The EUR/USD currency pair continues to consolidate. There is no defined trend. Investors assess the results of the Fed meeting. The regulator does not plan to raise interest rates, at least until the end of 2022. The Central Bank intends to continue to support the national economy, which has been suffered significantly by the COVID-19 pandemic. The Fed forecasts a 6.5% reduction in the country’s GDP this year. At the moment, the key range is 1.1320-1.1400. Today, we expect important economic releases from the US. Positions should be opened from key levels.

The Economic News Feed for 2020.06.11:

– Initial jobless claims in the US at 15:30 (GMT+3:00);

– US producer price index at 15:30 (GMT+3:00).

Indicators do not give accurate signals: the price is testing 50 MA.

The MACD histogram is near the 0 mark.

Stochastic Oscillator is in the neutral zone, the %K line has crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.1320, 1.1250, 1.1195

Resistance levels: 1.1400, 1.1450, 1.1500

If the price fixes above the round level of 1.1400, further growth of EUR/USD quotes is expected. The movement is tending to 1.1440-1.1460.

An alternative could be a decrease in the EUR/USD currency pair to 1.1270-1.1240.

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.27259

Open: 1.27450

% chg. over the last day: +0.13

Day’s range: 1.26510 – 1.27545

52 wk range: 1.1466 – 1.3516

GBP/USD quotes have become stable after prolonged growth. At the moment, the technical pattern is ambiguous. Financial market participants assess the Fed meeting. The key support and resistance levels are 1.2640 and 1.2730, respectively. Correction of the trading instrument is possible in the near future. We recommend opening positions from key levels.

The news feed on the UK economy is calm.

Indicators do not give accurate signals: the price has fixed between 50 MA and 100 MA.

The MACD histogram has moved into the negative zone, which indicates the development of the correction movement.

Stochastic Oscillator is near the oversold zone, the %K line has crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.2640, 1.2585, 1.2500

Resistance levels: 1.2730, 1.2800

If the price fixes above 1.2730, GBP/USD purchases should be considered. The movement is tending to 1.2800-1.2830.

An alternative could be a decrease in the GBP/USD currency pair to 1.2580-1.2550.

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.34166

Open: 1.34115

% chg. over the last day: -0.01

Day’s range: 1.33973 – 1.34984

52 wk range: 1.2949 – 1.4668

The loonie is being traded in a flat. There is no defined trend. At the moment, USD/CAD quotes are testing the “mirror” resistance of 1.3490. The 1.3425 mark is the nearest support. The USD/CAD currency pair is tending to recover after a prolonged fall. We recommend paying attention to the dynamics of oil quotes. Positions should be opened from key levels.

Today, the publication of important economic releases from Canada is not expected.

Indicators do not give accurate signals: the price has crossed 100 MA.

The MACD histogram has moved into the positive zone, which indicates the development of bullish sentiment.

Stochastic Oscillator is in the overbought zone, the %K line has crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.3425, 1.3360, 1.3300

Resistance levels: 1.3490, 1.3570

If the price fixes above 1.3490, USD/CAD quotes are expected to correct. The movement is tending to 1.3550-1.3580.

An alternative could be a decrease in the USD/CAD currency pair to 1.3370-1.3340.

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 107.727

Open: 107.087

% chg. over the last day: -0.58

Day’s range: 106.896 – 107.235

52 wk range: 101.19 – 112.41

The USD/JPY currency pair continues to show a steady downtrend. The trading instrument has updated local lows again. USD/JPY quotes have found support at the level of 106.90. The 107.25 mark is the nearest resistance. The further growth of the yen against the greenback is possible. We recommend paying attention to economic reports from the US. Positions should be opened from key levels.

The news feed on Japan’s economy is calm.

Indicators signal the power of sellers: the price has fixed below 50 MA and 100 MA.

The MACD histogram is in the negative zone, indicating the bearish sentiment.

Stochastic Oscillator is in the neutral zone, the %K line is below the %D line, which gives a signal to sell USD/JPY.

Trading recommendations

Support levels: 106.90, 106.50

Resistance levels: 107.25, 107.65, 107.90

If the price fixes below 106.90, a further drop in USD/JPY quotes is expected. The movement is tending to 106.50-106.30.

An alternative could be the growth of the USD/JPY currency pair to 107.60-107.80.

By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

For the past several weeks, we have been arguing that the performance of risk assets across the world are in total disconnect with economic and corporate fundamentals.

The enormous addition of money supply through fiscal and monetary authorities has been the key driver for stock markets and in the US has seen the S&P 500 recover all its losses for the year and the Nasdaq Composite reaching a new record high. After all, the Federal Reserve has doubled its balance sheet to $7.2 trillion from $3.7 trillion and the administration may still issue new fiscal measures after their initial $3 trillion package.

The scale of those policies in fighting economic depression has translated into a remarkable recovery in financial assets, as the Fed committed to supporting not only blue-chip corporates but also those below investment grade. Hence the risk of insolvency has dropped significantly and investors do not seem worried about the near-term future. Surprisingly, that is also the case with bankrupt companies. Retail stock traders have been piling into stocks like Hertz and JC Penney despite these firms going through bankruptcy proceedings. I don’t think we have ever seen market behaviour like this in recent history.

The Fed is now committed to keeping interest rates near zero until at least the end of 2022 and using all its tools to support the economy. This could translate into further speculative bets and push the rally in equities and corporate debt higher. However, without real economic recovery the market will have to deal with a more significant challenge, which is debt insolvency. That’s why the disconnect between asset performance and economic fundamentals cannot run forever and investors will need to become more rational with their investment approach.

