Preparing for publication of important statistics in EU and USA

The downward movement means the weakening of the euro against the US dollar. The EU’s external trade balance surplus in April was only €1.2 billion (excluding seasonal fluctuations of € 2.9 billion). It showed a powerful drop compared to € 25.5 billion in March. Recall that the Eurozone GDP decline in the 1st quarter of 2020 amounted to 3.1% in annual terms. The forecast for the 2nd quarter may be even more negative given this minimum trade balance data. Earlier, industrial production in the EU fell by 28% annually in April. On June 16, significant data will be released in Germany: May inflation and the ZEW business activity index. The forecasts are very positive. If they do not come true, then the euro may weaken. Retail sales for May, an important economic indicator, will be published in the US. The outlook is also positive, but this time for the US dollar. Moreover, Fed Head Jerome Powell is expected to speak.

When markets are down and feeling blue, trust the Fed to come to the rescue.

Such has been the apparent refrain guiding Wall Street, with US stocks erasing opening losses and ending Monday in positive territory after the Federal Reserve revealed how it will buy individual corporate bonds while opening its lending programme for US businesses. The Fed’s tremendous support for the US economy has lifted investor sentiment, with Asian stocks following in Wall Street’s footsteps as the Hang Seng index opened with a gain of 2.6 percent.

Fed chair Jerome Powell will have the opportunity to underscore the central bank’s support programmes when he begins his two-day semi-annual monetary policy report on Capitol Hill starting Tuesday. Powell had been accused of not being bullish enough after last week’s FOMC meeting, which was cited for one of the reasons for the downturn in US equities. However, of late, the Fed’s actions have spoken louder than words, at least enough to pare recent losses.

Still, much of the Fed’s support measures have already been priced into the equity markets. Should the bears achieve critical mass once more, coupled with further evidence that a second wave of Covid-19 cases worldwide is drawing closer, that could prompt a resumption of the recent selloff.

Risk assets could be buoyed further should the incoming US economic data prove that a V-shaped recovery is proving likelier. The May US retail sales and industrial production figures are due later today, and both are expected to show month-on-month expansions of 8.4 percent and three percent respectively.

The incoming economic indicators could add to signs that the world’s largest economy is stabilizing, following Monday’s release of the June US Empire Manufacturing data which saw a minus 0.2 print, beating market expectations of minus 29.6. This shows that manufacturing activity in the state of New York is inching back to growth as more of the US economy emerges from the lockdown.

The positive shocker from the May US non-farm payrolls report, which posted a surprise 2.5 million jobs added last month, is still ringing in investors’ minds. Meanwhile, the number of initial and continuing jobless claims have steadily decreased, suggesting that the worst of the Covid-19 induced layoffs are behind us.

If global investors are offered further signs that the US economy is on a more solid post-pandemic footing, the return to risk-on mode could result in a dead cat bounce for the Dollar index, which could see a return to the 96.0 support level once more.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

– No doubt, you’ve heard: The tech-heavy Nasdaq Composite just passed the 10-thousand mark for the first-time ever, even as the DJIA remains below its February high.

This infatuation with technology is nothing new.

Indeed, EWI’s publications have long noted that the most important peaks of the past 200 years have been associated with periods of intense technological advance.

As far back as the 1835 peak, market participants were enamored with electricity, photography, blast furnaces for the mass production of iron and indoor plumbing. In 1929, investors placed their hopes on commercial air flight and radio. In 1966, futurists were envisioning colonies on the Moon. And, in the year 2000, the shares of internet companies were skyrocketing.

At the time, our January 2000 Elliott Wave Financial Forecast, a monthly publication which provides analysis and forecasts for major U.S. financial markets, offered the following assessment of the technology sector:

In a bear market, reason, technology and science do not get the same respect. The prominence of its recent veneration suggests that a flight from them may be just around the corner.

As the chart shows, the NASDAQ topped in March 2000 — two months after the January 2000 peak in the DJIA — and declined 78% over the next 31 months.

The same topping sequence happened at the October 2007 peak on a shorter-term time basis. The Dow peaked on October 11, 2007 and the NASDAQ held up for several more weeks, topping on October 31, 2007. The market then declined more than 55% until March 2009.

How about here in mid-2020? Are investors facing another top in the technology sector?

After all, the DJIA peaked in February while the Nasdaq Composite just hit an all-time high.

Of course, it remains to be seen whether the current juncture unfolds in the same way.

Yet, Elliott Wave International’s June 8 U.S. Short Term Update, a thrice weekly publication which provides near-term forecasts for key U.S. financial markets, provided this insight:

History shows the NASDAQ topping last at the end of strong rallies.

