Pork supply is recovering gradually as meat plants across US ramp up production following slowdowns after coronavirus outbreak. Meatpackers slaughtered 450,000 hogs on Monday, up from 417,000 a week ago according to US Department of Agriculture. However, in March they slaughtered up to 498,000 a day. And farmers still have a backlog of livestock after animals could not be slaughtered due to temporarily shut slaughterhouses during the coronavirus outbreak. The number of livestock being killed each day has rebounded from April and May, increasing the supply of pork. Rising pork supply is bearish for LHOG.

Asian stocks on Friday are extending yesterday’s declines, following the latest rout on Wall Street. The Dow Jones index saw prices sandwiched between its 100-day and 200-day simple moving averages, before ending the session 6.9 percent lower to register its largest single-day drop since March 16.

The sharp descent in US equities appears to be a technical pullback after what has been an overextended rally since the multi-year low on March 23, with the Dow now shedding its overbought status. US futures are however gaining at the time of writing, suggesting that a positive end to the trading week is in store. Despite the VIX index surging back above the 40 line and returning to its highest level since April, it’s still too early to determine whether markets will see another period of heightened volatility a la March.

Still, the apparent catalyst for the selloff suggests that coronavirus-related concerns remain the dominant driver in the markets. The rising number of Covid-19 cases in Florida, Texas, California, and Arizona implies that investors cannot yet rule out the risk of a second wave of Covid-19 cases that may trigger another round of lockdowns. The city of Houston is reportedly “getting close” to reissuing stay-at-home orders, even as broad swathes of the States press on with restoring economic activity. While Treasury Secretary Steven Mnuchin eschews the idea of shutting down the world’s largest economy again in the event of a resurgence in Covid-19 cases, the ensuing fears would still be a hit to the gut for consumers, workers, and businesses that are craving for some form of normality; such a blow may perhaps choke economic activity once more.

For market participants who may have been lulled by the stunning gains in riskier assets over recent weeks, it’s now clear that risk sentiment remains fluid amid an outlook that’s riddled with uncertainties. Global investors are expected to continue reacting to significant developments surrounding the coronavirus outbreak and evidently have little qualms shifting into risk-off mode seemingly at the turn of a dime. More overt signs of a resurgence in Covid-19 cases could see the further unwinding of gains in riskier assets, while restoring safe havens to recent highs.

Oil attempts bounceback as markets shift into risk-off mode

The risk aversion has prompted Crude Oil to unwind most of its month-to-date gains as it slipped below the psychologically important $35/bbl level before resurfacing. WTI futures are still on course for their first weekly decline in seven weeks.

Oil markets are looking past the recent extension to the OPEC+ supply cuts, as demand-side uncertainties return to the fore. Should the spike in Covid-19 cases in US states gather momentum and derail the economic recovery, that could clear the path downwards for Oil prices. The fact that US crude inventories reached a record high of 538 million barrels last week also undermines the notion that Crude can be restored swiftly to pre-pandemic levels. The Fed’s dour outlook on the US economy has also dented WTI’s trajectory, in which interestingly, positioning just last week turned the most bullish in almost two years.

Oil markets require more concrete evidence that the global demand recovery is on a surer path, or risk the $40/bbl handle moving further out of its near-term reach.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Peter Epstein of Epstein Research profiles this explorer with a past-producing high-grade silver and gold mine.

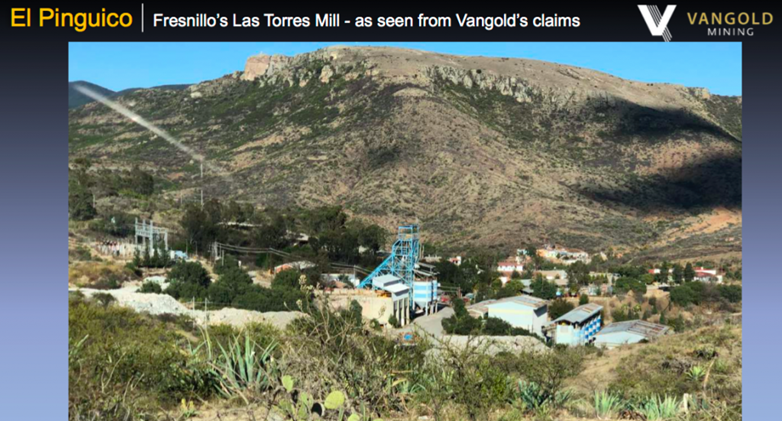

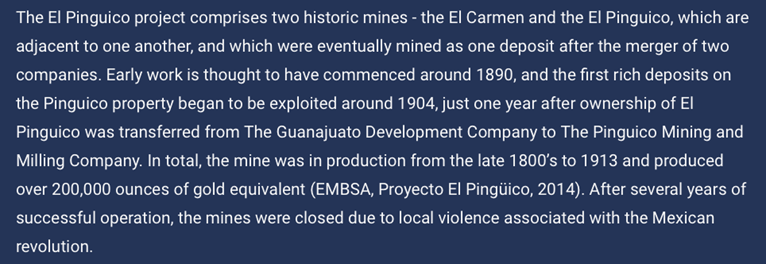

VanGold Mining Corp.’s (VGLD:TSX.V) flagship project, El Pinguico, hosts a high-grade past producing silver (Ag) and gold (Ag) mine (400 tonnes/day). It’s located 7 km south of the city of Guanajuato, in central Mexico. The mine operated from the late 1880s until 1913, mining the El Pinguico and El Carmen veins, thought to be splays of the Veta Madre, the Mother Vein. The Mother Vein (MV) outcrops for 25 km and is the most important source of precious metal mineralization in the region.

Management believes this major vein may cross onto its property underneath the high-grade El Pinguico and El Carmen veins, at a predicted depth of 400600 meters. The MV has been mined to within 250 meters of the company’s border. Minimal drilling has been done to date on the company’s concessions, and none has sought to intercept the MV.

VanGold’s main project is within 230 km of Endeavour Silver’s El Cubo and Bolanitos mine and mill complexes, Fresnillo PLC’s Las Torres mine and mill, and Great Panther’s Guanajuato complex.

Bulk sample results are good, a substantial de-risking event

On June 2nd, the company announced the completion of its bulk sample and metallurgical testing programs. Earlier, management had delivered 1,039 tonnes, (of an estimated 175,000-tonne surface stockpile), for processing at Endeavour Silver’s Bolanitos mill located ~28 km to the north. {excellent drone footage here}. Flotation metallurgical tests were performed, creating a very high-quality Au/Ag concentrate.

