central banking cartel.

The chart you see here is an illustration of three events: the first is the REPO operations launched in September 2019, which forced massive liquidity into the markets to prevent certain select hedge funds from blowing up, and which put a bid into stocks and accelerated into 2020. The second is the media-fueled panic that miraculously grew from a violent strain of influenza into a global pandemic, taking the S&P down 36% in thirty-four days. The final event is what we are living through today: a money-printing convulsion by central banks the magnitude of which makes the Great Financial Bailout of 20092011 look like a bake sale raffle.

I was trying to explain this distortion to a group of younger investors earlier in the week, and it was like trying to explain to Phil Kessel why backchecking is necessary, which means it was a) impossible and b) pointless. The only thing that matters to this new generation of investors is that “the Fed’s got our backs,” and that “cash is trash.” It matters not that there is a massive distortion between fundamentals and valuation, the direct result of the implementation of “moral hazard” as a policy tool.

What is important is that rising stock prices will make the average American consumer feel better about spending the money they no longer have. The Federal Reserve has pulled this trick at every sniff of a market correction since 1987, and have now completely engrained the notion that stocks are a “riskless venture,” a veritable ATM of government largesse and charity that will never fail.

David Rosenberg is a really smart guy who has been warning investors of a dangerous overvaluation of stocks on the basis that only a “V-shaped” recovery can have any chance of justifying these prices. I argue that it simply does not matter what the economy does, because the deflationary forces that should be knocking stocks back down are actually deflating the purchasing power of the U.S. currency unit.

As more and more fiat gets squeezed out of the pork machine by the Fed’s orgasmic display of debt monetization and futures market intervention, the more units of currency are going to be required to replace a common share of stock, any stock. So, when the left-leaning media starts whining about all of this Fed “liquidity” going to supporting the stock market, as opposed to starving citizens, they fail to learn from history that the number one priority of the Federal Reserve bank is to protect the member banks, and that means shareholders of the member banks. It is this unnatural distortion that allows an elite sector of the U.S. economy to indiscriminately manufacture “money” while being bestowed the ordained duty of choosing which citizens (or groups of citizens) are entitled to that taxpayer-provided charity.

The olfactory glands of the precious metals’ markets have detected a repulsive order emanating from the Eccles Building and have responded accordingly, with a 13.41% advance year-to-date versus a 3.67% decline in the S&P 500. Mind you, from the March lows, stocks have obeyed their banking masters and responded to the liquidity explosion, while gold has been harnessed to a trading range in the USD $1,700s per ounce, although it looks as though a more serious correction is possible, especially if it fails to hold $1,700 in the seasonally soft MayJuly period.

If I had to look to one glaring distortion, either natural or unnatural, that is staring us all in the face, it is that gold is not already through US$2,000/ounce, and that silver isn’t trading above 1/70th of the price of gold. Instead, thanks to countless blatant and criminal interventions, silver trades at 1/95th the price of gold, and is still over $2.00, beneath the Sept. 2019 high, at US$19.75, while gold drifts aimlessly, as the U.S. equity markets are valued at 147% market cap to GDP [gross domestic product] ratio.

The Friday jobs report came in with a massive “beat” (“better than expected”), with the economy adding 2.5 million jobs in May versus the expected minus 8 million. Just as the ringing of a bell by Dr. Pavlov caused his dog to salivate, the gold and silver markets felt obligated to crash 2.0% and 2.44% respectively.

Notwithstanding almost certain revisions to the Friday number, the Bureau of Labor Statistics (BLS) report showing a 13.3% unemployment rate is around 3.3% higher than the peak number during the 2008 Great Recession/Financial Crisis/Bailout, which came in at 10%.

Dow futures are called up 665 points, and the number of grinning CNBC guest commentators makes me want to lob my tackle box at the screen, because these cackling jabberwockies of self-professed financial acumen are the same clowns that were begging to have them “close the stock exchanges.” To see these Cheshire Cat faces all beaming with inferences of “I told ya so” is about as disingenuous as it gets.

I have been urging caution in the precious metal markets since April, and while my exit was premature, preserving subscriber capital has outweighed any need to give back the gains we have enjoyed this year thus far. Now that gold has knifed down to US$1,690/ounce, perhaps the miners will experience a deeper correction that will allow us to acquire our favorite names at prices closer to their 50-dma [daily moving average] levels.