Right now, EWI’s analysts are discussing an Elliott wave formation in the NASDAQ’s price chart.

If you’re new to Elliott wave analysis or need to brush up on your Elliott wave knowledge, you can read the online version of the “must read” book, Elliott Wave Principle: Key to Market Behavior, 100% free.

As this Wall Street classic notes:

The primary value of the Wave Principle is that it provides context for market analysis. This context provides both a basis for disciplined thinking and a perspective on the market’s general position and outlook. At times, its accuracy in identifying, and even anticipating, changes in direction is almost unbelievable.

All that’s required to enjoy free access to Elliott Wave Principle: Key to Market Behavior is a Club EWI signup. Club EWI is the world’s largest Elliott wave educational community and membership is also free.

This article was syndicated by Elliott Wave International and was originally published under the headline NASDAQ: Some Historical Insights into Techno-Mania. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

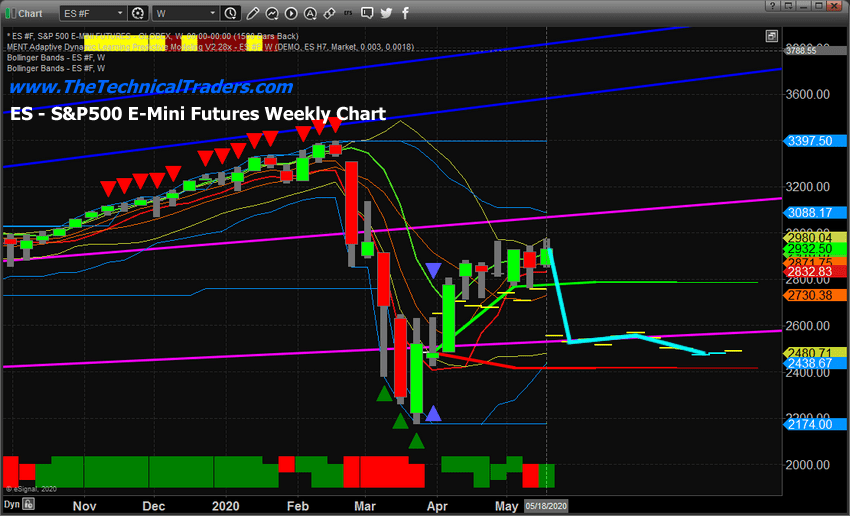

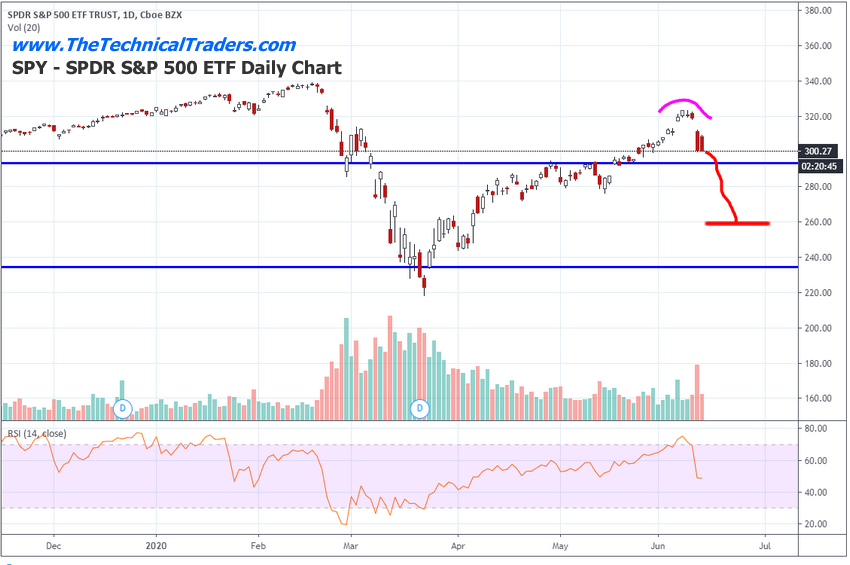

Our research team authored an article suggesting that our Adaptive Dynamic Learning Predictive Modeling system indicated the US major markets were 12% to 15% overvalued on May 23, 2020. This was just before the last “euphoric” phase of the recent rally took began the week after our prediction. From the date of May 23, 2020, to the recent peak in the markets, the SPY rallied another 9.72% above the price levels when we made the ADL prediction. This suggests that the major markets rallied to levels near 21% to 24% overvalued near the recent peak.

