US frozen beef supplies suffered a steep drop last month according to the US Department of Agriculture National Agricultural Statistics Service (NASS) monthly report released a couple of days ago. The total amount of beef in freezers was recorded at 415.221 million pounds, down 64.235 million, or 13.4%, from 479.456 million the previous month. Lower supply is bullish for the live cattle price. However, US cattle ranchers experience a massive backlog even as many slaughterhouses come back online with meat production recovering after a drop because of shutdowns of slaughterhouses and processing plants due to coronavirus outbreak. Thus, processors killed an estimated 119,000 cattle last Friday, up from 115,000 cattle a week earlier. Increasing production is a downside risk for the live cattle price.

By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

One of the biggest lessons learnt over the past three months is to respect the trend. Whether you believe the economy will go through a V, U, W, L or whatever-shaped recovery, going against the trend supported by enormous spending from central banks led by the Federal Reserve is a losing trade.

However, up trends may not be sustainable for a long time if they are not supported by fundamentals. By fundamentals we mean sustained economic recovery and improved earnings. As of now, many investors believe those earnings next year will return to 2019 levels for the S&P 500. If that’s the case, the steep rebound in equities seen since March 23 is justified and given that interest rates will remain near zero for a prolonged period, the reflation trade may still have a further way to go.

On the economic front, several indicators have bounced sharply since the coronavirus pandemic, that is especially true for leading economic data such as PMIs from across the US, Europe and China. But let us not forget they are picking up from an exceptionally low base and will only become meaningful if sustained.

Over the past 10 trading days the equity market has sold off twice, on June 11 and 24 with the S&P 500 declining 5.9% and 2.6% respectively. Such big moves are clear signs of anxiety. The index is now flirting with the long term 200-day moving average and a break below may be a threatening sign for the bullish trend. Short-term pessimism among investors has risen to unusually high levels according to the latest AAII sentiment survey and that may translate into further profit taking if the index breaks below the 200-day moving average.

These are all warning signs for the 3-month bull market. After a significant run, the question now is if there is still further fuel for the rally or are we on the verge of a reverse in trend? Of course, there are reasons to become cautious. Recent spikes in Covid-19 cases in several US states and across the globe is putting the re-opening of economies into question. Whether we’re seeing a second wave or just a continuation of the first wave, the outbreak may reverse actions taken by governments to re-open their economies, hence curbing hopes of a smooth recovery.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Equity markets are in red currently with US data expected to yet again show over million more Americans sought unemployment benefits last week while the declining trend for new applications persisted. Stock markets traded mixed yesterday in light of rising new coronavirus cases globally.

Forex news

Currency Pair

Change

EUR USD

-0.8%

GBP USD

+1.4%

USD JPY

-0.8%

The Dollar strengthening is intact today ahead of US Labor Department report expected to show 1.3 million Americans likely sought unemployment benefits over the last weeks. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, rose 0.5% Wednesday despite a Federal Housing Finance Agency report housing prices in US rose slower than expected in April. Both GBP/USD and EUR/USD reversed their climbing yesterday despite an Ifo institute report German business sentiment recorded its strongest recovery in June since the start of the statistics in 1990. Both pairs are down currently ahead of the release of European Central Bank monetary policy meeting minutes today. USD/JPY reversed its sliding yesterday while AUD/USD resumed its sliding with both yen and Australian dollar lower against the greenback currently.

Stock Market news

Indices

Change

Dow Jones Index

-0.32%

Nikkei Index

-1.58%

Australian Stock Index

-0.62%

Futures on three main US stock indexes are down today after a selloff on Wednesday. Stock indexes in US ended sharply lower on Wednesday as Chicago Fed President Charles Evans said the US economy may require more monetary stimulus. The three main US stock indexes recorded losses ranging from 2.2% to 2.7%. European stock indexes are extending losses currently after a pullback Wednesday following reports that US is considering imposing tariffs on some $3.1 billion worth of goods from France, Germany, Spain and the UK including beer, gin, olives and trucks. Asian indexes are mostly lower today led by Australia’s All Ordinaries ASX 200 with markets in Hong Kong and mainland China closed for holidays.

Commodity Market news

Commodities

Change

Brent Crude Oil

-0.83%

WTI Crude

-1.2%

Brent is edging lower today. Prices pulled back Wednesday after the US Energy Information Administration report that US crude oil inventories rose 1.4 million barrels last week for third week in a row. The US oil benchmark West Texas Intermediate (WTI) futures fell: July WTI lost 5.9% and is down currently. August Brent crude closed 5.4% lower at $40.31 a barrel on Wednesday.

Gold Market News

Metals

Change

Gold

+0.26%

Gold prices are extending losses today. August gold slipped 0.4% to $1775.10 an ounce on Wednesday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Jericho Oil Corp.’s just-closed $5 million insider financing allows it to capitalize on the distress in the market right now.

Update: On June 23, investor Michael L. Graves announced that through Catlett Sands-II, LLC he had acquired additional 8.473 million shares of Jericho Oil, bringing his total ownership via Catlett Sands and Inter Vivos Trust to approximately 16% of the firm.

With many small oil producers fighting for survival, Jericho Oil Corp. (JCO:TSX.V; JROOF:OTC) has taken the opposite tack and plans to go on the offensive and acquire assets, recently closing a $5 million non-brokered private placement with existing large shareholders.

“Jericho sees opportunity in the present environment and will look to acquire what it perceives to be high-quality assets in special situations,” the company stated. “While Jericho does not currently have any binding agreement to enter into any such transaction, having cash on hand will allow it to be nimble as market opportunities may present themselves.”