I continue to hold a larger-than-normal cash balance (over 70%) and am overweight one junior gold developer (Getchell Gold Corp. [GTCH:CSE]), and I look to add into the typical seasonal weakness that occurs in the JuneJuly doldrums. Aftermath Silver Ltd. (AAG:TSX.V), in the CA$0.30/share (or below) range, is also on my radar.

In closing, to those of you that wrote off the bullion bank behemoths as being “cooked” in their management of the Crimex gold market, once again, they have successfully capped price during the period of the greatest currency debasement in U.S. history while levitating stocks back into bull market territory. The truly great “unnatural distortion” is the movie being played right before your eyes; if you believe for one New York minute that today’s jobs number was anything but fiction, I have some lakefront in the Scugog swamp I will sell you.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Aftermath Silver and Getchell Gold. My company has a financial relationship with the following companies referred to in this article: Aftermath Silver and Getchell Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aftermath Silver and Getchell Gold, companies mentioned in this article.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Switzerland’s consumer prices remained unchanged in May: the consumer price index remained unchanged over month in May after 0.4% decline in April, when an 0.1% increase was expected. This is bullish for USDCHF.

The Dollar flickered to life on Friday afternoon after Nonfarm Payrolls (NFP) increased by a solid 2.5 million in May, smashing the market expectations of -8 million.

The unemployment rate also offered by a pleasant surprise by dropping -13.3% compared the -20% forecast while average hourly earnings came in at -1% month-on-month, below the 1% estimate. Overall, the jobs report is certainly encouraging and suggests that the largest economy in the world is trying to get back on its feet. However, this optimism may be squashed by over the coming weeks if economic data continues to disappoint. Is the worst of the coronavirus choas behind us? Time will tell.

All in all, this surprisingly solid jobs report may lower the chances of the Federal Reserve taking any further action. The absence of looser monetary policy could instil Dollar bulls with fresh inspiration, especially if macroeconomic conditions shows signs of stabilizing.

Looking at the charts, the Dollar Index has the potential to rebound towards 97.80 in the week ahead as sentiment towards the US economy improves. However, the technical outlook remains in favour of bears as prices remain below the 20 Simple Moving Average while the Moving Average Convergence Divergence points to further downside. Should 97.80 prove to be reliable resistance, prices may end up sink back towards 96.25.

But if the fundamental support king Dollar, a move back towards 97.80 could open the gates to 98.50.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Hydrogen has long been touted as the future for passenger cars. The hydrogen fuel cell electric vehicle (FCEV), which simply runs on pressurised hydrogen from a fuelling station, produces zero carbon emissions from its exhaust. It can be filled as quickly as a fossil-fuel equivalent and offers a similar driving distance to petrol. It has some heavyweight backing, with Toyota for instance launching the second-generation Mirai later in 2020.

The Canadian Hydrogen and Fuel Cell Association recently produced a report extolling hydrogen vehicles. Among other points, it said that the carbon footprint is an order of magnitude better than electric vehicles: 2.7g of carbon dioxide per kilometre compared to 20.9g.

All the same, I think hydrogen fuel cells are a flawed concept. I do think hydrogen will play a significant role in achieving net zero carbon emissions by replacing natural gas in industrial and domestic heating. But I struggle to see how hydrogen can compete with electric vehicles, and this view has been reinforced by two recent pronouncements

The bulk of the car, bus and light-truck market looks set to adopt [battery electric technology], which are a cheaper solution than fuel cells.

Volkswagen, meanwhile, made a statement comparing the energy efficiency of the technologies. “The conclusion is clear” said the company. “In the case of the passenger car, everything speaks in favour of the battery and practically nothing speaks in favour of hydrogen.”

