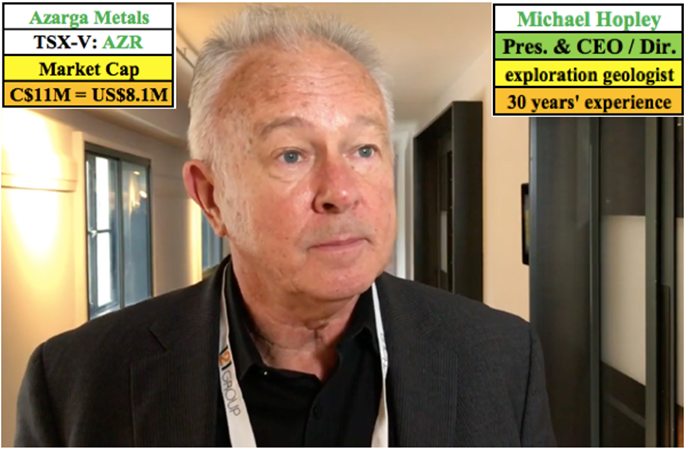

Azarga Metals CEO Michael Hopley speaks with Peter Epstein of Epstein Research about exploration at the company’s silver-copper project in Siberia and the resource estimate that will be released in the next few weeks.

WOW. What a three months it’s been. Things appear to be relatively better now, but I was very worried. At its worst, four major U.S. stock market indexes were down an average of 37.5% from all-time highs set in February. I feared stocks would keep falling and that copper might trade under US$1.50/lb for a long, long time. Luckily, that scenario did not play out.

I don’t know if we’re out of the woods yet, but copper is up nearly 20% from its March low. Perhaps analysts realizing that long-term demand for EVs has remained intact breathed some life back into Dr. Copper? Look no further than Tesla’s sky-high valuation (US$190 billion) for proof of concept!

Silver, although trailing behind gold, is up, so no worries there. I never claim to have any keen insights on commodity prices, but this time may be different. So much new debt and money printing, with no end in sight . So much uncertainty from COVID-19 . Precious metals are in a bull market that could be epic and long-lasting. Silver frequently outperforms gold in bull markets, that means there’s a lot of catching up to do.

With this in mind, I revisited my favorite Russian copper-silver play Azarga Metals Corp. (AZR:TSX.V) by interviewing its President and CEO Michael Hopley. We had a wide-ranging conversation in which a key takeaway is that A LOT IS HAPPENING at the company!

Impressive drill results and favorable metallurgical testing data was released, and a new resource will be out in a few weeks. If the resource estimate is strong, management might commission an optimized PEA. Mr. Hopley could not tell me much regarding the parameters, but in a prior press release management stated that its mineralized strike length had increased from 3.4 to 6.5 km (+91%), and that the overall grade has not changed much.

The current resource is 62 million tonnes. Given a 91% strike extension, I would not be surprised to see 90 million or 100 million tonnes, which could result in an Indicated and Inferred resource approaching two billion copper equivalent pounds. Several near-term catalysts could be impactful and the company is well funded. Please continue reading to learn more about Azarga Metals and its investment thesis.

Peter Epstein: Michael, please tell us how you landed as CEO of Azarga Metals.

Michael Hopley: For almost 20 years I’ve been part of management or on the Board of predecessor companies to Azarga Metals. The company acquired its flagship Unkur property in 2016 and successfully explored it later that year and in 201718. However, due to perceived geopolitical risks, and a difficult funding environment, the project has not advanced as rapidly as we would have liked.

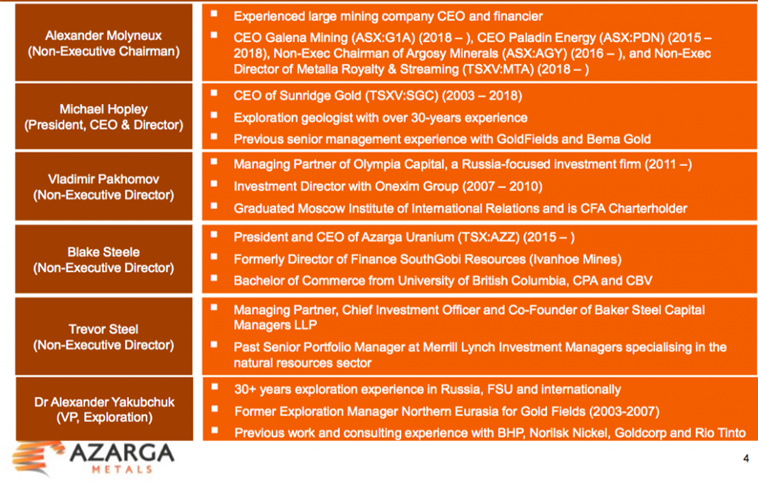

Since 2018, management has turned over; our new team {see team bios above} is very well suited for the specific tasks at hand. When we received a significant financing package from Baker Steel early last year, I was invited to come out of retirement to be president and CEO. As a director it was obvious to me that Unkur had serious potential to be a world-class copper-silver project, so I accepted.

Peter Epstein: Can you describe in greater detail Azarga’s 100%-owned Unkur Copper-Silver project?

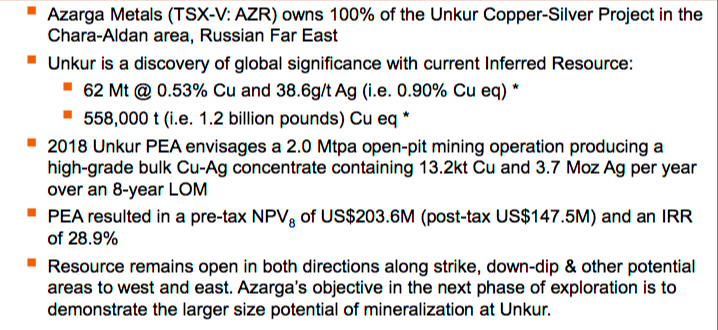

Michael Hopley: Yes, Unkur is located in eastern Russia (Siberia), ~400 km north of the Chinese border. China is by far the largest consumer of copper and silver. My team believes that Unkur hosts a discovery of global significance, with district-scale potential. It’s ~35 km from the giant Udokan copper project that reportedly contains >55 billion pounds of copper. The geological setting and possible scale of our project is similar to Udokan. Russian company Baikal Mining is building it and it’s scheduled to start production in 2022.

After completion of the first modern exploration in 20162018, we reported an NI 43-101 compliant Inferred resource of 62 million tonnes @ 0.53% Cu + 38.6g/t Ag, equivalent to 558,000 tonnes (1.2 billion pounds) copper equivalent (Cu Eq.) at an attractive grade of 0.90%. That’s ~US$52/t (~C$71/t) in-situ rock that’s mineralized rock in the ground. The resource remains open in both directions along strike and at depth.

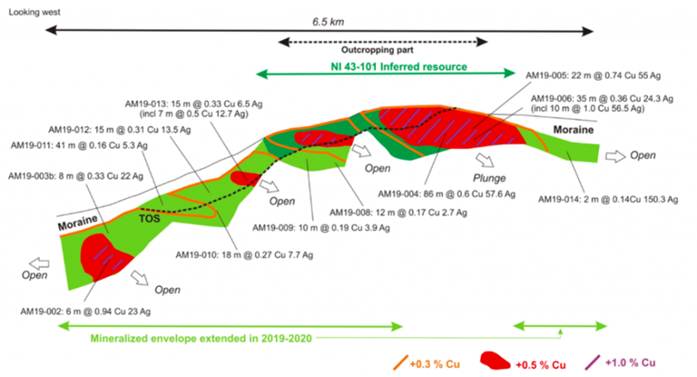

Peter Epstein: On April 9th, Azarga Metals announced drill results. Two assays stood out. The best had a 22-meter interval of 0.74% Cu and 55 g/t Ag. What do these results mean for the Unkur story?

Michael Hopley: This exciting result was from drill hole AM19-005, an in-fill hole drilled to test a higher-grade area north of our current resource. The intercept extended our high-grade envelope further north and deeper compared to the model we used to estimate our existing resource. Select recent drill results over a 6.5 km strike length {shown below}, are encouraging, especially as the project remains open in both directions along strike, and at depth.

As a frame of reference, the 22-meter interval you mentioned equates to ~US$74/t (C$100/t) in-situ value. And, that intercept included a shorter interval of 9m of 1.34% Cu + 99.4 g/t Ag, an in-situ value of C$181/t. To be clear, those two values are not indicative of the overall deposit. Still, if our metallurgy holds up, C$71/t rock (before recoveries) could be economic under the conditions, the right mine plan.

Peter Epstein: Speaking of metallurgy, please explain your latest results on that front.

Michael Hopley: Good question, this is important news. Previous metallurgical tests used only oxidized material from a surface outcrop. These new tests were on both oxidized & sulphide material taken from deeper parts of the Unkur deposit. Recoveries were up to 92% Cu and up to 88% Ag in our sulphide material, using conventional flotation.

The oxide results were as high as 96.4% Cu in an acid leach and up to 96.7% silver in a cyanide leach. Importantly, we think that a standard 30% Cu concentrate will be achievable, making it easy to sell to refiners. We believe this was a good outcome, especially for preliminary-stage testing. We think there’s a reasonable chance that we could use heap leaching to treat our oxide material.

Peter Epstein: Early last year, Azarga received a US$3M investment commitment from Baker Steel Resources Trust. How did that investment unfold?

Michael Hopley: Over the past several years it has been difficult for junior exploration companies to raise cash. Baker Steel took the view that among hundreds of risky companies destined for failure, there will always be some with projects of considerable merit. Azarga’s Unkur project stood out to them, a true vote of confidence.

Peter Epstein: Unkur’s resource estimate is 62 million tonnes @ 0.53% Cu, plus 38.6 g/t Ag. That’s a 0.90% Cu Eq. grade (~1.2 billion pounds Cu Eq.). How deep is the mineralization?

Michael Hopley: Mineralization at Unkur has been drilled to ~350 meters’ depth, but remains open at depth and in both directions along strike. A new resource estimate by SRK is coming out in two or three weeks. While I can’t say what that new resource might look like, I can reiterate what we said in a May 11th press release, namely that recent drilling had extended the mineralized strike length by 90% from 3.4 to 6.5 km.

Peter Epstein: Your 2018 PEA delivered promising financial metrics. Might Azarga be able to extend the 8-yr. mine life?

Michael Hopley: Yes, the existing PEA contemplates mining ~25% of our existing resource, or meaningfully less than 25% of our new resource estimate. We’re looking to announce a significant increase in the resource size in the next two or three weeks. If the resource expansion is strong, then we would look to extend the mine life.

Instead of an 8-year mine life with throughput of 2.0 millin tonnes/year, perhaps we could increase it to 3.0 million or 3.5 million tonnes/year and extend mine life by a few years. I’m not saying we can get there from our upcoming resource update alone; we have to study the new numbers. But, if we can increase annual production, and possibly extend mine life, without a major increase in cap-ex, the impact on NPV, IRR and payback period could be quite favorable.

Peter Epstein: What are the biggest risk factors of the Azarga story?

Michael Hopley: Aside from metals’ pricing, there are two primary concerns. Increased political tensions between Russia and the West, and the speed at which the world’s use/investment in copper and silver returns to normal after the impact of COVID-19.