“Jericho Oil is regarded as an interesting speculative play here for a possible reversal leading to a potentially sharp upleg.” – Technical analyst Clive Maund

Jericho benefits from a tight share structure with committed shareholders. “Insiders own around 27% of Jericho’s shares, with another 50% or so owned by large shareholders and family offices. There were just a handful of investors in the private placement that closed on June 12, four of whom comprised the vast majority,” Jericho CEO Brian Williamson told Streetwise Reports.

“Our shareholder base provides us not just capital, but also valuable access to some of the most knowledgeable and successful oil and gas families and great business leaders,” Williamson said. “Having shareholders and access to incredibly successful leaders like Ed Breen, CEO of Dupont (DD:NYSE), a $38.5 billion market cap company, and others of his ilk, provides us with great resources to assist in navigating these markets. They believe that these are the times in which to act and we couldn’t agree more. We have seen that it’s not always the best price that wins in a market like this, it’s speed and certainty of closing that are the most valuable assets.”

Technical analyst Clive Maund has Jericho on his radar, writing on June 15, “The company is understood to have some powerful backers, which helps to explain why the financing was fully subscribed even in the current awful environment for the industry, which is thought to bode well. . .Jericho Oil is regarded as an interesting speculative play here for a possible reversal leading to a potentially sharp upleg.”

Jericho has raised $47 million since 2014. “With all those raises we have never engaged a bank or paid a finder’s fee,” Williamson said. “Why is that important? With banking fees ranging from 6% to 8% that means we have not paid ~$3.5 million in fees. That money has gone ‘into the ground.’ ”

“Our insiders and large shareholders is why we have closed every deal that we have been the successful bidder. Our shareholders are there for us when we need to close on a deal. I am confident that going forward we can continue to expect their support. History has shown that,” Williamson stated.

Jericho is one of the few junior oil companies raising money in this market and credits the company’s shareholder base. “We can call on our shareholders for financing and advice. We are unique in that regard and one of the reasons I believe this team will be the junior to capitalize on the distress in the market right now,” Jericho Director Allen Wilson noted.

Steven Hegna, a longtime shareholder of Jericho, said, “Having owned and operated my business for 20+ years, I know what it takes to build and run a company through good and bad markets. And I’ve seen Jericho’s management team react through good and bad markets as well. They are doing an excellent, responsible job and that is part of the reason I continue to support this oil company. They are driven to succeed.”

“Never a company to waste a crisis and noticing the carnage in the marketplace, we decided to turn the situation to our advantage,” Williamson said. “The oil market has had very little opportunity to realize any sizeable upside in the last five years, as the price of oil has stayed under or around $50 per barrel for most of that time with heavy bouts of volatility. Many companies began to drill wells only to see the forecasted revenue materially change to their detriment due to drastic price declines. With many of these wells drilled on debt, a downturns like this can create distress. This seems like a buyers’ market but there is a lot of capital looking for ‘cheap deals’ and few sellers. We believe Jericho’s ability to offer both cash and stock in a transaction provides optimism for potential upside and the company’s capacity to act quickly could be the key to its success in this market.”

The firm is focusing on major and mid-major oil companies that are selling non-core assets. “Those assets can be hundreds of barrels a day of production that we can make money on at these prices. Why? We have assembled a top tier team that can operate them and by default, our G&A will be lower. That couldn’t be more evidenced by the team taking pay cuts now. We have incentivized our top tier team with options to keep that G&A down and align our team’s success with the shareholders,” Williamson stated.

“The idea is to look for a larger acreage position held by existing production, ultimately maintaining the resource upside in the ground so that as prices recover, we see the opportunity to develop those assets in a meaningful way,” Shane Matson, Jericho’s head of geology, said. “We see the opportunity in mid-to-large cap companies shedding non-core or smaller assets with a lot of development upside that a small company can turn into real value.”

Jericho plans to use the funds as leverage to obtain larger projects. “We see the $5 million as a placeholder with the goal of doing something bigger. It also demonstrates to the market that our shareholders are there to push our advantaged position through this market turmoil. We want to be the minnow that swallows the whale,” Williamson said.

“We will continue to do what we do best: stay nimble and look to capitalize,” Williamson said. “Pursuing this equity raise leaves our balance sheet in a strong position. We see this as an opportunity to make Jericho bigger, stronger and more powerful in terms of the quality of the assets.”

“The complete shock of the COVID pandemic and resulting oil price action has left the current marketplace for acquisitions limited, with many debt holders in the driver’s seat for many of these stressed situations. Once the pandemic aftermath settles, we believe assets will make their way to the market over the next 60120 days, where we will look to be opportunistic. We hope our shareholders will be rewarded for their patience and resolve,” Williamson concluded.

Technical analyst Clive Maund wrote on June 15, “One of the remarkable attributes of Jericho Oil is that, despite being a junior oil company and therefore a member of one of the most out of favor sectors that you could find in the recent past, it has just managed to complete a $5 million financingthat was fully subscribed and mostly bought by insiders and the money raised is not going to be used to keep the company limping along until it has to “pass the hat round again” but instead is to be earmarked for future strategic acquisitions. Its stock is very cheap here after a severe 2-year bear market and the reason that we have some interest in it now is that, in addition to the above mentioned positive fundamentals, there are subtle signs on its charts that it may be about to reverse to the upside.”

Disclosure: 1) Patrice Fusillo compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Jericho Oil. Click here for important disclosures about sponsor fees. An affiliate of Streetwise Reports is conducting a digital media marketing campaign for this article on behalf of Jericho Oil. Please click here for more information.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Jericho Oil, a company mentioned in this article.