Hydrogen’s efficiency problem

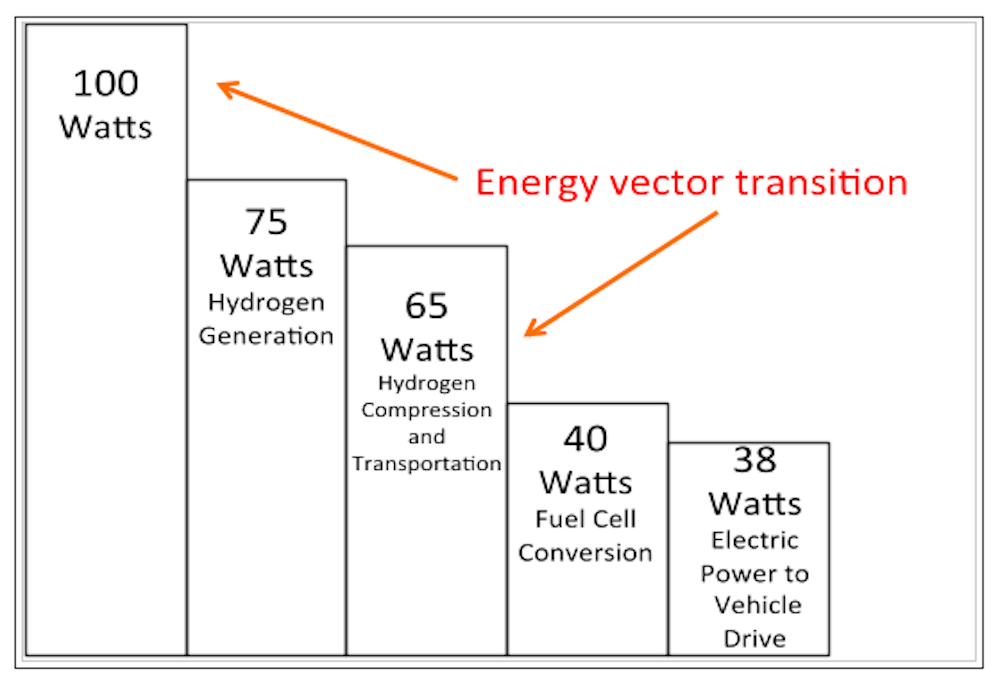

The reason why hydrogen is inefficient is because the energy must move from wire to gas to wire in order to power a car. This is sometimes called the energy vector transition.

Let’s take 100 watts of electricity produced by a renewable source such as a wind turbine. To power an FCEV, that energy has to be converted into hydrogen, possibly by passing it through water (the electrolysis process). This is around 75% energy-efficient, so around one-quarter of the electricity is automatically lost.

The hydrogen produced has to be compressed, chilled and transported to the hydrogen station, a process that is around 90% efficient. Once inside the vehicle, the hydrogen needs converted into electricity, which is 60% efficient. Finally the electricity used in the motor to move the vehicle is is around 95% efficient. Put together, only 38% of the original electricity – 38 watts out of 100 – are used.

