The central bank of Belarus cut its benchmark interest rate for the third time, saying domestic inflation was slowing faster than expected while inflation in trading partners was also slowing down more rapidly, leading other central banks to actively lower their interest rates.

The National Bank of the Republic of Belarus (NBRB) cut its refinancing rate by another 25 basis points to 7.75 percent and has now cut it 125 points this year following cuts in February and May.

Since April 2016 NBRB has been easing its monetary policy and cut the rate 19 times by a total of 17.25 percentage points.

The rate cut was decided at an extraordinary meeting of NBB’s board today, ahead of the scheduled meeting on Aug. 12, with the rate cut taking effect on July 1.

In addition to cutting the refinancing rate, the overnight loan rate was also cut 25 basis points to 8.75 percent and the overnight deposit rate to 6.75 percent.

The board meeting comes after Belarus President Alexander Lukashenko on Friday asked the central bank to look into lowering the refinancing rate at a meeting to discuss economic support measures, according to local press reports.

According to BelTA, the state-owned national news agency, Lukashenko said all countries are lowering their interest rates to revive economic activity, inflation is within forecasts, and the central bank should carry out this rate cut before the end of June.

Belarus, formerly known as White Russia or Belorussia, became independent of the Soviet Union in 1991 and Lukashenko has been president since 1994.

Headline inflation in Belarus eased to 4.9 percent in May from 5.4 percent in April, just below NBRB’s target of 5.0 percent, while core inflation slowed to 3.9 percent from 4.5 percent in April.

Under these conditions, the central bank said continued easing its monetary policy, with moderately soft monetary conditions would allow it to maintain an acceptable level of price and financial stability.

After depreciating sharply in February and March, the Belarus ruble has risen since April though it remains well below its level at the start of the year.

In January Belarus’ government and the central bank adopted a major strategy to improve trust in the Belarusian ruble by pushing a coordinated policy to reduce reliance of foreign currency in the country and ensure the domestic currency had a leading role in transactions.

The government’s debt is around 97 percent denominated in foreign currency. A new Belarusian ruble was introduced in July 2016.

This strategy includes full transition to inflation targeting by 2021, a reduced footprint by NBRB in the foreign exchange market, reduced monopolies in the economy, lower state debt, regular issues of debt in Belarusian rubles, and ensuring that all taxes, rents, tariffs and prices by state-run organizations are set in Belarusian rubles.

The Belarusian ruble was trading at 2.37 to the U.S. dollar today, up 10.5 percent from a record low of 2.62 on March 24 and down 11.4 percent this year.

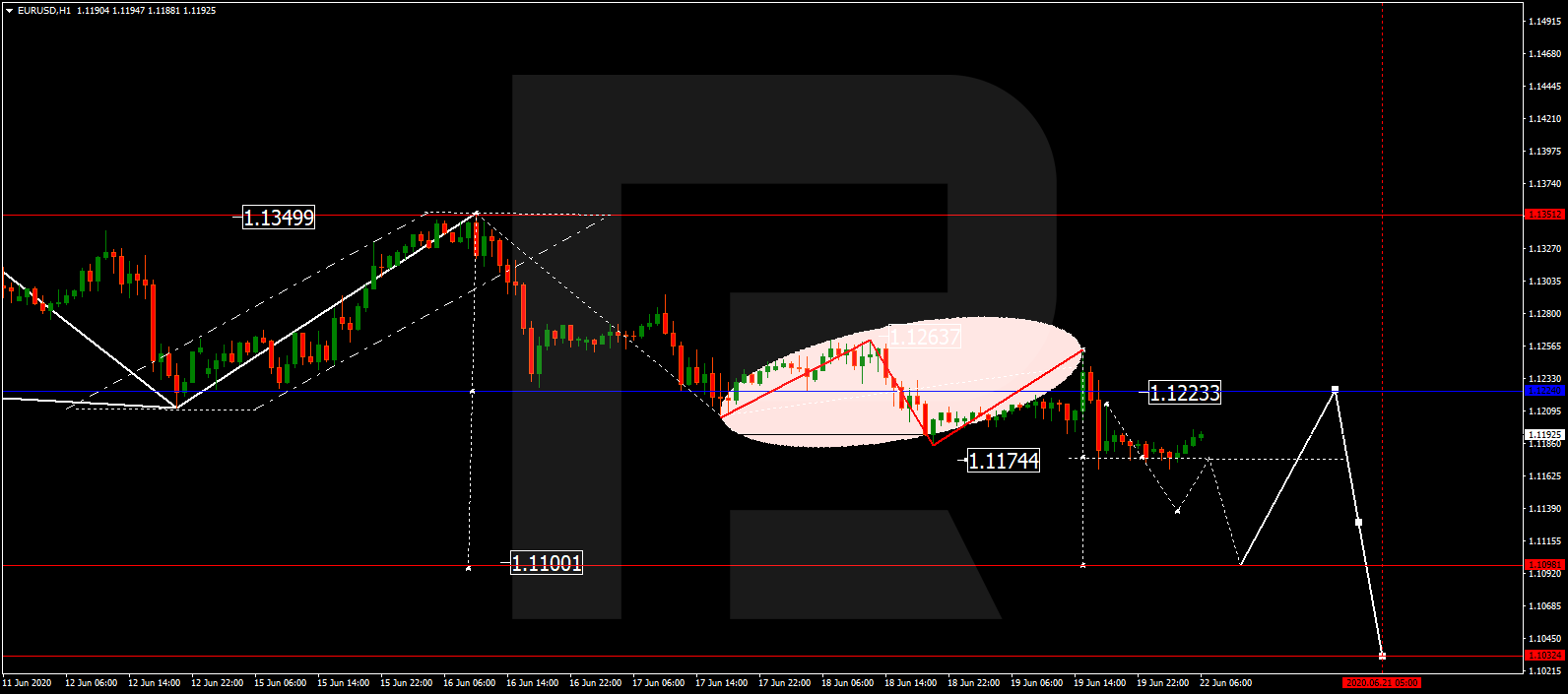

After being badly bullied by king Dollar and most G10 currencies last week, the Euro has stormed into the new trading week with a renewed appetite for revenge.

Over the past 18 hours, the Euro has jumped almost 1% against the Dollar, sending prices back above the 1.1250 psychological level. The sheer momentum of this astonishing rebound suggests that the EURUSD may target 1.1290 in the short term with a softer Dollar guiding prices closer towards 1.1300 before fundamentals steal the show.

It must be kept in mind that the core factors weighing on the European single currency remain unchanged. Fears of a second wave of coronavirus, uncertainty over the European Commission’s recovery fund and disappointing economic data are just a handful of negative themes haunting investor attraction towards the Euro.

Euro volatility may be on the cards on Tuesday, June 23rd as the latest PMI’s from France and Germany will be published. This will be accompanied by the EU Manufacturing PMI which should offer insight into how the coronavirus has impacted the manufacturing sector. The Euro could become timid, meek and shy against other G10 currencies if the pending data fails to meet market expectations.

Looking at the technical picture, the EURUSD has the potential to target 1.1300 if 1.1250 proves to be reliable support on the H4 timeframe. Bears still have some degree of control below the 1.1300 resistance with sustained weakness under this level taking prices back towards 1.1250 and 1.1170.

On the daily timeframe, prices are back within the wide 160 pip range with support around 1.1200 and resistance at 1.1360. A daily close back above 1.1280 could encourage a move back towards the upper range at 1.1360.

While the near-term outlook for the Euro will be influenced by the pending PMI’s, the medium to longer-term remains in favour of bears. If the Dollar finds it footing and wakes up from its current slumber, the Euro will be in trouble once again.