Additional Disclosure

CliveMaund.com Clive Maund does not own shares of Jericho Oil, and neither he nor his company has a financial relationship with the company.

The Weekly Missive, which usually arrives over the weekend (sometimes on Friday, sometimes on Sunday) was delayed this weekend for one reason: I had to change it.

I started out last week with an idea that was leaning in the direction of full-on capitulation in the sense that this latest, three-month, Fed-fueled rally was beginning to smell like 2009 and 2002 and 1988. All occurred after precipitous market plunges; all were the direct result of Fed policy actions; and all obliterated the shorts.

I have been very successful in 2020 in moving into markets gripped with fear and moving away from markets obsessed with greed, but of those two emotions that have always been the “controllers” of markets since the late 1800s, greed absolutely conflagrates during Fed “printing” orgies, while fear dissipates into only minor outbursts of selling. This has been the exact playbook by which the Fed (totally owned and operated by a consortium of publicly traded banks) has been able to change the “rules of engagement” by which traders and investors have operated since inception.

These two emotions are like the exertion required in weight training to move muscle efficiency to its maximum; muscles must be forced to strain against immovable mass to become “Olympian.” However, remove “mass” from the exertion and you have zero result in muscle development and sculpture. Remove “fear” from the “free market capitalism” equation and you not only have a market completely hijacked by “greed,” you have a “condition” whereby the buying and selling of stocks and bonds and gold and silver only resemble a “market.” In reality, it is anything but a market. Athletic endeavor devoid of meaningful resistance is not “training;” the buying and selling of stocks devoid of meaningful risk carries no science, and therefore is not anything close to what we older guys used to call a “stock market.”

I want to talk tonight about something that I hold remarkably close to my heart: Mother Nature. I was recently anchoring in a small baylet within the larger entity known as Georgian Bay when a rather larger turtle arrived at the side of the boat looking for some after-dinner food scraps. This beast had a head the size of a German shepherd, with a shell at least one foot in radius, and the way it moved around in its own environment was nothing less than impressive.

Upon sighting the creature, my fellow boaters bolted for dry land but as I was still in the water, I decided to swim toward the leviathan and see what his reaction might be to a curious neighbor, non-threatening in his 67-year-old body, and unquestionably at this prehistoric monster’s beck and call.

What happened is the topic of tonight’s missive. Did this 75-pound snapper look at me and decide that “Mama just rang the luncheon bell?” The answer is “Hell no!!!” This reptilian beast just turned and ran for the closest shoreline, scrambling up the banks with his prehistoric claws only to retract all arms, legs and heads into a shell totally impenetrable to human hand, foot or teeth (all of which our human ancestors have tried).

I was standing no more than six feet from the head of this creature, as he retreated in true “defensive posture,” when it finally occurred to me that he has been forced to do this all of his life. He is like a seasoned stock trader that has learned all rules but is finally unable to apply them to the function of “making money.” The term “defensive shell” has never carried more meaning.

Somewhere around the year 2002, the stock market stopped taking its cues from market mavens like Dan Farrell and Martin Zweig, and began to react to a new wave of market “rock stars”only this time, the rocks stars weren’t math wizards or ex-floor traders. The new breed of financial pied pipers were economiststhe most boring group of academics on the planet. By and large, these newborn market messiahs had never had to meet a payroll; they had never been recipients of the dreaded margin calls issued by brokers in need of additional collateral for a failed trade.

In fact, from 2002 until today, the track record of this gaggle of prognosticating pitchmen has been as dreadful as any in the history of financial (and economic) forecasting. So, considering their meager business experience and poor results, how is it that they can still be relied upon for guidance? The reason is that they are “central bankers,” the unelected chosen few bequeathed the elite privilege to be custodians of the creation of credit and the maintenance and longevity of bull markets in stocks.

Those born before 2002, and especially those trained in the Inflationary Seventies, would be hard-pressed to even name the Fed chairman of the era. The role of the Fed was different back then, as they cringed away from cameras and spotlights and were generally allergic to sunlight. You might have a comment on page 11 of the Wall Street Journal, but never, ever would you have a twenty-minute segment on “60 Minutes” with the Fed chairman, for two very strong reasons: 1) they were generally devoid of any semblance of charisma, and 2) there would be no viewers because no one cared.

Investing in 2020 has become an exercise in mind-reading, body language interpretation and tie color guessing. Jerome Powell seems to prefer grey suits and purple ties, but he also prefers lights, cameras and a great deal of action as he carves out his well-earned legacy as “Savior of the 2012???? bull market in everything.”

I guess that is why I have such a difficult time capitulating to the status quo of “don’t fight the Fed.” It is not as if I disagree with it; I learned it back in the 1980s from my hero and popular guest Martin Zweig on what was the only television show in the U.S. covering stocks (and, to a lesser degree, bonds) at the time. It was Louis Rukeyser’s “Wall Street Week.”

Not surprisingly, it wasn’t some CNBC anchor or “guest commentator” that invented the phrase; it was Zweig’s double-pronged rule, which I continue to obey to this very day, that says “You don’t fight the Fed and you don’t fight the tape.”

And when I tell you that even rules as simple as these have been rendered obsolete, I will also tell you that the reason they are obsolete is that in 2020, the Fed is the “tape.” Absent the natural flow of resistance, the muscle that gets flexed every time the markets enter a corrective phase is the money-printing bicep, and it matters not whether you called economic activity correctly, you will get killed if you take a position counter-friendly to the whims of Powell and Company.

