The Philippine central bank cut its key interest rate for the fourth time this year and for the seventh time in just over a year, saying “a further reduction in the policy rate amidst a benign inflation environment would help mitigate the downside risks to growth and boost market confidence.” Bangko Sentral Ng Pilipinas (BSP) cut the rate on its overnight reverse repurchase facility (RRP) by a further 50 basis points to 2.25 percent and has now cut it 175 points this year following cuts in February, March and April. BSP has been lowering its interest rates since May 2019 and has now cut them by 250 basis points since then. The Philippine peso has been on a rising trend since October 2018, with the seven rate cuts only slowing the general upward trend slightly. Today the peso was trading at 50.0 to the U.S. dollar, up 1.5 percent since the start of this year and 8.6 percent higher than a low of 54.3 in early October 2018.

In addition to the cut in RRP, the bank’s monetary board cut the rate on the overnight deposit facility to 1.75 percent and the rate on the overnight lending facility to 2.75 percent.

Inflation in the Philippines fell to 2.1 percent in May, the fourth consecutive month of deceleration, and BSP said the latests forecast show inflation could settle near the low end of its inflation target of 3.0 percent, plus/minus 1 percentage point in 2020 and up to 2022.

The decline in inflation had fueled expectation by some analysts that BSP would cut its rate today.

Although economies around the world are beginning to reopen from measures to prevent the spread of Covid-19 and the functioning of financial markets has improved, BSP said the global recovery is likely to be “protected and uneven” and domestic economic activity has slowed.

“Hence, there remains a critical need for continuing measures to bolster economic activity and support financial conditions,” BSP said, pointing to measures to protect human health, boost agricultural productive and build infrastructure. BSP said it remains committed to “deploying its full range of monetary instruments and regulatory relief measures as needed” to meet its mandate of promoting non-inflationary and sustainable economic growth.

Bangko Sentral Ng Pilipinas issued the following statement:

“At its meeting on monetary policy today, the Monetary Board decided to cut the interest rate on the BSP’s overnight reverse repurchase (RRP) facility by 50 basis points (bps) to 2.25 percent, effective Friday, 26 June 2020. The interest rates on the overnight deposit and lending facilities were reduced to 1.75 percent and 2.75 percent, respectively.

Latest baseline forecasts indicate that inflation could settle near the low end of the target range of 3.0 percent ± 1 percentage point inflation for 2020 up to 2022, with inflation expectations remaining firmly anchored over the policy horizon. Meanwhile, the balance of risks to the inflation outlook leans toward the downside from 2020 up to 2022 owing largely to the potential impact of a deeper and more disruptive pandemic on domestic and global demand conditions.

The Monetary Board observed that domestic economic activity has slowed with the enforcement of necessary protocols to slow the spread of the virus in the country. At the same time, the outlook for global growth has deteriorated further as considerable uncertainty still surrounds the extent of the health crisis. The Monetary Board noted that even as economies begin to reopen, the global recovery would likely be protracted and uneven. Hence, there remains a critical need for continuing measures to bolster economic activity and support financial conditions, especially the effective implementation of interventions to protect human health, boost agricultural productivity and build infrastructure.

Given these considerations, the Monetary Board decided that a further reduction in the policy rate amidst a benign inflation environment would help mitigate the downside risks to growth and boost market confidence. Even as domestic liquidity dynamics and market function continue to improve owing to prior liquidity-enhancing measures, the Monetary Board believes that keeping an accommodative stance will further ease the cost of borrowing and ensure ample credit and liquidity in the financial system as the economy transitions toward recovery in the coming months.

Going forward, the BSP reiterates its support for the health and fiscal programs already being rolled out by the National Government in responding to the needs of Filipino households and businesses. The BSP remains committed to deploying its full range of monetary instruments and regulatory relief measures as needed in fulfillment of its mandate to promote non-inflationary and sustainable growth.”

Market sentiment is mixed today with US stocks opening lower, but so far being well supported by the widely watched 200-day moving average. European markets are more positive while the greenback is making gains, after a smorgasbord of US domestic data showed a steady, if depressed jobs market and bumper durable goods figures which keep the dreams of a v-shaped recovery alive.

Markets continue to fret over the risks of an unchecked rise in Covid cases and yesterday’s threat of US tariffs on EU goods puts US protectionism back on the table leading into the November elections.

Price action may be swayed by month and quarter end rebalancing flows, and what a quarter it has been! Records of every type have been regularly broken in the financial markets with two-way markets expected to reign going forward as traders wait for the next defining catalyst.

The saga of German fintech Wirecard might be a worthy metaphor for the current market volatility as the company filed for insolvency today sending the stock crashing over 70%.

EUR/USD still contained in its range

Today’s ECB Minutes told us that President Lagarde is ready to do more heavy policy lifting if it is needed, and low growth and disinflationary pressure were the main drivers of the June decision to ramp up the size of the PEPP.

EUR/USD support around the 1.12 level is proving solid for the single currency bulls. Short-term resistance lies above at 1.1270 followed by 1.13. Playing the range seems sensible in the 1.12-1.14 trading band as price action is fairly contained at present.

GBP following the dollar mood

There’s been no major domestic news in today’s session, so traders are following the wider risk environment. Eyes will be on the resumption of trade talks with the EU next week.

Having been stuck between its 50-day and 100-day moving average for the past session, cable is now trading below the former at 1.2420. Solid support remains in the 1.2330 area with resistance above at 1.2530/40.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Chris Temple of The National Investor delves into what sets Omineca Mining and Metals apart.

I had been familiar with the story and potential of uber micro-cap (a valuation of little more than C$3 million or so for a LONG time!) Omineca Mining and Metals Ltd.’s (OMM:TSX.V; OMMSF:OTCMKTS) for years. But as gold was beginning to percolate and other necessary ingredients came together as last year got underway it was time for me to bring this incredible opportunity to my members.

“Back in late February/early March when gold stocks got annihilated for a while along with the broader market, Omineca didn’t flinch. The share price has fairly methodically “stair-stepped” higher for a while now.”

I and others that are in the business of researching and recommending “story” companiesespecially in the resource spacecontinuously stress the CRITICAL element of management. Many a promising company and project has been destroyed by bad management; whether that is of greedy execs milking an emerging company dry via high salaries, simply not having the right talent for the specific jobs at hand or whatever.

Over the years, few managements have served our Members better than have those led or initiated by the MacNeill family of Saskatoon, Saskatchewan. “Dad” Bill is one of the most accomplished resource investors in the province, most notably, for our purposes, as the founder and long-time chairman of the former Claude Resources, which was bought out in 2016 by SSR Mining (Nasdaq-SSRM). And as some of you know, SSRM has since demonstrated what Bill and many of us long believed: this little gold mine he founded is the anchor of one of Canada’s emerging new districts.

A trip down Memory Lane; the 1997 construction of the head frame at Claude’s Seabee Mine. The MacNeill clan L to R: Tom, Ken, Dad Bill, Mom Sharon and Jon.

One son, Ken, is the president and CEO of Star Diamond Corporation. As I have said in years past upon my recommendation initially of the former Shore Gold and subsequently, I have seldom met a more frank, honest and understated chief executive of a company; notableamong other reasonsespecially given that the company owns the largest diamond-bearing kimberlites in the world. These days, Rio Tinto has joined Star as an advanced exploration and potential development partner.

