Investors who have been “paying attention” have been topping–up their investment portfolios and will continue to do so, says the CEO of one of the world’s largest independent financial advisory and fintech organizations.

The comments from Nigel Green, the chief executive and founder of deVere Group, which has $12bn under advisement, come as stock markets around the world further rallied on Tuesday after the U.S. Federal Reserve announced an expansion to its historic stimulus programme.

Mr Green affirms: “Global stocks have been buoyed by the news from the Fed – the world’s de facto central bank – to buy individual corporate bonds in addition to the exchange-traded funds it is already purchasing, to support the world’s largest economy.

“This extra stimulus acts as a ‘backstop’ or ‘floor’ for equities.

“The additional Fed support was widely expected by the markets and therefore, investors who have been paying attention have been topping-up their investment portfolios recently as entry points will inevitably continue to go higher as we move forward.”

He continues: “It is likely that savvy investors will continue to enhance portfolios as the backing is likely to be maintained for years, not quarters.

“Also, it has been reported that President Donald Trump’s administration is preparing to unveil a $1 trillion infrastructure package. This will further boost asset prices.”

The deVere boss called the additional measures last week.

He noted on Thursday June 11: “Further stimulus can be expected from the Fed – and also perhaps from Congress too – in the near future… This will support and likely boost asset prices moving forward. Investors will now be eyeing the opportunities before any fresh or enhanced stimulus packages are announced.”

London’s FTSE 100 and Frankfurt’s Dax both jumped 2.2% in morning trading on Tuesday, the pan-European Euro Stoxx 600 gained 2%. U.S. futures markets suggested that U.S. stocks would rise further when trading begins on Wall Street, with S&P 500 futures up 1%.

In Asia-Pacific, Tokyo’s Topix shot up 4% and Australia’s S&P/ASX 200 gained 3.9%. Meanwhile, Hong Kong’s Hang Seng rose 2.4% while China’s CSI 300 index was 1.5% higher.

Nigel Green concludes: “Few things can fuel markets like another stimulus injection.

“The message investors are taking away is that the U.S. central bank and government are prepared to do whatever it takes to support the recovery.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

Some of the recent economic indicators are lining up with what we saw in Japan in the late ’80s, prior to the massive stock crash which led to what’s known as “the Lost Decade”.

It’s wise to pay attention to some of the warning signs that might be out there.

The collapse of the Japanese stock market in the early ’90s should always be in the mind of equities traders. Not just because it was dramatic, but even almost thirty years later and massive amounts of fiscal stimulus, the Nikkei has still not recovered.

This goes against conventional wisdom for investment that indices, on average, grow over the long term.

Why We Should Worry

Generally, the cause of the Japanese Asset Bubble (and subsequent burst) is still a subject of extensive debate. In fact, as GB Shaw said, “if you laid out all the economists in a row, they’d never reach a conclusion.”

However, the main consensus is that stock prices moved higher, well out of proportion to their underlying value. This was partially due to a lack of action by the BOJ, coupled with a significant expansion of the monetary base.

Today, we see stock valuations in the tech sector well beyond reason. There are also unprecedented levels of margin in the market, and central banks are desperately pushing money into the market.

Those are not the uncanny similarities, though.

Tears in the Rain

The ’80s saw a rise in expectations that Japan would become the world’s economic powerhouse.

In fact, you could see it in the movies of the time. In Blade Runner, for example, the future is portrayed as a mixture of English and Japanese.

Japan, in many ways, occupied the same place as China does today. It was a massive exporter and manufacturing base.

In fact, the US allegedly put pressure on Japan to increase the yen in order to reduce the trade deficit. Japan at the time was the largest holder of US treasuries. It wasn’t a trade war in the form of tariffs, but it was a political trade policy nonetheless.

What Could Happen?

Of course, the world today isn’t exactly the same. However, in the interest of being prepared, what could happen if there were a similar asset burst, but this time in the whole world?

The most vulnerable index would be the Nasdaq because it is the heaviest in overvalued tech stocks. The third-largest component – Amazon – doesn’t even pay a dividend, and trades at a P/E ratio of 122.

The more diverse S&P 500 would fare better, with companies having more reasonable earnings ratios offsetting some of the losses. Ironically, some of the less solid stocks could perform better, simply because they are less leveraged.

A Bursting Bubble Lets Out Excess Margin

The DJIA might initially have a steep decline because, as all of its components are blue-chip, brokerages allow higher levels of margin investing. But the index could recover quite quickly since the components have solid valuations.

As indices rise in the middle of a pandemic and decreasing revenue for most companies, people will likely keep fretting that the stock market is disconnected from reality.

The big test will be when the central banks have to stop the flow of infinite money which is propping up stock prices.