However, it is my considered view that this love affair with central banking’s caretaking role of salvaging markets and prolonging periods of obvious over-valuation is about to come to a resounding halt. The brainwashing of the younger generation of Fed-fondling opportunists has made them like the rats following the piper off the pier and into the canal. The musical narcotic of free money and upwardly manipulated prices is at once captivating and intoxicating, and it is only when the drip from these intravenous stimuli is removed that the markets relapse into convulsive spasms of reality-check liquidation.

That is what I see happening over the second half of 2020, as either rampant inflation or devastating deflation descends upon the valuation landscape. In either event, of course, gold and silver will undoubtedly outperform, so long-term holders should be rewarded in spades. For new investors coming into the markets, they have to ask themselves whether they are late or early in establishing their initial precious metals positions.

More than a few subscribers have asked me what it will take for me to revisit my two favorite gold miner exchange-traded funds (ETFs), the Senior Gold Miner (GDX:US) and the Junior Gold Miner (GDXJ:US). The answer is twofold: First, I want to exit the period of seasonal weakness, which some would say is the end of June, but my experience says is in late July or early August.

Second, getting back to the Marty Zweig rule, we know that both fiscal and monetary conditions are wildly bullish for precious metals, which means that we don’t fight the Fed. Since gold is still in a trading range, the tape is not completely friendly. While it is by no means hostile, I would change my stance and go long GLD, SLV, and the GDX/GDXJ dynamic duo if gold enters an extension move above the April 14 intraday high at US$1,789/ounce. By that, I mean at least two or three daily closes above that level, lest we get hit with a whipsaw reversal.

In the interim, I continue to accumulate gold and silver developers with ounces in the ground and dynamic leverage to any upside in precious metals prices. There are also more than a few exploration issues that have once again pulled back to levels from which there is minimal downside versus significant upside in the event of a discovery. These will be ideal purchase candidates in August and subscribers will receive the complete list at that time.

It is the junior gold developers that are going to get the most love once the precious metals’ trading ranges are vacated. Silver certainly has the leverage to explode from here given the gold-silver ratio (GSR) at 98. But when the legions of new precious metals enthusiasts enter the battlefield, it is the gold stocks that will be most sought after. Hence, my largest holding remains Getchell Gold Corp. (GTCH:CSE) (US$0.195), whose 1,069,000 ounces at Fondaway Canyon, Nevada, are valued at roughly US$14.60 per ounce (cheap by any and all measurements).

We are now officially into the seasonally quiet period (summer markets are boring), so I will continue to accumulate in anticipation of an explosive conclusion to 2020, as the unintended consequences of central bank insanity weighs heavily on purchasing power fragility in the global currency arena. Supply shocks are starting to impact food prices, so if you think that protests over police misbehavior are alarming, watch the incendiary acceleration in pitchforks and torches once milk and bread prices start to double. Will the restless masses be willing to accept rampant inflation on top of disappearing jobs? There is only one answer:

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Getchell Gold. My company has a financial relationship with the following companies referred to in this article: Getchell Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold, a company mentioned in this article.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Fund manager Adrian Day assesses recent developments at two junior gold companies, as well as provides a brief update on the gold market.

Midland Exploration Inc. (MD:TSX.V, 0.86) has optioned its Casault property to neighboring company Wallbridge Mining Co. Ltd. (WM:TSX), which made a discovery on its property last year. We view this as potentially quite positive, both because Wallbridge is well financed and aggressive, but also because it has a high profile, with leading gold investor Eric Sprott as a recent shareholder. Midland should come to the attention of gold investors who follow Mr. Sprott. Wallbridge has been consolidating the area, and earlier this year acquired Balmoral Resources.

Casult, on the prolific Detour Trend in northwest Quebec, consists of 322 claims, and includes the Vortex Zone discovered by Midland and then-partner Soquem Inc.; Vortex returned some high grades in 2017, but it was never properly followed up. Earlier this year, Soquem returned the property in exchange for base metals properties in Gatineau. (Soquem, a government mining unit, focuses on base metals more than gold.)

Money in the ground

Wallbridge can earn a 50% interest over a four-year period by spending $5 million and making modest payments to Midland. Expenditures and payments increase to take Wallbridge to 65%. It will be the operator, and will commence immediately on exploration at Vortex. Walbridge said the agreement “sets the stage for additional discoveries.” Midland retains other land in the Detour Belt, which it plans to explore this coming season.

With a strong balance sheet (CA$13 million), technically strong and market-savvy management, a deep property portfolio with a growing list of partners, and a recommitment to the prospect generator model, Midland is one of our favorite exploration companies. This new agreement provides a catalyst and makes Midland a buy at this price.

Vista Monetizes Assets to Fund Growing Mount Todd Property

Vista Gold Corp. (VGZ:NYSE.MKT; VGZ:TSX, US$0.91) said recent geologic work suggests continuity of mineralization among three deposits at its Mount Todd property in Australia, which, together with a stronger gold price, makes it “possible to envision a 20-year mine life,” according to CEO Frederick Earnest.

Raising money without diluting shareholders

Separately, the company amended its option agreement on its Guadalupe de los Reyes, accelerating its final option agreement and granting Prime Mining Corp. (PRYM:TSX.V) the right to purchase an option and other rights on the property. This continues Vista’s program of monetizing various assets in order to focus on Mount Todd, without a dilutive equity raise. Together with a recent agreement on an Indonesian property, Vista now stands to realize over $6 million over the next 16 months.

Because of the recent run in Vista’s stock price and our concern about a possible pullback in the gold price, we are holding, but would be buyers on a correction.