Our longest-tenured members remember Star as one of THE most rewarding picks I’ve ever passed on; one of my Top Ten most profitable individual stocks ever. Getting into both Shore/Star and former fellow SK diamond explorer Kensington Resources (which Shore later absorbed) not too far from the C10 cents/share area, most of my recommended selling came in the neighborhood later of C$5.00/share. Those awesome gains were realized when the company’s kimberlite bodies in Saskatchewan’s Fort a la Corne provincial forest likewise vindicated what the MacNeills had believed: that much better, larger and higher-grade diamonds existed there than what had been seen in scant prior exploration.

Years later the family re-gathers (save for Tom who couldn’t make it, but was replaced by geologist daughter Laura) on the occasion of the one millionth ounce of gold poured at Seabee.

And as I first expressed back last March when I added Omineca to my recommended list, signs have been increasing here as well (not the least of which has been evidenced by that enviable stock price chart on the first page!) that it is now THIS MacNeill-run company’s turn to shine!

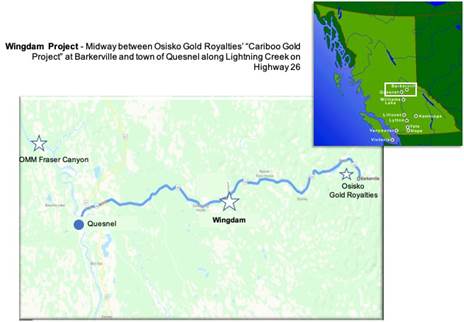

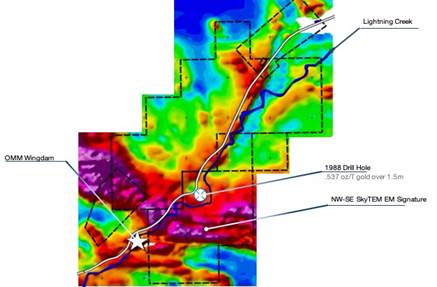

Omineca’s Wingdam Project

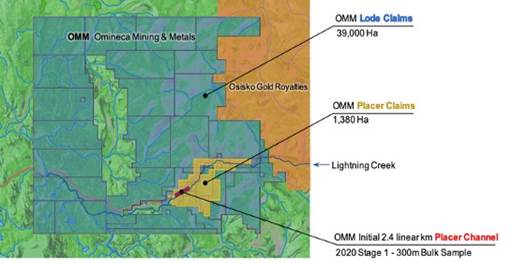

As you’ll see on Omineca’s websiteits chief asset is the Wingdam Gold Project, about 45 km east of Quesnel, British Columbia. Past exploration and sampling work there suggests that the area of a unique alluvial gold-bearing deposit OMM controls here has the richest gold grades of anything known of in the entire Cariboo District.

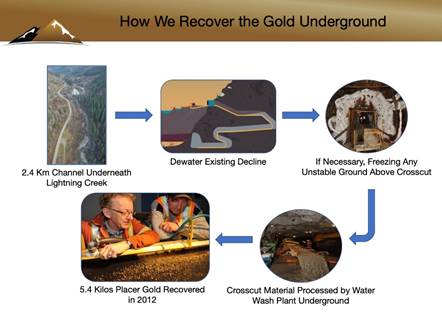

The material in question is what’s called an “unconsolidated conglomerate” about 50 meters below the present-day surface of Lightning Creek. Think of a typical stream channel that was at one point buried by gravel and glacial till. That there is such an apparent high grade of gold in this underground paleo channel is because it is so “hidden”; the prospectors who flocked to this area of British Columbia around 1860 after gold was discovered in the surface streams of Lightning and Williams Creeks in the Cariboo recovered what they could see. Obviously, they could not see the older buried stream below the one they were panning gold in!

Of course, recovering this gold is challenging due to the “loose” nature of the material and the 50 meters or so of gravel, etc. on top of it. But back in 2012, management demonstrated that gold could be recovered from this underground paleo channel by freeze mining: freezing solid the area surrounding gold-bearing gravels so as to make it safe to take one “slice” at a time from the underground channel. Indeed, it was “sister” company 49 North Resources, Inc. (TSXV-FNR; OTC-FNINF) that was an original funder, bringing to Saskatchewan this kind of freezing technology.

Under the leadership of Len Sinclair and OMM’s lead geologist Steve Kocsis (left/right, respectively, in the nearby photo, examining some of the gold recovered) Wingdam (then a private company before being brought under the ownership of Omineca) successfully recovered 5.4 kilos of placer gold in one narrow “crosscut” underneath about 40 meters, in that location, of wet overburden underneath Lightning Creek. Sinclair is still part of the project, serving on Omineca’s Advisory Board. Kocsis”Mr. Cariboo” as C.E.O. MacNeill calls him due to his vast experience in the areais heading up exploration.

Two things were demonstrated in that successful recovery. The first was that this kind of freeze mining (still used to this day to mine potash and phosphates from underground mines in the province) could work to cover buried alluvial gold as well. So while a tedious prereparation process is required, this can be done!

Secondand more excitingis that the gold recovered in 2012 was double what management had expected to see in this one cross-cut. This further bolsters the company’s own estimate and that of geologists and engineers that have been involved that there could be in the neighborhood of 200,000-250,000 ounces of gold within the 2.4 kilometer-long focus area under Lightning Creek.

Yet management decided for a couple reasons to “sit” on Wingdam for a while. First of all, as you likely remember, this was the point at which the torrid gold run of late 2008-2011 was reversing. So with a falling gold price, financing the work and/or finding a partner here was not an attractive option. That was made more of a challenge by the fact that there is not an NI 43-101-compliant resource estimate at Wingdam. And as C.E.O. Tom MacNeill has pointed out to me over time in our conversations, the C$10 million-plus that would have to be spent to confirm a resource to that standard would largely be wasted money, since the company was confident of what it has.

The process to, at last, exploit the potential at Wingdam restarted in earnest last March 1, when Omineca announced that it had contracted with HCC Mining and Demolition, Inc. of Saskatoon, Saskatchewan to be its partner at Wingdam. A 125 year-old company that Omineca knows well, HCC is supplying all the equipment and up-front capital necessary to, initially, start a “bulk sampling” program in the paleo channel. Omineca gets half of the gold recovered at a cost to OMM of C$850.00 per ounce. The Canadian currency price of gold as of this writing is around C$2,350.00/ounce.

Compared to most any other kind of gold recovery (and with this alluvial deposit, it can’t be more simple as virtually all is so-called “free” gold) the process of recovering gold in the first bulk sample contemplated in the agreement will be relatively easy and likely won’t take terribly long. Having already successfully “plugged” an upstream source of waterand preparing the paleo channel as we speakit seems as though the first freezing and cross-cuts will be taking place this summer. Barring any surprises, the companies believe they can fully bulk sample an initial 1.5 kilometer area (working out from the middle of the 2.4 kilometer target) in the next 1824 months.

Keeping in mind that 1. There is NOT an NI 43-101-compliant “resource” and 2. There is no guarantee of anything (which is why Omineca is necessarily characterized a speculative stock) let’s “speculate” and say that the companies ultimately recover but 10% of the gold believed to be in the paleo channel. That to OMM would mean its share would be between 10,000 and 12,500 ounces. I’ll use the smaller number.

At a net to Omineca of C$1,500/ounce, that would mean cash to the company of C$15 million, or HALF its current market cap even after the strong move of recent months. If the companies’ prior estimates are realized, that’s C$150 million in cash for Omineca; FIVE TIMES ITS MARKET CAP.