I find it encouraging that the Cu price fell to ~US$2.10/lb in mid-March, but has since recovered to ~US2.56/lb. Global automakers seem to have maintained fairly aggressive electric vehicle rollout plans, a promising sign for copper demand. Due to its industrial and investment / safe-haven attraction, silver futures touched US$11.80/oz, but have since rebounded to US$17.70/oz (+50%).

Peter Epstein: Why should readers consider buying Azarga Metals?

Michael Hopley: Azarga is one of the few juniors that’s well funded. We’re able to move the Unkur project forward with drill results, metallurgical testing, a new resource calculation in coming weeks and hopefully a new PEA in 6-9 months.

Our chairman, Alex Molyneux, is based in Asia and is well connected. He’s also highly experienced in investment finance/M&A. Russian investors, as well as global sovereign wealth funds, are looking to diversify away from oil, gas and coal. Silver, and especially copper, are critical, green energy, high-tech metals of the future.

Peter Epstein: Thank you, Michael, for this timely update. I can honestly report that few other metals and mining juniors are doing as much during this pandemic. I look forward to seeing your updated resource estimate in coming weeks.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Azarga Metals, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Azarga Metals are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Azarga Metals was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

Coming up David Morgan of The Morgan Report joins me to discuss a range of topics including the recent disruptions in the paper-based precious metals futures markets that cost some major bullion banks to lose their shirts — and how it may be a telltale of a change in the pricing mechanisms for gold and silver.

David also shares why he believes we’re in the beginning stages of a massive financial system reset and why people need to be bracing for a lower standard of living in the days ahead as inflation heats up. So, don’t miss a jam-packed interview with our good friend David Morgan, coming up after this week’s market update.

Precious metals markets are finishing out a choppy week of trading that saw prices make little net progress through Thursday’s close.

As of this Friday morning recording, gold prices are up a slight 0.4% for the week to trade at $1,747 per ounce. Meanwhile, silver is showing a 1.0% weekly gain to come in at $17.84 an ounce.

Turning to the PGMs, platinum is now up 1.5% on the week to trade at $838. And finally, palladium prices are down 0.7% since last Friday’s close to bring spot prices to $1,984 per ounce.

Bullion premiums have been drifting lower in recent weeks after spiking earlier this spring. That in part reflects a waning of fear among investors… and a hope for markets and the economy returning to normal as we head into the summer.

But make no mistake, these are NOT normal times. Not with some parts of the economy still locked down. Not with the Federal Reserve embarking on an unlimited Quantitative Easing program that will dwarf all others that came before it. And not with the fabric of American society being ripped apart by radicals who are bent on erasing history and fomenting a race war.

Police officers in large cities across the country are bracing for a summer of continuing violence, property destruction, and unrest at the same time as many are looking for new jobs. Militant anti-cop hatred in the streets and a lack of support from mayors and prosecutors will leave many cities with hollowed out police departments that are unable to protect the public from crimes.

With these dangers simmering, volatility spikes could return to markets in the weeks ahead.

Summer – which officially begins on Saturday – is usually uneventful in the precious metals markets. Trading volumes tend to diminish, and demand for jewelry and bullion products tends to soften ahead of the seasonally stronger fall period.

But in a year that has been like no other in so many ways, we wouldn’t necessarily count on this summer being a typical one for gold and silver markets.

Investors will have to brace for a number of broad risks.

For one, the U.S. dollar could take a big hit as the government continues to add to an unprecedented budget deficit, the Fed piles on more trillions to its balance sheet, and the U.S. relationship with China turns increasingly adversarial.

Senior Chinese officials warned this week that the U.S. dollar’s privileged status as world’s reserve currency is in jeopardy. Although China has not yet acted to dump the bulk of its dollar holdings, it is continuing to forge various new trading partnerships with other countries that could gradually dethrone King Dollar.

Meanwhile, Jerome Powell and company at the Fed seem to be doing everything they can to undermine the purchasing power of the U.S. currency. They are openly calling for higher rates of inflation as they pump up the central bank’s balance sheet to $7 trillion and counting.

The Fed’s QE and repo market injections are likely to slow somewhat compared to the record pace seen earlier this spring. Since the stock market has been closely tracking the directional moves of the Fed’s balance sheet, central bankers may need to give it another boost if they want to keep Wall Street’s rally going.

They have already stretched and skirted the legal limits of their powers by purchasing corporate bonds and subsidizing small business loans. Perhaps they will soon begin buying up stocks, real estate, and other assets as well.

If the COVID-19 virus continues to spread and prevent the economy from firing on all cylinders, we can expect more stimulus programs from both the Fed and Congress. Heading into an election, politicians will be trying to buy as many votes as they can with handouts and promises of delivering even more handouts if they are elected.

Politicians today resent the historic role of gold and silver in the monetary system, which once served as a restraint on their ability to spend. But the more our currency moves away from the strict limits imposed by sound money, the more important it is for savers to move some of their wealth out of U.S. dollars and into precious metals.

Amid this dangerous social, economic, political, geopolitical, and monetary environment, physical gold and silver are likely to shine in the months ahead.

Well now, without further delay, let’s get right to this week’s exclusive interview with the man they call the Silver Guru.

Mike Gleason: It is my privilege now to welcome back our good friend David Morgan of The Morgan Report. David, we appreciate the time, great to have you on again and how are you?

David Morgan: Mike, I am well under the circumstances and actually, I’m feeling pretty good today. Thanks for having me on. It’s always fun to be with you.

Mike Gleason: Yeah, certainly great to have you back. Well David, let’s start with the big picture here and ask to hear your thoughts and get your take on what’s going on in the world today. Since we last spoke earlier this year, we’ve now got a full-fledged global pandemic, social unrest, massive unemployment and huge amounts of government stimulus and money printing to try to combat that, a movement now to defund police departments… a widely covered autonomous zone in your home state there, that has come about in response to this. Certainly lots going on in the world, to say the least. So comment on what you’re seeing and then where you see this all going, David. Let’s start there.

David Morgan: Well, you outlined it well and summarized just about everything. I’ll just add on that one, we really don’t know the ultimate outcome. Obviously, the trend change has taken place. It’s part of what I call the reset. Overused word, but the reset is a reset, not only in the financial system, but a reset of probably the pricing of almost everything… real estate, commercial real estate, food, communications, you name it down the line.

Obviously, the supply disruptions through this pandemic thing has been substantial and it will not come back to 100%. So, there’s going to be a general contraction in the economy. They’re still in debate whether or not it’s going to be pushed more toward globalization or global interaction versus the other, which is more localized… local food production, more localized government, et cetera. It’s that direction I’m almost certain, not that the globalist won’t push really hard for implementing their plan as much as they can. But I think the physical economy has broken up to such a level that they really can’t put it back together.

So, I don’t know how far I want to go further with that, Mike. I just think it’s a sad situation. It was inevitable without CV (COVID-19). We were already moving that direction. People probably already forgotten that the financial system was absolutely collapsing before our eyes with the repo market, where the federal reserve was putting in billions in the overnight loans because of a trust factor – these banks not trusting loans for 24 hours based on what the collateral was.

So, we were already there, this CV-19 was the needle that popped the bubble, but it isn’t the total cause. It was much, much deeper than that, a long time coming as I and many others have outlined and you’ve got many guests on your show explaining similar situations. I’d say, let me sum it up by saying that, be prepared for lowering standard of living pretty much across the board. That’s our new reality.

Mike Gleason: Yeah. And with all that said, in our view, there is literally never been a better fundamental case for buying gold and silver than there is right now. The Federal Reserve, which you alluded to and Congress are completely off the chain in terms of printing, borrowing, and spending.

The Fed is buying back junk bonds and ETFs. There’s no limits to what they’re willing to do. You talked about the repo markets and how they had to step in there to sustain that market. But somehow, the U.S. dollar seems to be holding up okay. The metals are performing fairly well, but there certainly are no fireworks, at least not yet. What do you make of this? And then, when do you think we’ll see these extraordinary fundamentals start mattering and showing up in the price of metals?

David Morgan: Well, reality dawns on people slowly and then all of a sudden. I mean, the general public is not familiar with the financial system and how it actually works, to sense that something’s wrong. They are, even in a casual way, pretty much aware that the Federal Reserve is pounding out fiat at a frequency that’s never been seen before.

If we just go back briefly and touch on 2008, look at what was produced. I think it was a roughly 4.3 trillion by the U.S., 5 trillion by the European Central Bank and 5 trillion by Japan. And that sort of, and I say sort of, got us through the 2008/2009 crisis, to the point where we are now and that amount of funny money that was put into the system to keep it going, pales in comparison to what’s going on now.

So we are facing probably an inflationary depression at some point, but I want to make the point that the dollar is actually one of the most trusted financial assets that you can have. And this goes right along with John Exter, Exter’s Pyramid, that you can look it up, where people seek safety.

And the safest thing most people know of isn’t gold because they don’t know it. They don’t understand it, they haven’t been educated about it. All they know is that it exists. And as far as they’re concerned, it’s nice to have a wedding ring made of gold and that’s about as much as they know.

Having said that, dollars are where they’re most comfortable. So, you’re going to see, as we are, a big push into the U.S. dollar as the money of last resort, except it isn’t. And it isn’t because if you studied history, monetarily, like I have, you have, most of the listeners have, we know that all fiat fails.

So, there’ll be a run in the dollar and probably see them both go up together for a while. Then there’ll be this bifurcation, meaning that the dollar price of gold will continue to accelerate, even as maybe gold is … excuse me, the dollar is doing better relative to all other currencies, but it will fail at some point.

So, we’re going to be in a very difficult stagflation where most the world, Americans included, are going to be struggling to get the currency de jour, the currency of their country to pay their bills and maintain their lifestyle. And at the same time, there’s this flood of printed money that’s going out everywhere, that dilutes what they’re able to obtain. And so it’s going to look really like a deflation at first. I am convinced of that. And the extra funding money will be going into the assets of probably the stock market, which it seems to be the main place right now.

I hope I’m not confusing anyone. It’s basically not that confusing. Just realize that we are going to see hard times ahead. And if we do, and I believe we will hit an inflationary depression, don’t think too much about the inflation part. Think more about the depression part because in an inflationary depression, the currency becomes worthless or near worthless. In a deflationary depression, the currency becomes more valuable. So, for a while, we’ll see it act that way, that the currency is more valuable because there’s so many people out of work or working part-time or not getting their job back that they once had.

So there’ll be a struggle there and it will look as if its deflationary depression, it is not. In the background, we have an inflationary depression. Once that mindset takes place in the marketplace, meaning basically the financial markets and everyday purchases. I mean, the people still have the power. If everybody decided to stop buying product-X, they’d be out of business literally overnight.

But back on point, you’ll see the inflation in the food sector almost immediately. I’m saying at least six months to a year out, you could see food prices double… maybe in a year, year and a half and that’s a huge increase. And Americans only spend 5% of their disposable income on food. But if you’re in the Philippines, 40% of your income goes to food. So, think outside of the U.S., how much food is a major factor in a normal person’s budget?

And this is almost irrefutable, the amount of destruction through the food supply chain has been astronomical and hasn’t caught up yet. We have reserves, there’s still stuff in the supply chain. And it probably won’t be all that apparent for a few more months, Mike. But once it becomes apparent, the general consensus of opinion will be, “Uh-oh, there’s inflation. Food prices keep going up and up and up.”