News of a second wave of coronavirus cases has begun to emerge in the US after the reopening of numerous states. While it might take several weeks to know if this is a broader problem, infection counts will again become a key barometer of risk that cannot be ignored. Another steep rise in virus cases will end up delaying the economic recovery further and lead to a rethinking of how to be positioned for a more depressed outlook.

Overall, I think the rally in equities has become overstretched and I wouldn’t be surprised to see a return of volatility with the market correcting to the downside.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Lower rainfall in Ivory Coast bullish for #C-COCOA

Lower than usual rainfall in Ivory Coast last week highlighted need for more rain to boost the crop. Ivory Coast is the world’s top cocoa producer. The International Cocoa Organization (ICCO) cut its forecast for global production by 74,000 tons to 4.75 million in its latest quarterly update on May 29. It forecast a global cocoa deficit of 80,000 tons in the 2019/20 season that runs from October to September. The estimate is slightly below its previous projection of 85,000 tons. ICCO forecast production in Ivory Coast to reach 2.15 million tons in 2019/20, down from a previous projection of 2.18 million. Data showed rainfall in both western and eastern regions of Ivory Coast were below the average last week. Lower rainfall in top cocoa producer country is bullish for cocoa price.

There is a cloud of wariness hanging over global equity markets today, after Fed officials forecasted no interest rate hike until at least 2022, perhaps slightly denting some of the optimism over a rapid recovery in the US economy. Asian stocks and US futures are lower, after the S&P 500 and Dow Jones index declined by 0.5 and one percent respectively.

Federal Reserve Chairman Jerome Powell, as expected, stuck to his message that the central bank will keep rolling out support measures until the American job market has recovered sufficiently. Powell also said that the Fed is “not even thinking about thinking about raising rates”. Despite the profit-taking seen overnight, equity bulls should be able to draw plenty of comfort from the Fed’s reassurance that its support measures will be around for as long as needed. Such an environment, coupled with the calls for more fiscal stimulus, should create conducive conditions for stocks to reach greater heights in the interim.

With firming expectations over lower-for-longer US interest rates, no surprise then that the Dollar index (DXY) is now testing the 96.0 support level to trade around its weakest levels since March.

The weaker Dollar and the Fed’s dour outlook combined to send Gold surging past the $1730. Gold bulls have been seemingly relentless, bringing Bullion prices back from sub-$1700 territory to notch a gain of nearly three percent so far this week.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Equity markets are retreating currently with US data expected to yet again show over million more Americans sought unemployment benefits the last week while new applications declined. Stocks fell yesterday on the Fed projection the US economy would shrink 6.5% in 2020 while Powell said the economic recovery will be “a long road.”

Forex news

Currency Pair

Change

EUR USD

+0.24%

GBP USD

+3.3%

USD JPY

-0.11%

The Dollar strengthening has resumed today ahead of a Labor Department report expected to show over 44 million Americans likely sought unemployment benefits over the last twelve weeks. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, lost 0.3% Wednesday as Fed chair Powell said interest rates would stay at near zero until 2022 while asset purchases continue, and US consumer price index fell 0.1% over month in May. EUR/USD and GBP/USD continued climbing yesterday but both pairs are down currently. USD/JPY continued falling yesterday while AUD/USD reversed up with both pairs lower currently.

Stock Market news

Indices

Change

Dow Jones Index

-1.53%

Nikkei Index

-1.71%

Hang Seng Index

-2.01%

Australian Stock Index

-3.01%

Futures on three main US stock indexes are sharply down after a mixed trading on Wednesday. Stock indexes in US ended mostly lower on Wednesday while technology stocks as Treasury Secretary Mnuchin told the Senate Small Business and Entrepreneurship Committee that more fiscal stimulus may be needed. The three main US stock indexes recorded returns ranging from -1.0% to +0.7%. European stock indexes are down currently following a two-session-in-a-row retreat Wednesday led by travel and leisure shares. Asian indexes are falling today led by Australia’s All Ordinaries ASX 200 .

Commodity Market news

Commodities

Change

WTI Crude

-2.09%

Brent is edging lower today. Prices rose Wednesday despite the US Energy Information Administration report that US crude oil inventories rose 5.7 million barrels last week after two consecutive weekly declines. The US oil benchmark West Texas Intermediate (WTI) futures rose: July WTI added 1.7% but is falling currently. August Brent crude closed 1.3% higher at $41.73 a barrel on Wednesday.

Gold Market News

Metals

Change

Gold

-0.12%

Gold prices are retracing higher today. August gold lost 0.7% to $1720.70 an ounce on Wednesday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Money manager Adrian Day reviews the prospects of two of his favorite resource companies and comments briefly on the pullback in gold prices.

Following the strong rally in gold and gold stocks since the March low, we expect a pullback over coming weeks. It is already underway. We do not expect it to be particularly long or deep, and will present opportunities to buy. For now, however, patience is the best course.

Altius Minerals Corp. (ALS:TSX.V, 10.44) reported royalty revenue down on a year ago, with thermal coal and iron ore down while potash was up. Overall, COVID-related shutdowns also contributed to lower revenues. For the quarter, revenue was $16.3 million, down from $21.9 million. The company has withdrawn its full-year guidance because of the shutdowns, with analysts looking for around $65 million in revenue this year (down from $78 million for 2019).

One major negative this quarter was the bankruptcy of Alderon Iron Ore Corp. (IRON:TSX), in which Altius held equity and debt. It owned the Kami iron ore deposit, which has been seized by its major creditor. Altius took a write-off of $0.08 per share, and wrote down its debt to CA$1 million. The royalty on the project remains, however.

The company has a deep pipeline of projects, some in development and others very early stage. But it said it was not seeing many opportunities in the current environment. Balance sheets at base metals companies were not as stretched as they had been, while in the current environment, companies wanting or needing to do a royalty would prefer to do it on any gold by-product rather than on the base metals.