Take your pick. But on this potential cash flow alone, I and others who listened to me were sufficiently excited in the recent past to participate in two private placements the company offered to fund an even more staggering potential. In the end, this could be even more of a blockbuster story than I first thought; and why I have on a few recent occasions suggested that one day Omineca Mining and Metals could supplant biotech Sarepta Therapeutics (NASD-SRPT) as my MOST profitable recommendation ever.

NOW WE’LL MAKE THINGS REALLY INTERESTING!

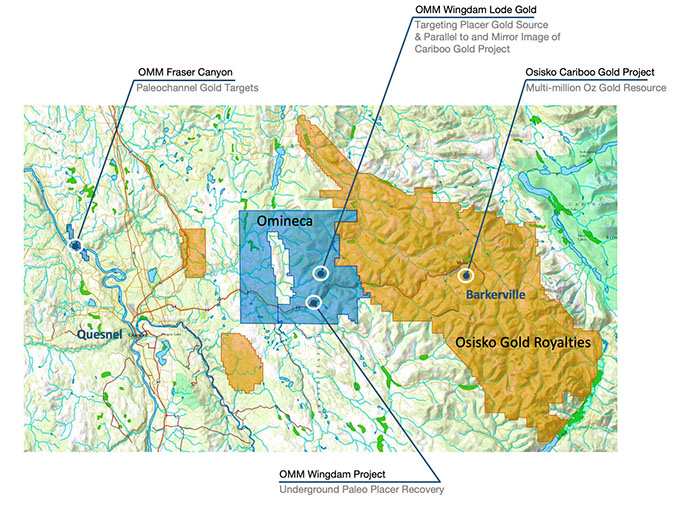

As the attention of a few people was beginning to turn to Omineca’s story last year, the potential of the broader Cariboo area got a much higher-profile shot in the arm. In late September, Osisko Gold Royalties (NYSE-OR) announced that it was paying a 44% premium for Barkerville Gold Mines whichas you see in the below graphicis essentially Omineca’s “next-door neighbor.” The acquisitive-minded Osisko was animated not only by Barkerville’s existing high-grade gold resource, but believe there’s more where that came from.

Omineca has long had its eye on the area surrounding what it already held at Wingdam, believing there to be numerous attractive explorationand ultimately drillingtargets for hard rock or “lode” gold around the paleo channel area. But when the company announced back on January 17 that it had increased its claims 13-fold in and around the ground it already held, a powerful story already became a potentially explosive one.

It needs to be understood that there is no place in the province of British Columbia that has ever produced higher gold grades than the Cariboo (for some very interesting history, check out Cariboo Gold Rush for some of the back story; indeed, B.C. became a province on the strength of the first Cariboo Gold Rush back when!)

It’s one thing to understand the hidden nature of the underground gold in the buried paleo channel at Wingdam. But it’s thepotential “lode” (hard rock) gold nearby Wingdam that may be about to take on new meaning for Omineca as well.

Back around the time of the first announcement (January 17, which you can read with other recent a news) that Omineca had considerably increased its own foot print to, now, being the second-largest land holder in the Cariboo behind Osisko) I had a particularly fascinating conversation with Tom. In fact, it stretched into parts of two days, and was incredibly detailed to me by a man who is characteristically VERY understated as are his father and brother Ken, but who was now bubbling over with excitement.

Among other things, Omineca had come into possession of additional historical information on Wingdam and the surrounding area; specifically for our present discussion purposes here, SKYTem geophysical data from a different company back in 2012 that had flown over the Wingdam area. Over a few days’ time, I went through the nearly 200-page wrap-up of that survey.

MacNeill and his brain trust began connecting some dots once they started to study this information. Previously, on the past small bulk sample at Wingdam, he had remarked, “One of the striking things that came out is the nature of the gold.” Without getting into technical details/definitions, it was clear by the coarse and “nuggety” nature of the gold recoveredand the relative lack of “fine” goldthat what was recovered so far at Wingdam did not travel very far at all.

Often timesin most any setting where there is placer golda search will ensue for the possible lode, or hard rock, source. Again, in simple terms, a combination of factors initially led to such gold being liberated from someplace and settling in one or more downstream places. That’s where gold ever found in streams came from, by and large. And MacNeill has always suspected that the gold they have seen thus far could well have come from a nearby source, given its appearance. Indeedas he also mentioned to me during one of our past discussionseven during that prior 2012 bulk sample, as the underground recovery finished gathering the unconsolidated/buried placer materialnoticeable in the wall was visible gold within quartz veining.

As other dataincluding that 2012 surveyhave been compiled, one astonishing possibility that has been revealed is that even that underground gold-bearing paleo channel about to be bulk sampled may be sitting right on top of or VERY near a heavily mineralized lode deposit.

Nearby, you see one graphic from that 2012 survey which is a “magnetic” look of the Wingdam area proper. The highly magnetic (purplish) signature is from a depth of 99 to 115 meters below surface.

Two things were immediately evident, even to me. First, the purplish coloration from, roughly, more West-to-East near the bottom of the graphic is hot. Typically, metals, etc. associated with gold will give off such a magnetic signal; this is always what you look for in doing airborne or other magnetic surveys.

Second, this area is not only fairly well-defined/constrained but cross-cuts the paleo channel and modern-day river bed above. Further, it is a bit upstream from the Wingdam camp area (which is specifically the thin white area in the bottom left portion of the nearby graphic, marked with a star.)

The hypothesis, in part, is that 1. Past activity could have ripped apart some of the “wall” in that purple/surrounding area and deposited some gold in the paleo channel area at Wingdam and 2. Almost all of that past wall appears still intact and heavily mineralized. So the second major priority for 2020and a potentially HUGE second catalyst for the company’s story and its stockwill be for Omineca to start drilling these and other nearby hard rock targets for gold.

Getting to Work!

On June 10, Omineca announced that it had closed an oversubscribed private placement and had commenced field work at Wingdam. Stephen Kocsis, P. Geo, has been appointed the lead geologist for the Wingdam hard rock exploration project. Based in nearby Quesnel, B.C., Kocsis has spent his career exploring for gold and other mineral deposits in the Cariboo Mining District and has authored numerous papers and technical reports covering the project area, including on Wingdam itself.

With snow cover now receded, management, Stephen and the geological team from Axiom Exploration Group have been to the site and surveyed the initial locations of interest identified by geophysics to coordinate plans and procedures for the 2020 exploration and drilling program. As you can read in the above-cited news release, ultimately the plan is to drill some 8,000 meters of core in 27 specific targets within about a three-kilometer “sphere” of the underground paleo channel area, once the work to narrow the specific targets is done and permits are in hand.

Separately, I expect before much longer to see an update on the underground bulk sample program work’s progress as well.

Summing Things Up

Those of you particularly who have more experience than the average investor in gold exploration know that the majority of smaller exploration companies do NOT make it for one reason or another. They are inherently speculative; but can carry very high rewards if things work out, to go along with the risk.

As I have shared Omineca’s story with, first, my members at The National Investor as well as colleagues, it’s exhibited itself as one that is truly unique. With not one but two major projects for a small company such as it isthe underground bulk sample-gold recovery via its partner HCC and now the aggressive hard rock exploration in its own rightOmineca’s potential is mind-boggling if even just one of these gambits is a success. If both are, this company could be one of those once-in-a-generation wealth builders for those who get in before the (hoped-for) fireworks start.

I need to quickly discuss the chart from the beginning of this article again. Among the important points I really need to drive home here is that back in late February/early March when gold stocks got annihilated for a while along with the broader marketOmineca didn’t flinch. The share price has fairly methodically “stair-stepped” higher for a while now.