In keeping with our research team’s conclusions, the downside price move that initiated on Wednesday, June 10, 2020, after the US Fed statements, and really broke down on June 11, 2020, will likely continue resulting in the US major markets attempting to find support near our ADL predictive modeling system levels. The downside price trend could extend below our ADL price target levels if the selling in the markets pushes into an extreme selling event. It is not uncommon for the price to attempt to move through the ADL price levels attempting to find support and/or resistance.

This is the ES chart showing our ADL predictive modeling system results from the May 23, 2020 date. You can see the ADL predicted price levels near 2520 on this chart and the fact that the markets rallied away from these levels in late May created what we call a “price anomaly”. This is when price moves away from the ADL levels in a manner that is somewhat unreasonable. The same thing happened during the peak price level in early February 2018 and the October peak in 2018.

SPY ADL PREDICTED TARGET LEVEL DAILY

Based on our ADL predictive modeling system and the targeted price levels, we believe the SPY will fall to levels close to or below $260 over the next 10 to 15+ days. It makes perfect sense that the markets over-extended a speculative price rally based on the context that the US economy would rebound from the COVID-19 shutdown.

Now that the US Fed has deflated that expectation and the riots and other issues related to social and political events are pending, we believe a “sudden realization” within the markets could send the US stock market price levels much lower over the next 2+ weeks – eventually attempting to find support near recent lows.

We actually posted our technical forecast for the market crash, the 30% rally, and called this blow-off top and reversal 4 days before it happened in this video a while back.

Concluding Thoughts:

Remember, developing a winning strategy is not about trading every trend and day-trading every move, it is about timing your trades and strategically positioning your portfolio to take advantage of the “best asset now”. We’ve developed proprietary technology that assists us in determining the best assets to be invested in and our predictive modeling and other proprietary tools assist us in identifying confirmed trade triggers. Our objective is to assist our clients in generating consistent profits – not hundreds of trades.

If you were caught on the wrong side of this move recently, please remember that we tried to warn you of our multiple research articles and clear content. We’ve been warning that this upside rally was a speculative price move driven by foreign and US investors believing the V-shaped recovery was real. The reality of the situation is that this recovery is going to be much more volatile than many people believe. This is a global economic event – not just a Fed Blip or some other isolated panic volatility.

You better stay on top of these trends and risks in the markets to stay ahead of these bigger moves.

As a technical analyst and trader since 1997, I have been through a few bull/bear market cycles in stocks and commodities. I believe I have a good pulse on the market and timing key turning points for investing and short-term swing traders. 2020 is an incredible year for traders and investors. Don’t miss all the incredible trends and trade setups.

Subscribers of my Active ETF Swing Trading Newsletter had our trading accounts close at a new high watermark. We not only exited the equities market as it started to roll over in February, but we profited from the sell-off in a very controlled way with TLT bonds for a 20% gain. This week we closed out SPY ETF trade taking advantage of this bounce and entered a new trade with our account is at another all-time high value.

Ride my coattails as I navigate these financial markets and build wealth while others watch most of their retirement funds drop another 35-65% during the rest of this financial crisis going into late 2020 and early 2021.

Just think of this for a minute. While most of us have active trading accounts, what is even more important are our long-term investment and retirement accounts. Why? Because they are, in most cases, our largest store of wealth other than our homes, and if they are not protected during the next bear market, you could lose 25-50% or more of your net worth. The good news is we can preserve and even grow our long term capital when things get ugly like they are now and ill show you how. One of the best trades is one your financial advisor will never let you do because they do not make money from the trade/position but we do have a way for you or your advisor can take advantage of the market gyrations with our Technical Wealth Advisor investing signals.

If you have any type of retirement account and are looking for signals when to own equities, bonds, or cash, be sure to become a member of my Passive Long-Term ETF Investing Signals which we issued a new signal for subscribers.

Chris Vermeulen Chief Market Strategies Founder of Technical Traders Ltd.

Shares of Reata Pharmaceuticals traded 30% higher after reporting that Blackstone Life Sciences will invest $350 million in the company to advance bardoxolone methyl as a potential therapy for Alport syndrome and other rare and serious chronic kidney diseases.

Clinical-stage biopharmaceutical company Reata Pharmaceuticals Inc. (RETA:NASDAQ) and Blackstone Group Inc. (BX:NYSE) today announced that “funds managed by Blackstone Life Sciences will lead a $350 million royalty and equity investment in Reata to fund the development and potential commercialization of bardoxolone methyl, an investigational once-daily oral therapy being studied for chronic kidney disease (CKD) in Alport syndrome and autosomal dominant polycystic kidney disease (ADPKD).” The firms advised that these are life-threatening diseases with few or no effective U.S. Food and Drug Administration (FDA) approved therapies.