On June 9th, the company announced results of the bulk sample testing, in which management gained critical insights into metallurgy, recoveries, reagent usage and the mineralogy of the ore. This information, and associated cost components, will be studied to assess the potential to direct ship El Pinguico’s surface stockpile, (combined with a similar-sized underground stockpile that’s at least ~3 times the grade), to one of several mills in the area.

Average recoveries of gold were 75.2%, (high of 77.7%) and silver at 60.4%, (high of 67.2%). Importantly, a strong concentrate ratio of 232 to 1 was obtained. After removing a small amount of the milled metals for future analysis, the final product consisted of 4.265 tonnes averaging 132 g/t Au, plus 6,661 g/t Ag.

The overall head grade after processing was 1.23 g/t gold equivalent (Au Eq), using a 96 to 1 Au-Ag ratio. The successful bulk sample enabled management to gain a much better understanding of how higher recoveries might be achieved and how to replicate, or possibly improve upon, these results.

Few juniors see data like this ahead of large investments

Arguably more important than the metallurgical metrics is the substantial de-risking of the VanGold Mining story. How many juniors, pre-maiden resource, get to see this kind of data before committing years of time, managerial resources and equity capital? Mission critical info from June, 2020, not from decades ago. Info that helps management, in many respects, beyond just metallurgy.

Armed with these valuable findings, VanGold can negotiate with greater confidence and credibility with toll millers (Endeavour Silver, Great Panther and Fresnillo Plc), local community leaders, strategic investors and permitting bodies.

How many otherwise early-stage juniors could become meaningfully cash flow positive within the next year? Once cash flow starts, monetizing the two stockpiles is expected to take roughly 30 months. This is a company with a pro forma Enterprise Value {market cap +debt cash} of ~C$7 million [share price C$0.12], (pro forma for ongoing exercises of C$0.10 warrants).

VanGold will not need to raise much additional cash if/when the 30-month cash flow period begins, (probably in Q1 2021). Management expects to have at least C$1.5 million in cash at the end of June.

As great as this bulk sample de-risking news is, VanGold is also a compelling exploration story. Hundreds of thousands in cash flow per month, if achieved, would pay for a lot of drilling at El Pinguico. And, there would be plenty left over for exploring the company’s other targets and/or making acquisitions.

Total cash flow could be 2x-4x VanGold’s C$7 million enterprise value

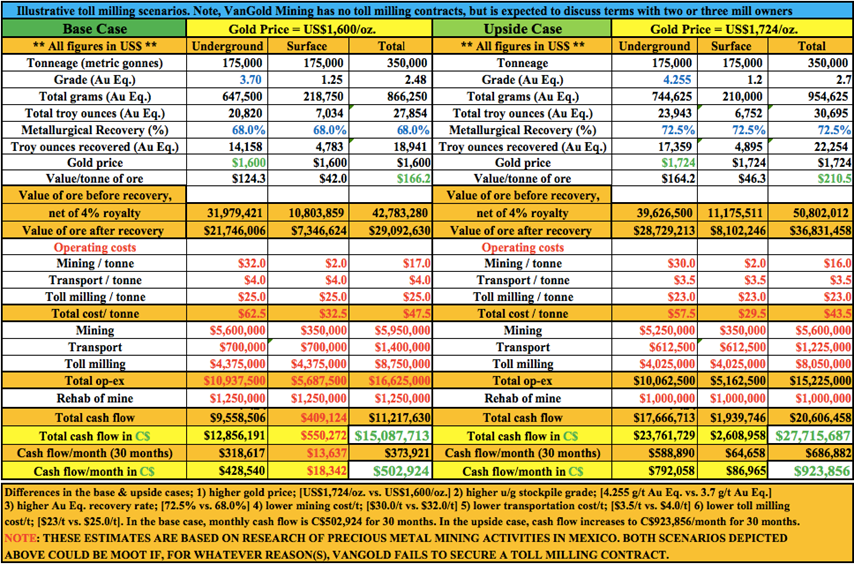

Until this week’s news, it was hard to estimate how much cash flow might be generated from toll milling the stockpiles. While it remains difficult to know, I put together base and upside cases for toll milling the underground and/or surface stockpiles.

The key metrics in each case are, Au Eq. price; US$1,600/oz vs. US$1,724/oz, recovery rate; 68.0% vs. 72.5%, and lower operating costs in the upside scenario as shown below.

The upside scenario enjoys a modestly higher underground stockpile grade of 4.225 g/t Au Eq vs. 3.7 g/t Au Eq. There’s a chance that the 3.7 g/t assumption is too low. In 1959, the Mexican Geological Survey estimated the grade to be 5.6 g/t Au Eq. Plugging in 4.225 g/t Au Eq (+15%) reflects this possible upside.

In the two scenarios depicted below, monthly cash flow of between C$502k & C$923k could commence early next year and last up to 30 months. Total cash flow from monetizing the stockpiles, assuming that a toll milling contract can be negotiated & signed, is C$15 to C$27 million.

Compare that to VanGold’s pro forma enterprise value of about C$7 million. Notice that the upside case’s Au Eq. price assumption is today’s spot price, so hardly a stretch.

Next step, regain access to mine

Clearing debris from the El Pinguico shaft is expected to begin in coming weeks. Once the shaft is safe & clear, VanGold will sample along the bottom of the underground stockpile that contains ~175,000 tonnes grading ~183 g/t Ag & ~1.75 g/t Au (~3.7 g/t Au Eq near current spot prices). The management team is trying to determine how consistent the grade is throughout the stockpile.

Clearing the shaft will allow for the inspection of the mine’s #7 Adit (aka the “Sangria” adit), which may provide an inexpensive haulage route to transport underground stockpile material to surface. This is the company’s preferred method of accessing the material, but fully refurbishing the shaft is another option under consideration.

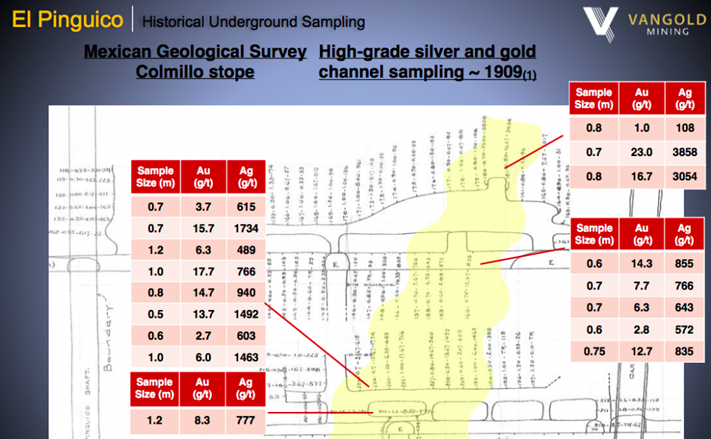

Once back into the El Pinguico shaft, crews should be able to access the Colmillo Stope, a high-grade portion of the mine prior to its closure in 1913. Examples of historical channel sampling from this area in 1909 can be found on page 5 of VanGold’s corporate presentation. Notice the eight samples of >10 g/t Au, and five grading 1,000+ g/t Ag among a few hundred samples taken.