About 75% of Omineca is owned by management and insiders (the lion’s share of that by 49 North.) None of them are going to take a five-bagger of recent months and cash in anything with such potential lying ahead. Likewise, those of us who have been getting into Omineca for the last year or so now understand the huge potential here, and I, for one, want to be along for ALL of this ride!

I urge you to do your own “homework” on Omineca, and quickly. Among other things, take the time to check out Omineca’s just-updated Corporate Presentation.

For more information, a good “primer” of sorts for you would be CEO Tom MacNeill’s presentation at the Metals Investor Forum in Vancouver earlier this year; it can be seen here.

Finally, here’s a lengthy interview as well with Tom given to our mutual friend Peter Bell (on the far left in the photo above, visiting with Tom at the M.I.F.).

Wrapping it all up from the end of that interview to bring my own interest in and excitement about Omineca back home, heres that interviews close, after kudos to analyst David Morgan for highlighting Omineca at that Forum:

Peter Bell: And a shout-out to Chris Temple, as well. Another voice in the wilderness there.

Tom MacNeill: He was the first person to talk about us in print. And that’s because, Chris, very much like you Peter, is early onto stories. He was up in Saskatchewan back in the 1980s when my father was originally developing the Seabee project in Saskatchewan. Like you, he gets there early because he’s a deep thinker and he knows exactly where to look for wins. One of the things I think he understands is to bet on the jockey, not the horse.

Don’t forget that those of you so inclined can follow my thoughts, focus and all daily.

HOW TO PURCHASE SHARES OF OMINECA MINING IF YOU ARE A U.S. INVESTOR USING A U.S.-BASED BROKERAGE ACCOUNT

For those of you who are not already used to buying shares of companies such as Omineca that are listed primarily in Canada, I want to give you a quick and easy “tutorial.” It’s MUCH easier than you think, if you have never done so, to buy such companies in any U.S. brokerage account. Indeed, as I have explained in one of my investor tutorials, it’s just as easy and inexpensive to buy shares in an Omineca as it is to buy Apple!

Many larger Canadian and other foreign companies have primary listings on more than one major exchange. For those listed on the New York Stock Exchange or the Nasdaq as well as Toronto, you need only buy/sell using the U.S. market. Generally, there would be no reason to check prices and such on the Toronto Exchange first.

More often than not, smaller companiesfor both cost and logistical reasonsdo not LIST their shares on a major U.S. exchange. But they are still easily TRADABLE in the U.S. via the NASDAQ’s OTC Market. All you need to know is the company’s symbol; unlike most U.S.-listed companies, it will always be a five-letter symbol ending with an “F.”

In Omineca’s case, its ticker symbol in the U.S. is OMMSF , while on the Toronto Venture Exchange in Canada it is OMM.

The main consideration in buying shares of Canadian stocks via the U.S. OTC market is that SOMETIMESif you look at the OTC quote FIRSTyou are not getting as fresh and accurate a price as you would if you went to the Canadian Exchange. This is because with most, the majority of their activity is on the Canadian market where it is listed; sometimes hours can go by between trades on the OTC, if the company you’re looking to buy isn’t actively traded at the time. Thus, you simply need to insure, via a simple process, that you are neither overpaying for a stock when you buy it, nor getting less than you should when you sell. That is easy to accomplish.

The most reliable and current quotes for shares of companies such as Omineca are to be found first on the Canadian Exchange where they are primarily LISTED. Prices and volume activity are updated all through the trading day on the Toronto Exchange, TSX.V and the TSXV, just as they are on the NYSE or NASDAQ, and are generally fresh/instantaneous.

I will use the following example to show the simple process that will normally take you LESS THAN TWO MINUTES to enter a trade to buy Omineca’s stock via the OTC market in the U.S., in a typical U.S.-domiciled brokerage account:

1. First check the Canadian quote for the company, via its ticker symbol on the TSXV, which is OMM. You’ll find this at the Exchange’s web site, https://tmx.com/. Plug in “OMM.” We’ll say for purposes of this lesson that the current asked price for OMM’s shares is C$0.30, or 30 cents per share in Canadian currency.

2. Next determine what that price is in U.S. currency. If you don’t follow exchange rates on a daily basis, you can get a fresh picture by going to Kitco’s website, at www.kitco.com (or your own favorite one that lists currency differentials; there are many.) Near the bottom of Kitco’s front page, you will find a table of various currency exchange rates. At this writing the Canadian dollar, rounded off, is worth 73.5 cents in U.S. currency.

3. Do the math as to what OMM’s U.S. asked (selling) price on the OTC market should be:

C 30 cents per share X .735 = US 22.05 cents per share.

4. Finally, enter a LIMIT ORDER to buy the number of shares of Omineca you want in your U.S. brokerage account at or very near that price. Personally, I would first start with US 22.1 cents per share. If the order doesn’t fill right away, bump it up by a tenth of a cent once or twice until it does (these days, most online brokers will allow you to use tenths of a cent in pricing.)You would use the company’s 5-letter symbol, which is OMMSF.

It’s that simple! And, of course, you would do much the same thing when it was time to sell some of your holdings. But in the case of a sale, you would focus on the bid price listed on the TSX’s site for the company in question.

Chris Temple is editor and publisher of The National Investor. He has had an over 40-year career now in the financial/investment industry. Temple is a sought-after guest on radio stations, podcasts, blogs and the like all across North America, as well as a sought-after speaker for organizations. His ability to help average investors unravel, understand and navigate today’s markets is unparalleled; and his ability to uncover “off-the-radar” companies is likewise.

His commentaries and some of his recommendations have appeared in Barron’s, Forbes, CBS Marketwatch, Wall Street’s Best Investments/The Cabot Group, Kitco.com, the Korelin Economics Report, Benzinga.com, Palisade Radio, Mining Stocks Education, Mining Stock Daily and other media.

Disclosure: 1) Chris Temple’s and The National Investor disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Omineca Mining and Metals. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Omineca Mining and Metals. Please click here for more information. An affiliate of Streetwise Reports is conducting a digital media marketing campaign for this article on behalf of Omineca Mining and Metals. Please click here for more information.The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Omineca Mining and Metals, a company mentioned in this article.

The National Investor is published and is e-mailed to subscribers from [email protected]. The Editor/Publisher, Christopher L. Temple may be personally addressed at this address, or at our physical address, which is: National Investor Publishing, P.O. Box 1257, Saint Augustine, FL 32085. The Internet web site can be accessed at https://nationalinvestor.com/. Subscription Rates: $275 for 1 year, $475 for two years for “full service” membership (twice-monthly newsletter, Special Reports and between-issues e-mail alerts and commentaries.) Trial Rate: $75 for a one-time, 3-month full-service trial. Current sample may be obtained upon request (for first-time inquirers ONLY.) The information contained herein is conscientiously compiled and is correct and accurate to the best of the Editors knowledge. Commentary, opinion, suggestions and recommendations are of a general nature that are collectively deemed to be of potential interest and value to readers/investors. Opinions that are expressed herein are subject to change without notice, though our best efforts will be made to convey such changed opinions to then-current paid subscribers. We take due care to properly represent and to transcribe accurately any quotes, attributions or comments of others. No opinions or recommendations can be guaranteed. The Editor may have positions in some securities discussed. Subscribers are encouraged to investigate any situation or recommendation further before investing. The Editor receives no undisclosed kickbacks, fees, commissions, gratuities, honoraria or other emoluments from any companies, brokers or vendors discussed herein in exchange for his recommendation of them. All rights reserved. Copying or redistributing this proprietary information by any means without prior written permission is prohibited. No Offers being made to sell securities: within the above context, we, in part, make suggestions to readers/investors regarding markets, sectors, stocks and other financial investments. These are to be deemed informational in purpose. None of the content of this newsletter is to be considered as an offer to sell or a solicitation of an offer to buy any security. Readers/investors should be aware that the securities, investments and/or strategies mentioned herein, if any, contain varying degrees of risk for loss of principal. Investors are advised to seek the counsel of a competent financial adviser or other professional for utilizing these or any other investment strategies or purchasing or selling any securities mentioned. Chris Temple is not registered with the United States Securities and Exchange Commission (the SEC): as a broker-dealer under the Exchange Act, as an investment adviser under the Investment Advisers Act of 1940, or in any other capacity. He is also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.