Global Head of Blackstone Life Sciences Nicholas Galakatos, Ph.D., stated, “This investment aligns with Blackstone Life Sciences’ mission to help advance promising new medicines to patients with high unmet needs. If approved, bardoxolone has the potential to provide for the first time a therapy that improves the quality of life for tens of thousands of patients around the world suffering from Alport syndrome.”

Reata’s CEO and President Warren Huff commented, “Bardoxolone has been a primary focus of our company’s research and development efforts to date…We are extremely pleased that Blackstone Life Sciences has recognized the potential of bardoxolone, and the potential of Reata more generally. We are proud to enter into this strategic investment agreement with Blackstone Life Sciences.”

Paris Panayiotopoulos, senior managing director of Blackstone Life Sciences, added, “Bringing the first potential therapy to Alport syndrome patients, a devastating genetic condition with no approved treatments, is very motivating…With this investment, we will support Reata in further developing bardoxolone for CKD in Alport syndrome, autosomal dominant polycystic kidney disease and multiple other chronic kidney diseases.”

Under the terms of the investment agreement, Blackstone Life Sciences will invest $300 million in Reata in return for certain royalty payments on worldwide bardoxolone net sales made by Reata and its licensees with the exception of sales by Kyowa Kirin Co. Ltd. As part of the deal, Blackstone Life Sciences will invest $50 million to buy 340,793 shares of Reata’s Class A common stock at a price of $146.72 per share. The transaction is expected to close on or before June 24, 2020, with Reata receiving the $350 million investment upon closing.

Reata’s COO and CFO Manmeet S. Soni remarked, “This $350 million financing further strengthens Reata’s balance sheet, and extends Reata’s cash runway through the end of 2023. It positions us to make strategic investments to further expand our development and commercial capabilities in preparation for the potential approval and launch of our drugs.”

The company explained that “bardoxolone methyl is an investigational, oral, once-daily activator of Nrf2, a transcription factor that induces molecular pathways that promote the resolution of inflammation by restoring mitochondrial function, reducing oxidative stress, and inhibiting pro-inflammatory signaling, and that the FDA has granted Orphan Drug designation to bardoxolone for the treatment of Alport syndrome and ADPKD.”

Reata Pharmaceuticals is a clinical-stage biopharmaceutical company based in Plano, Tex., that focuses on developing medicines for patients with serious or life-threatening diseases. The firm’s therapeutics target molecular pathways that are involved regulation of cellular metabolism and inflammation.

Blackstone Life Sciences is a private, global investment firm that invests in numerous companies and products in the life science sectors.

Reata Pharmaceuticals has a market capitalization of around $4.4 billion with approximately 33.24 million shares outstanding and a short interest of about 11%. RETA shares opened 26% higher today at $165.00 (+$34.08, +26.03%) over yesterday’s $130.92 closing price. The stock has traded today between $156.99 and $177.48 per share and is currently trading at $171.24 (+$40.32, +30.80%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

– The Federal Reserve has become more aggressive again, after several years of acting docile. As you can see on this chart of the Fed’s balance sheet, it has very rapidly expanded from a baseline from (prior to) 2015 through 2018, of about $4.4 trillion. After which, it had attempted to taper, getting down to $3.8 trillion last summer. Then it was obliged to reverse itself well before responding to the COVID lockdown. Since then, its balance sheet has gone vertical.

More is expected to come. So, needless to say, more of what people call inflation—that is, rising prices—is expected to come. Never mind that in 1983, a pair of Levis 501 jeans was $50 (Keith remembers paying that price at that time) and today, the price is $35.70 at Levis.com. After 37 years of relentless—and increasingly rapid—increase in the quantity of dollars, the price of blue jeans has dropped 25%. Did we mention that crude has had not one, but two crashes in the last 6 years?

As an aside, when critics of the Fed give the impression that the main evil committed by the central bank—if not the only evil—is to cause prices to rise, and then prices do not rise, they give the impression that the Fed is doing alright. It’s not alright, as this chart shows.

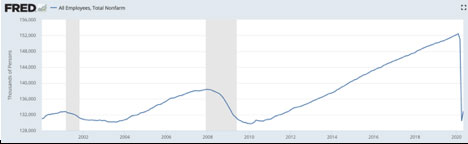

During the last debt crisis, the economy shed all of the jobs it created since the previous crisis. And now (notwithstanding there’s no grey shading yet, indicating recession) all of the jobs created since both 2009 and 2002 are gone. More will be going, when many business owners run out of money or throw in the towel. And more, when the so called Payroll Protection Plan stops subsidizing jobs for workers who are not producing enough to cover the cost of employing them.