Conclusion

Every mining junior on the planet dreams of being in a position to self-fund exploration and development, to avoid massive equity dilution. Very few management teams have the opportunity to make that dream a reality like VanGold does. To be clear, significant risks remain, but the blue-sky potential for this sub C$10 million company is compelling.

As management continues to de-risk the VanGold Mining (TSX-V: VGLD) story, and if gold and silver prices remain elevated or go higher, there’s ample room for the stock price to run. Blessed with a strong technical team & Board, a great project and a tremendous jurisdiction, the best is yet to come.

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Vangold Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Vangold Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned stock and warrants in Vangold Mining, and the Company was an advertiser on [ER].

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

The Federal Reserve has vowed to provide up to US$2.3 trillion in lending to support households, employers, financial markets and state and local governments struggling as a result of the coronavirus and corresponding stay-at-home orders.

Let that number sink in: $2,300,000,000,000.

I have a Ph.D. in economics, direct the Sound Money Project at the American Institute for Economic Research and write regularly on Federal Reserve policy. And, yet, it is difficult for me to wrap my head around a number that large. If you were to stack 2.3 trillion $1 bills, it would reach over halfway to the Moon.

Put simply, it is a lot of money. Where does it all come from?

Unlike the trillions of dollars the Treasury is spending to save the economy by bailing out companies or beefing up unemployment checks, very little of the Fed’s money actually comes from taxpayers or sales of government bonds. Most of it, in fact, emerges right out of thin air. And that has costs.

Printing green

It is common to hear people say the Fed prints money.

That’s not technically correct. The Bureau of Engraving and Printing, an agency of the U.S. Treasury, does the printing. The Fed, for its part, purchases cash from the bureau at cost and then puts it in circulation.

Although you may have heard some economists talk about the Fed figuratively dropping cash from helicopters, its method of distribution isn’t quite as colorful. Instead, it gives banks cash in exchange for old, worn-out notes or digital balances held by the banks at the Fed. In this way, the Fed can help banks accommodate changes in demand for banknotes, like those in advance of major holidays or after natural disasters.

These exchanges are dollar-for-dollar swaps. The Fed does not typically increase the monetary base – the total amount of currency in circulation and reserves held by banks at the central bank – when it distributes new banknotes.

Magicking green

To put more money into circulation, the Fed typically purchases financial assets – in much the same way that it plans to spend that $2.3 trillion.

To understand how, one must first recognize that the Fed is a bankers’ bank. That is, banks hold deposits at the Fed much like you or I might hold deposits in a checking account at Chase or Bank of America. That means when the Fed purchases a government bond from a bank or makes a loan to a bank, it does not have to – and usually doesn’t – pay with cash. Instead, the Fed just credits the selling or borrowing bank’s account.

The Fed does not print money to buy assets because it does not have to. It can create money with a mere keystroke.

So as the Fed buys Treasuries, mortgage-backed securities, corporate debt and other assets over the coming weeks and months, money will rarely change hands. It will just move from one account to another.

Costs of magical money

While the Fed can create money out of thin air, that does not mean it does so without cost. Indeed, there are two potential costs of creating money that one should keep in mind.

The first results from inflation, which denotes a general increase in prices and, correspondingly, a fall in the purchasing power of money. Money is a highly liquid – easily exchangeable – asset we use to make purchases. When the Fed creates more money than we want to hold on to, we exchange the excess money for less liquid assets, including goods and services. Prices are driven up in the process. When the Fed does this routinely, expected inflation gets built into long-term contracts, like mortgages and employment agreements. Businesses incur costs from having to change prices more frequently, while consumers have to make more frequent trips to the bank or ATM.

The other cost is a consequence of reallocating credit.

Suppose the Fed makes a loan to the “Bank of Fast and Loose Lending.” If the bank wasn’t able to secure alternative funding, this suggests that other private financial institutions deemed its lending practices too risky. In making the loan, the Fed has only created more money. It has not created more real resources that can be bought with money. And so, by giving the Bank of Fast and Loose Lending a lifeline, the Fed enables it to take scarce real resources away from other productive ventures in the economy.

The cost to society is the difference between the value of those real resources as employed by the Bank of Fast and Loose Lending and the value of those real resources as employed in the productive ventures forgone.

Uncharted waters

In recent years, the Fed has shown itself to be quite adept at keeping inflation low, even when making large-scale asset purchases.

The central bank purchased nearly $3.6 trillion worth of assets from September 2008 to January 2015, yet annual inflation averaged roughly 1.5% over the period – well below its 2% target.

I’m less sanguine about the Fed’s ability to keep the costs of reallocating credit low. Congress has traditionally limited the Fed to making loans to banks and other financial market institutions. But now it is tasking the Fed with providing direct assistance to nonbank businesses and municipalities – areas where the Fed lacks experience.

It is difficult to predict how well the Fed will manage its new lending facilities. But its limited experience making loans to small businesses – in the 1930s, for example – does little to alleviate the concerns of myself and others.

Congress gave the Fed the ability to create money from thin air. The Fed should wield this enormous power wisely.

Curis Inc. shares are up more than 130% and established a new 52-week high price after reporting that the FDA cleared the company’s IND Application for CI-8993, its monoclonal anti-VISTA antibody.

Biotechnology company Curis Inc. (CRIS:NASDAQ), which concentrates its efforts on developing innovative therapeutics for treating cancer, today announced that “the U.S. Food and Drug Administration (FDA) has cleared its Investigational New Drug (IND) application for CI-8993, the first-in-class monoclonal anti-VISTA antibody. Curis plans to initiate a Phase 1a/1b study of CI-8993 in the second half of 2020.”

The company’s President and CEO James Dentzer commented, “The clearance of our IND is an important step for the advancement of VISTA therapies, as CI-8993 becomes the first anti-VISTA antibody in development to enter clinical testing…When activated, VISTA plays a critical role in suppressing T cell activity. Conversely, it has been shown in preclinical studies that blocking VISTA reduces the suppression of T cells and reactivates anti-tumor immune function. We are eager to leverage our extensive experience with VISTA and pioneer this first-in-class anti-VISTA antibody program.”