Mike Gleason: Yeah, well said. There’s been a theme with a lot of my guests here over the last several weeks, where we’re going to see periods of deflation. Then we’re going to see big periods of inflation and people need to be prepared to ride that wave because it will probably oscillate between one or the other.

We don’t need to spend a whole lot of time on this, but I did want to ask. We saw some trouble brewing in gold markets in March and April. There was a huge premium being paid in the COMEX futures for gold versus London spot markets. Some of the bullion banks lost huge amounts of money in March. They got caught short physical bars and had to pay up to get metal they needed to deliver.

Some of these banks, including Scotia, have decided since to close their metals trading operations. Now the bullion banks have had an extraordinary record when it comes to trading metals profitably. And in our view at least, that is in large part because the game has been rigged, but they got nailed hard this spring. Explain to our listeners how the banks got caught. And more importantly, give us your thoughts on what this might mean for paper gold and silver markets moving forward.

David Morgan: Well, I want to stay as factual as possible. So number one fact is they’re all over leveraged. I mean, they basically run a fractional reserve gold and silver system. It’s just like going back in history where the Goldsmiths held the gold and gave you a certificate for it. And they noticed that only about 10% of the population ever wanted the gold back. They’re very happy to take a certificate and trade that in the marketplace. So that gave them the ability to print more certificates than actual gold in existence.

Same story, just more sophisticated. So what happened was, there was a huge arbitrage opportunity because of the physical supply. And of course, this was told to be the inability to ship physical gold due to flight restrictions and that type of thing. There’s probably some truth to that because I am well-connected as you know, and I did talk to some of the refineries and there were flights that they could not get metal from the refinery into the United States.

So, the arbitrage took place, which usually will rectify the market at some point. And it has been since, but Mike, you’re right – and you might want to add onto it – but the fact is there was an arbitrage opportunity, existed for a long time. Physical metal finally did make it into New York. And basically, the two markets were back to “normal.”

Mike Gleason: Yeah, we have seen it return to normal, essentially in gold. Silver now does have a pretty big spread between London and U.S. futures. And we’re starting to see that a difficulty of getting commercial bars to satisfy the contracts here in the U.S.

Speaking of silver, what’s holding it back? And no one is more knowledgeable when it comes to silver than you are, so why hasn’t it been unleashed yet in terms of the price, do you think?

David Morgan: Well, at the risk of sounding like a broken record, primarily what holds it back is the inability to have a free market in silver. That’s one. Another one that isn’t talked about often enough is what is the real price of silver? And well, wait a minute, David, what do you mean? And here’s what I mean, the COMEX sets the price and that’s the real price. But really what it is, is a paper price for a contract to buy silver. Most of those contracts are never exercised.

But if you buy silver in the European continent, for the most part, there’s a 17% Value Added Tax. If you buy it almost anywhere outside of North America, there’s either a Value Added Tax or a premium that’s substantially larger than you get in the gold market. So, if silver were treated like gold, and there was a across the board, worldwide 3% markup between the bid/ask spread on silver, you would see a vast amount of physical silver investors moving into the market because the availability and the pricing mechanism would be normalized or not broken. It’s broken.

And so metals investors, primarily through the rest of the world, as I’m stating, look at their pocket book. And they say, well, geez, if I buy gold, I only have to overcome a 3% premium and I’m in the money and I’m ahead. Whereas with silver, it’s a 17% VAT on top of a premium that’s larger than the gold premium. And so I’ve got to see like a 25% move in silver just to be even, I don’t want to pay that big a premium.

So, there’s a huge detriment to buying physical silver outside of the North American continent, for the most part. And even in Mexico, where there’s a great deal of silver, spreads are more reasonable in South America and Mexico relative to the rest of the world. So, there’s going to be a day where with the algorithms that can be written, that there will be a world price of silver. That will be what the retail price or what I like to call the honest to God price, of silver really is when you factor in what the actual purchase would be in let’s say, Germany and France and the UK and Australia and Japan and India. And you could take all those and average them out on a weighted basis and find out what the real price is silver.

So, that’s one that isn’t talked about very often. And the last one is coming back to the paper price, fortunately or unfortunately, there has enough physical silver for most of the time, to satisfy the true physical demand. So, let me explain, in 2008, during the financial crisis, a lot of silver investors with some really big names. In fact, I just got a phone call from somebody. I digress, but he was at a level of a bank that you wouldn’t believe if I told you. And of course I’ll keep it anonymous, but when he bought silver, he bought at the bottom and he bought enough to be substantial.

Let me come back on point. There was a huge premium disparity for physical silver in the retail market. We’ve seen that again now. And Mike, you know as well as anybody, you might want to add on to my comment, where if you really want the metal you’re going to have to pay five, six bucks, maybe seven, eight. I mean, it’s varied. I know the premiums are falling back to more normal to get physical silver.

What’s interrupting this time, is that we didn’t see it in the 2008 crisis, you could buy, in fact I did buy three 1000 ounce bars, basically off the exchange. But this time, even the thousand ounce bars seem to have a bit of, I’ll call it a problem, for you to get them quickly. And that of course has got my eyebrows raised, but I don’t want to make too much of it. I like to see more data, but as you stated a moment ago, there’s this spread between the London market and the COMEX on commercial bars.

So, until that squeeze happens, where the physical market basically can’t keep up with the demand and we’re there, but I don’t want to project too far because the few times it’s happened, it has fallen back. Then this whole paper paradigm nonsense is going to go away and you’ll be pretty much in a cash market. Doesn’t mean that the COMEX closes down and quits putting out a price. They probably won’t, but it’ll be a joke. It will become a laughing matter because people will say, well, if you’re stupid enough to sell your silver at $17.50, when I have to buy it for $25, good luck. I’m not selling it until it hits $25 at the minimum. The only reason anyone would sell it back to anyone else would be because they absolutely were desperate, needed the money or something like that.

So, I think we’re getting to the end of their game of manipulating the market through this paper paradigm that has worked so well for them for so long, only there’s been enough physical of backup their nonsense. But I think that they are reckoning, that I’ve talked about and many others for so long, is approaching.

Mike Gleason: Yeah. Wouldn’t that be nice if we get true price discovery for once and no longer the ridiculousness of these paper derivatives setting the price for a physical commodity. And I think you’d probably see that coiled spring effect take place if it did finally unwind and we had the physical market setting the price, instead of the paper market setting the price.

Sticking with silver here, we’ve been reading about global mine production being severely disrupted due to government mandated suspensions of mining operations in response to COVID-19. Something like 66% of silver output has been taken offline as a result. Talk about this and what it may mean for the silver price down the road.

David Morgan: Yes. Well, as you know, Mike, I do a weekly perspective and that was one I did this a couple of weeks back. I continue to learn more about a lot of things. And of course, silver still fascinates me. And so I started looking into what was the effect of this shutdown on all the metals. And to my surprise, I didn’t realize that silver was the most. Silver was at 66%. I backed it up on the video I made a with the data showing on the screen. And uranium was 33%, so uranium being the second most hurt by the shutdown, was only half as bad as silver.

So, that will spill over. How much remains to be determined because even though supply has been curtailed, demand has been curtailed for the industrial side, but not necessarily investment side. The investment side is really quite robust. So, what will happen, as already stated, we’re going to see more and more investment demand come into both the metals and eventually move into the silver market because of so many factors. It’s more affordable. It’s undervalued, even relative to gold. And it may become more accessible through the Blockchain.

And I don’t want to be too one way on this because I am affiliated with a certain silver backed cryptocurrency, there are others but this will be a way for, going back to earlier in the conversation, where someone in India or Japan or the UK can buy real physical silver through the Blockchain system, without all this nonsense of VAT and all the rest of this stuff, which will be a huge boon to potential silver investors, that I do think there’s a pent up demand. I do believe again, I’ll repeat that if you had as much access to the silver market, as you do the gold market on a global basis, there would probably be a lot more silver investors out there than there are presently.

Mike Gleason: Yeah, well said. I couldn’t agree more on that. Well finally, before we let you go, give us any final thoughts you may have. Perhaps summarize the answer to the question, why metals and why now, because I know you have a lot more to say on that question and then anything else you care to comment on as we begin to close today?

David Morgan: Well, thank you for that. Yeah. In summary, I try to be a realist. I don’t want to be too big of a Debbie Downer, but the reality is we are going to have a lower lifestyle. We are going to have to adjust and you’re going to have to be mentally prepared for that. On top of that, the metals have shown throughout all of recorded history, that in times of uncertainty, it’s good to have some.

You don’t need to put your life savings in the metals. You don’t need to sell all your real estate holdings and buy gold. I’m not advocating that. But I am advocating, if you are awake and alive, you do need to have a hedge, which means you need precious metals. How much? Well that’s to be determined by you. But primarily, most people in the industry would recommend somewhere in the 10% range to be a sufficient amount for most people.

And that would take the gold and silver markets to heights that would be unimaginable because the whole financial system basis today, there’s less than really 1% in the gold market. So you would see, if it went to a 10%, a factor of 10, going into gold based assets. And silver represents like .02% of the whole financial system. I mean, it’s so minuscule that it’s almost not worth talking about. Of course, it’s important, it’s essential, it’s mandatory. It’s something that cannot be lived without it.

We couldn’t have modern technology without silver. You can live a pretty similar life to what we have without gold in the mix. But without silver, this lifestyle would be nonexistent. You wouldn’t be able to have the communications, the computers, the touch screens, flat screens. I mean, all this stuff that depends on the silver market.

So I think I’m so very bullish for a number of reasons, but you don’t have to be so bullish that you overdo it. Again, 10% is probably best for everybody to have, for most people. There are others that are over-weighted in metals, I’m one, it’s my specialty. And I do see an advantage to be over-weighted in the sector, but that’s me. For the general person, 10% is not very much as far as, you have 90% that could be in stocks or bonds or real estate or a partial owner of a business, or whole life or whatever, and still have enough that if something were to go awry, which it is happening as we speak, that precious metals position would actually rescue you financially from everything else going down substantially.

Mike Gleason: Yeah. You make a great point about how, if we go from say less than 1% ownership or approximately 1% ownership in precious metals to 10%, my gosh, what that would do to the demand and the supply-demand situation for physical metal. After all, they can’t print gold, they can’t print silver like they can with paper money.

Well, good stuff, David. It’s always a pleasure and we appreciate your insights, once again. Now, before we let you go, please tell people about the Morgan Reports and tell them how they can get on board with you and follow you more closely.

David Morgan: Sure, Mike. The easiest thing is go to the main landing page, which is TheMorganReport.com, all one word. You can sign up for our free newsletter. Interviews like this, I’ll send you in your email box. Also, I do a weekly perspective each week, which is a wrap up of the entire financial markets. And I usually do a video that shows you the screens. Some of the stuff is mainstream, Bloomberg Reuters, some of the mainstream type of press that they don’t really put in your face, but I do because this contraction, as I said, has been going on for a long time before the CV needle punctured the balloon.

Anyway, I try to be succinct. I try to make it like 10 to 15 minutes total. I always try to wrap up with something about the precious metals, one or the other or both. And also my main thesis has always been to get people to think critically on their own, so that’s available. You can look me up on Twitter. I have a YouTube channel.

If you go to the blog, which is TheMorganReport.com/blog, over on the upper right hand legend, you have all the icons for Twitter, YouTube, LinkedIn, everything I’m on. You can just click those from that page and it’ll take you right to the Twitter feed or right to the YouTube feed or right to the LinkedIn feed and be able to watch videos that I’ve posted to Twitter, as an example.