Notice regarding forward-looking statements: certain statements and commentary in this publication may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 or other applicable laws in the U.S. or Canada. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of a particular company or industry to be materially different from what may be suggested herein. We caution readers/investors that any forward-looking statements made herein are not guarantees of any future performance, and that actual results may differ materially from those in forward-looking statements made herein.

Copyright issues or unintentional/inadvertent infringement: In compiling information for this publication the Editor regularly uses, quotes or mentions research, graphics content or other material of others, whether supplied directly or indirectly. Additionally he makes use of the vast amount of such information available on the Internet or in the public domain. Proper care is exercised to not improperly use information protected by copyright, to use information without prior permission, to use information or work intended for a specific audience or to use others’ information or work of a proprietary nature that was not intended to be already publicly disseminated. If you believe that your work has been used or copied in such a manner as to represent a copyright infringement, please notify the Editor at the contact information above so that the situation can be promptly addressed and resolved.

Additional disclosure: Omineca Mining & Metals was formally recommended to paid subscribers/Members of The National Investor in March, 2019. Neither this nor any company recommended by Chris Temple pay for such recommendations, which the Editor makes based on his own research, opinions, due diligence, best efforts, etc. In some cases, following a recommendation to subscribers/Members, companies will work with National Investor Publishing in regard to media placement and added advertising/distribution of Editors recommendation of the company. In the case of Omineca, the company has paid to National Investor Publishing a total of approximately US$7,500.00 prior to and concurrent with this particular report for the companys profile being included in a separate, Gold-centric Special Issue, for this particular individual Profile of the Company and for reprint rights/rights to separately distribute the same as it sees fit. This is simply an advertising/editorial service provided to Omineca by National Investor Publishing. National Investor Publishing does not engage in investor relations, brokerage, investment advisory or any similar, regulated activity in conjunction with the publishing of this Special Report. As of the date of this Special Report, the Editor owns securities of Omineca.

EURUSD bias bearish despite recovering German consumer confidence

Consumer confidence in Germany continued to recover in June: German GfK consumer climate index rose to -9.6 in June from -18.6 in May, when a recovery to -11.7 was expected. This is bullish for EURUSD, but the pair is still falling.

– The financial sector has been one of the global stock market’s bedrocks for decades. That’s why its performance is so critical to the overall stock market health.

Well, here’s a chart of the European Stoxx 600 Banks Index over the past four years.

Not pretty, we know.

Now let’s zoom in on the price action since January of this year.

This is where the mainstream’s story about Europe’s beaten down banking sector starts. It’s a story of being “hit hard,” of credit losses which exceed those in the 2008 financial crisis — and finally, the onset of “more pain” in the future. All “thanks” to the coronavirus.

Except, it’s a mistake to blame Europe’s banking sector sell-off on the coronavirus.

Yes, the sector fell 43% since the start of 2020, but that’s not when the “beat down” started!

It began in 2018 — many months before the first reported case of coronavirus on December 31, 2019.

Back in 2018, the EuroStoxx 600 was a top-performer and stood at a two and a half-year high.

At the time, there was no bearish “fundamental” backdrop like the coronavirus, and few things suggested to mainstream analysts any weakness ahead.

BUT — on April 6, 2018, Elliott Wave International’s Monday-Wednesday-Friday publication European Short Term Update showed subscribers this red line down for emphasis and said,

April 6, 2018 forecast: “…banks have a long way further to fall. Stay immediately bearish this sector.”

From there September 2019, the sector plunged 40%. A rally into the end of 2019 was met with renewed optimism that “Europe’s bank stocks poised for best start to a year since 2013.” (Bloomberg)

But to Elliott Wave International’s analysts, further bearish potential was clear.

As you may know, Elliott wave analysis doesn’t look at the so-called fundamentals. Factors like unemployment, GDP, etc., don’t lead the stock market — they follow it.

In other words, to know the stock market’s next move, you must skip “fundamentals” and instead look at market psychology, the true driver of trends.

That’s exactly what Elliott wave patterns in market charts show you.

Which brings us to this year’s continued sell-off in Europe’s banking sector.

On January 13, 2020, well before coronavirus really got going, Elliott Wave International’s European Short Term Update identified a completed countertrend advance on the Banks Sector index.

January 13, 2020 forecast: Europe’s bank stocks “should decline directly.”

From there, the sector indeed hit the skids in a sell-off to levels not seen in more than a decade — that 43% slide we mentioned earlier.

And please note this: Elliott Wave International’s analysis didn’t mention coronavirus even once when making that bearish January 13 forecast. The bearish outlook was based on the fact that the price pattern called for a 3rd wave down directly ahead.

Third waves are fastest and strongest parts of the Elliott wave patterns. That helps explain the speed and ferocity of this year’s decline in Europe’s banking sector.

This is just one example (of MANY!) where Elliott Wave International’s European Financial Forecast Service put subscribers on the right side of the trend.

What are we saying now? What’s next for Europe, its markets and economies?

See for yourself right now, 100% free.

Through July 1, read Elliott Wave International’s Europe-focused publications free during the ongoing FreeWeek: Europe event.

“Free” means free. There is no catch. There is no credit card required. You can see where Europe’s key markets and economies are headed next, according to Elliott waves. Just click the link below for instant access to the latest forecasts.

This article was syndicated by Elliott Wave International and was originally published under the headline Europe’s Banking Sector: When (and Why) the Rout Really Began. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

Mexico’s central bank has cut interest rates 8 times since it started its current loosening cycle last year. It has now cut a total of 275 basis points.

That’s the second-fastest pace and largest cut of central banks in the world. But at 5.5%, Mexico still has one of the highest (inflation-adjusted) interest rates in the world.

However, it doesn’t seem to be enough to jumpstart the economy. And there are various expectations of further rate cuts in the near future.

The Banxico is in an especially difficult place. The Mexican economy already heading into a recession even before COVID reached the country.

It’s understandable that their focus is much more on the exchange rate and economic activity, and that they don’t care so much about inflation.

Without an improvement in underlying economic activity, we can expect this to be the theme not just for this meeting, but for the next several months

What We Are Expecting

There is a near-unanimous consensus that the Banxico will cut interest rates again by another 50 basis points. This would bring the rate to 5.0%.

Expectations are for the subsequent press conference to be quite pessimistic. The Governor is likely to reiterate that further action is necessary. That’s also what the market is pricing in, so it’s unlikely that there will be a sudden move in the MXN immediately after the policy decision.