The firm mentioned that certain cancers may be amenable to monotherapy treatment with anti-VISTA therapy. Curis stated that several of these cancers are known to be highly driven by VISTA including mesothelioma, triple negative breast cancer, non-small cell lung cancer and gynecologic malignancies. The company noted that with some other types of cancers, anti-VISTA therapy may be more effective as part of a combination therapy approach.

The company advised that it expects to commence a multi-center Phase 1a/1b dose escalation study of CI-8993 in patients with relapsed/refractory solid tumors in H2/20. The trial will enroll about 50 patients with the objective of determining recommended dosage levels.

The firm explained that “VISTA is a novel negative checkpoint ligand that is homologous to PD-1/PD-L1 and suppresses T cell activation and that it relieves negative regulation by hematopoietic cells and enhances protective anti-tumor immunity, and is highly expressed on myeloid cells and T cells.”

Curis Inc. is a biotechnology company based in Lexington, Mass., that is engaged in developing therapeutics to treat cancer. The company is engaged in a collaboration with ImmuNext for development of CI-8993, a monoclonal anti-VISTA antibody. Curis indicated that it is also collaborating with Genentech, a member of the Roche Group, for commercializing Erivedge® for use in treatment of advanced basal cell carcinoma.

Curis began the day with a market capitalization of around $44.6 million with approximately 36.6 million shares outstanding. CRIS shares opened nearly 80% higher today at $2.19 (+$0.97, +79.51%) over yesterday’s $1.22 closing price and reached a new 52-week high price this morning of $3.59. The stock has traded today between $1.88 to $3.59 per share and is currently trading at $2.87 (+$1.65, +135.24%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

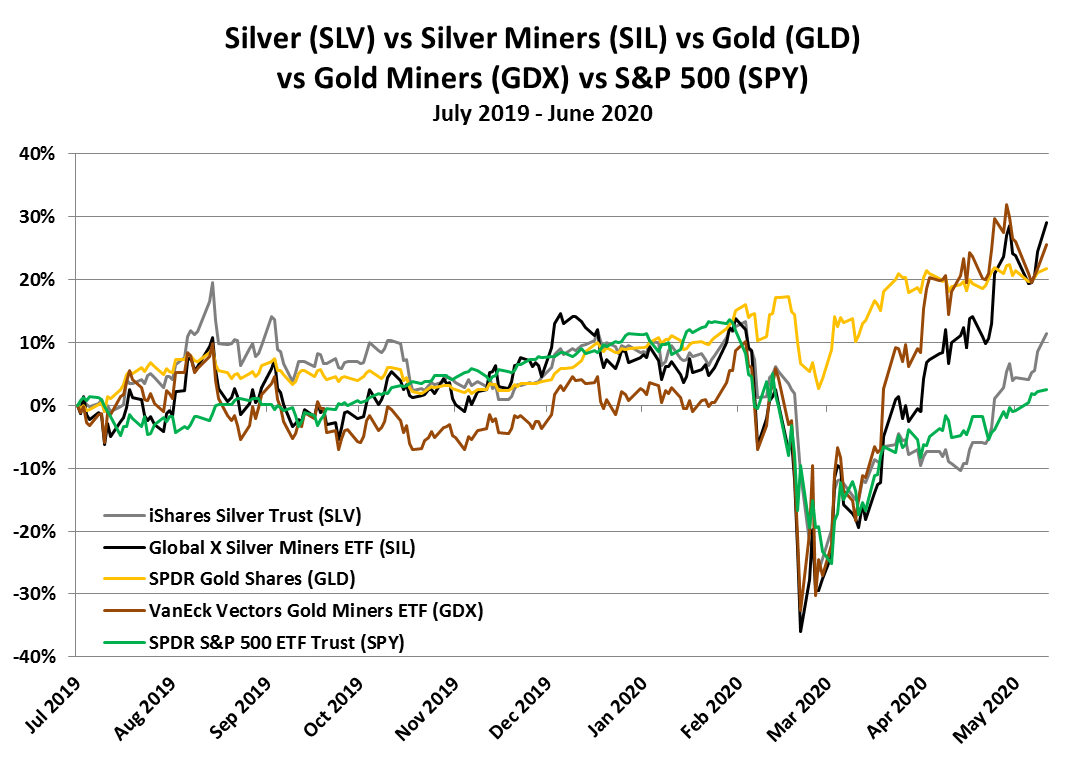

Although the gold to silver ratio has tightened a bit, it remains elevated and could indicate more upside for silver, according to McAlinden Research Partners.

Silver and silver miners popped in May on the back of a rebound in industrial activity around the world. Ultra-low interest rates and expectations of a weaker dollar have compounded several political pressures that begun popping up at the end of the month. Though the gold to silver ratio has tightened a bit, it remains elevated and could indicate more upside for silver.

Silver futures capped a gain of nearly 24% for the month of May, the largest monthly gain since 2011. The metal jumped strongly on hopes of an upturn in industrial activity as economies around the world have begun to “reopen” in the aftermath of the COVID-19 pandemic.

As the Wall Street Journal writes, silver has lagged behind gold for years and tends to be more volatile. Silver’s industrial uses have held prices back in the past, but now they’ve provided a short-term boost.

Silver felt the pull of the downturn in industrials over the months preceding April, particularly in March, when the gold-silver ratio reached an all-time high of 126.43. As Forbes writes, in most periods of economic downturn, the gold-silver ratio tends to rise. This makes sense because gold tends to experience greater inflows as a result of investors seeking safety and industrial uses for silver slow. No better example of this relationship in action was in March when it felt as though the entire global economy stood still. Though both gold and silver were caught up in the downward spiral of nearly every asset class, silver undeniably fell harder.

But, likewise, the gold-silver ratio tends to fall after a recessionary period. Though the U.S. appears to be at the very bottom of its recession, many major economies in Asia and Europe have managed to stoke industrial activity, which has now brought the gold to silver ratio all the way below 95.

Additionally, non-COVID uncertainty has combined with the uptick in global economic activity to help silver close the gapparticularly toward the end of last month.

Massive protests against police brutality and systemic injustice in Minneapolis, which were derailed by looting and rioting, remain ongoing and have spilled over to nearly every major metro areas across the country and beyond. Days of heated protests and other events, combined with a dash of U.S.-China trade tension, has created a premium for safe havens and comparatively cheap silver has seen renewed interest.

In the 3rd week of May, according to Aberdeen’s Dunn, “silver ETFs added 33 million ounces which would be its best week since July 2019. The investment demand for physical silver continues to be strong. Governments and central banks continue to inject liquidity into the financial markets to offset the negative economic impact of COVID-19. With nominal rates near zero and expected to remain low, the environment for silver is attractive.”