Sometimes you guys put stuff out that I think, everyone ought to read this article that’s in the precious metals market, so I’ll put it on my Twitter feed. And this is for people that want to go a bit deeper, but I do recommend, I do a lot of work for free, that if you want to stay in touch, go to the blog, I’d say two or three times a week. And if you’re lazy, just sign up for the newsletter, we’ll pretty much mail it to you every weekend.

Mike Gleason: Yeah. Well, thanks again, David. I’m an active follower of you on Twitter @silverguru22, for people who want to do that. You always put out excellent stuff and enjoy reading the things that you’re finding there, either original content that you’re putting out or great little news articles or videos that you’re finding and people should definitely do that.

Well, all the best to you. Appreciate the time, stay safe and healthy and have a great weekend, my friend. We’ll talk again soon.

David Morgan: All right, Mike, thanks for having me, same to you.

And don’t forget to tune in here next Friday for next Weekly Market Wrap Podcast, until then this has been Mike Gleason with Money Metals Exchange, thanks for listening and have a great weekend everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

The phenomenal market rally sustained by monetary and fiscal stimulus, suddenly appeared unsustainable with risk aversion sending investor sprinting towards Gold, the Japanese Yen and King Dollar.

It has been a mixed week for the mighty Dollar thanks to the return of risk aversion and general caution.

Although the Dollar was able to steamroll the Pound, Euro and Swedish Krona other currencies like the Japanese Yen and Swiss France were able to fight back. Expect the Dollar to pressure G10 currencies in the week ahead as global growth concerns and coronavirus fears trigger another dash for cash.

Looking at the technical picture, the Dollar Index is experiencing a rebound on the daily charts. Although prices trading below the 20 Simple Moving Average, bulls seem to be eyeing 97.80. A breakout above this level may open the doors towards 98.50 and 99.00.

Alternatively, a breakdown below 97.15 may open the doors back towards 96.00.

Euro bulls wave flag of defeat

It has not been the best of trading weeks for the Euro which has weakened against almost every single G10 currency.

Earlier in the week, we discussed how the Euro was struggling against the Dollar with prices heading towards 1.1200. With this target reached, the next key point of interest for the EURUSD will be found around 1.1100.

A solid weekly close below the 1.1200 may confirm further down in the week ahead.

Pound pummelled and pounded

If you thought the Euro had it bad this week, take a look at the British Pound.

The GBPUSD has tumbled over 300 pips this week thanks to an appreciating Dollar and a central bank that seem to be saving its ammunition for a later date. The BOE was widely expected to leave interest rates left unchanged at 0.1% and increase purchases of government bonds by £100 billion but it seems investors were looking for more action.

Given how the coronavirus has swept through the UK economy like a crazy tornado, there was hope for the BoE to increase QE purchases by £150 – £200 billion. Such a move would lower the interest rates offered on loans and mortgages – ultimately encouraging consumption which remains an engine for growth in the United Kingdom.

Looking at the technical picture, the GBPUSD may tests 1.2200 if a weekly close below 1.2350 is achieved.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Here is a quick view of where gold, the dollar, and miners have been, what to expect if the stock market starts a new bull market, and what to expect if we start a new bear market. Hope this helps ?

Azerbaijan’s central bank cut its policy rate for the second time this year and for the 14th time since February 2018 and said future policy decisions will be aimed at keeping inflation within its target range, maintaining financial stability and supporting economic activity. The Central Bank of the Republic of Azerbaijan (CBA) cut its discount rate by 25 basis points to 7.0 percent and has now cut it by 50 points this year following a cut in January. Since February 2018, when CBA began easing its monetary policy stance, the rate has been cut 14 times and by a total of 800 basis points. Azerbaijan’s inflation rate eased to 2.9 percent in May from 3.0 percent in April and CBA said its updated forecasts point to inflation of 3.0 to 3.5 percent by the end of this year, within its target range of 4.0 percent, plus/minus 2 percentage points. It added the situation on the foreign exchange market remained stable in May, with supply exceeding demand at its auctions, while the monetary base had risen 8.0 percent since the end of April but was still down 10.6 percent since the start of the year. CBA said the negative impact from the Covid-19 pandemic on Azerbaijan’s economy was continuing in May and June, with a drop in all parts of aggregate demand though official data showed growth in the non-oil, gas and agricultural sectors in the first five months. Retail turnover in the first five months was down 1.7 percent from the same period last year while investments in the non-oil sector had fallen 16.7 percent, CBA said.

Producer prices in Germany continued falling in May: producer prices index declined 0.4% after 0.7% decline in April, when a 0.3% decline was expected. This is bearish for EURUSD.

It was a dark time for animals. Poaching was rampant. Wild birds and mammals were being slaughtered by the thousands. An out-of-control wildlife trade was making once-common animals hard to find and pushing rare species into extinction.

This is the story of North America a century ago, and of Asia today. But there was a surprise ending in America, and I believe there could be one in Asia.

Today North America has abundant wildlife. Much of my research as a wildlife biologist focuses on documenting the rebound of species that once were hunted into scarcity, including wolves, deer and fishers.

This is the outcome of what I call the North American wildlife conservation miracle. A century ago, with many species on the brink of extinction, people here stopped overusing wildlife and created a new culture of conservation.

Today unregulated wildlife trade in Asia is decimating species in much of the world, and now even threatens humans through the likely spillover of the SARS-CoV-2 virus from bats or pangolins to humans. Suddenly the harm caused by this rampant wildlife trade is in the spotlight, which creates an opportunity to pull off a conservation miracle in Asia. I hope lessons from the American experience can help.

Out-of-control wildlife trade

In the late 1800s and early 1900s the seemingly endless bounty of America’s wildlife began to run out. By 1878, three northeast species – the Labrador duck, great auk and sea mink – went extinct. The eastern elk, the largest mammal in most eastern states, followed in the 1880s. Even highly resilient species like white-tailed deer and Canada goose declined sharply. Bison once numbered 30 million, but were down to a few hundred animals by the late 1880s.

The pioneer delusion of endless bounty was replaced by an acceptance that there was nothing they could do about it. American settlers had a “manifest destiny” mindset, believing they were destined to expand across the continent, and accepted that the loss of other species was an inevitable consequence of that.

Then the bison didn’t go extinct.

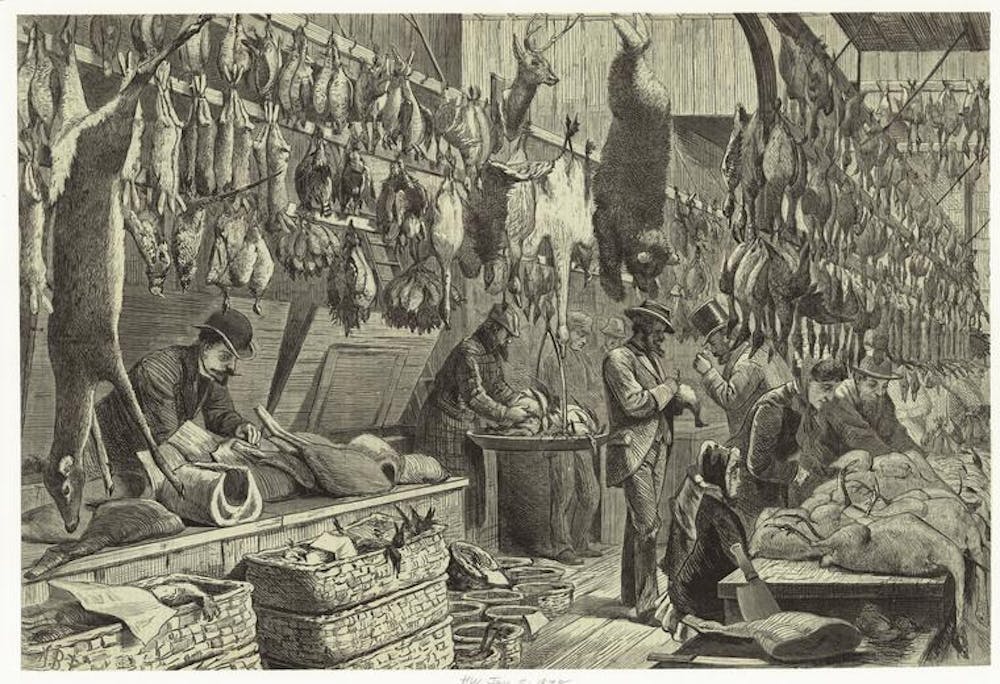

‘The Christmas Season,’ 1878, an engraving by Arthur Burdett Frost of a wild game stand at New York City’s Fulton Market showing a bear, deer and many types of birds. NYPL

Back from the brink

For some Americans, including Theodore Roosevelt, the prospect of erasing an iconic species like bison was a call to action. They formed the American Bison Society, which bred bison at New York’s Bronx Zoo and shipped them west in hope of repopulating their former ranges.

As president, Roosevelt helped create some of the first national wildlife refuges and signed laws restricting the wildlife trade. But the bulk of the work was done by states and individuals.

Americans spoke out against large-scale hunting. George Bird Grinnell, editor of the sporting journal Forest and Stream, used the magazine as a platform to call for protecting birds. Grinnell later teamed with Teddy Roosevelt to create the Boone and Crockett Club, a group of conservation-minded hunters. Two Boston socialites, Harriet Hemenway and Minna Hall, formed the Massachusetts Audubon Society and worked to end the custom of adorning ladies’ hats with plumes from wild birds.

By the 1930s every state had a wildlife agency funded by taxes and hunting license fees. These agencies shut down most wildlife harvests, protected and restored habitat and reintroduced animals that had been eradicated, such as turkeys and otters.

The first U.S. ‘duck stamp,’ issued by the federal government in 1934. Purchase of a current duck stamp is required to hunt migratory waterbirds, with proceeds funding migratory bird conservation. USFWS

When hunting resumed, states managed when it could take place and how many animals a person could harvest. Ecology was a new field, and scientists like Aldo Leopold adapted its principles to create wildlife management as a new branch of study that could help inform these regulations.

Today deer, turkey, bear, elk, ducks and geese are abundant in many parts of North America. State governments carefully regulate harvests. Wildlife is not sold commercially for food in the U.S., unlike Australia and much of Europe. Trapping and sale of fur-bearing animals like beaver and fisher is managed sustainably.

Of course, wildlife conservation in North America still faces serious challenges, including habitat loss, climate change and pollution. But unsustainable hunting is no longer a problem, and legal hunting helps fund conservation for all species.

Will Asia stop eating wildlife?

Over the last 20 years, demand for wildlife products in Asia has driven a collapse of animal populations there, as well as in Africa and Latin America. Most larger mammal species outside of North America today are primarily threatened by poaching for food, art and traditional medicines of dubious effectiveness.

Conservationists hope to seize on the tragedy of the SARS-Cov-2 spillover to end the global wildlife trade, or at least regulate it more tightly. What lessons can the North American experience offer?

First, it is critical to reduce demand. This was a slow process a century ago. But COVID-19 has cast a stigma on wildlife products that could help turn the tide in Asia, just as public shaming in the U.S. helped end demand for things like feather hats and fur from spotted cats.

Today animal welfare advocates are using social media to urge Asian consumers to avoid products made from endangered animals. In response to efforts like these, China banned domestic sales of ivory in 2017, and Chinese consumption of shark fin soup has declined sharply over the past decade.