New projects coming on stream Altius will experience sharply falling revenues from the 777 Mine in 2022, ahead of mine closure; this was previously one of its largest earners. It has four projects in the development phase that are scheduled to replace this revenue.

Most important is the Gunnison copper project, in which Altius has both equity and a royalty; it was expected to produce its first copper this quarter but commissioning is currently suspended. Starting small, the operator, Excelsior Mining Corp. (MIN:TSX; EXMGF:OTCQB), plans to expand production from the initial 25 Mlb/year up to 125 Mlb/year over the next seven years.

Other near-term growth will come from the underground expansion of the Voisey’s Bay project, in which Altius has an effective 0.3% royalty. This expansion will extend the mine life to 2034. Mining at Voisey’s Bay is also suspended. Both these projects will resume shortly, it is expected.

Major new division in renewables, generating revenue In addition, Altius has recently made large investments in renewable projects, totaling about CA$100 million, including:

· Last year, a $30 million investment, to be paid over three years, in Texas-based wind and solar energy concern Tri Global Energy LLC; to date, three royalties have come from this investment.

· In March, a CA$47 million investment in Apex Clean Energy for future royalties on North American wind and solar projects in development.

Altius’ renewal energy unit already has a management team in place. The plan is to raise additional equity from a major investor by the end of the year and then spin it out as a separate public company, perhaps as early as Q1/2021. Multiples on stand-alone renewal companies are about twice what Altius is receiving in the market, so that should boost Altius’ stock price, as well as provide ongoing revenues. The expectation is that Altius will be receiving full royalty revenue on these investments by the end of 2023.

Strong balance sheet with several potential revenue sources Currently, Altius has $32 million in cash and net debt of CA$122 million. It also owns a very liquid $50 million in Labrador Iron Ore Royalty Corp. (LIF.UN:TSX) shares, as well as a portfolio of junior resource companies, currently valued at CA$34 million, with the write-off of Alderon offset by generally improving prices. This consists for the most part companies with which Altius has joint ventures, or has royalties on a property owned by the companies. It has done a very good job of managing its junior equity portfolio, generating almost CA$1 million from sales at the end of 2019, for example.

There are future sources of revenue outside of the royalties. Major holder and famed Canadian investor Prem Watsa is expected to exercise his warrants in the company by the end of 2022, helping to pay off its debt by mid-2023. There is a partially undrawn line of credit for major new investments. And there is a potential payoff from ongoing litigation against Alberta in a “takings” lawsuit over its coal royalties, but it is not expecting a resolution until the end of 2022. General and administrative (G&A) expenses are low, at CA$6 million a year, of which about $1.5 million is for the renewable energy business, which will go away for Altius when the renewables unit is spun out.

Core holding in resource sector Altius remains one of our favorite resource companies and a core holding: disciplined and innovative management, a good balance sheet, and diversified assets and deep pipeline. The stock is now back at its February highs, and given our concern about a pullback in the resource sector, we would hold and wait for better prices to buy. If you do not own it already, however, it is good value and can be bought as a long-term holding.

Midland Moves Ahead on Many Fronts

Midland Exploration Inc. (MD:TSX.V, 0.85) continues to move ahead on its existing projects, as well as generating new projects. Last month, it generated over 170 claims in the northern Abitibi region, along the Casa Berardi zone, adding to other claims acquired in recent months along the Detour trend, near to new discoveries by other companies, including the Area 51 discovery of Wallbridge Mining Co. Ltd. (WM:TSX), and in James Bay. Most of this ground has had minimal, if any, exploration, and Midland will likely undertake initial work before readying properties for joint venture partners.

Exploring its projects and seeking partners The provincial government in Quebec last month announced companies could resume exploration, and Midland is planning extensive work at several of its properties. These include a new drill campaign now underway by Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE) on the Cadillac joint venture; and on two 100% projects, its large Mythril project, and Vortex, which saw some very exciting results initially. Midland regained the property from partner Soquem Inc., whose mandate does not include gold, in exchange for regional alliance in the north.

After large spending programs at Mythril, Midland is returning to its prospect-generator roots, seeking more partners for many of its properties. But it will also continue its own exploration on 100%-owned properties. Last week, it commenced exploration at two properties close to Wallbridge’s recent discoveries (Area 51 and Reaper) on the Detour Belt. With recent property acquisitions, Midland has several properties along the belt, strategically located. We would expect some drilling this summer.

The company has a strong balance sheet, with over CA$13 million in cash. Again, because of our concern about a gold pullback, we are holding Midland, but would buy on any pullback, perhaps to the mid-70s.

Top Buys

As mentioned above, we think we are likely to see a pullback in gold and resources in coming weeks, so would hold off most buying. Best buys this week would be Lara Exploration Ltd. (LRA:TSX.V, 0.69) and Kingsmen Creatives Ltd. (KMEN:SI, 0.22). We fully expect that in the next week or two, we shall start to see more good buys.

Upcoming Conferences

Two of my favorite conferences are coming up next month, one virtual and one live. The Sprott Resource Symposium is going virtual this year, July 2225, with many of the top names in the resource investing world, and several companies having “virtual exhibits.” For details or to register, click here.

Adrian Day, London-born and a graduate of the London School of Economics, heads the money management firm Adrian Day Asset Management, where he manages discretionary accounts in both global and resource areas. Day is also sub-adviser to the EuroPacific Gold Fund (EPGFX). His latest book is “Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks.”

Disclosure: 1) Adrian Day: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Midland Exploration, Altius Minerals, Lara Exploration. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Funds controlled by Adrian Day Asset Management hold shares of the following companies mentioned in this article: All. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Midland Exploration, Lara Exploration and Altius Minerals, companies mentioned in this article.