The euro is up, in an attempt to reverse losses from last Thursday and Friday.

Price action rebounded after slipping below the 1.2616 level, which is now serving as support.

While the near term outlook remains to the downside, price action remains at a critical level.

A close above 1.1347 will potentially put the euro back to the 11th of June highs.

This will then put the EURUSD back in sight within the 1.1400 price level.

To the downside, watch for a reversal below 1.1347. If price fails to post further gains, we expect the correction to resume.

GBPUSD Rebounds Off Support, Will Price Go Higher?

The British pound sterling is posting gains after the support level near 1.2516 is holding up.

The rebound remains in line with the view of a retracement ahead of a correction. The downside bias remains as long as GBPUSD is trading below the upper resistance level of 1.2643.

In the event that price breakouts above this level, we expect the bullish momentum to continue pushing higher.

However, in the near term, we expect prices to remain range-bound within the said levels.

A breakout off these levels will potentially determine the direction of the trend.

WTI Crude Oil Holds Steady Above 34.42 Technical Support

Crude oil prices are posting modest gains, up over 1.4% on the day.

This rebound comes after prices held up near the 34.42 technical support.

To the upside, WTI crude oil is approaching the price level of 37.67.

A breakout above this level will potentially set the stage for a move toward the 40.00 handle.

The potential of a double bottom pattern near the 34.42 level also adds to the bullish upside.

In the event of price failing to rise above 37.67, we expect some consolidation to take place. This will also potentially put pressure on the support area as well.

Gold Prices Continue To Consolidate Near Highs

The recent reversal in gold prices has pushed the precious metal close to the previous highs.

Price action reversed direction, just a few points above the technical support of 1700.00.

For the moment, price action is testing the price level of 1724.62.

A close above this level could potentially push gold prices to the next key target of 1747.00. We expect the consolidation to continue overall in the near term.

The UK lockdown measures were eased yet again this week, and the UK continues to move further along the stages towards total freedom.

Boris Johnson announced that as of Monday, June 15th, all non-essential retailers in the UK will be allowed to re-open. This is provided they implement strict social distancing measures and make an effort to maintain the health and safety of the public.

The easing comes three months on from the beginning of lockdown in March. It also comes three weeks after UK citizens were given the green light to meet members of other households on an outdoor one-to-one basis only.

UK GDP Suffers Record Fall

There has been growing pressure over recent weeks for the government to relax the economic restrictions.

These restrictions have caused shops to sit shuttered around the country. Meanwhile, the UK GDP is plummeting at a record 20.4% in April as a result. As such, many within the business community have warned that any further delay in reopening risks colossal financial damage.

Q1 GDP came in at -2%. This means that should a second negative quarterly reading come up in Q2, it would confirm a technical recession.

The government is now hoping that the economic recovery will start to gather pace as people return to retail centers.

Risks To The Recovery

However, there are still big question marks over how readily the public will engage with businesses once they are reopened. This will all depend on the level of caution among the general population as the UK death toll has surpassed 40k.

Many non-essential retailers (such as galleries, indoor markets, betting shops etc) have reopened. However, other parts of the economy (such as pubs, dine-in restaurants, gyms, and hairdressers) remain closed until at least July.

This means that even with a high level of activity among reopened businesses, the UK economy will still be operating at a greatly reduced capacity.

Furthermore, there are still many concerns among health authorities regarding the potential for a second wave. This is especially concerning considering the steady increases in infection numbers in the US since reopening began there a few weeks ago.

Next Review July 4th

July 4th is the date of the next review. At that point, expectations are for the government to announce the reopening of pubs and restaurants. This, of course, is provided there is no fresh spike in the virus ahead of that time.

The hospitality sector remains the trickiest call to make for the government given the inherent risks of socializing. But, as the death toll continues to slow in the UK, the business community remains hopeful that July will mark the start of the slow return to business as usual.

However, that move also saw a sharp reversal, and price is now back under the level. While below here, a further rotation lower cannot be ruled out. However, if buyers can break back above the level, focus will turn to the 1.32 region next.

– In the coming months, success or failure to contain the global pandemic and overcome the coronavirus contraction has potential to make or break the promise of Southeast Asia in the early 21st century.

By the end of the 2nd quarter, the total number of confirmed cases may total close to 10 million, while deaths could surpass 225,000. What was an epidemic in China at the turn of January and February grew into a pandemic in the 1st quarter, due to the belated and inadequate mobilizations in the US and Europe.

In early year, the epicenter of the virus was in China and the rest of Asia. By March-April, it had moved to Europe and the United States. As I projected three months ago, global devastation would escalate by summer as the epicenter is shifting to emerging and particularly developing economies.