Former NBA star Yao Ming has campaigned for a decade to reduce Chinese demand for wildlife products.

Second, this effort will involve many players, including national governments, regional authorities and nongoverment organizations like Save Vietnam’s Wildlife, Bat Conservation India Trust and Save Pangolins. These groups understand local culture and politics, and can connect directly with communities where wildlife is hunted and sold.

Finally, we need some optimism. The persistence of the bison a century ago showed Americans that extinction wasn’t the only option. It is important now to monitor wildlife populations so that efforts can target species most at risk, and to celebrate recoveries that might be early signs of a second conservation miracle.

Russia’s central bank cut its policy rate for the third time this year and for the 8th time in the last 12 months, saying the downward pressures on inflation are higher than expected and further rate cuts will be considered in coming policy meetings.

The Bank of Russia cut its key rate by another 100 basis points to 4.50 percent and has now cut it by 175 basis points this year following cuts in February and April.

Since June 2019, when the central bank began to reverse two rate hikes in the second half of 2018, the rate has been cut eight times by 325 points.

Today’s decision was well-telegraphed by Governor Elvira Nabiullina who said on June 5 that a 100 basis-point rate cut was among the options that would be considered as there was significant room for monetary policy easing due to fading inflationary pressure from the measures taken by governments worldwide to curb the spread of the Covid-19 pandemic.

“Disinflationary factors have been more profound that expected due to a longer duration of restrictive measures in Russia and across the world,” the central bank said, adding the effect of short-term pro-inflationary factors have largely been exhausted, inflation expectations have eased and financial stability risks in global markets have declined.

“In these circumstances, there’s a risk that in 2021 inflation might significantly deviate downwards from the 4.0% target,” the bank said, adding its rate cut was aimed at limiting this risk.

Russia’s inflation rate eased to 3.0 percent in May from 3.1 percent in April as the upward pressure on prices from a lower ruble and higher demand for certain goods ahead of quarantines and a disruption to supply chains, begin to fade.

As of June 15, inflation rose back to 3.1 percent, the central bank said, adding inflation in coming months will be contained by the rise in the ruble in May and early June on the back of more stable global financial markets and rising oil prices.

But at the same time, inflation will also rise this year due to the low base effect of 2019.

In April the central bank forecast inflation would average 3.1 to 3.9 percent this year, down from 2019’s 4.5 percent.

The current risks of disinflation are mainly due to the uncertainty over the virus and the scale of measures to fight it, and the impact of these measures on economic activity and how fast the global and Russian economy recover.

“If the situation develops in line with the baseline forecast, the Bank of Russia will consider the necessity of further key rate reduction at its upcoming meetings,” the bank said.

Russia’s ruble tumbled 25 percent from Jan. 12 to March 19 but since then it has rebounded 17 percent and was trading at 69.3 to the U.S. dollar today, down only 10.5 percent this year.

Some of Russia’s measures to contain the spread of Covid-19 remain in place and together with the considerable drop in external demand this is putting longer-than-expected pressure on economic activity and recent surveys of business reflect cautious sentiment.

“The contraction of GDP in the second quarter could prove more sizable than expected,” the central banks said, confirming its forecast for Russia’s economy to contract 4-6 percent this year as compared with growth of 1.3 percent in 2019.

In the first quarter of this year Russia’s GDP grew an annual 1.6 percent, down from 2.1 percent in the previous quarter.

The Bank of Russia released the following press release:

“On 19 June 2020, the Bank of Russia decided to cut the key rate by 100 bp to 4.50% per annum. Disinflationary factors have been more profound than expected due to a longer duration of restrictive measures in Russia and across the world. The effect of short-term pro-inflationary factors has been largely exhausted. Financial stability risks related to the situation in global financial markets have declined. Household and business inflation expectations have abated. In these circumstances, there is a risk that in 2021 inflation might significantly deviate downwards from the 4% target. The key rate decision taken by the Bank of Russia is aimed at limiting this risk and maintaining inflation close to 4%.

If the situation develops in line with the baseline forecast, the Bank of Russia will consider the necessity of further key rate reduction at its upcoming meetings. In its key rate decision-making, the Bank of Russia will take into account actual and expected inflation dynamics relative to the target and economic developments over the forecast horizon, as well as risks posed by domestic and external conditions and the reaction of financial markets.

Inflation dynamics this year and in the first half of 2021 will be largely influenced by a steep decline in domestic and external demand occurred in the second quarter. The disinflationary effect of weak demand has strengthened due to both current and deferred economic effect of restrictions. Household and business inflation expectations have abated after a short-lived growth in March-April.

The influence of the weaker ruble and the episodes of increased demand for certain product groups in March has been exhausted. According to preliminary data as of 15 June, annual consumer price growth rate was around 3.1%. In the coming months, consumer price dynamics will be additionally contained by the strengthening of the ruble observed in May — early June on the back of stabilising global financial markets and growing oil prices. Current monthly annualised inflation will continue to decline. At the same time, annual inflation rate will rise in 2020 owing to the low base effect of 2019.

In the context of prevailing disinflationary factors, there is a risk that in 2021 inflation might significantly deviate downwards from the 4% target. The key rate decision taken by the Bank of Russia is aimed at limiting this risk and maintaining inflation close to 4%.

Monetary conditions slightly eased in May-June after some tightening in March-April. OFZ and corporate bond yields dropped below the levels observed at the beginning of the year, including owing to the current monetary policy stance. The country risk premium went down, largely owing to an improved situation in global financial and commodity markets. Interest rates on deposit and housing mortgage loans decreased. At the same time, increased credit risks in the real sector push interest rates up and lead to a tightening of non-price lending conditions in certain market segments. The Bank of Russia’s decisions to cut the key rate, along with a notable drop in OFZ yields, pave the way for reduction in interest rates in other financial market segments in the future. Coupled with the Government and other Bank of Russia’s measures, this will support lending, including in the most vulnerable sectors of the economy.

Economic activity. Some of the previously enforced restrictive measures remain in place. Alongside a considerable drop in external demand, the negative pressure this is exerting on economic activity is more extended than the Bank of Russia assumed in April. There was a significant drop in business activity in the services sector and manufacturing; a sizeable contraction was reported in the numbers of new orders in external and domestic markets; investment declined. Unemployment went up and incomes shrank. There was a considerable drop in retail sales. The phased lifting of restrictions between May and June is helping consumption-oriented sectors gradually recover. However, recent business surveys invariably reflect cautious sentiment.

The contraction of GDP in the second quarter could prove more sizeable than expected. At the same time, the Russian economy is gaining support from the Russian Government and the Bank of Russia’s additional measures aimed at the mitigation of economic effects of the coronavirus pandemic. In these conditions, GDP will decrease by 4-6% in 2020. Recovery growth of the Russian economy will continue in 2021-2022.

Inflation risks. Disinflationary risks prevail over pro-inflationary ones. Under the baseline scenario, disinflationary risks are chiefly connected with uncertainty as to further developments in the coronavirus pandemic situation in Russia and globally, the scale of possible measures to fight it and their impact on economic activity, as well as the speed at which both the global and Russian economies will recover as restrictive measures are mitigated.

The short-term pro-inflationary risks connected with a potential sizeable pass-through into prices of the recent ruble weakening as well as with the episodes of increased demand for several product groups have all been exhausted. However, disrupted supply chains as a result of the curbs and the additional costs of protecting personnel and consumers from the coronavirus spread could exert upward pressure on prices. The periods of strengthened volatility in global markets can be reflected in exchange rate and inflation expectations.

Medium-term inflation dynamics will be significantly impacted by fiscal policy parameters, in particular, the scale and efficiency of the Government’s measures towards mitigating the consequences of the coronavirus pandemic and overcoming structural constraints, as well as the speed of the 2021-2022 budget consolidation.

If the situation develops in line with the baseline forecast, the Bank of Russia will consider the necessity of further key rate reduction at its upcoming meetings. In its further key rate decision-making, the Bank of Russia will take into account actual and expected inflation dynamics relative to the target and economic developments over the forecast horizon, as well as risks posed by domestic and external conditions and the reaction of financial markets.

The Bank of Russia will hold its next key rate review meeting on 24 July 2020. The press release on the Bank of Russia decision is to be published 13:30 Moscow time.”

The US dollar strengthened over the past 7 days due to improved US macroeconomic data. Investors believe that large-scale financial assistance from the Fed will help the economy without rising inflation. In particular, an increase in US retail sales in May had the maximum positive impact. At the same time, there was an increase in global risks against the background of pessimistic forecasts of a fall in world GDP in 2020 from all authoritative world organizations such as the World Bank, OECD and others. This helped to strengthen the “protective” currencies – the yen and the Swiss franc.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

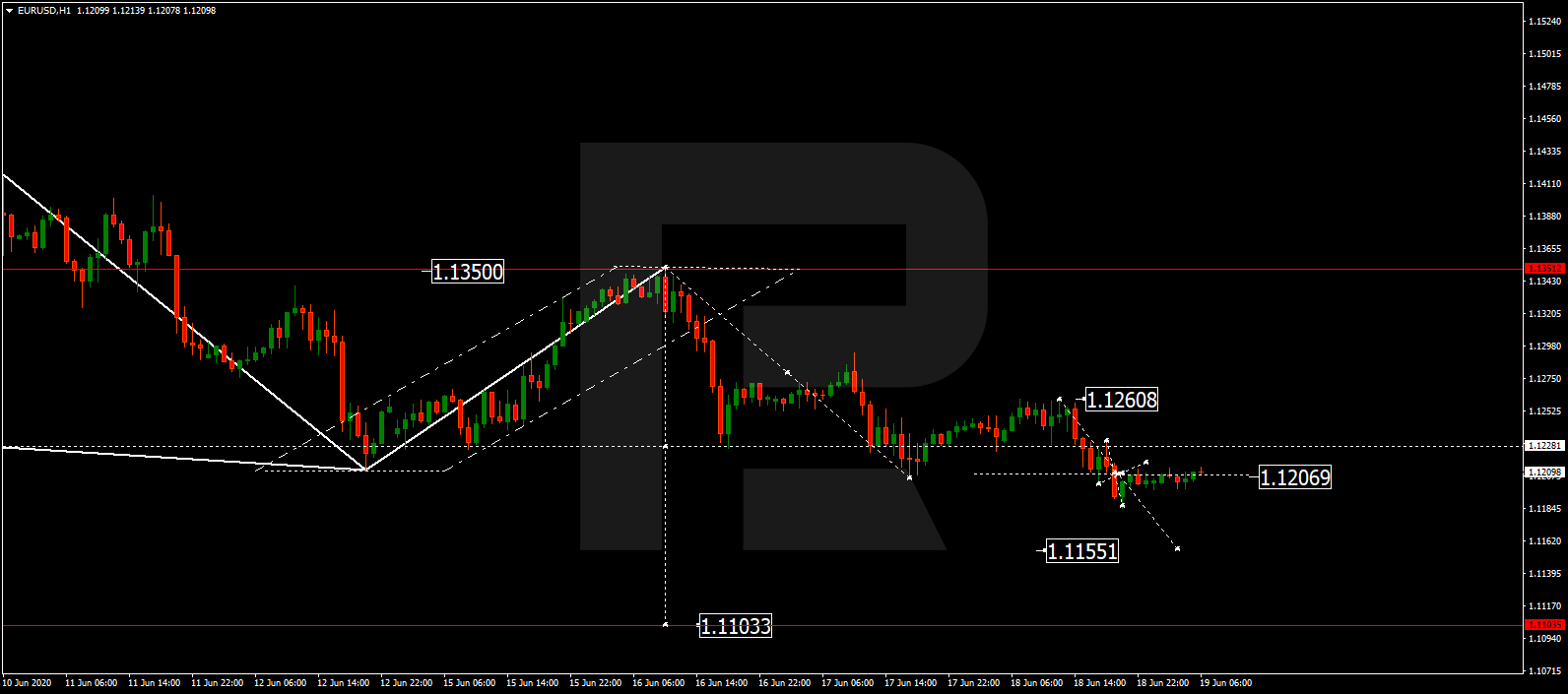

EURUSD has expanded the consolidation range down to 1.1185. Possibly, today the pair may grow to test 1.1222 from below and then resume trading downwards with the short-term target at 1.1100.