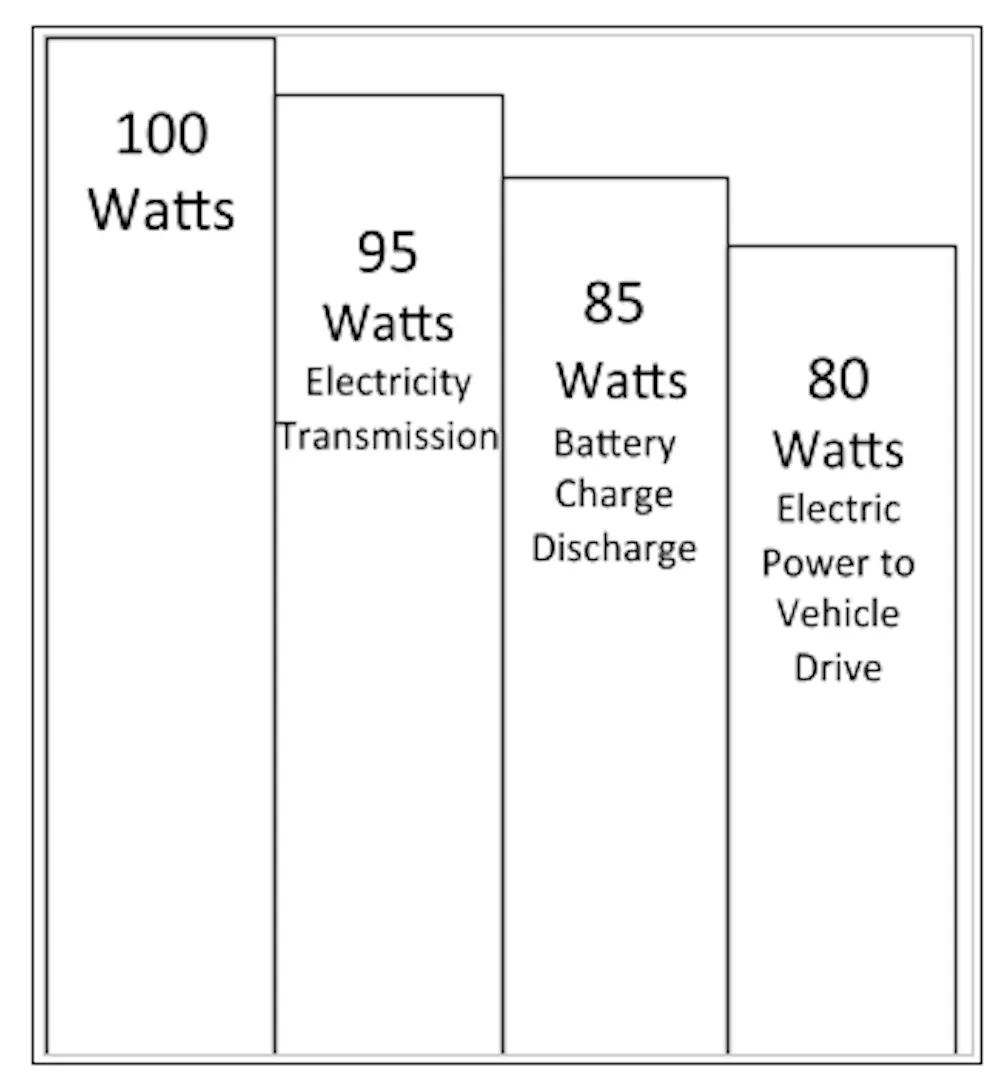

With electric vehicles, the energy runs on wires all the way from the source to the car. The same 100 watts of power from the same turbine loses about 5% of efficiency in this journey through the grid (in the case of hydrogen, I’m assuming the conversion takes place onsite at the wind farm).

Energy efficiency in electric vehicles.

You lose a further 10% of energy from charging and discharging the lithium-ion battery, plus another 5% from using the electricity to make the vehicle move. So you are down to 80 watts – as shown in the figure opposite.

In other words, the hydrogen fuel cell requires double the amount of energy. To quote BMW: “The overall efficiency in the power-to-vehicle-drive energy chain is therefore only half the level of [an electric vehicle].”

Swap shops

There are around 5 million electric vehicles on the roads, and sales have been rising strongly. This is at best only around 0.5% of the global total, though still in a different league to hydrogen, which had achieved around 7,500 car sales worldwide by the end of 2019.

Hydrogen still has very few refuelling stations and building them is hardly going to be a priority during the coronavirus pandemic, yet enthusiasts for the longer term point to several benefits over electric vehicles: drivers can refuel much more quickly and drive much further per “tank”. Like me, many people remain reluctant to buy an electric car for these reasons.

China, with electric vehicle sales of more than one million a year, is demonstrating how these issues can be addressed. The infrastructure is being built for owners to be able to drive into forecourts and swap batteries quickly. NIO, the Shanghai-based car manufacturer, claims a three-minute swap time at these stations.

China is planning to build a large number of them. BJEV, the electric-car subsidiary of motor manufacturer BAIC, is investing €1.3 billion (£1.2 billion) to build 3,000 battery charging stations across the country in the next couple of years.

Not only is this an answer to the “range anxiety” of prospective electric car owners, it also addresses their high cost. Batteries make up about 25% of the average sale price of electric vehicles, which is still some way higher than petrol or diesel equivalents.

By using the swap concept, the battery could be rented, with part of the swap cost being a fee for rental. That would reduce the purchase cost and incentivise public uptake. The swap batteries could also be charged using surplus renewable electricity – a huge environmental positive.

Admittedly, this concept would require a degree of standardisation in battery technology that may not be to the liking of European car manufacturers. The fact that battery technology could soon make it possible to power cars for a million miles might make the business model more attractive.

It may not be workable with heavier vehicles such as vans or trucks, since they need very big batteries. Here, hydrogen may indeed come out on top – as BloombergNEF predicted in its recent report.

Finally a word on the claims on carbon emissions from that Canadian Hydrogen and Fuel Cell Association report I mentioned earlier. I checked the source of the statistics, which revealed they were comparing hydrogen made from purely renwewable electricity with electric vehicles powered by electricity from fossil fuels.

If both were charged using renewable electricity, the carbon footprint would be similar. The original report was funded by industry consortium H2 Mobility, so it’s a good example of the need to be careful with information in this area.