Top Buys

Despite a strong rally on Friday, gold appears to be losing short-term momentum, with increasingly smaller inflows into gold exchange-traded funds (ETFs)and almost $100 million of withdrawals on the last reported day. Gold mutual funds are also seeing smaller inflows and coin sales have dried up. Gold stocks have also seen lower highs and lower lows over the past month. This all suggests the rally is losing momentum, and we could see a pullback in the next few weeks.

Much the same holds true for many other resources. Because of these concerns, we are buying little in the gold, or resource, space right now, but stand ready to buy on meaningful pullbacks.

Adrian Day, London-born and a graduate of the London School of Economics, heads the money management firm Adrian Day Asset Management, where he manages discretionary accounts in both global and resource areas. Day is also sub-adviser to the EuroPacific Gold Fund (EPGFX). His latest book is “Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks.”

Disclosure: 1) Adrian Day: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Evrim Resources, Midland Exploration, Royal Gold. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Funds controlled by Adrian Day Asset Management hold shares of the following companies mentioned in this article: All. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Midland Exploration, Osisko Gold Royalties, Vista Gold and Evrim Resources, companies mentioned in this article.

Translate Bio shares traded 45% higher reaching a new 52-week high after the company reported that it is expanding its collaboration with Sanofi Pasteur to develop mRNA vaccines across all infectious disease areas.

Clinical-stage messenger RNA (mRNA) therapeutics company Translate Bio Inc. (TBIO:NASDAQ) and Sanofi Pasteur, the vaccines global business unit of Sanofi SA (SNY:NYSE), today announced that “the two firms have agreed to expand their existing 2018 collaboration and license agreement to develop mRNA vaccines for infectious diseases.”

The companies advised that under the terms of the expanded agreement, “Translate Bio will receive a total upfront payment of $425 million, consisting of a $300 million cash payment and a private placement common stock investment of $125 million at $25.59 per share representing a 50 percent premium to the 20-day moving average share price prior to signing.” Translate Bio will also be eligible to receive additional payments up to $1.9 billion if certain milestones are met as stipulated in the terms of the 2018 agreement.

Sanofi Pasteur will be responsible for all costs during the collaboration term and in return will receive the exclusive worldwide rights for infectious disease vaccines.

Sanofi Pasteur’s EVP Thomas Triomphe remarked, “As all eyes are on prevention of infectious disease through vaccines, this is a pointed moment in time where we are called upon to seek innovative ways to protect public health…We are excited by the novel technology and expertise Translate Bio brings, and we believe that adding this mRNA platform to our vaccines development capabilities will help us advance prevention against current and future infectious diseases.”

Ronald Renaud, CEO of Translate Bio, commented, “The expansion of our collaboration with Sanofi Pasteur validates the progress we’ve made in the development of mRNA vaccines for infectious diseases since our work together began in 2018 and also speaks to the potential of our mRNA platform. We are excited to work with Sanofi in this broadened capacity with the goal of ultimately delivering vaccines on a global scale, a need underscored by the current pandemic…Translate Bio will also be well positioned financially to continue to build upon our internal capabilities with a focus on advancing innovations in platform discovery and on the development of ongoing and additional preclinical therapeutic programs as we aim to bring multiple programs towards clinical development.”

Under the collaboration agreement terms, Translate Bio is employing its mRNA platform to create and manufacture vaccine candidates and Sanofi Pasteur is providing vaccine expertise to accelerated and advance vaccine candidates through development.

The teams are already working together on several COVID-19 vaccine candidates in vivo for immunogenicity and neutralizing antibody activity to support lead candidate selection and the companies hope to initiate a first-in-human clinical trial in Q4/20.

The Sanofi Pasteur and Translate Bio collaboration was initially formed in 2018, whereby Translate Bio entered into an exclusive license agreement with Sanofi Pasteur to develop mRNA vaccines for up to five infectious disease pathogens. The agreement was later expanded to include the collaborative development of a novel mRNA vaccine for COVID-19 in March 2020.

Sanofi, based in Paris, is a $131.0 billion market cap global biopharmaceutical company involved in research, development, manufacture and marketing of therapeutic solutions. The firm employs more than 100,000 people in 100 countries.

Translate Bio is a clinical-stage mRNA therapeutics company headquartered in Lexington, Mass. The firm concentrates its efforts on developing a new class of potentially transformative medicines to treat diseases caused by protein or gene dysfunction. Translate Bio is mostly focused utilizing it technology to treat pulmonary diseases caused by insufficient protein production or where the reduction of proteins can modify disease.

Translate Bio began the day with a market capitalization of around $1.0 billion with approximately 62.91 million shares outstanding and a short interest of about 2.9%. TBIO shares opened 52% higher today at $24.69 (+$8.45, +52.03%) over yesterday’s $16.24 closing price and reached a new 52-week high price this morning of $27.24. The stock has traded today between $21.56 and $27.24 per share and is currently trading at $23.60 (+$7.36, +45.32%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

The COVID-19 pandemic has disrupted the U.S. recycling industry. Waste sources, quantities and destinations are all in flux, and shutdowns have devastated an industry that was already struggling.

Many items designated as reusable, communal or secondhand have been temporarily barred to minimize person-to-person exposure. This is producing higher volumes of waste.

Grocers, whether by state decree or on their own, have brought back single-use plastic bags. Even IKEA has suspended use of its signature yellow reusable in-store bags. Plastic industry lobbyists have also pushed to eliminate plastic bag bans altogether, claiming that reusable bags pose a public health risk.

As researchers interested in industrial ecology and new schemes for polymer recycling, we are concerned about challenges facing the recycling sector and growing distrust of communal and secondhand goods. The trends we see in the making and consuming of single-use goods, particularly plastic, could have lasting negative effects on the circular economy.