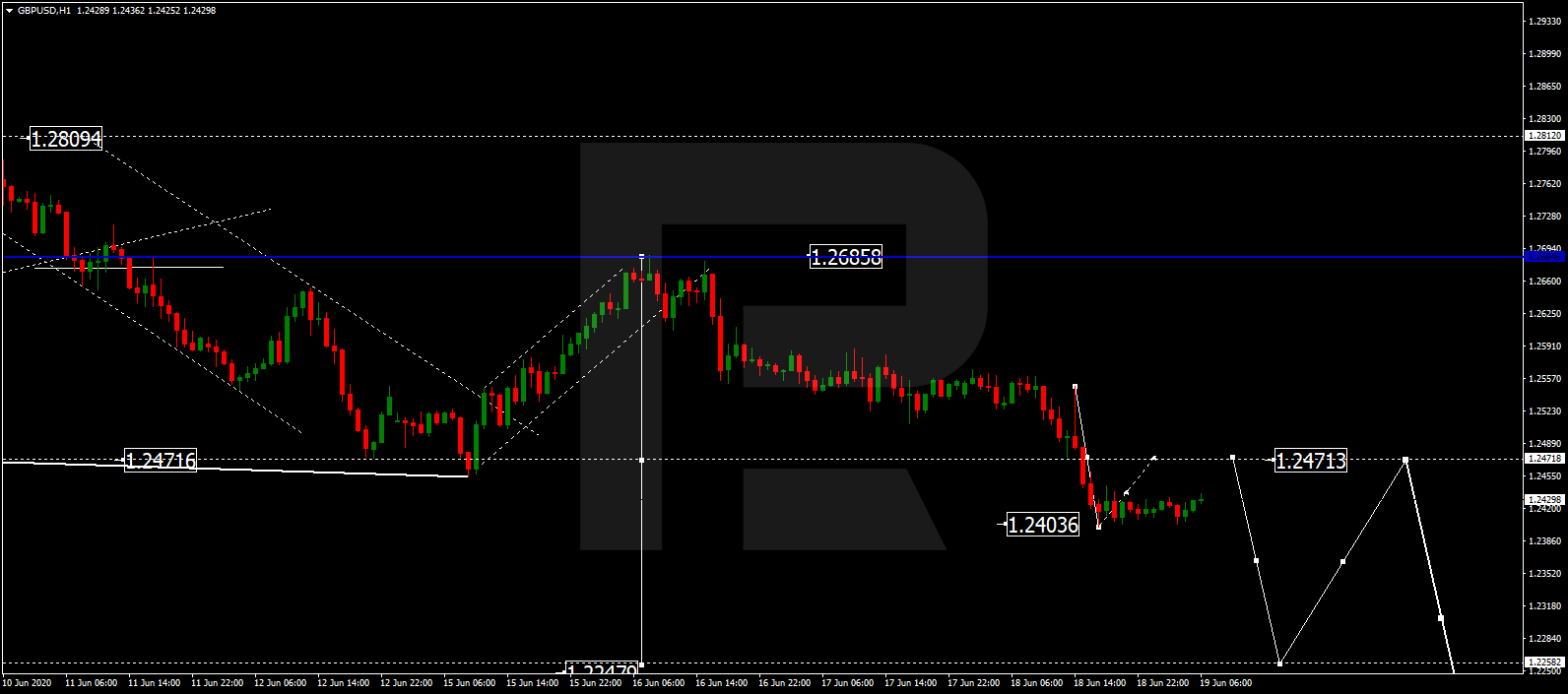

GBPUSD, “Great Britain Pound vs US Dollar”

GBPUSD continues forming the third wave within the downtrend. Today, the pair may correct to test 1.2470 from below and then resume trading downwards with the short-term target at 1.2250.

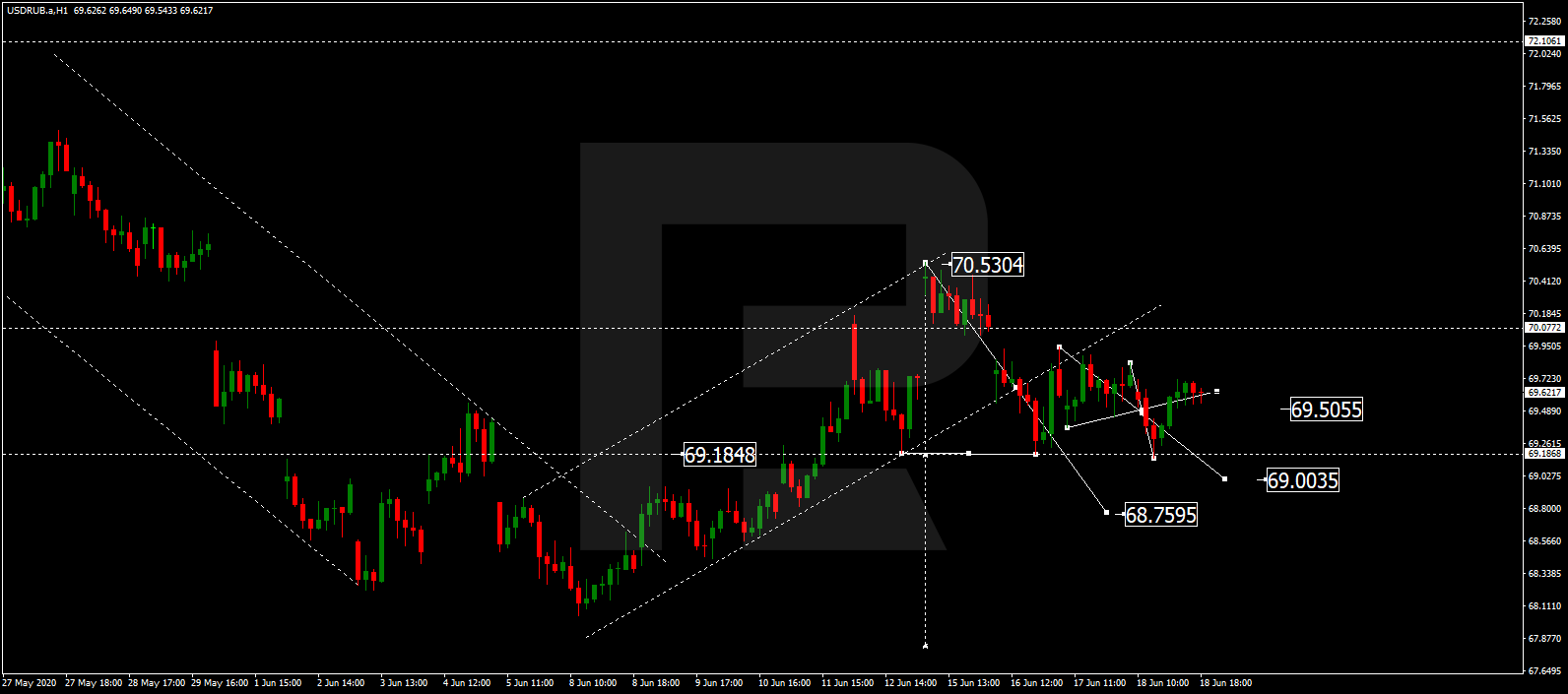

USDRUB, “US Dollar vs Russian Ruble”

USDRUB is consolidating around 69.90. Possibly, today the pair may fall to break 69.00 and then continue falling with the target at 68.75 or even 67.50. However, if the price breaks the range to the upside, the market may continue the correction towards 71.00.

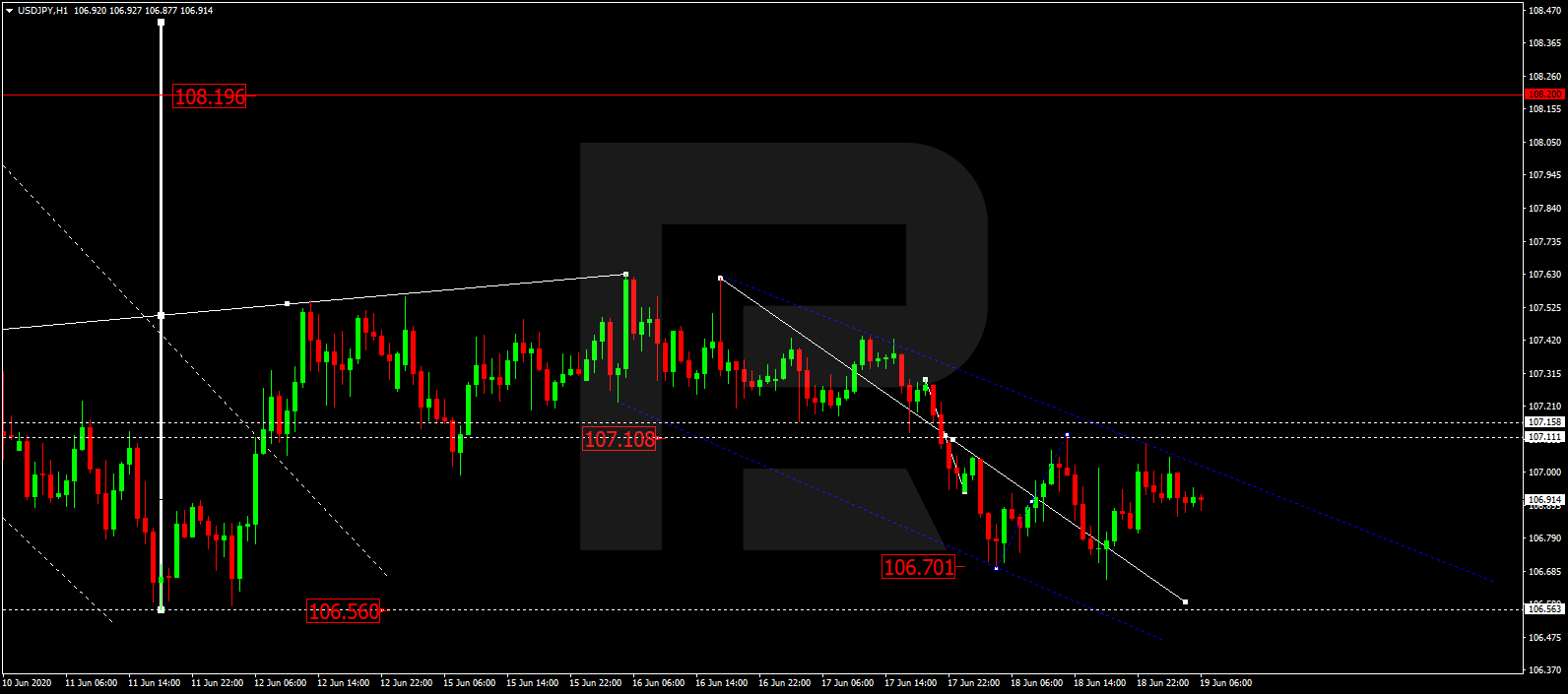

USDJPY, “US Dollar vs Japanese Yen”

USDJPY continues falling towards 106.60. After that, the instrument may correct to test 107.10 from below then resume trading downwards with the target at 106.00.