Millrock Resources CEO Gregory Beischer speaks with Maurice Jackson of Proven and Probable about his company’s drill program in the shadow of the Pogo gold mine.

Gregory for someone new to Millrock Resources, please introduce the opportunity the company presents to the market and in particular, the 64North project, which has market participants anxiously awaiting news results.

Gregory Beischer: Millrock is a team of early-stage exploration geologists. We want to make a discovery of a giant ore deposit and sell it to a major mining company, that’s our goal, but we take a different approach than a lot of early-stage explorers. It’s a risky business. So we will invest our capital to generate projects, come up with a new idea, acquire the mineral rights, but before any really big dollars are spent for exploratory drilling, we’ll bring in a partner. And that way we can operate five or six projects at any one time, increasing our odds of making the discovery that will drive our share price way up, but also it’s a sustainable company, one that has a core group that’s with us year after year doing excellent scientific work. And we know that’s one of the key ingredients to successful mineral exploration and discoveries.

Maurice Jackson: Sticking with the 64North project, can you provide us with an update on drilling?

Gregory Beischer: These are exciting times for Millrock right now. We’ve developed a huge district-scale project looking for another gold deposit in the vicinity of the Pogo gold mine. Pogo was discovered in 19941995. It’s been producing excellent gold grades and ounces over the past decade. Millrock is confident that we may find another mine just like it. And I believe the area around Pogo has the potential to host multiple mines in the future. I think the Goodpaster Mining District in which our 64North project is located will have in the end multiple mines that will produce tens of millions of ounces of gold, comparable to something like Red Lake in Ontario, or Val-d’Or in Quebec, or Kalgoorlie in Western Australia. Millrock has the dominant land position by far in the district. We had a unique opportunity a year ago where after eight bad years in the mining cycle, the ground had all come open.

And so we were able to stake the whole district. And there was an aggressive move on our part, but one that’s paid off. We have an Australian junior company funding the work. We’re executing that work in collaboration with their technical team. I am glad to convey that our geological crews are mobilizing to the field today. And the drill is meant to have arrived on site today. And by the end of the week, we should be drilling again at the Aurora target on the 64North project, just to the immediate west of the Pogo gold mine, so exciting times. I know you and other shareholders have been following this particular project quite closely. And it’s a relief now to be exploring again, after being slightly derailed by this pandemic.

Maurice Jackson: Besides drilling, what other work is being conducted to delineate the 64North project to increase the chances for success?

Gregory Beischer: Millrock is conducting work on multiple fronts. It’s an enormous attractive claim, we’ve done a lot of studies, desktop studies looking at our extensive database for the district generating new drill targets. We have this obvious, compelling target at Aurora west of Pogo, but there are lots of other places that are coming forward too. We’re going to have a steady pipeline of drill-ready targets on this project for years to come. And so we’ve developed plans, exploration plans for each one of those prospects that will be executed later in the year, but also more particularly on the West Pogo, we’re about to do two geophysical surveys, airborne geophysical surveys that will help our image below the surface of the Earth, map out the structures. And as you know, the deposits at the Pogo mine are relatively flat-lying.

They dip gently, and so at about 25 or 30 degrees. As those dip off to the Northwest, they’re going to come on to Millrock’s ground. And these geophysical surveys will help confirm the existence of the structures, and to determine the depth to which we’ll have to drill, to intersect them. And we would plan to do the geophysics, in early June, but we would plan then to drill those targets in the down-dip direction from the Goodpaster Deposit Pogo Mine later in the summer. The Aurora is being drilled now, geophysics happening now, but we should be drilling through the year on this project.

Maurice Jackson: Truly exciting times for Millrock Resources. Sir, what is the next unanswered question on the 64North project? When can we expect a response, and what will determine success?

Gregory Beischer: The very first hole we drilled at 64North in March had a lot of great geological signs in it. We could see a lot of hydrothermal fluids had moved through the rocks, mineralizing them with quartz veins and veinlets and sulfide minerals that are very typically associated with gold. Everything looked great, but surprisingly the gold values were pretty weak. But we know we’re in the right area, and we’re probably peripheral to a deposit by a short distance. And we know we’ve got the structures. We know we’ve got the right mineralization. We just need the gold. Millrock will be moving our drill northward. And I’m very hopeful that we’ll intersect the same structures, but this time with lots of gold in them, and that’ll be the next big test and measure of success for Millrock and its team.

So we’re hoping to make in this drill program that we’re currently executing a new gold deposit discovery. And if we do, I don’t think Millrock’s share price will be 22 cents much longer. It’s been great to see some exploration companies having exploration success, and shareholders being rewarded at the same time as there are some good drill holes lately, and one particularly in Alaska that resulted in a tenfold share price increase. So we’re hoping to repeat that kind of success.

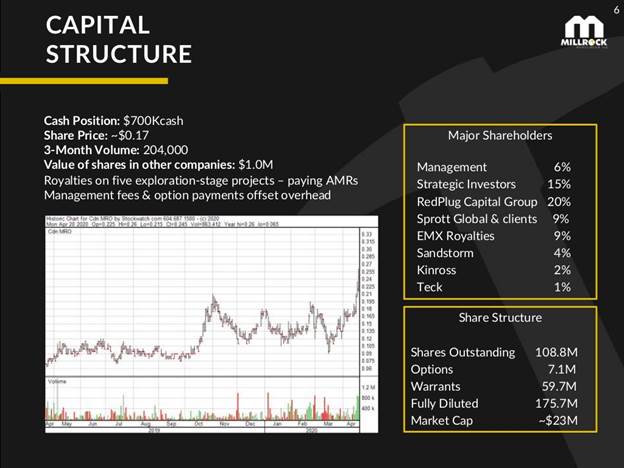

Maurice Jackson: Well, in many regards you have, in nine months the stock prices almost tripled. What are the current stock price and the capital structure for Millrock Resources?