Goodwill’s Canton, Mich. site looks overwhelmed on June 16, 2020, with an oversupply of donations and little immediate chance for resale. Brian Love, CC BY-ND

Recyclers under pressure

Since March 2020, when most shelter-in-place orders began, sanitation workers have noted massive increases in municipal garbage and recyclables. For example, in cities like Chicago, workers have seen up to 50% more waste.

According to the Solid Waste Association of North America, U.S. cities saw a 20% average increase in municipal solid waste and recycling collection from March into April 2020. Increased trash can be attributed partly to spring cleaning, but most of it is due to people spending greater time at home. Restaurants struggling to survive under COVID-19 restrictions are contributing to the rise in plastic and paper waste with takeout packaging.

Although higher volumes of recyclables are being set on the curb, budget deficits are squeezing recycling programs. Many municipalities are struggling with multimillion-dollar shortfalls. Some communities, such as Rock Springs, Wyoming, and East Peoria, Illinois, have cut recycling programs.

And these stresses are testing a business already faced uncertainty.

While bottle deposit stations remain closed, recyclables pile up in basements and garages. David Rieland, CC BY-ND

Turmoil in scrap markets

The global recycling economy has suffered since 2018 as first China and then other Asian nations banned imports of low-quality scrap – often meaning improperly cleaned food packaging and poorly sorted recyclable materials. As in any business, the value of raw recyclables is linked to supply and demand. Without demand from nations like China, which formerly took up to 700,000 tons of U.S. scrap annually, recyclers have scrambled to stay in business.

The pandemic has boosted prices for some materials. One industry leader told us that between February and May 2020, prices doubled for recycled paper and tripled for recycled cardboard. These shifts reflect higher demand for tissue products and shipping packaging under shelter-in-place orders.

However, he also reported that prices for the most-recycled categories of reclaimed plastics – PET (#1) and PE (#2 and #4) – were at 10-year lows. An influx of cheap oil has driven the raw material cost of oil-derived virgin plastics to their lowest levels in decades, outcompeting recycled feedstocks.

Difficult economics

Ideally, revenues from recycling offset municipalities’ costs for collecting and disposing of solid wastes. However, given worker safety concerns, low market prices for scrap materials, a slowed economy and cheaper alternatives for disposal, many communities and businesses across the U.S. have temporarily suspended collection of recyclables and bottle deposits.

Meanwhile, as the commercial sector slowed, the distribution of waste generation changed. As people have spent more time producing waste at home, waste collectors implemented new procedures to protect their employees from infection.

Recycling is a very hands-on process that requires workers to manually sort out items from the collection stream that are unsuitable for mechanical processing. Workers and waste collection companies have raised many safety questions about recycling during the pandemic.

Precautions like social distancing and use of personal protective equipment have become commonplace among waste collectors and sorters, though concerns remain. Sorters are increasingly relying on automation, but implementation can be costly and takes time.

Collections on pause

Based on monitoring since 2017 by the trade publication Waste Dive, nearly 90 curbside recycling programs had experienced or continue to experience a prolonged suspension over the past several years. About 30 of these suspensions have occurred since January 2020.