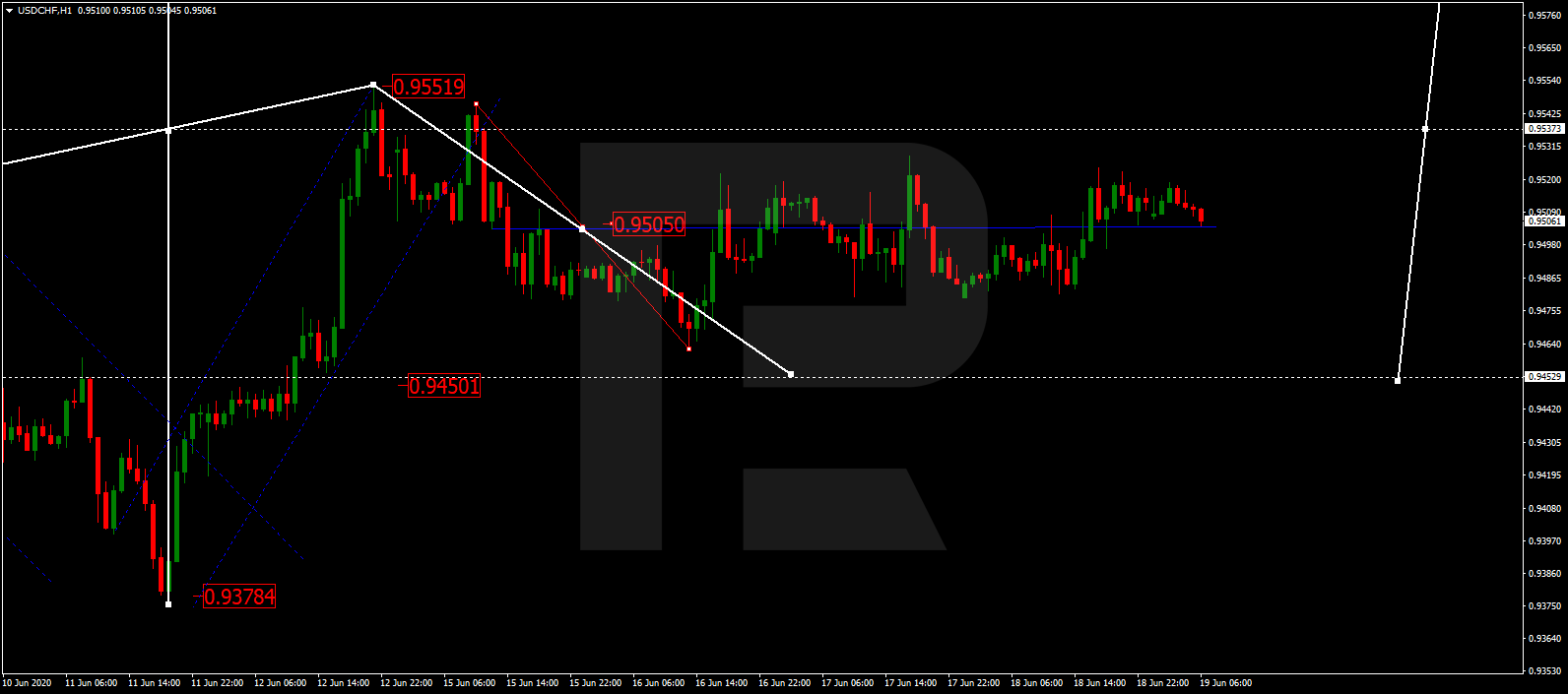

USDCHF, “US Dollar vs Swiss Franc”

USDCHF is still consolidating around 0.9500. Possibly, today the pair may fall to reach 0.9450 and then form one more ascending structure to break 0.9550. Later, the market may continue trading upwards with the short-term target at 0.9650.

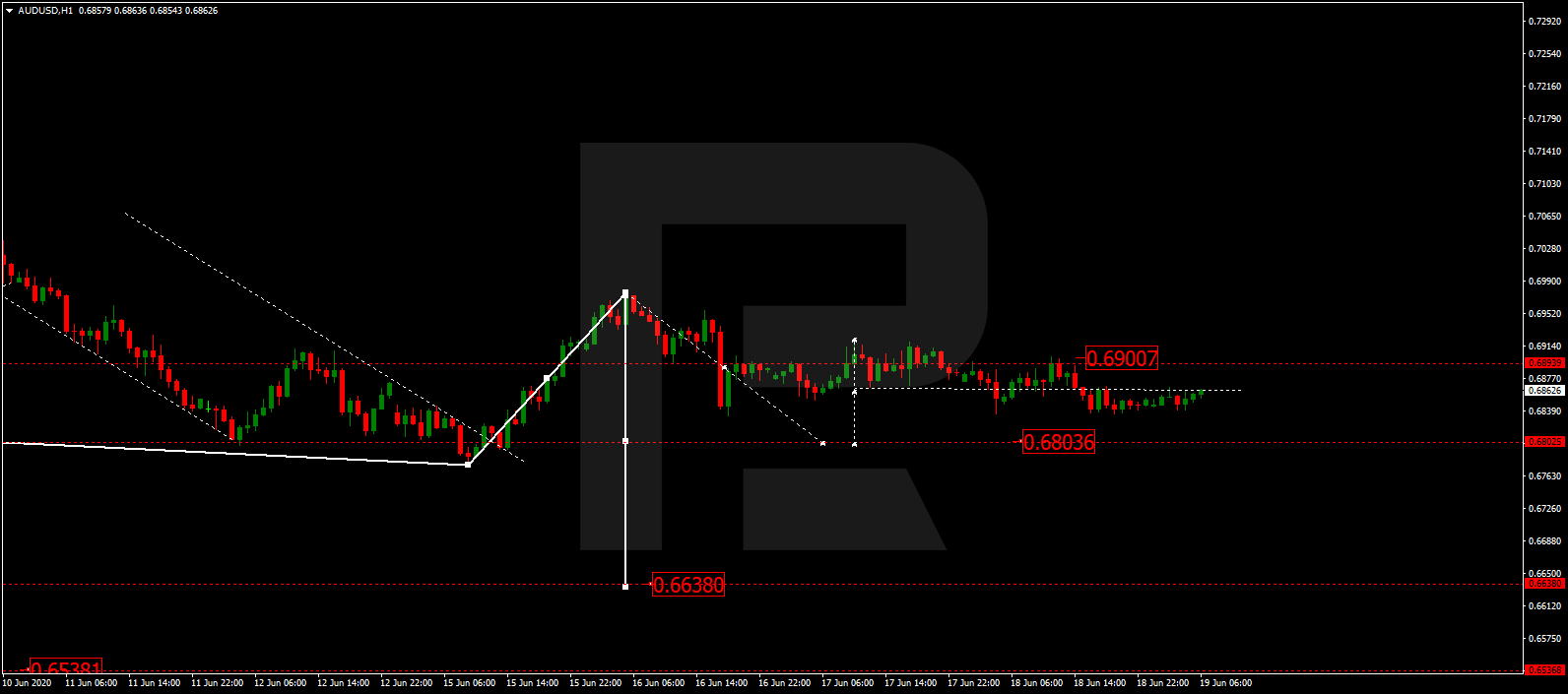

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD is consolidating around 0.6900. Today, the pair may form a new descending wave towards 0.6800 and then grow to return to 0.6900. If later the price breaks the range to the downside, the market may resume trading downwards with the short-term target at 0.6716.

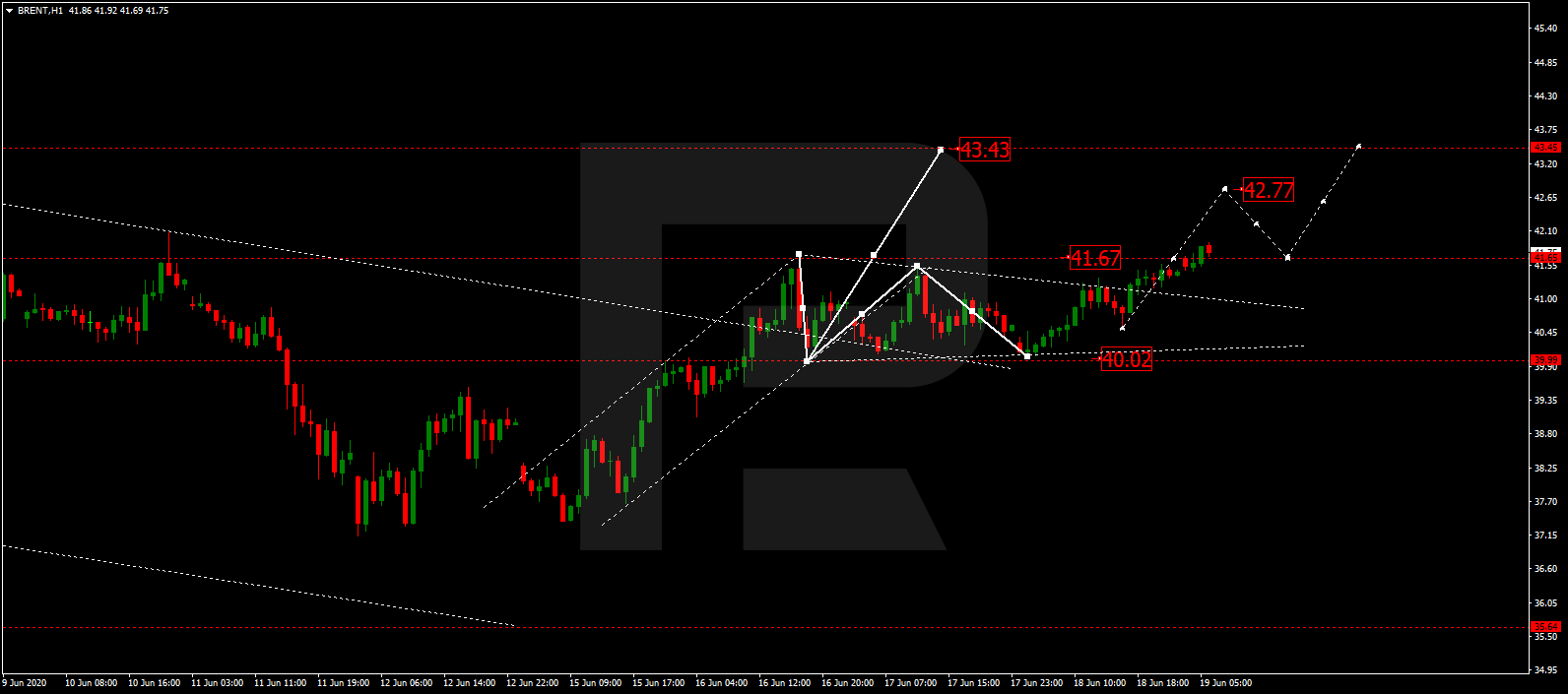

BRENT

Brent is moving upwards. Possibly, the pair may break 41.67 and then continue growing to reach 42.77 or even 43.43. After that, the instrument may start a new correction towards 41.65 and then form one more ascending structure with the target at 47.50.