Gregory Beischer: Now, the last time I looked, an hour or so ago, we were at 22 cents. That’s three times higher than it was a year ago when you and I and others participated in a private placement financing when Millrock raised some money. So that feels good to have had that success, but I think we’re just barely getting going. Maurice, I think about 2009, Millrock share price has got all the way down to a similar level of 5 cents when the market crashed badly in 2008, but 12 months later Millrock was at $1.05. And that was simply because we had a very supportive market. Things came roaring back, and Teck invested in Millrock; Altius Minerals and Kinross all invested in Millrock. We were doing really good work and in that rising tide, in that good market, our share price increased significantly. Today we’re a much, much stronger company. And if we were to make a real bona fide gold deposit discovery at this time, it would be a remarkable thing for our share price.

Maurice Jackson: Well, speaking of a strong company, what is the capital structure?

Gregory Beischer: Millrock has 109 million shares outstanding right now. The market cap is roughly $20 million. We also have warrants that are outstanding and now in the money. And so we anticipate that we may get some warrants exercised and that would bring some more money into our treasury. We want to deploy some cash as soon as we can to buy up more gold projects. We see that the market is here. We’re getting inquiries from other junior explorers looking for projects. And so we want to make some quick moves to generate more gold projects in Alaska, as soon as we possibly can.

Maurice Jackson: Sir, what keeps you up at night that we don’t know about?

Gregory Beischer: Well, I’m like everyone concerned about this pandemic. We put in rigorous safety precautions for our teams, so they can get back to work safely. As you can imagine though, traveling together in vehicles and that sort of thing poses some risks. We think we’ve got it well handled, but it’s a worry. We would hate for this drilling program to get derailed again. And so we’re trying our very best to have those safety protocols to minimize the chance that that’s going to happen.

Maurice Jackson: Last question, what did I forget to ask?

Gregory Beischer: Well, often, Maurice, we talk about the gold price, and I’ve already done that to some degree, seems like it’s moving up and so much of capital availability and interest in the mining and mineral exploration sector seems to depend on the gold price, but everything’s moving the right way now. And I’m sure you’re seeing it, but the generalist investing public now is starting to pour into precious metals. And it’s great to see because it’s putting some wind under the wings of mining companies and explorers.

Maurice Jackson: Yes, sir. A lot of synergies and a lot of catalysts coming into the space. Mr. Beischer, where can audience members receive more information on Millrock Resources?

Gregory Beischer: The website address is www.MillrockResources.com. There you’ll find the contact information for Melanie Henderson who’s in charge of investor relations for Millrock. And if any of the current shareholders or future shareholders would like to speak directly to me, I’d be glad to take the time to speak with them.

Maurice Jackson: Mr. Beischer, thank you for joining us today on Proven and Probable. Wishing you and the entire Millrock team the absolute best, sir.

Millrock Resources is a sponsor and we are proud shareholders.

And as a reminder, I’m a licensed representative for Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio from physical delivery, off-shore depositories, and precious metal IRAs. Call me directly at 855-505-1900 or you may email, [email protected].

And finally, please subscribe to provenandprobable.com, where we provide mining insights and bullion sales.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Millrock Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Millrock Resources is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Millrock Resources, a company mentioned in this article.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Peter Epstein of Epstein Research discusses the Nevada lithium project and potential paths that the company could take.

Cypress Development Corp. (CYP:TSX.V; CYDVF:OTCQB; C1Z1:FSE) owns 100% of a giant, leachable, lithium-bearing claystone-hosted resource, the Clayton Valley Lithium Project (CVLP), adjacent to Albemarle Corp.’s Silver Peak brine operations in Nevada. The company has an Enterprise Value (EV) {market cap + debt cash} of C$17.5 million.