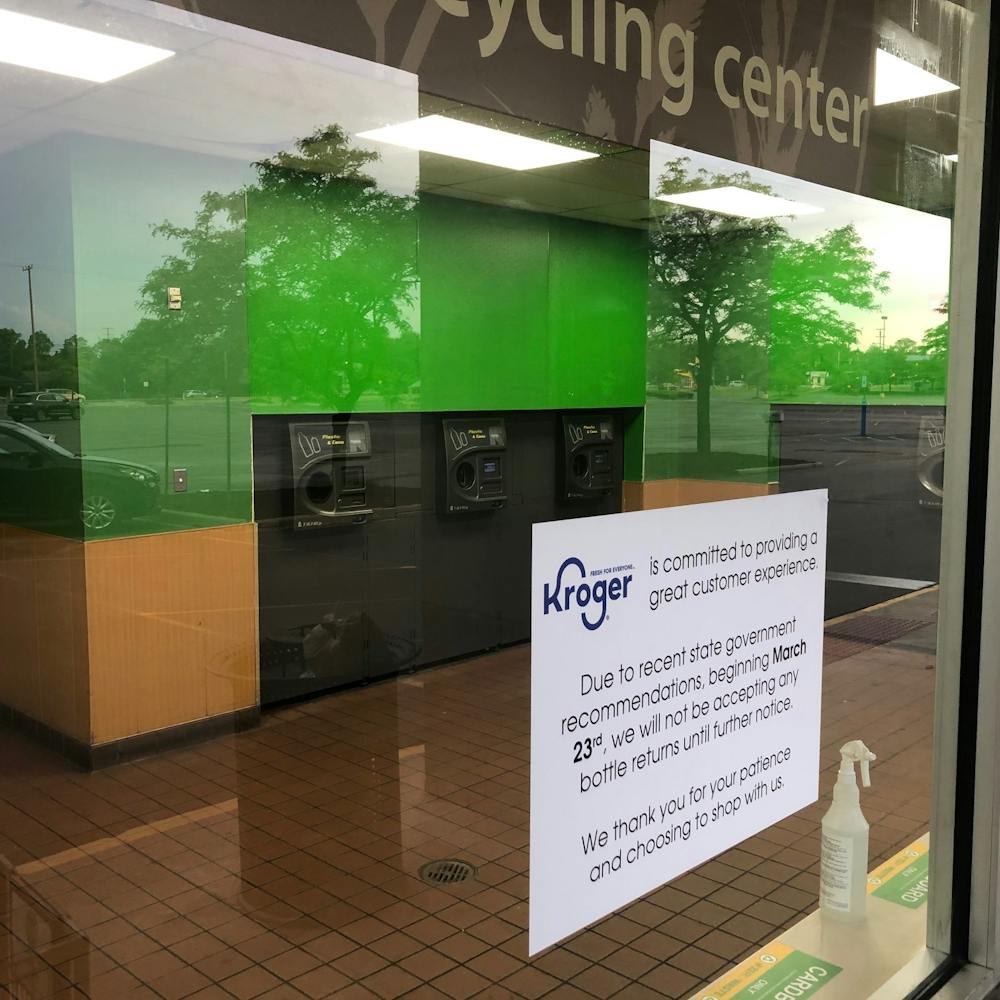

Like many bottle deposit programs, Kroger’s Ann Arbor, Mich. drop-off center shut down on March 23. Michigan bottle deposits across the state resumed on June 15, 2020 with new safety protocols. Brian Love, CC BY-ND

On a broader scale, it’s not clear how much more waste Americans are currently producing during shutdowns. Commercial and residential waste aren’t directly comparable. For example, a granola bar wrapper thrown away at the office is tallied differently than if discarded at home.

It is also challenging to quantify the effects of the pandemic while it is still unfolding. Historically, waste output from the commercial and industrial sectors has far outweighed the municipal stream. With many offices and business closed or operating at low levels, total U.S. waste production could actually be at a record low during this time. However, data on commercial and industrial wastes are not readily available.

At the California-based Peninsula Sanitary Service, which serves the Stanford University community, total tonnage was down 60% in March. The company attributes this drop to reduced commercial waste, particularly from construction. Similarly, the city of Vancouver, British Columbia, noted a 10% decrease year over year of waste collection levels for April.

Expected sectors of plastic waste increase due to COVID-19, based on 2018 plastic usage distribution data from PlasticsEurope and Klemes et al., 2020. Brian Love and Julie Rieland, CC BY-ND

More plastic trash

As cities and industries reopen in the coming months, new data will show the pandemic’s effects on consumer habits and waste generation. But regardless of total volume, the mix of materials in household wastes has shifted given the new ubiquity of single-use plastic containers, online shopping packaging and disposable gloves, wipes and face masks. Many of these new staples of pandemic life are made from plastics that are simply not worth recycling if there are any other disposal options.

Today Americans are trying to balance their physical well-being against ever-mounting piles of plastic waste. At a time when reducing and reusing could be dangerous, and recycling economics are unfavorable, we see a need for better options, such as more compostable packaging that is both safer and more sustainable.

Georgia’s central bank lowered its benchmark policy rate for the second time this year as it continues to gradually exit from a tight monetary policy stance as the significant weakening of external and domestic demand is leading to a lower inflation forecast. The National Bank of Georgia (NBG) cut its refinancing rate by another 25 basis points to 8.25 percent and has now cut it 75 points this year following a 50-point cut in April. Despite today’s rate cut, NBG said its monetary policy remains tight to ensure inflation returns to its target, adding “the pace of further policy normalization will depend on how quick inflation expectations recede.” The central bank began tightening its policy stance in September last year to curb inflation from a decline in the lari’s exchange rate, hiking its rate four times by a total of 200 basis points. These rate hikes helped the lari rebound but on March 19, the day after it kept its rate steady amid a massive spree of rate cuts worldwide in response to the hit to economic activity from measures to contain the Covid-19 pandemic, the lari plunged. By March 27 the lari had lost some 21 percent of its value, forcing the central bank to intervene in the foreign exchange market. NBG has intervened 6 times in the market totaling $180 million. This intervention helped calm the market and on April 8 NBG announced a series of emergency measures in response to the pandemic, including the provision of $400 million through swaps to commercial banks and microfinance institutions, allowing banks to use foreign currency buffers to manage lari liquidity and an easing of banks’ capital requirements. Today the lari was trading at 3.05 to the U.S. dollar, up almost 15 percent since the low of 3.50 on March 27 but still down 6.2 percent since the start of this year. Georgia’s inflation rate eased to 6.5 percent in May from 6.9 percent in April, but is still above NGB’s target of 3.0 percent. The central bank confirmed its view from April that it expects inflation to gradually decline over the rest of this year and reach its target level in the first half of 2021 as the impact of higher costs of some goods and services in connection with measures to prevent the spread of Covid-19 only affects inflation in the short term. The impact of weaker external and domestic demand, however, will have a longer lasting impact on inflation though it cautioned that above-target inflation has the risk of stoking inflation expectations. “Taking these factors into account, the Monetary Policy Committee deemed it appropriate to continue the gradual exit from the tightened monetary policy stance and reduced the rate by 0.25 percentage points,” NBG said. Preliminary data show mixed signals regarding the expected drop in demand, the central bank said, adding significant fiscal stimulus is also expected to boost demand. Current estimates show a 16.6 percent year-on-year fall in economic activity in April while payment card transactions in May rose 21 percent from the previous month, though it was still negative in annual term. And high growth of cash in circulation points to increased economic activity and there has been an improvement in credit activity in the wake of a gradual lifting of restrictions.

On May 1 the International Monetary Fund’s executive board raised Georgia’s access to its extended fund facility (EFF) to 230 percent of its quota, releasing some US$200 million to help the country meet urgent balance of payments and fiscal needs, including higher spending on health. This brought the IMF’s total disbursements under the 3-year EFF to some US$448 million.