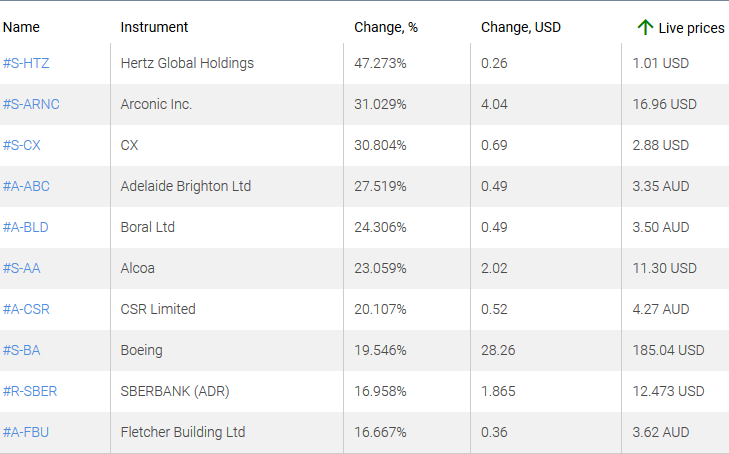

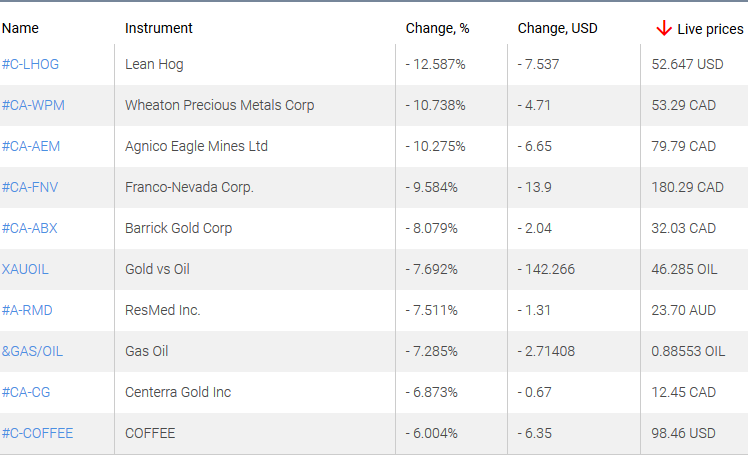

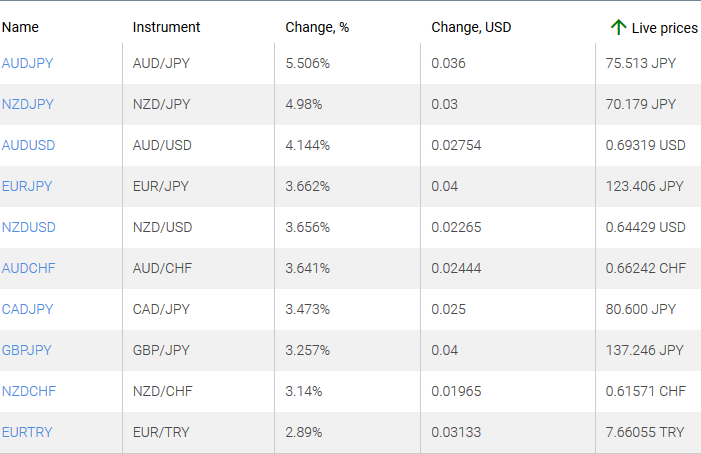

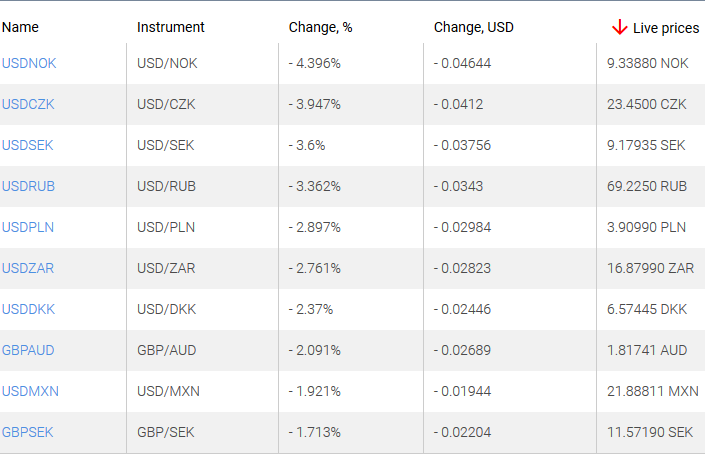

In the past seven days, the world markets have been in turmoil, with the United States dollar falling along with the gold quotations.Typically, the value of these assets moves in different directions, as investors view the US currency as an alternative to precious metals. Accordingly, this time the stocks of the Canadian gold mining company and currency pairs based on the weakened dollar became the Top Losers. American pork has fallen in price amid the worsening US-Chinese trade war, since China is its major buyer.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.