Demand for silver has been stronger than gold lately, said Commerzbank analyst Daniel Briesemann. “The silver ETFs tracked by Bloomberg have registered inflows of 2,479 [metric] tons since the beginning of April, i.e., since the start of the quarter. This has seen holdings rise by 12.3%, allowing silver to overtake gold in this respect Inflows into silver ETFs since the start of the year now total 3,786 tons (+20%), which equates to almost two months of global silver mining production.”

Loose monetary policy around the world bodes well for precious metals, said BMO Capital Markets Friday in updating its gold and silver forecasts. BMO said it was hiking its previous 2020 gold forecast by 5% to an average of $1,732 an ounce for the full year. It also upped its 2021 to 2024 price expectations by 4% to 8% as well as its “long-run forecast” by 17% to $1,400 an ounce from $1,200 previously.

In the case of silver, BMO said it upped its 2020 forecast by 2% to a full-year average of $17.60 an ounce, with the outlooks for 2021 to 2024 increased by 2% to 6%. The bank’s “long-run” price view was increased by 6% to $18.25 from $17.25 previously.

These upgrades are especially rare for BMO, as the bank’s price assumption for each metal had been static since 2015.

Oftentimes, a weaker dollar correlates with stronger precious metals prices. MRP highlighted this relationship a number of times, especially in regard to the effect of real rates and expansion of the monetary base, going back to March 2019 when we released our “Time for Gold” Viewpoint report. Back then, spot prices for the yellow metal were around $1300/oz. Since then, gold has surged to about $1740/oz, a gain of about 34%. Recently, real rates in the U.S. plummeted and went negative, while multi-trillion dollar stimulus packages have undoubtedly pushed the monetary base to new heights.

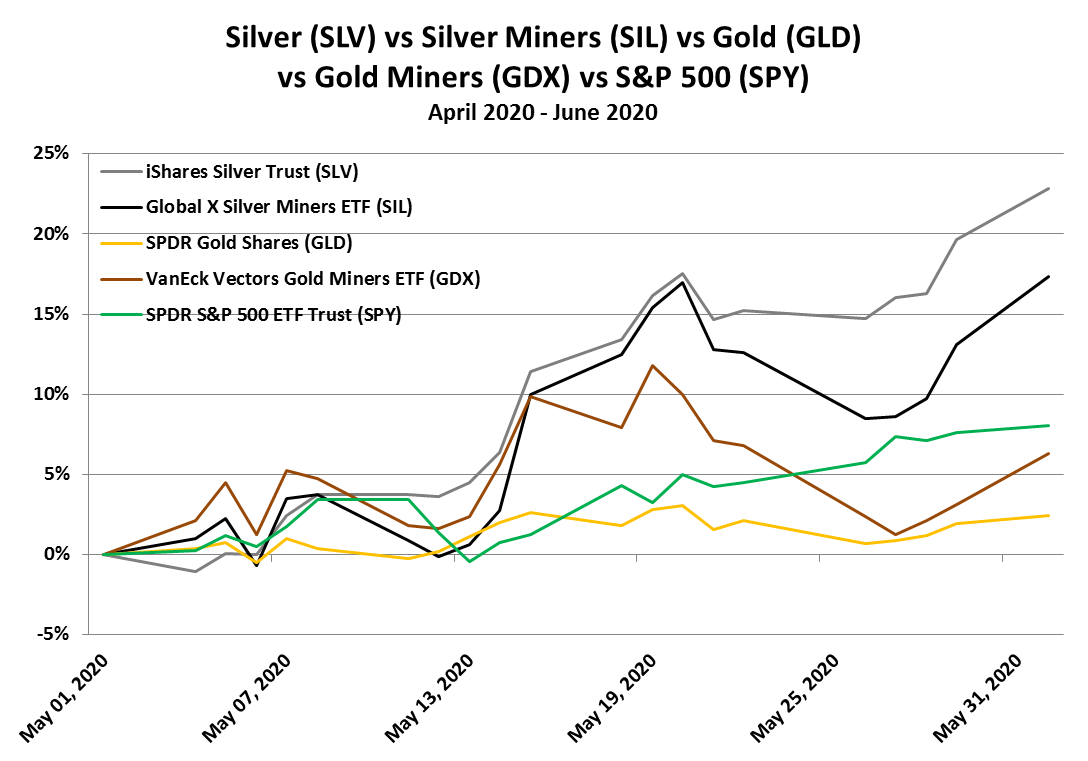

Last summer, we noticed that silver had largely missed out on that rally, becoming historically cheap when compared to gold. As a result we added LONG Silver & Silver Miners to our list of themes on July 22, 2019. Since then, the iShares Silver Trust (SLV) and Global X Silver Miners ETF (SIL) have returned 11% and 29%, respectively, outperforming the S&P 500’s 3% over the same period.

Following a broad rebound in silver prices and miner stocks, the SLV and SIL handily beat out gold and gold miner ETFs, after soaring 23% and 17% on the month. The SPDR Gold Shares (GLD) and VanEck Vectors Gold Miners ETF (GDX) rose just 2% and 6%, respectively.

This content was delivered to McAlinden Research Partners clients on June 2. To receive all of MRP’s insights in your inbox Monday – Friday, follow this link for a free 30-day trial.

McAlinden Research Partners (MRP) provides independent investment strategy research to investors worldwide. The firm’s mission is to identify alpha-generating investment themes early in their unfolding and bring them to its clients’ attention. MRP’s research process reflects founder Joe McAlinden’s 50 years of experience on Wall Street. The methodologies he developed as chief investment officer of Morgan Stanley Investment Management, where he oversaw more than $400 billion in assets, provide the foundation for the strategy research MRP now brings to hedge funds, pension funds, sovereign wealth funds and other asset managers around the globe.

Disclosure: 1) McAlinden Research Partners disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

McAlinden Research Partners: This report has been prepared solely for informational purposes and is not an offer to buy/sell/endorse or a solicitation of an offer to buy/sell/endorse Interests or any other security or instrument or to participate in any trading or investment strategy. No representation or warranty (express or implied) is made or can be given with respect to the sequence, accuracy, completeness, or timeliness of the information in this Report. Unless otherwise noted, all information is sourced from public data.

McAlinden Research Partners is a division of Catalpa Capital Advisors, LLC (CCA), a Registered Investment Advisor. References to specific securities, asset classes and financial markets discussed herein are for illustrative purposes only and should not be interpreted as recommendations to purchase or sell such securities. CCA, MRP, employees and direct affiliates of the firm may or may not own any of the securities mentioned in the report at the time of publication.