One of the things that affect the market reaction to Mexican rate decisions is that the central bank is seen as unsure between contradictory positions. It tries to signal a need to boost the economy while at the same time trying to keep markets from overheating.

The lack of clarity makes projecting future policy harder. Therefore, it gets in the way of pricing in market reaction.

Standing Out Isn’t Always the Best

The Banxico stands out among its Latin American peers as having the smallest deviation from its regular policy, despite being in the middle of a pandemic.

There has been increasing criticism that the central bank hasn’t done enough to help the economy. Political pressure might propel more aggressive action in the future, even as other countries stabilize policy.

Ironically for the central bank trying to keep a lid on the exchange rate, expectations of further cuts in the rates might make it harder to control the currency’s depreciation compared to peers.

Future Trajectory

While there is a strong consensus for today’s meeting, after that, analyst consensus diverges a bit.

All the surveyed economists predict that the Banxico will cut rates by at least another percent from today to the end of the year. A small majority, however, project an even more drastic cut, to reach between 3.0-3.5%.

With the inflation rate projected to be in that range for this year, it would effectively mean cutting rates to 0%

The consensus is that the underlying economic circumstances won’t change the trajectory of the policy all that much. Rates are expected to fall while the Banxico tries to talk up the currency. More “hawkish cuts” appear to be in store.

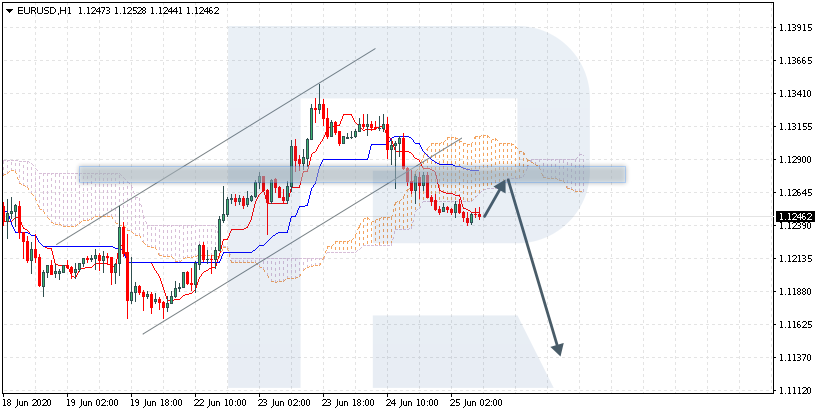

EURUSD is trading at 1.1246; the instrument is moving below Ichimoku Cloud, thus indicating a descending tendency. The markets could indicate that the price may test the cloud’s downside border at 1.1265 and then resume moving downwards to reach 1.1135. Another signal in favor of further downtrend will be a rebound from the resistance level. However, the bearish scenario may be canceled if the price breaks the cloud’s upside border and fixes above 1.1310. In this case, the pair may continue growing towards 1.1395.

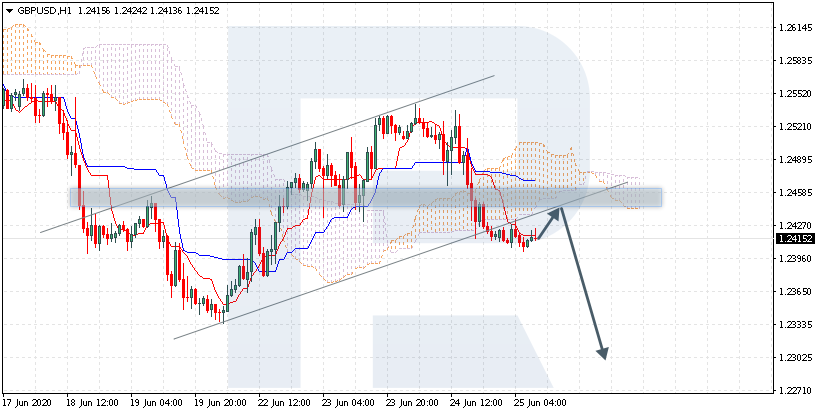

GBPUSD, “Great Britain Pound vs US Dollar”

GBPUSD is trading at 1.2415; the instrument is moving below Ichimoku Cloud, thus indicating a descending tendency. The markets could indicate that the price may test the cloud’s downside border at 1.2440 and then resume moving downwards to reach 1.2305. Another signal in favor of further downtrend will be a rebound from the rising channel’s downside border. However, the bearish scenario may no longer be valid if the price breaks the cloud’s upside border and fixes above 1.2525. In this case, the pair may continue growing towards 1.2715.