This graph suggests that all the jobs created since 2000 were fueled by the Fed’s falling interest rates. Such jobs would be in capital-consuming industries, and not sustainable. We say this because every such job has evaporated in a time of credit crisis, in 2001, 2008, and 2020 (and we know that cutting the interest rate does juice up GDP, but activity that depends on falling rates is not sustainable.)

So today in 2020, despite a larger population and workers able to work later into their golden years (and forced to, by economic circumstances), the economy is not able to employ more workers than it did in 2000. The Fed (along with other government policies) has caused enormous discoordination. People still want to consume more, and most unemployed people want to work, but government has built a wall keeping these two groups apart.

Speaking of employment, Monetary Metals is creating value and growing—we are hiring a bookkeeper. Please contact us if interested.

It’s All About the Debt

This brings us to today’s topic. The flip side of the dollar is debt. Perhaps because people think of the dollar as money, they picture the Fed printing and skip over a Grand Canyon of faulty assumptions and unwarranted inferences to the idea that people somehow have more money to chase the same goods, and hence bid up prices. So let’s cut through this fallacy.

When the Fed creates more dollars, none of them appear in your pocket.

They do not get into the pocket of your neighbor, either. No, not even the rich guy down the street who is always driving a new Ferrari. That is not how it works.

The Fed does not gift free money to the people. It does not drop bags of cash from helicopters, notwithstanding disingenuous comments by a former Fed Chairman. It does not even give free cash to the big banks.

The Fed buys assets from them. Historically it bought Treasury bonds, but now its appetite has expanded to include mortgage bonds, corporate bonds, and municipal bonds.

To help clarify our point, let’s go through the mechanics of this. Step one, a commercial bank borrows $1 million. Step two, the bank buys a bond. That is, it gives up $1 million in cash, and gets a $1 million bond in exchange. Step three, the Fed borrows $1 million. Step four, it buys the bond. That is, it gives up $1 million in cash to the commercial bank, and gets the $1 million bond in exchange.

The act of borrowing and the act of buying are combined in one step with the Fed. It’s simple but it’s so hard to see, because people think of the dollar as money. However, the dollar is actually the Fed’s liability. When a bank sells a bond to the Fed, it prefers the Fed’s liability to the bond. If the bond is a Treasury bond, then why would the bank prefer the Fed’s credit to the Treasury’s credit?

There is not so much difference between the two. Both are government credit. The Treasury pays interest (barely) and has a maturity that is a date in the future. By law, the Fed’s credit is a current asset, that is, zero maturity. And it may be used to pay all debts.

To sell a bond is to exchange one credit paper for another.

This act does not provide free value to either party (though the Fed generally buys on an uptick in price, which is a downtick in interest rates, so there is a little capital gain). No one finds money that just appeared in his pocket. Hordes of people are not dollared-up, running out to stores to throw more dollars after the same goods.

This picture, evoked by the Quantity Theory of Money, is not a picture of reality the way Hogwarts is not a picture of a real school.

It’s hard to wrap your head around the idea that the Fed borrows from everyone who demands what they think is money. The Fed does not print out of thin air, it borrows from everyone. People willingly—happily—lend to the Fed. Because they think they are getting money!

Carl Sagan expressed it succinctly:

“One of the saddest lessons of history is this: If we’ve been bamboozled long enough, we tend to reject any evidence of the bamboozle.”

The Argument for the Rising Demand for Cash

Many economists would respond to the above, and say, “well, prices wouldn’t rise if demand for money increased along with the quantity.” There is a grain of truth to this.

The desire (or need) to hold a cash balance is rising. This is not due primarily to the rise in quantity of dollars. Nor to Keynes’ so called animal spirts. It is due to two facts. It is the rising quantity of debt times the rising net present value of each dollar of debt.

Suppose you own a small print shop, free and clear. No debt. How much cash do you need to hold? Perhaps two or three months of expenses, would be a guess.

And suppose your competitor across the street has an identical shop, but owes $1 million. How much cash does he need to have? Before answering that, suppose it is short-term debt. He is obliged to roll it over every six months. He incurs the risk that when he needs to refinance a note, the market may not be willing. Therefore, we can be certain that he needs a lot more cash than you do.