Ron Struthers of Struthers’ Resource Stock Report considers the current outlook for miners in Nevada and highlights ProAm Explorations, which he believes is a bargain primed for advancement.

We are entering into a new gold and gold mining bull market. I expect this will go down as the biggest gold bull market in history, with record paper currency printing. It is coming off the bottom of the worst mining bear market in history.

This long-term chart of the Barron’s gold mining index reveals the bear market bottom of late 2015 was around the same level as the 2001 and 1976 bottomssimply amazing, since gold was three to four times higher than those past bottoms in the index. The March crash sent the index to 400, and it fully recovered by the end of April and hit new highs in May. There is a lot of upside left and I expect the index to go well above the 2011 high.

To get maximum benefit from this new bull market, my plan is to buy a basket of quality juniors in good jurisdictions like Mexico, Canada, Australia and Nevada, a state that is a gold country in its own right. Consider this about Nevada:

Gold is the state’s top overseas export by value, accounting for $4.9 billion, or 44%, of the state’s $11 billion of exports in 2018. A year earlier, gold accounted for more than half the total. The top destinations are Switzerland and India, where Nevada-mined gold is refined.

The state produces more than 80% of the gold mined annually in the United States. If it were a separate country, Nevada would be the world’s fifth-largest producer, behind China, Australia, Russia and Canada.

Over the past decade, gold production has averaged about 5.5 million ounces per year. The value of that production in 2018 was just over $7 billion, representing 84% of all mining production in the state.

I met with one of the principals behind ProAm at the PDAC, and I have known a recent addition to the board, Al Fabbro, for many years. Al Fabbro was a major factor behind Roxgold Inc. (ROXG:TSX), which has done well since we bought it in 2012, although we ended up stopped out in 2013 at breakeven. Al Fabbro would not come on the board of just any company. ProAm has a Nevada project that is a great jurisdiction for gold exploration. It is rare to find good properties there, but a ten-year bear market has helped.

ProAm Explorations Recent Price: $0.11 per share 52-week trading range: $0.05 to $0.12 Shares outstanding: 7.1 million; management = 30%

Highlights:

New company with tight share structure

Well experienced management team with past success

Property in a great jurisdiction; Nevada has very good infrastructure

Surface sampling revealing high-grade silver up to 6.99 opt, and copper to 8.84%

Property has never been drilled, so a maiden drill program

5 drill holes to test a 4.5-mile (7,250-meter) rhyolite dyke system.

Management (from the company website)

Donald MacDonald, president and CEO: Mr. McDonald graduated from the University of Manitoba in 1970 with a B.Com (Honours) degree. He has held several senior management positions in the securities brokerage industry. Mr. MacDonald’s education and experience provide him with the relevant knowledge to act as a member of the Audit Committee.

Al Fabbro, director: Mr. Fabbro has over 30 years’ experience in both the finance and mining industries. From 1984 to 1990, Mr. Fabbro headed the retail trading department of Yorkton Securities, followed by six years with Yorkton’s Natural Resources Group. After working for 10 years as an investment advisor with Canaccord Capital, specializing in the natural resource sector, Mr. Fabbro left to become Lead Director of Roxgold Inc., which was named the top company on the TSX Venture 50 and raised in excess of $60 million in equity financing during his tenure.

David L. Trueman (Ph.D, P.Geo.) Director: Mr. Trueman brings 54 years of exploration and mining experience to ProAm Explorations. He has spent time in academia, government and industry, and in the last 41 years specialized in the rare metals field. He has since worked on rare metal deposits through the Arctic in Canada, Greenland, the U.S. and Russia, and his work has taken him to Australia, Namibia, South Africa, India, the PRC, Brazil, Argentina, Chile, Saudi Arabia, Spain, France, Wales, Denmark and East Germany. He has held a number of directorships on various exploration and mining companies and has authored or co-authored some 70 papers in various professional journals.

Bruce W. Downing (M.Sc., P.Geo, FGC, HON FEC) Consultant: A graduate of Queens University and the University of Toronto (M.Sc.), Bruce Downing has over 30 years of experience as a senior geologist working for several corporations, and as a consultant on surface and underground gold and base metal exploration and production projects in British Columbia and around the world. Mr. Downing was involved in the exploration and pre-production at the Windy Craggy open pit and underground massive copper sulphide deposit; wrote reclamation and closure plan for an open pit copper-gold mine (British Columbia) [and] was involved in several acid rock drainage studies.

Jet Property, Nevada, 100% Earn-In

The property consists of three main areas, known as Jet, Barite Hill and Quarry. The infrastructure is great, with Nevada Highway 93A bisecting the property, with secondary roads to the claims. There has been very little modern exploration and little historical data. Some exploration in the early 1920s was probably focused on precious metals.

PMX is earning a 100% interest in the Jet property, subject to a 2.5% NSR [net smelter return], in return for staged payments totaling US$452,000 cash, 1.5 million shares and US$700,000 on exploration, culminating in a NI-43-101 resource report by fourth anniversary of the agreement (2023).