“The COVID-19 pandemic has hit the Georgian economy hard,” IMF said, noting a fall in external demand and tourism has widened the current account and fiscal deficits, depreciated the exchange rate and led to a substantial decline in economic activity.

The IMF also supported NBG’s “moderately tight monetary policy,” while allowing the exchange rate to remain flexible, adding monetary policy decisions should be based on monitoring inflation expectations.

The IMF forecast Georgia’s economy would contract 4.0 percent this year, down from 5.1 percent growth last year, and then expand 4.0 percent in 2021.

Inflation is seen averaging 4.7 percent this year, slightly up from 4.5 percent in 2019, and then easing to 3.9 percent in 2021.

Measured in lari, Georgia’s current account deficit is seen widening to 11.3 percent of GDP, up from a 4.9 percent in 2019, and then narrowing to 7.5 percent in 2021. In U.S. dollar terms, the deficit this year is seen widening to 1.7 percent of GDP and then 1.3 percent in 2021.

The National Bank of Georgia issued the following statement:

“The Monetary Policy Committee (MPC) of the National Bank of Georgia (NBG) met on June 24, 2020, and decided to cut the refinancing rate by 0.25 percentage points to 8.25 percent.

In May, annual inflation stood at 6.5 percent. According to the NBG forecasts, inflation will continue to gradually decline over the rest of the year and will reach the target level in the first half of 2021. The inflation dynamics will be determined by the interaction of both demand and supply side factors. On the one hand, the Covid-19 prevention measures led to an increase in the cost of supply of some goods and services. However, the increase in costs has only a short-term effect on inflation rate. On the other hand, the impact of significantly weaker external and domestic demand on inflation will last longer, leading to a reduction in inflation forecasts. At the same time, it should be noted that above target inflation in a long-term creates the risks of rising inflation expectations. Taking these factors into account, the Monetary Policy Committee deemed it appropriate to contiსnue the gradual exit from the tightened monetary policy stance and reduced the rate by 0.25 percentage points. Despite the decline, monetary policy remains tight, ensuring a return of inflation to its target level in the medium term. The pace of further policy normalization will depend on how quickly inflation expectations recede.

Preliminary indicators produce mixed signals regarding the expected reduction in aggregate demand. According to current estimates, economic activity in April fell by 16.6 percent annually. At the same time, in May, compared to the previous month, the volume of transactions with payment cards increased by 21 percent, although the annual growth rate is still negative. On the other hand, high annual growth of cash in circulation points to increased economic activity. At the same time, in the wake of the gradual lifting of restrictions, some improvement in credit activity has been observed. All these factors reveal that there is quite some uncertainty about the scale of the expected decline in aggregate demand. In addition, over the year the aggregate demand is expected to be positively impacted by significant fiscal stimulus, including planned partial subsidies on interest charges for mortgage loans. The latter is, in fact, equivalent to additional easing of monetary policy stance.

According to forecasts, as a result of the economic downturn in trading partner countries, external demand will remain significantly weakened throughout the year. According to preliminary data, exports of goods in May declined by 31 percent annually, while the tourism revenues fell by 97 percent. Along with the decline in revenues from exports, imports in May also fell by 34 percent year on year.

The NBG will continue to monitor the developments in the economy and financial markets and will use all instruments at its disposal in order to ensure the price stability.

The next meeting of the Monetary Policy Committee is scheduled on August 5, 2020.”

Tomorrow we get the final chance to adjust the measurement of the US Q1 GDP.

The broad consensus is that it will simply repeat the second reading, to confirm a -5.0% contraction. However, given the logistics issues around COVID, there is a higher chance than usual for a change this time around.

The markets have already priced in a recession, and are looking towards reopening.

A further adjustment to the downside (it’s very, very unlikely to be adjusted back up), might just be the catalyst needed to push markets down.

While risk sentiment has been improving, recent trends show that the bulls are quite fickle and unsure.

What Now?

We’re coming to the close of the second quarter, which is less than a week away.

If the first was bad, the second is broadly expected to be much worse, since that’s when the bulk of the shutdowns happened. Starting next Wednesday, we get the first measures of the quarter. And this is likely to set the tone for markets.

With the recent rebound in equities sputtering out, fear of a W-shaped recovery is starting to return.

After taking a hiatus in early June, COVID is once again the most common subject in the media.

Regardless of the political implications and explanations, the relatively slight uptick in cases compared to the large increase in coverage has made investors a little more nervous.

And China?

There’s something else to keep traders up at night.

As the COVID situation at least stabilizes, geopolitics has come back on the radar. Many strategists are pointing to recent activity in China as a potential sign that the Asian giant is seeing an opportunity with the US distracted by internal issues, to push their interests.

Taiwan has repeatedly warned off Chinese fighter planes, recently, in a noticeable increase in tensions. And then there was the border clash between China and India.

What worries the markets the most, however, is best illustrated by what happened on Monday night.

US Trade Rep Peter Navarro replied to a reporter’s question in a way that allowed the journalist to report that the official said that the US-China trade deal was over. This sent markets reeling until President Trump had to come out to clarify that the trade deal was still on.

With Washington and Beijing escalating the war of words, it shows how sensitive markets are to potential negative news. This underscores the fragility of the recovery so far.

We Need Concrete Data

Preliminary reports for June in the form of PMIs have been positive. However, they are just the first month of recovery. It’s still a full month before we get the first reading of US Q2 GDP reading.

And by then we will be in the middle of earnings season.

On a positive note, many companies are seeing the situation stabilized enough to start issuing guidance. Over the next couple of weeks, we can expect major firms to give their expectations for the development of the economy over the rest of the year.

That might be the defining element for whether we are going to see a V or a W in the recovery path.