The human costs of the global pandemic are mirrored by historical economic damage. As I predicted in early March, the economic impact of the coronavirus contraction would be comparable to the 1930s Great Depression. Recent World Bank data confirms the projection. The current baseline forecast envisions a whopping 5.2% contraction in global GDP in 2020.

The net effect will be the deepest global recession in eight decades, despite unprecedented policy support. As a result, per capita incomes and living standards in most emerging and developing economies will shrink this year. Meanwhile, across the world, economies are easing lockdown measures, trying to bring relief to those whose livelihoods have been drastically disrupted.

In Southeast Asia, the economic fallout has barely begun.

Pandemic impact on Southeast Asia

In the coming months, emerging and developing economies will seek to cope with the coming economic tsunami. With weaker healthcare systems, the poorest economies will take the heaviest hit. The populous economies in Southeast Asia – Indonesia, Philippines, Thailand and Vietnam, or the ‘ASEAN-4’ – are not an exception.

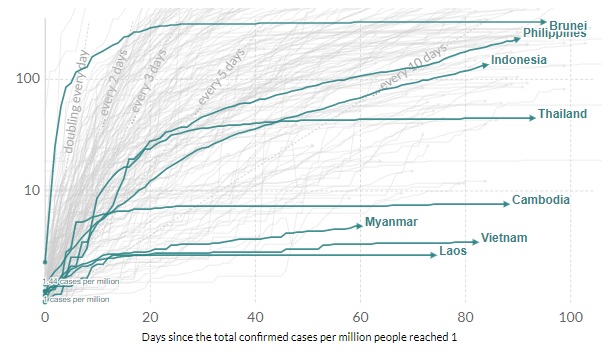

Among the ASEAN-4, the epidemic started with only 50 confirmed cases at the end of January. Yet, at the end of June, that figure is likely to be closer to 90,000. In five months, it has increased by more than 1,650 times.

At the end of the first quarter, Philippines was worst hit (2,084 confirmed cases), followed by Thailand (1,651), Indonesia (1,528) and Vietnam (212).

By the end of the 2nd quarter – that is, June 30 – the largest case counts are likely to be in Indonesia (over 52,000), followed by Philippines (over 32,000), Thailand (3,200) and Vietnam (some 340) (Figure 1).

Figure 1Cumulative confirmed cases in ASEAN-4

Source: WHO data, Difference Group

Relative to the population size (total cases/1m pop), the pandemic impact among the ASEAN-4 has been hardest in the Philippines and Indonesia, where the cases are still on the rise, followed by Thailand and, far behind, Vietnam (Figure 2).

Figure 2Total confirmed COVID-19 cases in selected ASEAN countries*

* Log.

Source: European CDC, Difference Group, Jan 26 – Jun 13, 2020

These comparisons rely on the assumption that the figures are valid. One way to assess that validity is testing. The more countries test, the more accurately the cases will reflect the actual impact, while the reverse applies as well.

Usually upper-middle-income countries, such as Thailand, have greater testing capacity than lower-middle income economies, such as the rest of ASEAN-4. Indeed, the intensity of testing (i.e., testing per 1 million people) across ASEAN-4 suggests that currently Thailand is testing most aggressively (about 6,700), followed by Philippines (4,500), Vietnam (2,800) and Indonesia (1,800).

Internationally, Vietnam has been portrayed as a pandemic success story, due to its low number of cases. The presumed success has been attributed to rigorous testing, young population, contract tracing and isolation. Yet, realities are different.

In fact, testing intensity suggests Vietnam is at par with Bangladesh and Mexico; there is little rigorous about it. Nor is young population a reason for the success. Median age in Vietnam (31) is slightly higher than in Indonesia (30) and far higher than in Philippines (24). That leaves contract tracing and isolation, which have been called “repressive” by critics.

Those countries that test relatively less are more likely to see new virus waves and residual clusters in the future. Moreover, they will face new challenges as the economy begins to ease lockdown measures and tourism will pick up. Such countries may also see surges in mortality rates, which may not be attributed to the pandemic, but to “pre-existing pulmonary conditions” and so on.

Economic impact on Southeast Asia

As the outbreak has spread, the disruption of supply chains and temporary plant shutdowns, coupled with a sudden full stop in global demand, weigh heavily on those ASEAN economies that rely on export-led growth, remittances, tourism and travel, retail, and so on.