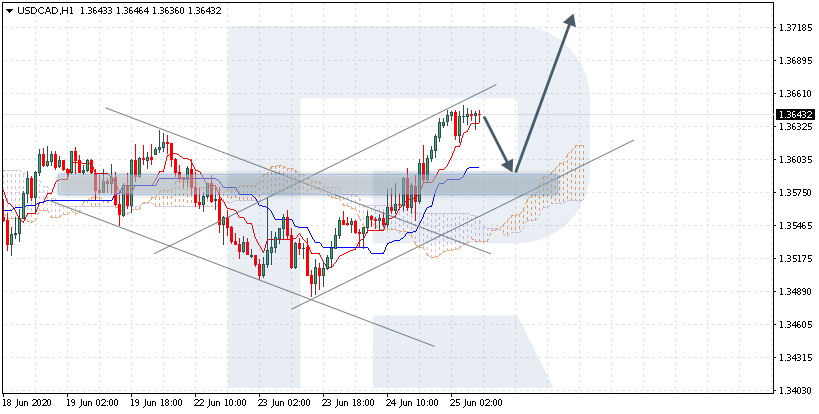

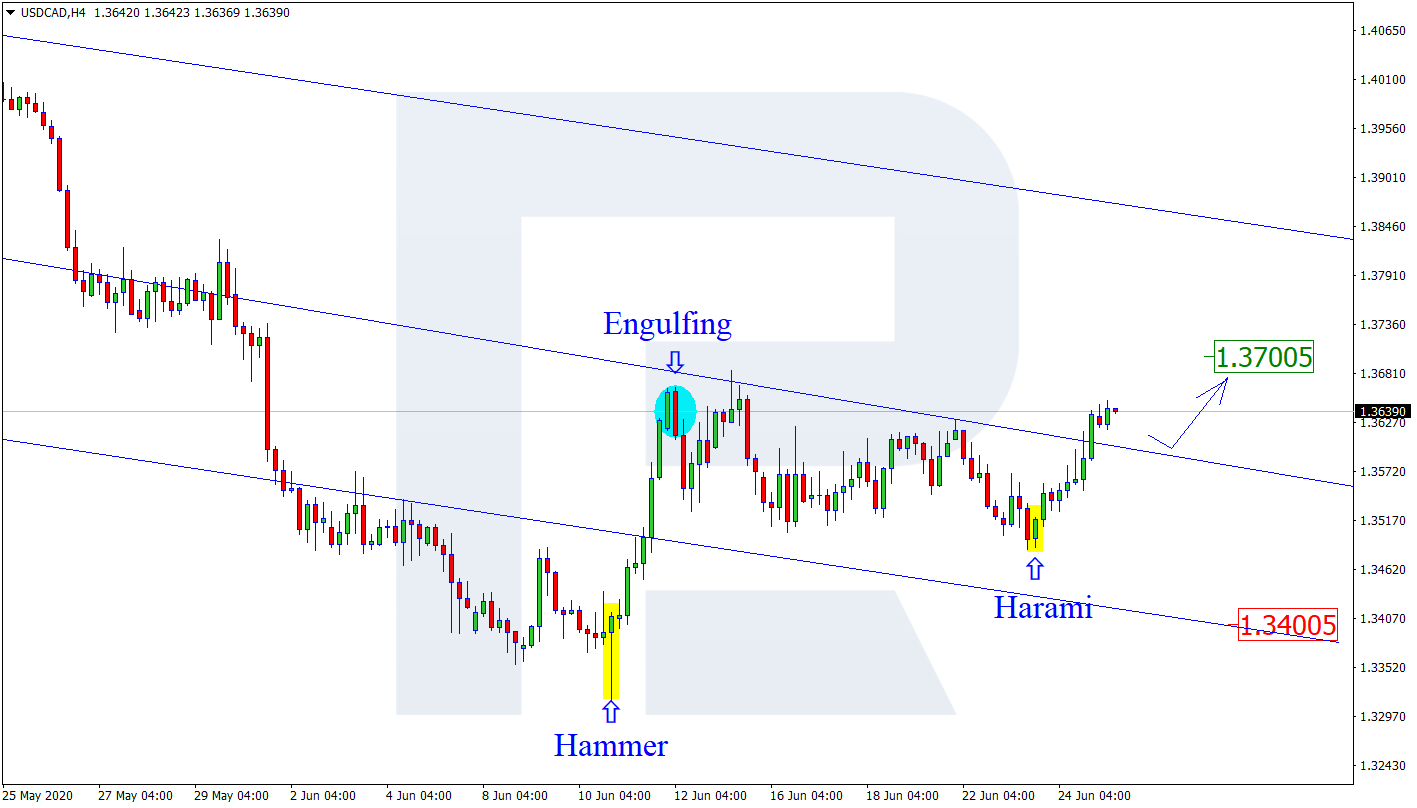

USDCAD, “US Dollar vs Canadian Dollar”

USDCAD is trading at 1.3643; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test Tenkan-Sen and Kijun-Sen at 1.3600 and then resume moving upwards to reach 1.3725. Another signal in favor of further uptrend will be a rebound from the rising channel’s downside border. However, the bullish scenario may no longer be valid if the price breaks the cloud’s downside border and fixes below 1.3525. In this case, the pair may continue falling towards 1.3435.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

As we can see in the H4 chart, USDCAD is still rebounding from the support level and reversing after completing a Harami reversal pattern. At the moment, the pair is moving below the resistance level. However, considering the current downtrend, one may assume that the asset may finish the correction and test 1.3700. Still, an opposite scenario suggests that the instrument may fall to reach 1.3400

AUDUSD, “Australian Dollar vs US Dollar”

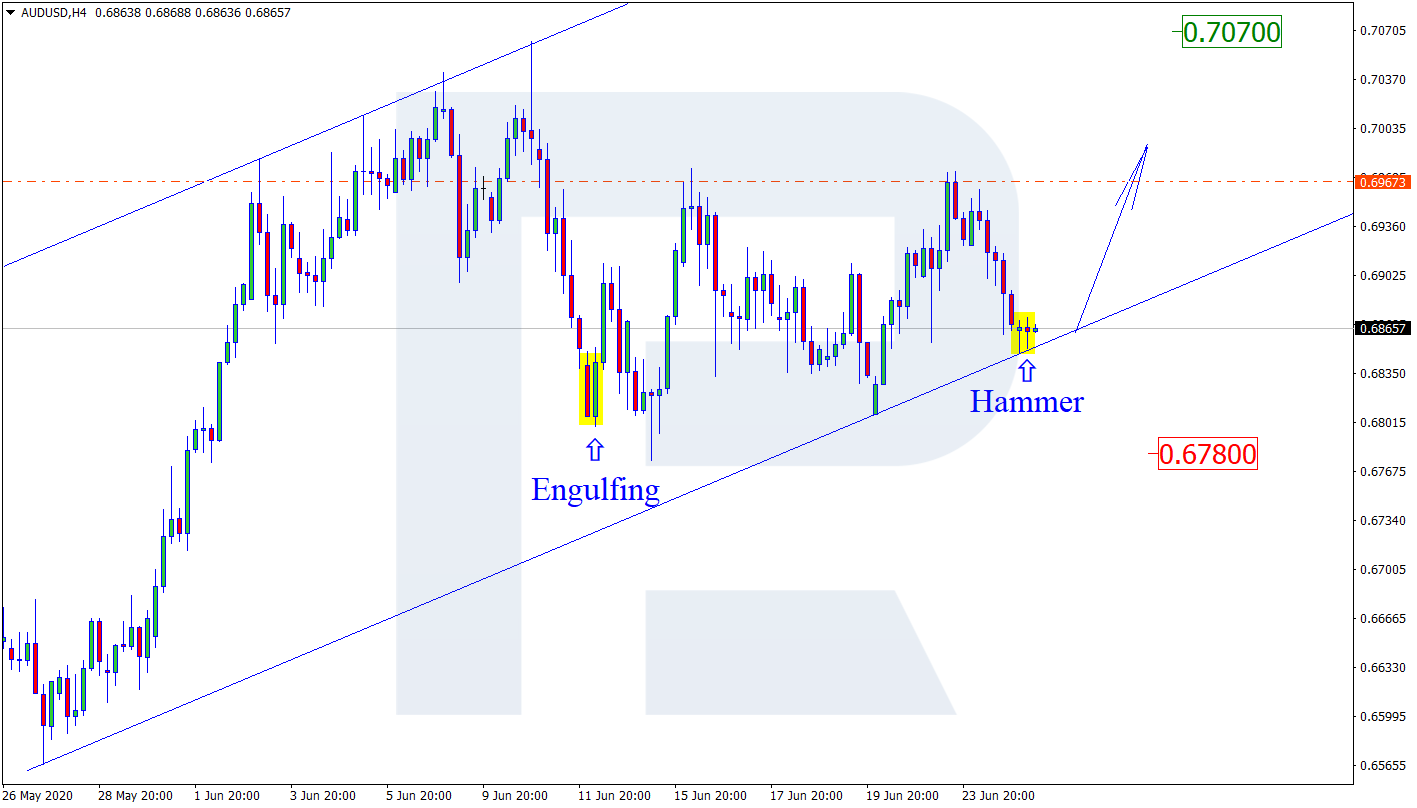

As we can see in the H4 chart, AUDUSD is still correcting within the uptrend. By now, it has formed a Hammer pattern not far from the channel’s downside border. The target of the reversal pattern is the closest resistance level. Later, the price may resume the rising tendency. In this case, the mid-term upside target remains at 0.7070. At the same time, one shouldn’t exclude another scenario, which implies that the instrument may continue falling towards 0.6780.