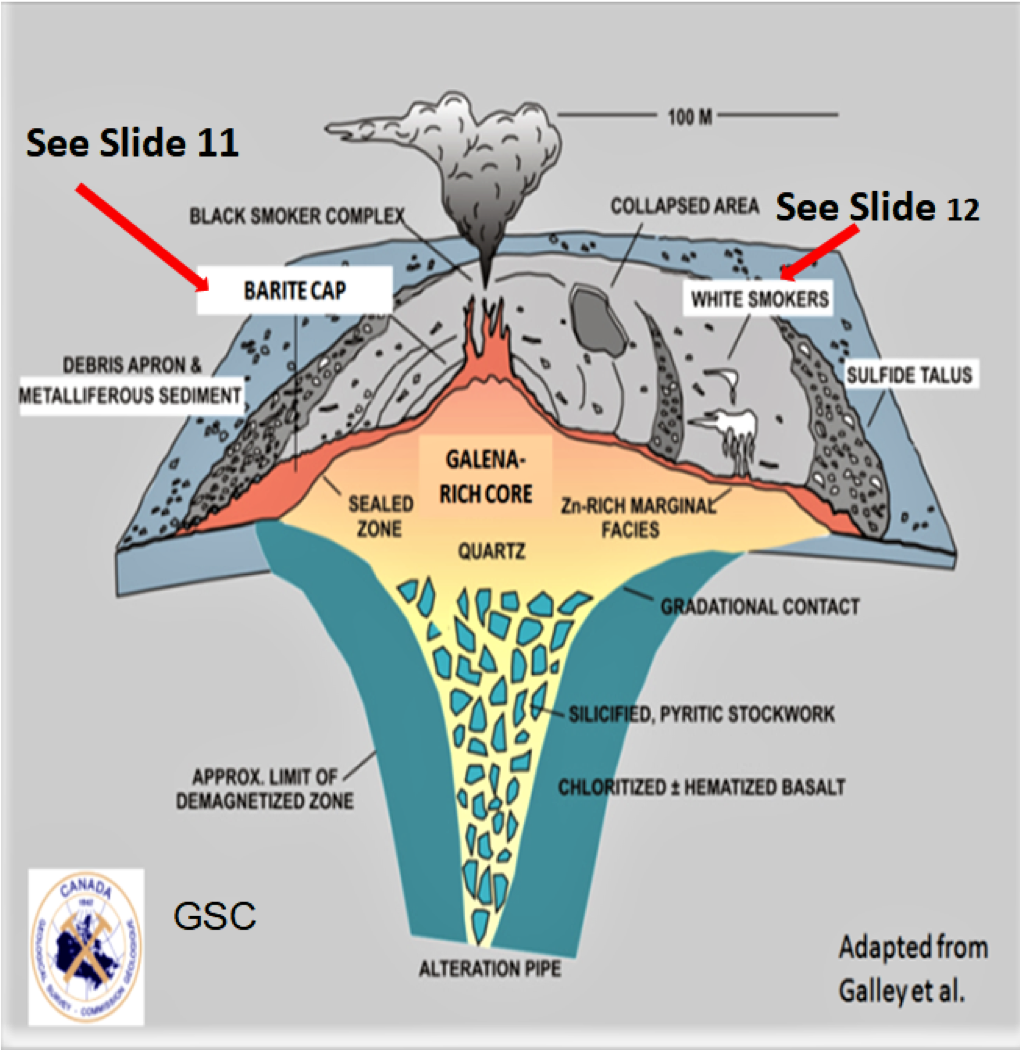

The geological model is called a black smoker. Black smokers are underwater hydrothermal vents that emit jets of particle-laden fluids. The particles are predominantly very fine-grained sulfide minerals formed when the hot hydrothermal fluids mix with near-freezing seawater. These minerals solidify as they cool, forming chimney-like structures. These black smoker complexes can host rich concentrations of copper, zinc, lead, silver and gold.

This next graphic is a combination of a few pictures to give you a good idea about the property.

Barite and silica are found in abundance at the Jet property, and these minerals are commonly associated with hydrothermal volcanogenic deposits. ProAm believes that circulating groundwater dissolved the metals associated with the nearby Wild Cat intrusion and potentially formed a carbonate-hosted Manto-style deposit. Geologist Chris Pedersen collected a series of samples from intermittent outcrops parallel to a 4.5-mile (7,250-meter) rhyolite dyke system.

These samples contained sulfate, oxide and carbonate minerals that are indicative of weathering and leaching of original metallic sulfde minerals. Highlights from the different areas on the property are shown in the next graphic.

In addition, a significant 6- to 8-kilometer-long gravity anomaly is coincident with the mineralization and may indicate an intrusive “heat source,” and in some areas potential metal sulfide mineralization. There is evidence of historical mining, such as this adit.

This is a table of the grab samples and cannot be construed as representative of wider areas of mineralization, but what I notice is the higher grades seem to be copper and silver. There might be a lot of silver in this system.

Next is a map of the proposed five-hole drill program that will test three areas on the project, Quarry, Area 2 and 3 (Barite Hill), and Area 6 (Jet).

Financials

Last financials reveal little cash and no debt. The current $250,000 financing at $0.07 per share will fund the company’s planned drill program.

Conclusion

ProAm is a new company with very few shares outstanding and a tight share structure. After the planned financing there will be only 10.7 million shares out, approximately. At $0.15/share this would only be a market cap of about $1.5 million, so there is a lot more upside than down from these prices.

Despite all the gold being mined in Nevada, new discoveries continue to be made. A new deposit, known as Goldrush, will start producing in 2021, and the adjacent Fourmile will follow sometime after 2025. They are located roughly 20 miles west of Elko, and each could produce 5 million ounces of gold over a decade.

Corvus Gold Inc. (KOR:TSX), near Beatty, Nevada, is still growing its Mother Lode and Bullfrog deposits, with the most recent preliminary economic assessment projecting 282,000 ounces produced per year over the mine life. Blackrock Gold Corp. (BRC:TSX.V; BKRRF:OTCMKTS), another Nevada junior on our list, has been on a tear since March, as it has begun drilling in Nevada.

I believe ProAm’s Jet project has very high odds of hitting some strong drill intersects and being successful. I expect we could see a much high share price with drilling on this project. With positive drill results on the upcoming drill program, management plans to raise more funds at higher prices for the next phase of exploration. There is a lot of interest in junior miners now that show results of a possible discovery, so I expect ProAm will have little problem raising further rounds to advance the project. The time to buy is now, ahead of the crowd and drill results.

You can see on the chart that this company has been quiet, and is not known yet. There was a cross of 2.5 million shares on May 14, and since then, trading activity has come to life a bit, but is still pretty quiet. I am not sure how much stock will come out at these prices, but there is some time before drilling, so do not chase it too high. I would go no higher than $0.15/share for now.

Ron Struthers founded Struthers’ Resource Stock Report 23 years ago. The report covers senior and junior companies with ample trading liquidity. He started his Millennium Index of dividend stocks in 2003 – $1,000 invested then was worth over $4,000 end of 2014 and the index returned 26.8% in 2016. He retired from IBM after 30 years in customer service, systems and business analyst, also developing his own charting software. He has expertise in junior start-ups and was a co-founder of Paramount Gold and Silver.

Disclosure: 1) Ron Struthers: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: ProAm Explorations. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company currently has a financial relationship with the following companies mentioned in this article: ProAm Explorations is a paid advertiser at playstocks.net. Additional disclosures below. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and images provided by the author.

Struthers Disclosure: All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author’s control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.

The market is riddled with uncertainties at the moment, but there is no doubt that we are facing – or will soon be facing – a crisis. The economy is no longer growing as rapidly as it used to, and businesses are beginning to struggle to stay operational. Lockdowns and physical distancing are not helping either.

However, some businesses (and industries) thrive in a time of crisis. As a global recession becomes imminent, we are seeing prominent industries holding steady and supporting local economies. Which businesses will benefit from a global recession? Let’s find out, shall we?