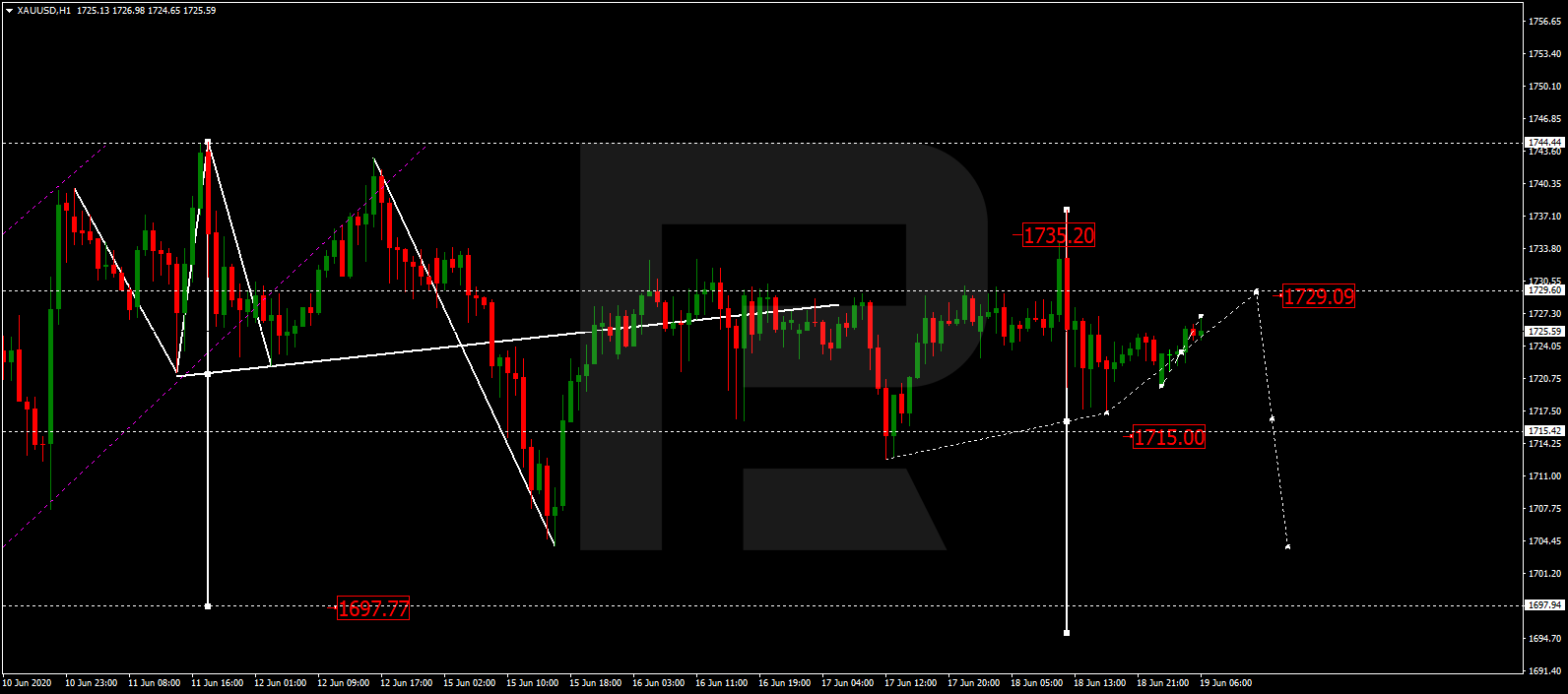

XAUUSD, “Gold vs US Dollar”

After completing the descending impulse towards 1720.00, Gold is correcting towards 1729.00. Today, the pair may fall to reach 1705.00 and then form one more ascending structure towards 1715.00. Later, the market may start another decline with the first target at 1697.77.

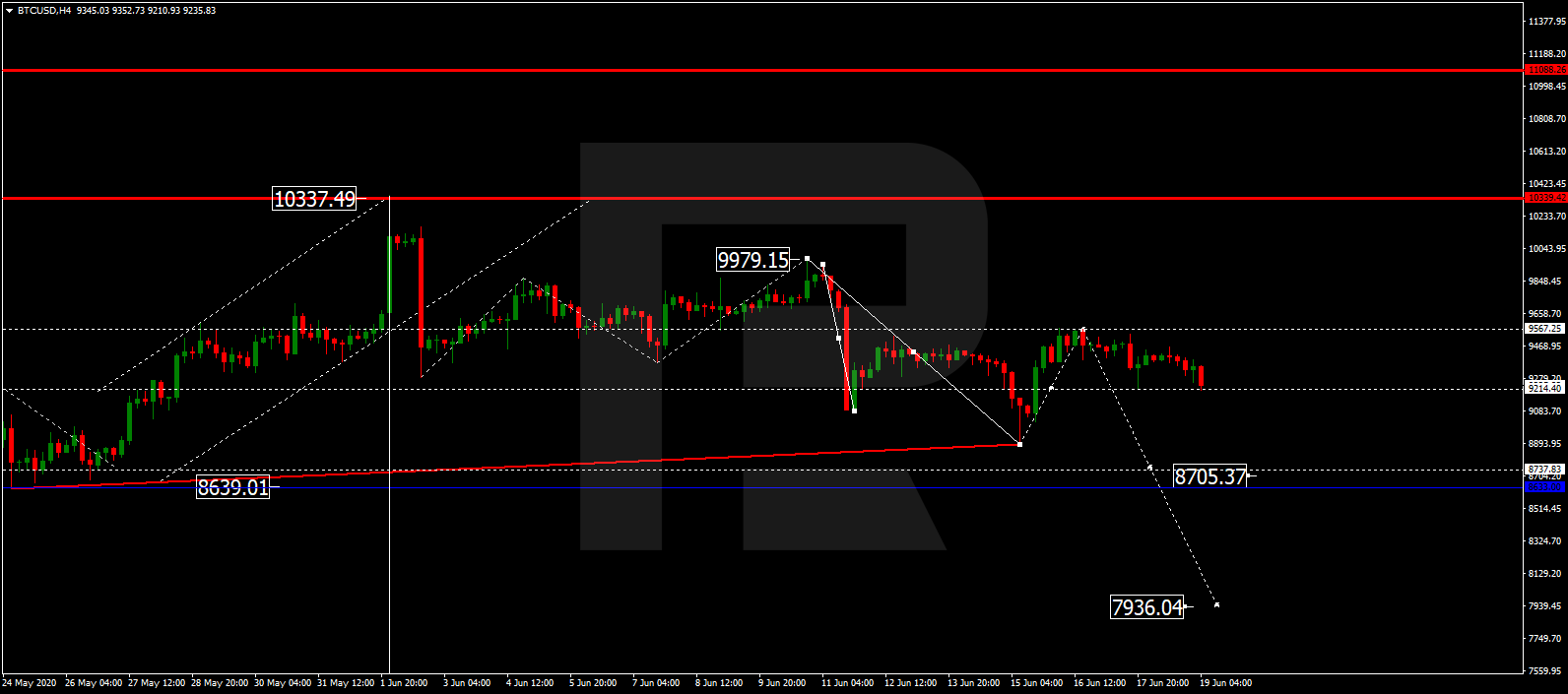

BTCUSD, “Bitcoin vs US Dollar”

BTCUSD is falling to break 9000.00. After that, the instrument may continue trading inside the downtrend towards 8700.00 or even with the short-term target at 7950.00.

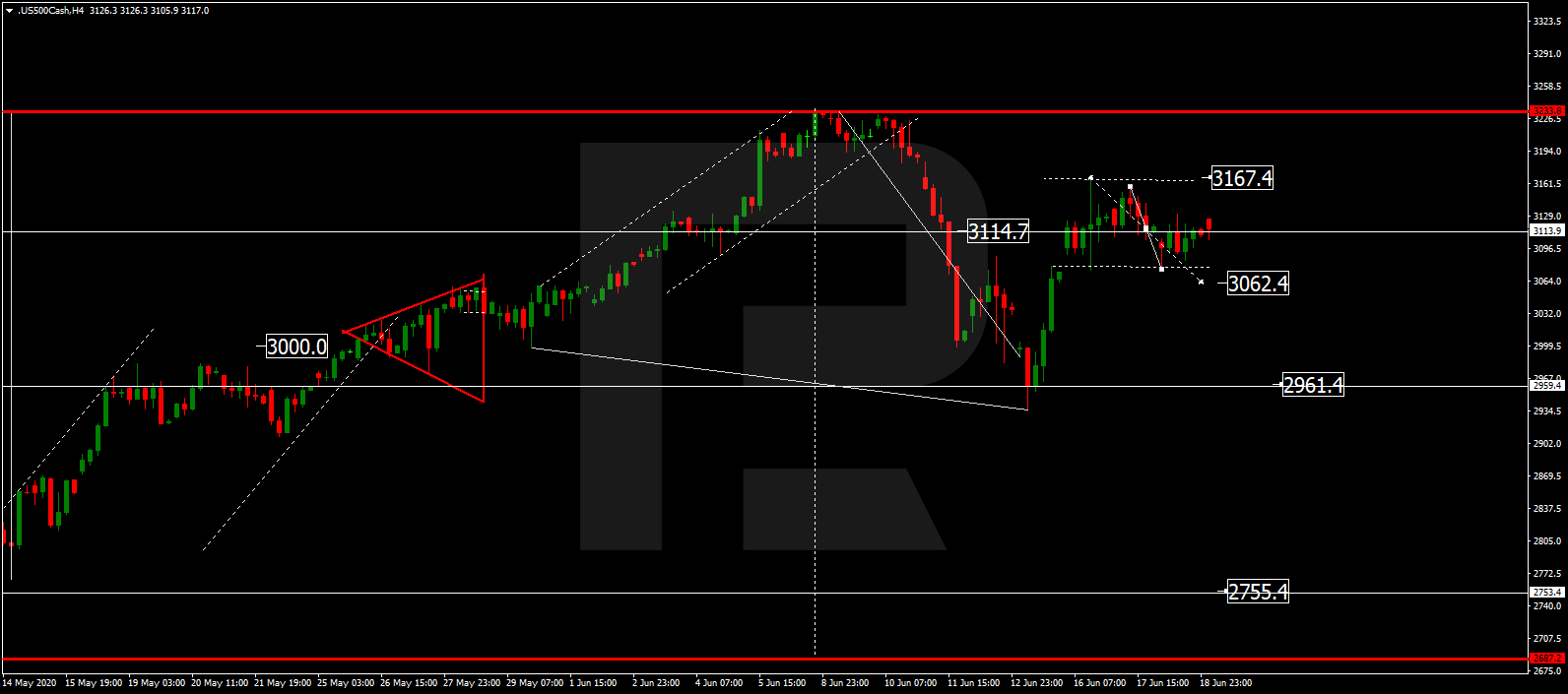

S&P 500

The Index is consolidating around 3115.0 without any particular direction. Possibly, the asset may expand the range down to 3062.5 and then form one more ascending structure to return to 3115.0. Later, the market may start a new decline to break 2961.4 and then continue trading downwards with the short-term target at 2755.5.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.