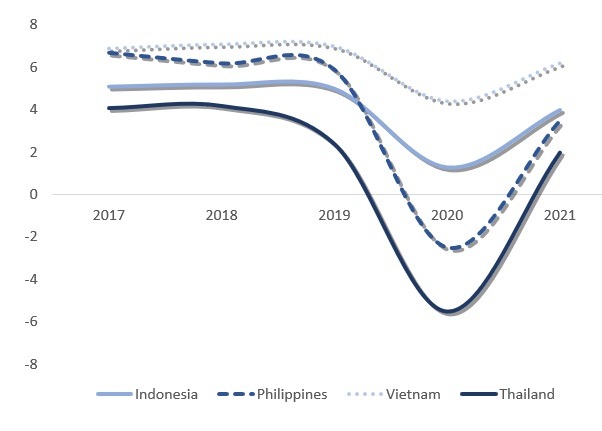

After the first quarter, the expectation was that ASEAN-4 will all suffer a severe growth contraction in the 2nd quarter that will cast a long shadow over the year.

In Indonesia, the contraction would result in a plunge from 5.0% in 2019 to 0.5% in 2020; in the Philippines, from 5.9% to 0.6%; and in Thailand, from 2.4% to -6.7%, respectively. Better positioned, Vietnam’s GDP growth was expected to fall from 7.0% to 2.7%, if it could minimize the virus impact at home.

Only one quarter later, the expected plunge in 2020 has deteriorated in the Philippines, which is expected to enter negative territory (-2.5%). In Thailand, the plunge will be worse (-5.5%) but slightly improved from a quarter before. Indonesia (1.3%) and Vietnam (4.4%) would do better than expected a quarter ago (Figure 3).

Assuming a relatively strong rebound scenario, ASEAN economies could have a V-shaped rebound by 2021, when Vietnam and Indonesia (4 to 6%) could perform significantly better than Philippines and Thailand (3 to 4%)

However, since Indonesia and Vietnam have not tested adequately, economic performance in the two countries could face new downside risks if the pandemic may linger longer than expected. Conversely, Philippines and Thailand could benefit from upside risks, if they manage to keep the virus in check in the near future.

In Indonesia, external risks are cushioned but only to a degree by a narrowing current account deficit and increases in foreign-exchange reserves. As the country is easing the lockdown, recovery relies on the containment of further infection spread.

As Vietnam, as well as Singapore and Malaysia, have discovered, two years of trade wars and a few months of a global pandemic can undermine a decade of export recovery. In turn, countries that depend on both tourism and exports (Vietnam, Singapore, Malaysia) must cope with longer-term economic malaise.

In Thailand, the restart of the economy will be phased and should bring some relief in the second half of the year. Yet, recovery is likely to prove slow, due to the plunge in tourism and weakness in trade. Meanwhile, the central bank will try to keep the Thai baht below 30 per US dollar.

Philippines could have been better positioned against the crisis, but that advantage was largely lost with the 2019 budget debacle. It delayed the government’s vital infrastructure investment program, which now faces far tougher economic conditions.

Domestically, Philippines, too, must balance between targeted quarantines and gradual exit from the lockdown. In turn, consumption cannot thrive as long as supply remains limited and demand is restricted. Internationally, economic turmoil will affect Philippines through slower inflows of foreign investment, weaker export performance and significant reduction of remittances.

Margin for error slim to nil

Moreover, even the current baseline scenario could prove too optimistic. The challenges in the West could linger, while the devastation in emerging and developing economies could spill over the latter half of the year. In the US, Europe and elsewhere, new virus waves and residual clusters could ensue, while imported infections could accelerate toward 2020-21.

In turn, the development of vaccine and viral therapies could take longer than expected, while US tariff wars might pick up against China, Japan and South Korea, even Europe. And as the heavily-indebted advanced economies are now taking record-volumes of new debt to support their economies, they could face new debt crises, which would spill over to poorer countries.

In the near future, Southeast Asia will face the greatest risks (and opportunities) since World War II. The margin for error in pandemic containment and economic policies is now slim to nil.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