Now consider a bank. When the average interest rate earned by the bank is 8%, and the bank is paying 4%, it earns a net spread of 4%. If the bank has $1 billion in assets, it is earning $40 million a year. But the interest rate falls and falls and falls. Today, a bank is paying close to 0% to savers but it is lucky if it can earn 1%. The same billion dollars in assets earns less than $10 million. So in order for the bank to make the same $40 million a year, it has to lever up. It needs over $4 billion in assets, compared to the $1 billion it needed previously.

This is why its baseline need for cash is probably four times higher. But what about when there are problems in the land of credit? Today, we know that many residential and commercial property owners are not paying their mortgages. While businesses are trying to draw down credit facilities, there are many who are in default. Banks need more liquidity. More cash.

So they exchange their bonds for cash. Not to spend the cash bidding up the price of everything from avocadoes to Zoom video calls. But to meet their obligations, and avoid being forced into bankruptcy.

The Math of Rising Demand for Cash

As the interest rate falls, everyone has both means and motive to borrow more. The means is that the monthly payment is lower. The motive is as we saw with the bank. When the rate of return drops, you need more assets to generate the same profit. You must borrow more to build or buy more assets.

So debt rises.

At the same time, the net present value of each dollar of debt also rises. All future payments on the debt must be discounted to calculate the present value. They are discounted at the market interest rate. So when the rate fell from 8% to 4%, the NPV of all extant debt doubled. And from 4% to 2%, another double. And so on.

This reflects the falling profit margin as more businesses borrow to add more capacity. They have to work harder and harder for the same net dollar of income. Older readers will remember restaurants before 2007, on Thursday through Sunday nights they handed out pagers and would page you when your table was ready. We don’t refer only to trendy midtown Manhattan or West End eateries. This was any decent restaurant even in suburbia. Today (even before the virus), most restaurants are not filling all the tables even on Friday nights.

Carmakers (even before the virus) were advertising 0% for 72 months (even when the Fed thought it should try hiking rates).

It is twice as hard to earn a dollar of free cash flow to pay down a debt, when the prevailing rate is 4%, compared to when it is 8%.

Unusual Behavior in the Silver Market

In our thoughtful disagreement with Ted Butler, we proved that there is no large-scale selling of futures to suppress the price. Our proof was that the basis falls as each futures contract heads into expiration. If the manipulators had a large futures position to suppress the price—a short position—then they would have to close their contracts before contract expiry.

To close a short futures contract position, you buy that contract.

Remember, these manipulators would have to buy with urgency, as the conspiracy theory says they have not got the metal to deliver. And keep in mind that this buying would be massive. A short position large enough to keep the price down would have to be bought back in a short period of time. It would push up the price of the expiring contract, relative to the price of physical metal (and farther-out futures).

Basis = future – spot

If the conspiracy theory were true, then the basis would rise as each contract headed into expiry. But we showed the data for every silver contract since 1996 (and every gold contract here). The basis of every one of them goes down as they approach expiry. This means that short-sellers are arbitragers, buying spot and selling future. And it is the long positions that must be closed before expiry (because most longs do not have the cash to pay for the metal and take delivery).

Incidentally, although Mr. Butler asked for thoughtful disagreement and said he was looking to check his premises, he did not respond to our argument and data.

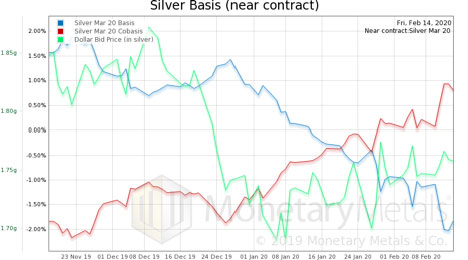

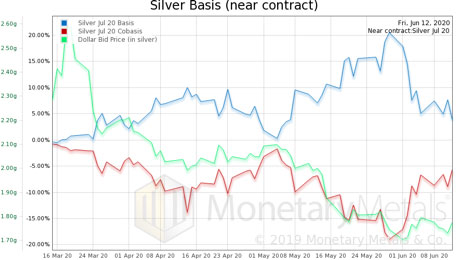

The March contract this year behaved normally.

The basis ends up around -2% by mid-February.

But here is the July contract.

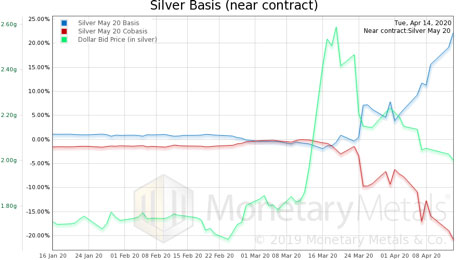

Note something odd. Until June 1, the basis was rising. Then it fell. And now look at the May contract.