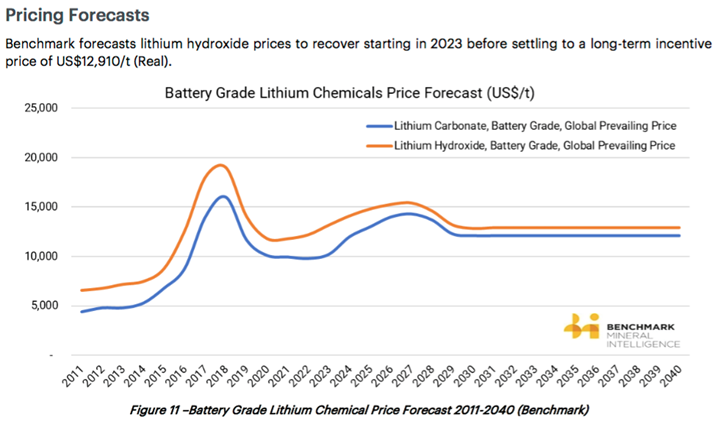

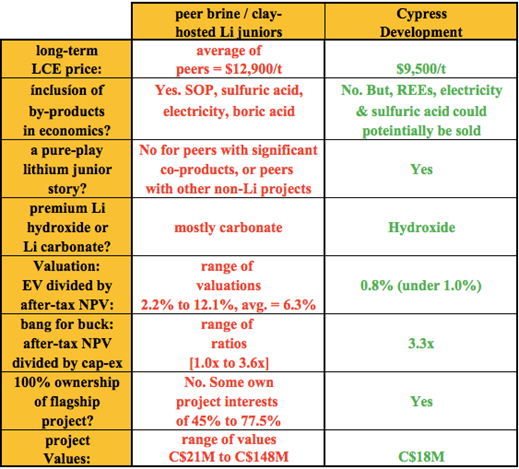

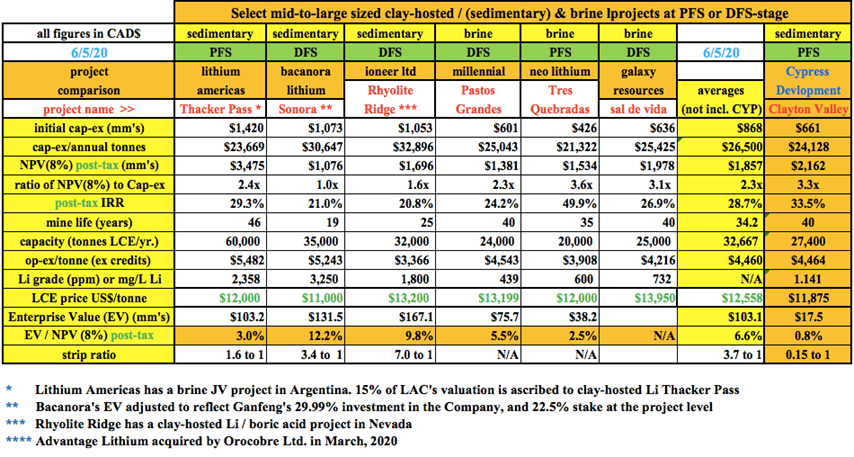

On May 19th, management delivered a highly anticipated press release summarizing its Pre-Feasibility Study (PFS) on the CVLP. Let me start by saying . It was worth the wait. Cypress adopted a low long-term price of US$9,500/tonne (t) of Lithium Carbonate Equivalent (LCE). The price used in a dozen other brine or clay-hosted (sedimentary) project reports (PEA, PFS or DFS) in the past three years ranged from US$11,000 to US$13,950/t and averaged US$12,558/t.

Cypress Development Corp. PFS a high-quality, serious report

Admittedly, lithium prices have been falling since 2018, but peer Nevada lithium and boric acid project developer ioneer ltd. announced (20 days before Cypress) a Definitive Feasibility Study (DFS) with a US$13,200/t LCE price assumption.

Hard rock juniors are pursuing lithium hydroxide, but brine projects have lithium carbonate in their plans. Cypress plans to make battery-quality lithium hydroxide. In Cypress’ PFS, nameplate capacity is 27,400 tonnes LCE/year. However, it takes less lithium to manufacture hydroxide than to make carbonate. If the CVLP project were to deliver 100% hydroxide, it would be operating at an average of 31,141 tonnes /year.

Some investors might be wondering why management didn’t use a higher long-term lithium price. I believe there are two reasons. First, that’s not how CEO Bill Willoughby rolls. Dr. Willoughby is a PhD in Mine Engineering and Metallurgy, making him the polar opposite of a Vancouver promoter, and the best choice imaginable to be leading Cypress.

Second, I suspect that Cypress is in talks with entities led by serious engineers, metallurgists and experienced mining experts like Dr. Willoughby. A detailed, highly accurate PFS was called for. Please note, management has never revealed to me a name of anyone they’ve spoken with in the past or presently.

Cypress is very attractive in peer comparisons and in valuation

Unlike peers, Cypress did not incorporate by-/co-products in the economics. By contrast, Lithium Americas’ Thacker Pass project includes 11% of gross annual revenue from the sale of excess electricity and sulfuric acid. Cypress might also have excess sulfuric acid to monetize, but management did not use it in the model.

Rare Earth Elements (REEs) [scandium, dysprosium and neodymium] are present at the CVLP, but zero credit was ascribed to these potential cash flows. If recoverable, the un-discounted value of the REEs is in the hundreds of millions. REEs will be studied and reported on in the Definitive Feasibility Study (DFS).

By-/co-products are included in the economics of some peer company projects. I mentioned Thacker Pass (electricity and sulfuric acid). Bacanora proposes to produce potassium sulfate (SOP) alongside lithium carbonate.

In order to more accurately compare projects, I adjusted the lithium price assumption in the CVLP PFS. Taking the midpoint between the base case of $9,500/t and the “upside” case of US$14,250/t, I interpolated key metrics at an implied LCE price of US$11,875/t, (5% lower than US$12,558/t peer average).

Cypress’ PFS compares quite well to the projects shown below. The average cap-ex was C$874 million vs. C$661 million for CYP.V, capital intensity; C$26,500/t vs. C$24,128/t for CYP.V, ratio of after-tax NPV(8%) to upfront capital; 2.3x vs. 3.3x for CYP.V., and IRR; 28.7% vs. 33.5% for CYP.V.

Again, these comparisons were done with a US$11,875/t price for Cypress. One last thing, the CVLP has a strip ratio of just 0.15 to 1. The other sedimentary projects have strip ratios ranging from 1.6 to 7.0 to 1, averaging 3.7 to 1.

Is Cypress a takeover candidate?

Could Tesla be looking at acquiring Cypress? With an EV of C$224.4 billion (12,824 times that of Cypress) it could easily afford to. However, I have no idea if Tesla is interested. I imagine that a few auto and/or Li-ion battery makers are kicking the tires. More importantly, I suspect that lithium and specialty chemicals giant Albemarle Corp. will be carefully reviewing the PFS.

Why would a C$15 billion company like Albemarle care about tiny Cypress? Simple. In a much larger company’s hands, the CVLP would be worth a lot more than C$17.5 million. A larger company could comfortably afford the initial cap-ex of C$661 million. Financially strong players can borrow at low interest rates.