USDCHF, “US Dollar vs Swiss Franc”

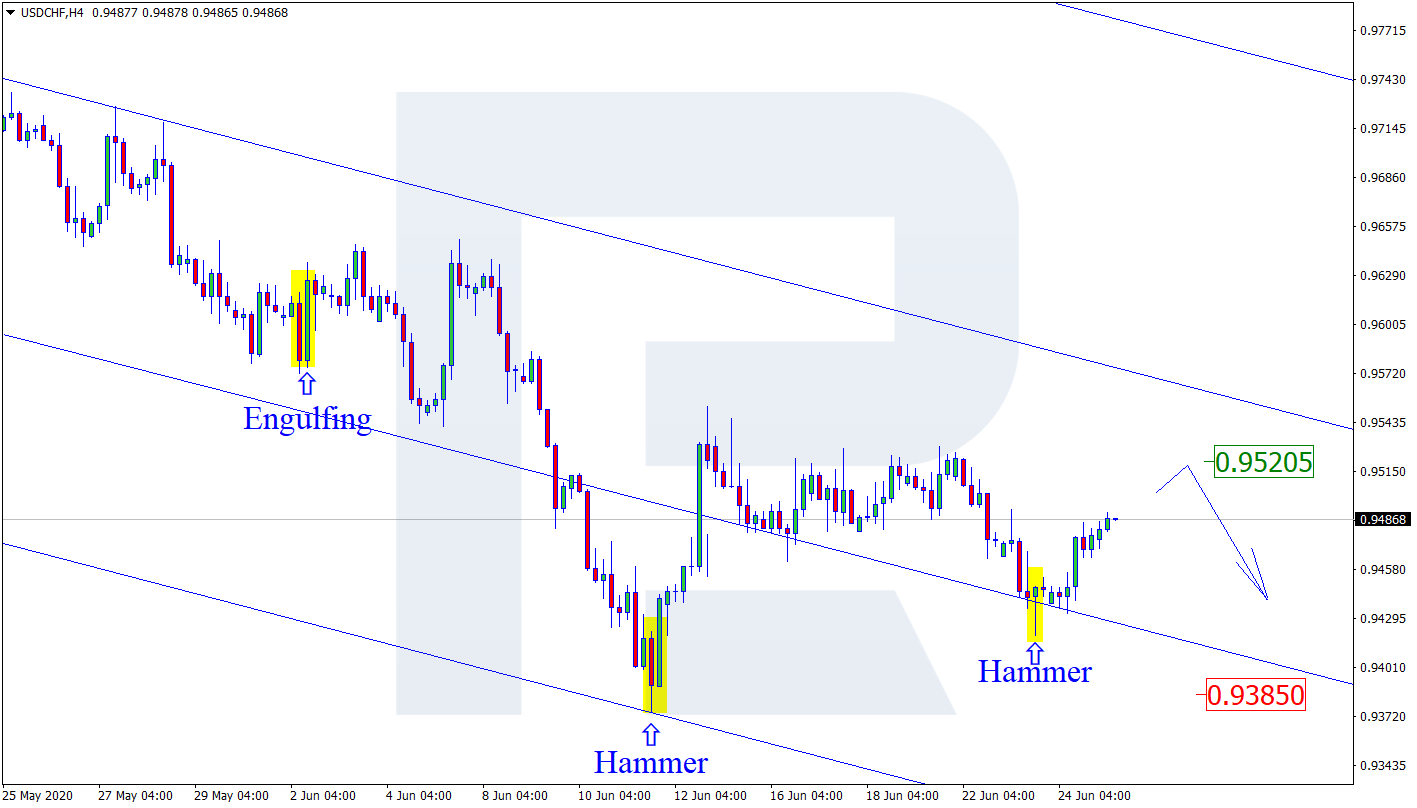

As we can see in the H4 chart, after forming a Hammer pattern and reversing, USDCHF has rebounded from the support level. At the moment, the pair continues forming the rising impulse. In this case, the upside target is the resistance area at 0.9520. Later, the market may rebound from this level and resume trading downwards. In this case, the downside target may be the support level at 0.9385.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

The euro currency is trading weaker on Wednesday after failing to keep up on the momentum from the previous session.

The common currency erased all gains from earlier as it moved back to the lower technical support near 1.1261.

This potentially creates a short term sideways range with the technical resistance at 1.1347 holding up as well. A breakout from either of these levels is needed.

We suspect that the risk is to the downside unless there is a rebound. A break down below the support area at 1.1261 will open the way for EURUSD to test the 1.1132 level this time around.

But, this will be subject to prices closing the previous lows near 1.1173.

GBPUSD Tumbles But Remains Range-Bound For Now

The pound sterling is down near 0.60% on the day, erasing some of the gains from the previous few sessions.

The reversal came after the pound sterling failed to breakout above the technical resistance level near 1.2516.

This has pushed price lower as a result. But the declines are limited for the moment.

GBPUSD is likely to find support near the 1.2368 level from which iT recovered earlier on.

However, if price breaks down below this level, it opens the risk for further declines.

The next key support area is around the 1.2250 level marking the 28 May lows.

WTI Slips On Inventory Build

WTI Crude oil prices are down over 3% intraday. The declines come just after prices touched a three-month high near 41.50.

Following this gain, oil prices are trading back below the 40 handle which had proven to be a bit of a struggle to break earlier on.

Currently, WTI crude oil is likely to slip further to the lower support area around the 37.67 handle.

We expect support to hold in here as it might attract new buyers into the market.

But there is a real risk of prices collapsing further pushing oil back to the lower support area at 34.42.

A test of this level could potentially cement the upside considering that the 34.42 handle wasn’t tested firmly.

Gold Prices Pause As Momentum Slows

The precious metal is seen slowing down its gains following the recent breakout.

There seems to be a technical resistance near the 1774.50 handle.

Still, at the time of writing gold prices are attempting to break out above this level. This will keep the 1800 level within sight for the precious metal.

However, there is also a risk of a pullback. We could expect to see a possible correction if gold prices close below the recent intraday lows of 1766.87.

A daily close below this level could see a move to the 1747 handle, followed by a retest of the 1732 level in order for support to be established.

The latest report from the Energy Information Administration showed that in the week ending June 19th, US crude stores rose by a further 1.4 million barrels.

This was above the rise in inventories recorded last week. It also surpassed the expected 1.2 million barrel reading the market was looking for. Once again, this reflects a lack of demand for fuel products, despite lockdown measures easing in the US.

The total products supplied number is used as a proxy to gauge overall demand. This number was down over the last four weeks by an average of 8 million barrels per day. This is 17% lower than the same period last year.

Second Wave Creating Headwinds

Crude oil prices have been back under this pressure this week. This comes as a result of a trickier risk environment, as equities retreat on rising fears of a second wave of COVID-19.

Fears of a fresh outbreak have taken the shine off the recovery underway across the globe as lockdown measures ease. Unfortunately, many countries are reporting fresh increases in the number of new infections.

Parts of the US has been reporting their highest numbers of the pandemic so far. This led to Apple announcing that it will temporarily close 11 US sites in response.

Elsewhere, China has placed Beijing back under lockdown. The city has reintroduced travel restrictions as, it too, deals with a fresh surge in infection numbers.

Meanwhile, in the UK, as the government prepares to ease lockdown measures further on July 4th, health authorities have warned of the risks of an increase in the virus.

Traders have been shying away from riskier assets this week including oil prices which have seen heavier selling following decent buying on Monday.

The risks of a return to lockdown measures in the event of a second wave raise obvious risks for crude oil. The commodity saw demand decimated over the first half of the year as a result of the virus.

Bullish Forecasts From Citigroup

The outlook is not totally bleak, however. Analysts at Citigroup see crude prices recovering to north of $60 over the next 18 months.

This would be fuelled by the heavy supply cuts in effect from OPEC+, along with the reduction in shale oil output as producers reduce activity amidst the price crash.

Crude Still Capped by 61.8%

Crude oil price made a fresh attempt at breaking above the 61.8% retracement of the decline from 2020 highs this week. However, the level continues to hold as resistance.

With bearish divergence showing on the RSI, the risk of a correction back lower is increasing. While price remains supported at the 33.17 level, however, focus remains on a further push higher and an eventual break of the 42.43 level.