Rental and Accommodation

The travel industry is suffering from the negative effects of a global recession, but the same negative effects cannot be seen in the rental property market. Long-term rentals are still in high demand, especially with people trying to adjust their living standards.

Becoming a landlord and offering affordable rentals to customers are steps that you can take to capitalise on this early trend. You can easily pick up an HMO insurance policy and start offering rental units to multiple occupants. In fact, more landlords are getting HMO insurance from top insurance companies to expand their business models and acquire more customers.

Financial Advisory

Financial markets are also suffering badly from a global crisis, but not all financial services are in low demand. As people struggle to make ends meet, maintain a healthy cash flow, and invest wisely, the demand for financial advisory services is also on the rise.

Once again, this is an industry with low entry barrier. If you have the skills, experience, and certifications to become a financial advisor – both for business and personal clients – then now might be a good time to enter the industry.

This is also an industry that grows rapidly as demand soars. Opening a consulting firm that specialises in debt reconstruction or personal financial management, for instance, is a great way to generate new revenue streams in a time of crisis.

Discount Stores

Sticking with the need to save money and be better at personal financial management as a theme, we also have discount stores and online retailers with plenty of special offers benefiting from the global crisis. Discounts are already attractive enough in normal times, so imagine how many more customers discount stores can acquire when everyone is trying to save money.

There are several ways businesses in this industry can offer better deals. They can specialise in certain items and lower their inventory costs. Manufacturers and wholesalers also need to move their merchandises quickly, so they are more likely to offer products at reduced prices; this is where discount stores can really lower their costs.

There are other businesses that will also thrive in a time of crisis. Grocery stores, food delivery services, and home maintenance service providers are among those businesses. The market is changing and a crisis is imminent, so be sure to explore business opportunities that you know can thrive in a time of crisis to generate new revenue streams.

Shares of Enochian Biosciences reached a new 52-week high after the company reported that it successfully completed its FDA INTERACT meeting for ENOB-HV-01, a potential cure for HIV.

Gene-modified cellular and immune therapies company Enochian Biosciences Inc. (ENOB:NASDAQ) today announced “the completion of an Initial Targeted Engagement for Regulatory Advice (INTERACT) meeting with the U.S. Food and Drug Administration (FDA) Center for Biologics Evaluation and Research (CBER) Office of Tissues and Advanced Therapies (OTAT).”

The company advised that the meeting included management and scientists from Enochian BioSciences together with CBER OTAT staff. The INTERACT meeting’s purpose was said to discuss the direction forward for ENOB-HV-01; “ENOB-HV-01 is a novel approach to autologous stem cell transplantation, with the potential to cure HIV by increasing engraftment of gene-modified cells that are resistant to HIV infection.”.

Dr. Mark Dybul, executive vice-chair of Enochian BioSciences, remarked, “We considered the meeting to be very successful, with strong alignment between Enochian’s approach to developing ENOB-HV-01 and the comments of the FDA reviewers…I want to thank the reviewers from FDA CBER OTAT for their time and helpful insight during our meeting. We look forward to advancing our thoughtful and deliberate pre-clinical work during the remainder of this year and into early next, leading to a pre-IND submission in 2021.”

The company’s Scientific Advisory Board Chair and former Chief Medical Officer of Calimmune Dr. W. David Hardy commented, “The novel approach we are pursuing has the potential to overcome the challenges of engraftment commonly encountered by others in the field. While still early, thus far the data have exceeded my expectations, and I believe the FDA reviewer feedback was very much aligned with our development plan. After more than 30 years as an HIV clinician and researcher, it is a great privilege to be involved with an enterprise with the potential to cure HIV, offering hope to millions of people.”

Enochian BioSciences is a biopharmaceutical company based in Los Angeles, Calif. The firm in engaged in developing and commercializing gene-modified cell therapies. The company noted that it gene-modified cell therapy platform can be utilized in many indications, including HBV, HIV/AIDS and oncology. The company states on its website that in 2017, 36,900,000 people throughout the world were living with HIV and 1,000,000 AIDS related deaths were reported in that same year worldwide.

Enochian started off the day with a market capitalization of around $191.6 million with approximately 46.5 million shares outstanding and a short interest of about 2.8%. ENOB shares opened greater than 220% higher today at $13.25 (+$9.13, +221.60%) over Friday’s $4.12 closing price and reached a new 52-week high price this morning of $13.43. The stock has traded today between $6.39 and $13.43 per share and is currently trading at $6.20 (+$2.08, +50.49%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

The sobering message from the Fed last night, trampling all over the stock market’s V-shaped recovery playbook, has punctured risk appetite today with concerns over a second wave of virus infections in the US bringing traders back to reality with a bump.

Although the FOMC noted that the health crisis posed “considerable risks” to the economic outlook, it reiterated its willingness to add more stimulus if needed, including strengthening forward guidance. This continued dovish stance is risk-supportive on its own and should bode well for an extension of the risk rally.

But Covid-19 is rearing its head once more with cases in America that re-opened earlier starting to surge again. This has obliterated the Fed impact and markets are firmly on the defensive with the JPY and CHF leading the majors in a clear boost to havens.

King Dollar is relishing the risk-off swing as corrective pressures slow and we may see a period of consolidation for markets now as investors digest the latest developments.

The weekly US initial jobless claims came in lower again, but this is now the twelfth straight week in which claims have topped one million. Continuing claims, which provide a clearer picture of how many Americans remain unemployed also printed higher than estimates.

GBP/USD trading around key level

The market continues to await tangible Brexit news after the EU’s refusal to change Chief Negotiator Barnier’s mandate. There has also reportedly been a rejection of a UK plan for secret intensive negotiations through July.

Prices spiked to 1.2815 post the Fed last night and into Fibonacci resistance, but we are now in another correction phase with intraday support at 1.2617. If we lose this level, a long-awaited broader pullback could be on the cards, although the bulls would prefer to see a consolidation phase after a first decline in eleven sessions. The 200d MA at 1.2689 could be a pivot point for direction.

EUR/USD ascent continues

Traders are maintaining their optimism over an EU aid package to solve all the region’s ills, but an agreement is unlikely to be reached before the EU leader’s summit on June 19.

EUR/USD is struggling to extend beyond the 1.14 region with bearish divergence in momentum warning of a broader consolidation phase – not surprising when its streak in overbought territory has been the longest since 2010. Solid support remains down to the mid-1.12s.

Commodity spotlight: Gold

Gold continues to build on its recent gains, advancing every day this week. After falling to the bottom of its two-month range, bullion cheerleaders have their eyes firmly fixed on this year’s high at $1765. A strong weekly close may see those cheerleaders break out with multi-year highs from 2012 at $1796 a likely target.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.