With substantial financial wherewithal and unrivaled, decades-long, expertise in specialty chemicals & lithium, Albemarle could bring a sedimentary project, one adjoining its own Silver Peak brine operations, to fruition faster than Cypress ever could. Silver Peak has been in operation since the mid-1960s. Assuming its current 6,000 tonnes LCE/year capacity, Albemarle says it has ~20 years of remaining mine life.

Think about the synergies that could be gained by adding the CVLP to Albemarle’s neighboring lithium complex. Silver Peak has all manner of industrial/chemical property, plant and equipment, and, of course, lithium processing facilities. Equally important, it has 50+ years of expert knowledge and experience with lithium compounds and local/state permitting.

Adding 27,400 tonnes/year LCE (or 31,141 tonnes/year hydroxide) to Albemarle’s 6,000 tonnes LCE/year would move the needle for Albemarle. Cypress does not include EBITDA in the summary press release of its PFS, but the op-ex is US$3,329/t. So, at an interpolated lithium price of US$11,875/t, the operating margin before taxes would be $8,546/t.

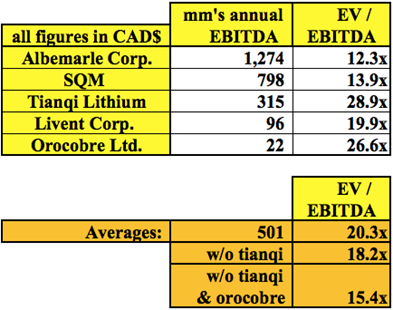

Therefore, 31,141 tonnes hydroxide, multiplied by a US$8,546/t operating margin, equates to ~C$346 million in cash flow/year. Compare that C$346 million to Albemarle’s trailing 12-month EBITDA of C$1.235 billion. All else equal, Albemarle’s EBITDA margin could jump from 27.1% to ~31.3% by acquiring Cypress. Can these two companies find a way to combine resources?

There are not that many lithium producers (of meaningful quantities), and SQM and Albemarle are not pure-play lithium investments. In the chart above, I show that EV/EBITDA multiples are fairly strong even with lithium prices at less than half 2018’s highs. Although there’s still a lot or execution risk, imagine what a potential cash flow stream of C$346 million/year for 40 years might be worth? A 15.4x multiple times C$346 million = C$5.3 billion. Discounting that figure back six years (from 2026) at a 20% discount factor, it’s still C1.78 billion.

Next Steps

The authors of the PFS recommend additional testing and studies be done in the areas of processing, mining, permitting and infrastructure. Further work is needed to confirm the flow sheet and determine recovery and reagent consumptions. A confirmation of the process and equipment in the leaching and filtration functions is sought and there’s further work to do to enhance solid-liquid separation to further reduce acid consumption.

Management must determine if there is any lithium or acid losses in the processing plant design and optimize lithium solution handling. Another important step will be to assess the economic viability of potassium, magnesium, REEs or other elements.

Drilling/limited test-mining is required to obtain material for metallurgical testing. Regarding permitting, a field program will be necessary to determine if any protected species of plants or animals are present, and to gather environmental and other data to prepare a mine Plan of Operations.

Finally, infrastructure: Feasibility-level designs for the mine, plant and tailings storage areas can now begin. A better understanding of power and water supply is needed. These are big ticket items that need to be sorted out over the next 1218 months, before a DFS can be completed.

Capital will have to be raised to fund a pilot plant, various reports and studies and a DFS. Importantly, funding need not come solely from equity raises. I suspect that a farm out or JV is possible as soon as this year. Management is confident that these and other critical factors can be addressed. Readers should remember that first commercial production is probably not until 2025; there’s plenty of time to address any challenges.

CONCLUSION

There are simply not that many 25,000+ tonne/year lithium hydroxide projects in the world at PFS-stage or more advanced, that could be in production in 2025, or perhaps 2024 if a company like Albemarle were to get involved.

Once car & battery makers see lithium projects get acquired, or have their production capacities tied up by off-take agreements away from them, there might be a rush of M&A activity. Cypress Development Corp. (TSX-V: CYP) (OTCQB: CYDVF) (Frankfurt: C1Z1), with a world-class project in a world-class location, an EV of just C$17.5 million and a project with cap-ex <US$500 million, is a company that should be high on the lists of prospective suitors.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Cypress Development Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Cypress Development Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Cypress Development Corp. was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

A review of CloudMD Software & Services and the reasons why it makes a compelling investment are provided in a Beacon Securities report.

In a June 4 research note, analyst Gabriel Leung reported that Beacon Securities initiated coverage on CloudMD Software & Services Inc. (DOC:TSX.V; DOCRF:OTCQB; 6PH:FSE) with a Speculative Buy rating and a CA$1.50 per share target price. The stock is trading now at about CA$0.71 per share.

Leung reviewed the company’s objective and revenue sources. CloudMD, based in Vancouver, British Columbia, aims to digitize healthcare delivery by providing patients access to all points of their care remotely, from a cellphone, tablet and/or laptop or desktop computer. “CloudMD has generated good early traction on this front,” Leung noted.

CloudMD generates revenues in two ways, Leung stated. One is from software as a service-based subscriptions to its technology services. They include CloudMD, a telemedicine platform that connects patients in British Columbia and Ontario to a licensed physician for real-time virtual appointments. MyHealthAccess is an online portal for patient appointments and a telemedicine platform. JunoEMR is a cloud-based electronic medical records software, and ClinicAid is a medical billing software. Livecare Connect is a standalone telemedicine platform used by health professionals across Canada. KindredPHR is a software for storing, managing and sharing personalized health records. As for future revenue, Beacon estimated CloudMD will generate $15 million in 2020 and $27 million in 2021.