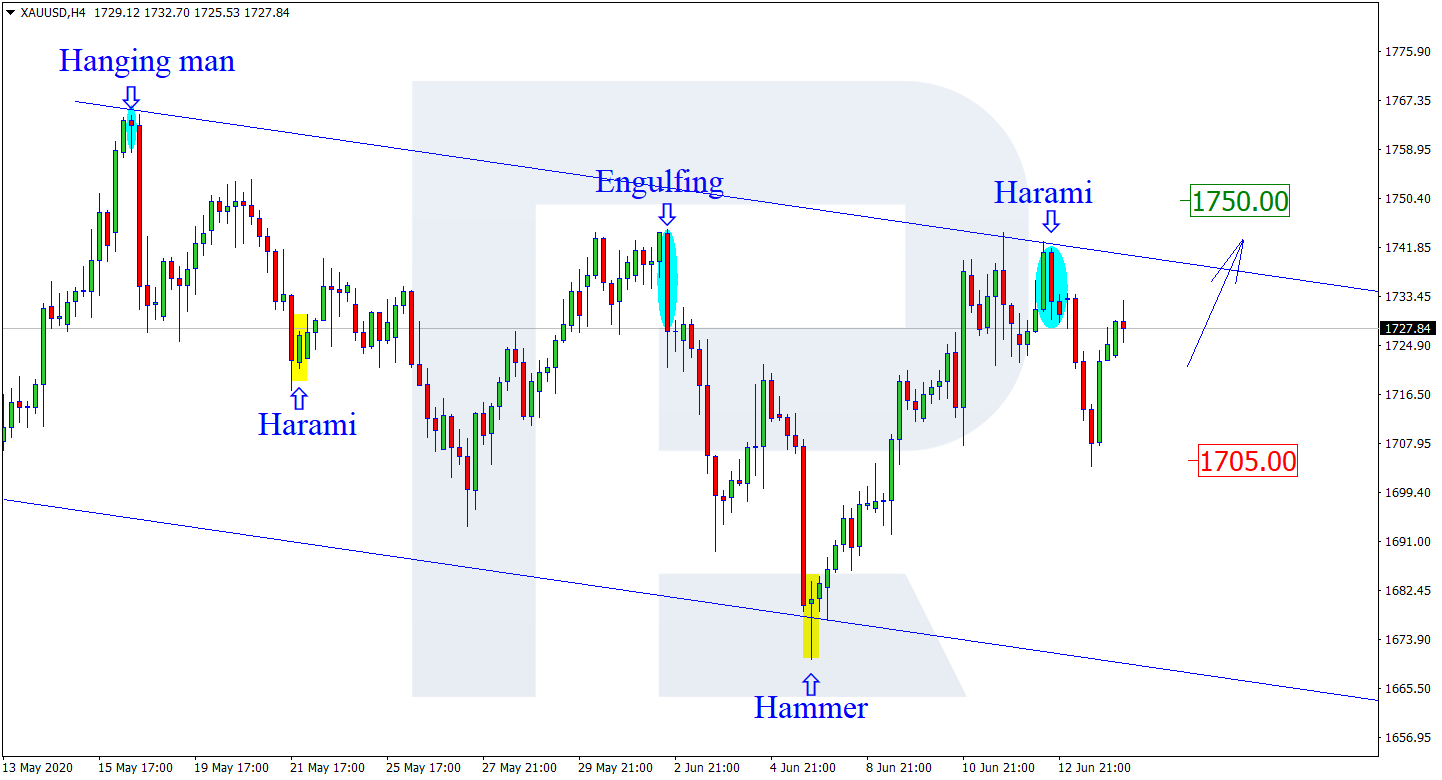

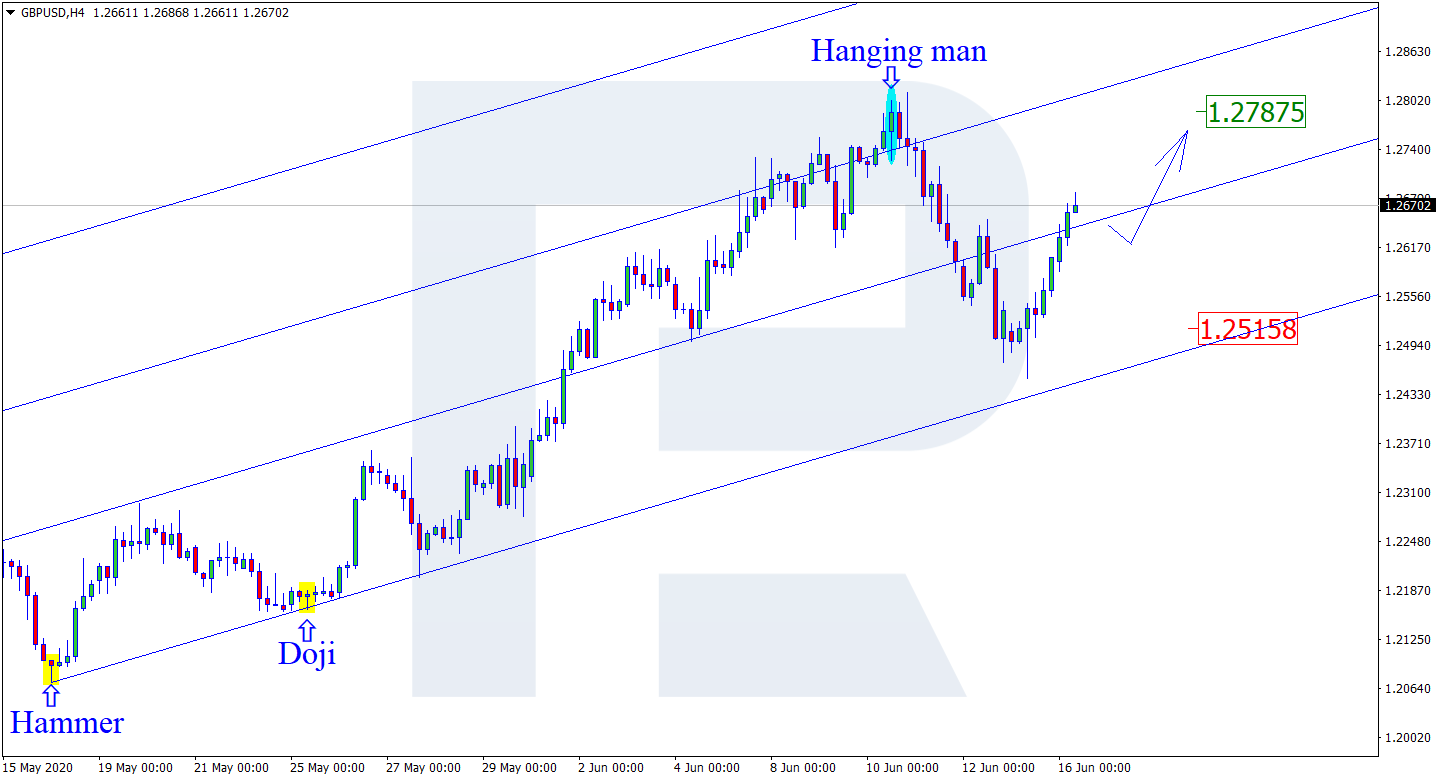

As we can see in the H4 chart, after testing the resistance level, forming a Harami pattern, and then reversing, XAUUSD has tested 1705.00 and rebounded from the support level. The current upside target is the resistance level at 1750.00. If the price continues growing, it may reach the next resistance area at 1760.00. At the same time, there might be another scenario, according to which the instrument may return to the support level at 1705.00.

NZDUSD, “New Zealand vs. US Dollar”

As we can see in the H4 chart, after forming a Harami pattern not far from the support level, NZDUSD is still moving inside the rising channel. Possibly, the pair may reverse and start a new correction to reach 0.6585. However, an opposite scenario implies that the instrument may fall and return to the support level at 0.6400.

GBPUSD, “Great Britain Pound vs US Dollar”

As we can see in the H4 chart, GBPUSD has formed a Hanging Man reversal pattern while testing the resistance level and reversed. At the moment, the pair continues growing towards the resistance level. The target is at 1.2787. If later the price breaks this level, the instrument may continue the ascending tendency.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