The basis rises all the way up to a few weeks before expiry, ultimately hitting over 20% (annualized). If you look at the chart in the Butler response article, you see there is no historical precedent for this (at least in the last 24 years).

Does this mean that there was a silver manipulation cartel who had to begin unloading a massive silver short position around mid-March, and which cleared out by the end of May? Obviously not, as this was a period when the silver price rose from about $12 to about $18.

We think the rising basis heading into expiry signifies the absence of the arbitragers. When speculators bought metal to bet on the rising price, there was no market maker to sell short a new contract and arbitrage the widening spread to spot silver.

And if we look at the simple fact of the basis being 22%, there is no reason why it should get to even a quarter of that level, in a world where the 10-year government bond—deemed risk-free—was paying 0.5%. Except if the would-be arbitragers were absent.

Now, the market is slowly returning to normal, as the July contract shows. The basis is down to under 4%. If the market offers a risk-free profit, someone will take it.

Gold had a rising basis through April 13, but it was not as extreme as in silver, nor as long-lived. The gold basis is now 2.4%, which is still elevated but not so remarkable.

One last thing needs to be said about the high silver basis. If you want the price to rise, you should want a low basis. Why?

The basis is the cost of carry, to those who prefer to hold their metal position in the futures market. The higher this cost, the stronger the disincentive to hold the position. For market participants who cannot or will not stack coins—hedge funds, family offices, etc.—they may have to close their silver positions (of course, we believe they should invest their metal Monetary Metals, which not only avoids the cost of carry but pays interest).

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

June 15, 2020 – Limassol, Cyprus – RoboForex, the company that provides brokerage services for trading on global financial markets, has received an award in the nomination “Best Global Mobile Trading App 2020”, which is presented for mobile applications for trading within the frameworks of “Global Forex Awards”.

Every year, Global Forex Awards organizers present awards to the companies, which demonstrate outstanding results in providing services on the Forex market. From April 1st to 29th, there was open voting on the organizer’s website, where anybody who wanted to could vote for a certain company from Asia, Europe, and the Middle East in various categories. The winners were announced and rewarded on June 5th, 2020.

Global Forex Awards are presented to the best companies and brands of the Forex market, both globally and regionally. They are awarded to the forex brokers that implement the most advanced and cutting-edge technologies, apply complex market research tools and progressive educational programs, and introduce up-to-date business solutions to provide clients with top-class services.

Denis Golomedov, Chief Marketing Officer at RoboForex: “We’re very pleased to receive this award. Nowadays, many familiar aspects of the world around us are changing, including consumer tastes and needs. Mobile devices have already made great changes in approaches to business development in many areas of the economy and industry. Trading is also developing by leaps and bounds, that’s why it’s very important for the Company to have mobile products that allow traders to perform trading operations from anywhere in the world on the conditions similar to fully-functional desktop platforms”.

About RoboForex

RoboForex Ltd is a company, which delivers brokerage services. The company provides traders, who work on financial markets, with access to its proprietary trading platforms. RoboForex Ltd has the brokerage license IFSC/60/271/TS. More detailed information about the Company’s activities and operations can be found on the official website at roboforex.com.

Bullion premiums drifted lower last week in response to slightly reduced buying demand and a few more investors selling.

Whether this continues will likely depend on stock prices which have rallied relentlessly since March. Many U.S. investors still assume the equity markets are a good indicator for where the economy is headed. They see the rally as evidence that a V-shaped economic recovery lies just ahead.

Other equity investors simply aren’t worried about nosebleed valuations or lousy fundamentals. They just know the Federal Reserve has their back.

Either way investors are less panicked than they were a month or two ago, and demand for physical gold and silver has eased a bit.

This reduction in fear coupled with higher gold and silver prices prompted a few more people to sell bullion back into the secondary market. Private mints and refiners are also gradually adding capacity. The supply outlook is better today than it has been in months.

Premiums fell on many silver rounds and bars, as well as 90% silver coins. It is now possible to buy these products between $2 to $3/oz over the spot price at Money Metals (but not necessarily elsewhere). This is better than the $4 to $5/oz premiums seen in recent weeks, though not as low as the sub-$1 premiums seen back in February.

Silver American Eagles are a bit of an exception, particularly for the 2020 date coins. Premiums for these popular coins remain high as the U.S. Mint still struggles to keep up with demand.

Bullion buying may have weakened from the frenetic levels seen in recent weeks, but it remains at least double its levels from January and February.