This array of telehealth solutions serves 375-plus clinics and more than 3,000 licensed practitioners, including emergency medicine physicians, which cumulatively have about 3 million registered patients. CloudMD has about 100,000 patients registered on its CloudMD platform alone.

Also, the company has partnerships with Save-On-Foods and Pure Integrative Pharmacies, which are pilot testing the presence of telehealth kiosks inside their facilities for on-demand, on-site virtual care.

Revenue also comes from the healthcare facilities that CloudMD runs, which are five medical clinics in the Lower Mainland and two pharmacies in Metro Vancouver.

“While it does have a brick and mortar presence, we believe the main growth and value driver for CloudMD will come via market share gains in the large and relatively untapped virtual care, telehealth market in Canada,” commented Leung.

Leung highlighted that three existing factors are setting the company up for further success. One is its healthcare background, another is its suite of telehealth offerings. The third is the impact of COVID-19 and new related governmental regulations around remote healthcare. “CloudMD is well positioned to capitalize on the telehealth opportunity in Canada,” he added.

Several potential catalysts are on the near-term horizon for CloudMD, Leung pointed out. They include possible acquisitions of further technology or clinics, for which the company has about $15 million in funds. Other possible stock moving events are an extension beyond the pilot phase of either of its two existing kiosk partnerships and an expansion of its pharmacy kiosk business into Ontario.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with CloudMD Software & Services Inc. Please click here for more information. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of CloudMD Software & Services Inc., a company mentioned in this article. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Disclosures from Beacon Securities, CloudMD Software & Services Inc., Initiating Coverage, June 4, 2020

Does Beacon, or its affiliates or analysts collectively, beneficially own 1% or more of any class of the issuer’s equity securities? No

Does the analyst who prepared this research report have a position, either long or short, in any of the issuers securities? No

Has any director, partner, or officer of Beacon Securities, or the analyst involved in the preparation of the research report, received remuneration for any services provided to the securities issuer during the preceding 12 months? No

Has Beacon Securities performed investment banking services in the past 12 months and received compensation for investment banking services for this issuer in the past 12 months? Yes

Was the analyst who prepared this research report compensated from revenues generated solely by the Beacon Securities Investment Banking Department? No

Does any director, officer, or employee of Beacon Securities serve as a director, officer, or in any advisory capacity to the issuer? No

Are there any material conflicts of interest with Beacon Securities or the analyst who prepared the report and the issuer? No

Is Beacon Securities a market maker in the equity of the issuer? No

This report makes reference to a recent analyst visit to the head office of the issuer or a site visit to an issuer’s operation(s)? No

Did the issuer pay for or reimburse the analyst for the travel expenses? No

Beacon analysts are not permitted to own the securities they cover, but are permitted to have a position, either long or short, in securities covered by other members of the research team, subject to blackout conditions.

Analyst Certification: The Beacon Securities Analyst named on the report hereby certifies that the recommendations and/or opinions expressed herein accurately reflect such research analyst’s personal views about the company and securities that are the subject of the report; or any other companies mentioned in the report that are also covered by the named analyst. In addition, no part of the research analysts compensation is, or will be, directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

– Watching out for sentiment extremes helps you avoid getting “caught up with the crowd”

Simply put, a market sentiment extreme is a situation when most everyone has already taken a bullish or bearish position in a financial asset, leaving almost no one left to buy or sell.

Silver provides an excellent case study.

Let’s briefly go back to April 18, 2011, when Elliott Wave International’s U.S. Short Term Update, which provides near-term forecasts for major U.S. financial markets thrice weekly, showed this chart and said:

The 10-day average of Market Vane’s Bullish Consensus has now risen to 93.3%, reflecting a broad consensus among advisors that silver will continue even higher. The Daily Sentiment Index of traders pushed to 97% bulls as of Friday’s close. … Extremes are extremes and have to be recognized as such otherwise one gets caught up with the crowd and fails to extricate themselves at a reversal.

Just a week later, silver hit a high of $49.91 and in less than three weeks, the price had plummeted 35%.

Now, sentiment measures are not always precise timing indicators. Markets can stay overbought or oversold for a long time. Still, extremes can be quite valuable when used along with the Elliott wave model, which was also signaling a turn in silver’s price trend in April 2011.

In the past nine years, silver prices have traded well below their 2011 high, but there have been rallies.

This brings us to 2020.

On May 11, a well-known precious metals website sported this headline:

Silver prices to soar by 40%+, here’s the case …

They proceeded to outline a bullish case that supported their views of even higher silver prices to come.

They may end up being right, however, the May 20 U.S. Short Term Update showed this chart and said:

[Silver]’s rally has coincided with a surge in the Daily Sentiment Index to 91%. Traders are more optimistic toward silver’s future prospects than at any time since the peak at $19.69 on September 4, 2019 (95%). The only other comparable reading was on February 21 of this year, when the DSI rose to 87%. The prior sentiment extremes corresponded with price highs. Silver declined 41% from September 2019 to March 18, at which time the DSI dropped to just 8% bulls. The environment has now come full circle. Today’s new intraday extreme was not confirmed by gold.

Just like back in 2011, today silver’s Elliott wave pattern provides even more insight into what to expect next for the precious metal.

If you’d like to learn more about Elliott wave patterns, Elliott Wave International has made the online version of the Wall Street classic book, Elliott Wave Principle: Key to Market Behavior available for free.

All that’s required to access the wealth of information in the book is a free Club EWI signup. Club EWI is the world’s largest Elliott wave educational community. When you join, you get free access to resources, reports and videos which provide you with Elliott wave insights on investing and trading, the economy and social trends that you will not find anywhere else.

This article was syndicated by Elliott Wave International and was originally published under the headline Silver: How to Gauge the Crowd’s Mindset. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.