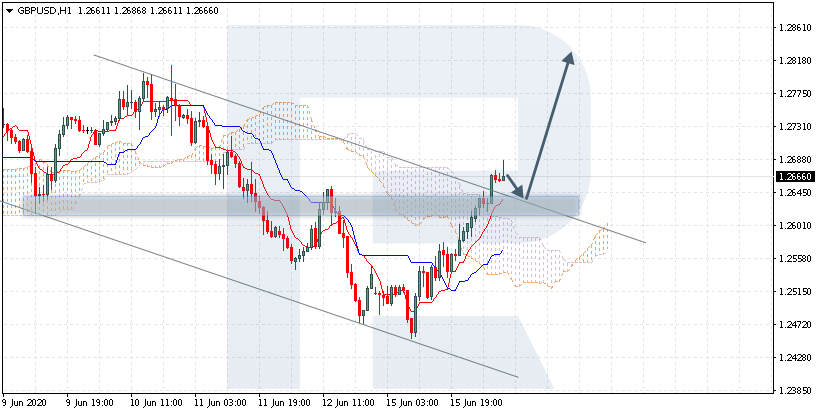

GBPUSD is trading at 1.2666; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test Tenkan-Sen and Kijun-Sen at 1.2640 and then resume moving upwards to reach 1.2825. Another signal in favor of further uptrend will be a rebound from the descending channel’s upside border. However, the bullish scenario may no longer be valid if the price breaks the cloud’s downside border and fixes below 1.2505. In this case, the pair may continue falling towards 1.2415.

USDJPY, “US Dollar vs Japanese Yen”

USDJPY is trading at 107.48; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test Tenkan-Sen and Kijun-Sen at 107.35 and then resume moving upwards to reach 108.40. Another signal is favor of further uptrend will be a rebound from the rising channel’s downside border. However, the bullish scenario may no longer be valid if the price breaks the cloud’s downside border and fixes below 106.90. In this case, the pair may continue falling towards 106.05.