Meanwhile, many of Money Metals’ competitors continue to struggle mightily in sourcing items for inventory or shipping promptly – a frustrating situation that continues to drive investors to Money Metals Exchange as their new dealer.

Vault Gold, Vault Silver, and Vault Platinum remain the lowest cost options for investors who don’t mind storing with Money Metals Depository. It is also possible to make very large purchases in both of these items.

Where premiums head from here will depend heavily on what investors see in the news. If the current social unrest escalates, or economic troubles such as unemployment start weighing heavily on investor sentiment, expect Americans to buy even more gold and guns.

Anyone who is planning to buy bullion and waiting for premiums to drop might want to grab the opportunity now in case prices soon zoom higher.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

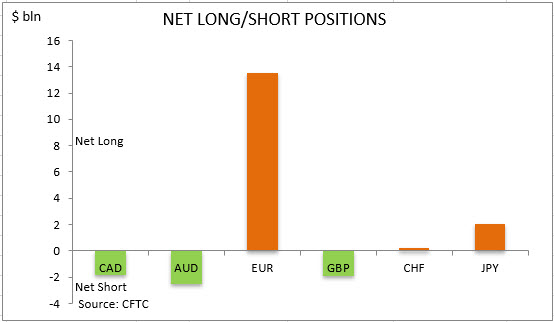

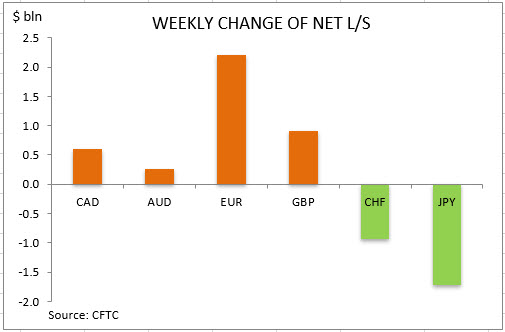

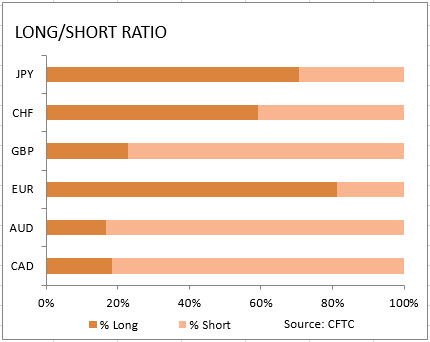

US dollar net short bets rebounded to $9.51 billion from $8.18 against the major currencies during the one week period, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to June 9 and released on Friday June 12. The change in overall dollar position resulted mainly due to significant decrease in bearish bets on Canadian and Australian dollars as well as British Pound. A significant increase in bullish bets on euro also contributed to increase in dollar bearish bets after the European Central Bank announced it would expand its Pandemic Emergency Purchase Program by €600 billion, or $674.5 billion and extend the program until June 2021 as the ECB kept interest rates unchanged. The Pound, Canadian and Australian dollars maintained net short positions against the dollar. The bearish dollar bets rose despite US Labor department surprise jobs report showing US economy regained 2.5 million jobs in May and the unemployment rate fell to 13.3%.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Sterling weakened against the Dollar and most G10 currencies on Monday as fears over a second wave of coronavirus drained risk sentiment.

The chronic uncertainty revolving around Brexit negotiations and the uncertain outlook for the UK economy added to the growing list of themes haunting investor attraction towards the Pound. With the GBPUSD tumbling to a two-week low below 1.2460, could further downside be on the cards over the coming weeks?

Looking at the daily charts, the GBPUSD is under pressure with prices struggling to break above the 1.2600 resistance level. Sustained weakness below this level may open a clean path back towards 1.2450. If 1.2600 proves to be unreliable resistance, prices may jump towards 1.2700.

Commodity spotlight – Gold

Gold entered the week on the wrong side of the bed, tumbling over 1% despite the resurgence of coronavirus cases in China and parts of the United States.

For those who may be wondering why Gold has depreciated despite the risk-off mood, the answer may be found in the Dollar’s performance. The Greenback seems to be back in fashion amid fears of a second wave of coronavirus destabilizing global growth and stability. If king Dollar continues to steal Gold’s safe-haven flows, the precious metal may become depressed and unloved in the short to medium term.

Prices have already tumbled over 1% on Monday with the downside momentum seen opening a path back towards $1700. If this psychological level proves to be unreliable support, Gold may test $1670.

All hope is not lost for bulls, especially when factoring how Gold remains in a very wide range with support at $1670 and resistance at $1747. A breakout above this resistance level could inspire an incline towards $176 and $1800, respectively.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.