AUDUSD, “Australian Dollar vs US Dollar”

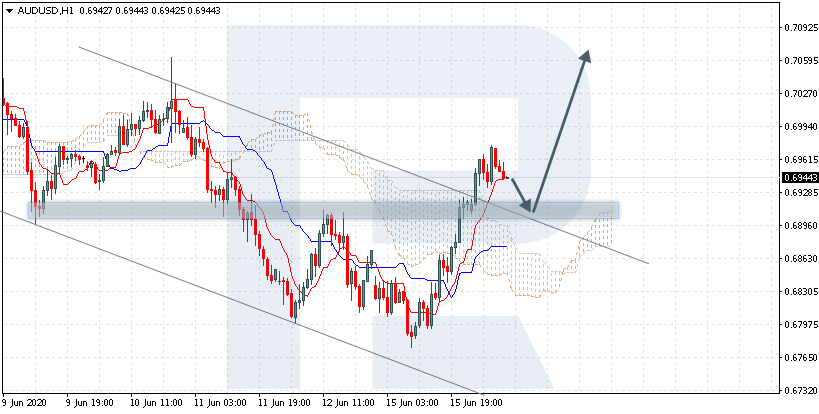

AUDUSD is trading at 0.6944; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test Tenkan-Sen and Kijun-Sen at 0.6905 and then resume moving upwards to reach 0.7065. Another signal in favor of further uptrend will be a rebound from the descending channel’s upside border. However, the bullish scenario may no longer be valid if the price breaks the cloud’s downside border and fixes below 0.6795. In this case, the pair may continue falling towards 0.6705.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

EUR/USD quotes have been growing. During yesterday’s trading session, the growth of the single currency exceeded 90 points. The Fed announced the start of the purchase of corporate bonds to support the country’s economy, which has been significantly affected by the COVID-19 epidemic. The US presidential administration also said it was preparing a nearly $1 trillion infrastructure package. At the moment, the EUR/USD currency pair is consolidating in the range of 1.1300-1.1350. Financial market participants have taken a wait-and-see attitude before today’s speech by the Fed Chairman at 17:00 (GMT+3:00). Positions should be opened from key levels.

The Economic News Feed for 2020.06.16:

– ZEW economic sentiment indices in Germany and the Eurozone at 12:00 (GMT+3:00).

– Report on retail sales in the US at 15:30 (GMT+3:00).

Indicators do not give accurate signals: 50 MA has crossed 100 MA.

The MACD histogram is in the positive zone, which indicates the development of bullish sentiment.

Stochastic Oscillator is in the neutral zone, the %K line has crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.1300, 1.1265, 1.1220

Resistance levels: 1.1350, 1.1400

If the price fixes above 1.1350, further growth of EUR/USD quotes is expected. The movement is tending to 1.1400-1.1420.

An alternative could be a decrease in the EUR/USD currency pair to 1.1270-1.1230.

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.25091

Open: 1.26050

% chg. over the last day: +0.76

Day’s range: 1.25864 – 1.26874

52 wk range: 1.1466 – 1.3516

There is an ambiguous technical pattern on the GBP/USD currency pair. The British pound is currently consolidating. The key support and resistance levels are 1.2600 and 1.2675, respectively. Investors expect additional drivers. Speech by the Fed Chairman, as well as a report on US retail sales, are in the spotlight. We recommend opening positions from key levels.

The UK has published a rather weak labor market report.

Indicators do not give accurate signals: the price has fixed between 50 MA and 100 MA.

The MACD histogram is in the positive zone, but below the signal line, which gives a weak signal to buy GBP/USD.

Stochastic Oscillator is in the neutral zone, the %K line is below the %D line, which indicates the development of bearish sentiment.

Trading recommendations

Support levels: 1.2600, 1.2545, 1.2480

Resistance levels: 1.2675, 1.2725, 1.2755

If the price fixes below the round level of 1.2600, a further drop in GBP/USD quotes is expected. The movement is tending to 1.2560-1.2530.

An alternative could be the growth of the GBP/USD currency pair to 1.2720-1.2750.

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.36012

Open: 1.35668

% chg. over the last day: -0.47

Day’s range: 1.35112 – 1.35982

52 wk range: 1.2949 – 1.4668

The technical pattern on the USD/CAD currency pair is ambiguous. The loonie is in a sideways trend. At the moment, the key support and resistance levels are 1.3510 and 1.3590, respectively. Financial market participants expect a speech by the Fed Chairman. We also recommend paying attention to the dynamics of oil quotes. Positions should be opened from key levels.

Today, the publication of important economic releases from Canada is not expected.

Indicators do not give accurate signals: the price has fixed between 50 MA and 100 MA.

The MACD histogram is in the negative zone, but above the signal line, which gives a weak signal to sell USD/CAD.

Stochastic Oscillator has reached the overbought zone, the %K line has crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.3510, 1.3455, 1.3390

Resistance levels: 1.3590, 1.3680

If the price fixes above 1.3590, USD/CAD quotes are expected to grow. The movement is tending to 1.3660-1.3700.

An alternative could be a decrease in the USD/CAD currency pair to 1.3460-1.3420.

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 107.316

Open: 107.325

% chg. over the last day: +0.01

Day’s range: 107.231 – 107.638

52 wk range: 101.19 – 112.41

The USD/JPY currency pair is still being traded in a flat. There is no defined trend. At the moment, the key support and resistance levels are 107.05 and 107.65, respectively. The technical pattern signals a possible correction of USD/JPY quotes. We expect the speech by the Fed Chairman, as well as a report on US retail sales. Positions should be opened from key levels.

The Bank of Japan, as expected, kept the key marks of monetary policy unchanged.

Indicators do not give accurate signals: the price has crossed 50 MA.

The MACD histogram has approached the 0 mark.

Stochastic Oscillator is in the neutral zone, the %K line has crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 107.05, 106.60

Resistance levels: 107.65, 108.20, 108.55

If the price fixes above 107.65, USD/JPY quotes are expected to rise. The movement is tending to 108.00-108.30.

An alternative could be a decrease in the USD/JPY currency pair to 106.70-106.40.

The US dollar has been declining against a basket of currency majors. The US dollar index (#DX) closed in the negative zone (-0.34%). Investors’ sentiment has been improved slightly after the Fed announced the start of a massive purchase of US corporate bonds. The regulator wants to provide companies with access to cash, as well as increase the liquidity of the credit market in the context of the ongoing influence of the coronavirus on the economy.

Investors still concern about the second wave of COVID-19. China has reported dozens of new cases of coronavirus, which were primarily found in Beijing’s large food market. Also, a new COVID-19 outbreak was recorded in Tokyo, after the nightclubs and bars of the capital opened. The total number of cases has already exceeded 8 million. Today, the speech by the Fed Chairman is in the spotlight. Jerome Powell should give a speech to Congress and present to the legislators the Fed’s vision regarding economic prospects.

The “black gold” prices have been growing. Currently, futures for the WTI crude oil are testing the $37.50 mark per barrel. At 23:30 (GMT+3:00), API weekly crude oil stock will be published.

Market indicators

Yesterday, there was the bullish sentiment in the US stock market: #SPY (+0.93%), #DIA (+0.63%), #QQQ (+1.22%).

The 10-year US government bonds yield continues to grow. At the moment, the indicator is at the level of 0.73-0.74%.

The news feed on 2020.06.16:

– UK labor market data at 09:00 (GMT+3:00);

– ZEW economic sentiment indices in Germany and the Eurozone at 12:00 (GMT+3:00);

Global equity bulls were injected with a renewed sense of inspiration on Tuesday after the Federal Reserve deployed measures to soothe markets and support businesses hit by the coronavirus pandemic.

Although this move may revive investor confidence and even lift global sentiment, the resurgence of coronavirus cases in China and parts of the United States will most likely dampen the positive mood. With risk aversion likely to make an unwelcome return on coronavirus fears and global growth concerns, safe-haven assets such as the Japanese Yen, Dollar and Gold are set to shine through the chaos.

USDJPY remains in a 100 pip range

A lack of appetite for the Japanese Yen has sent the USDJPY punching above 107.60 this morning.

However, the currency pair remains in a wide range on the daily charts with support at 107.00 and resistance at 108.00. A solid daily close above 108.00 may inspire an incline towards 109.40. Alternatively, if 108.00 proves to be a reliable resistance level, the USDJPY may sink back towards 107.00 and 105.90.

Dollar Index eyes 96.00…

As the market mood improves on the Federal Reserves’ support, appetite for safe-haven assets such as the Dollar may wane.

The Dollar Index is under pressure on the daily charts with prices trading around 96.25 of writing. A breakdown below 96.00 may open a path towards 95.00 in the short to medium term. Alternatively, a breakout above 97.15 may trigger an incline towards 97.80.

Commodity spotlight – Gold

Gold remains in a very wide range on the daily charts with support at $1670 and resistance at $1765.

Expect the precious metal to remain rangebound until a fresh directional catalyst is brought into the picture. If prices are able to keep above $1715, Gold could push towards $1765. Alternatively, a breakdown below $1715 could drag the precious metal towards $1670.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.