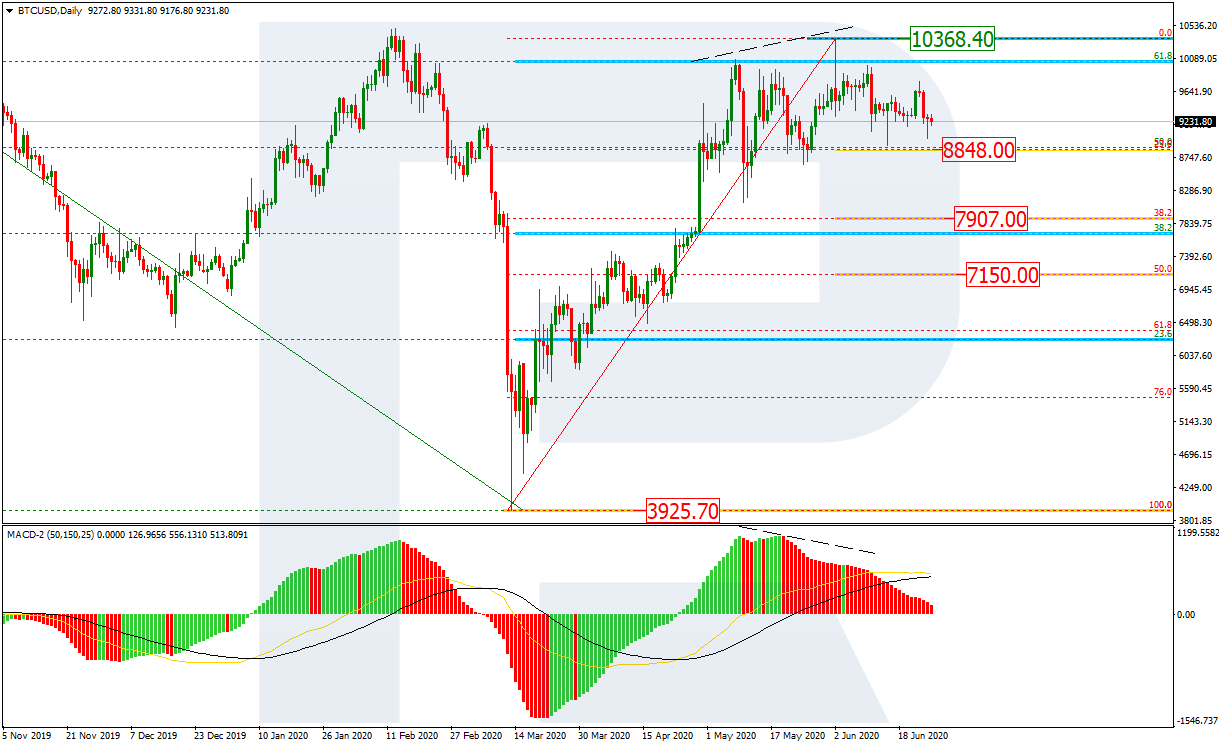

In the daily chart, the situation has remained unchanged for quite a long time. After Bitcoin reached the mid-term 61.8% fibo, there was a divergence but the price failed to start a new downtrend. All attempts to grow are facing strong bearish pressure. The asset is still trading between the high (10368.40) and the first correctional target, which is 23.6% fibo at 8848.00. If the instrument breaks this level, it may continue falling towards the next targets – 38.2% and 50.0% fibo at 7907.00 and 7150.00 respectively.

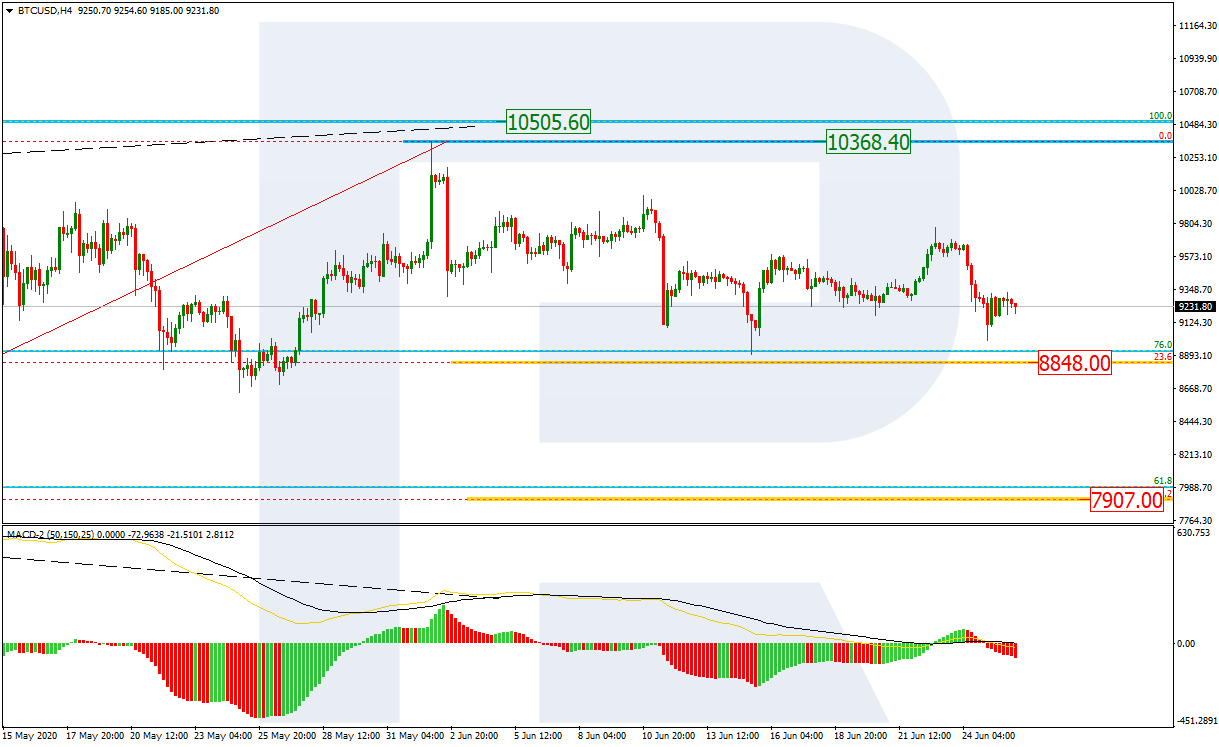

As we can see in the H4 chart, after completing the local rising correction, the pair has finished the descending impulse towards 23.6% fibo at 8848.00.

ETHUSD, “Ethereum vs. US Dollar”

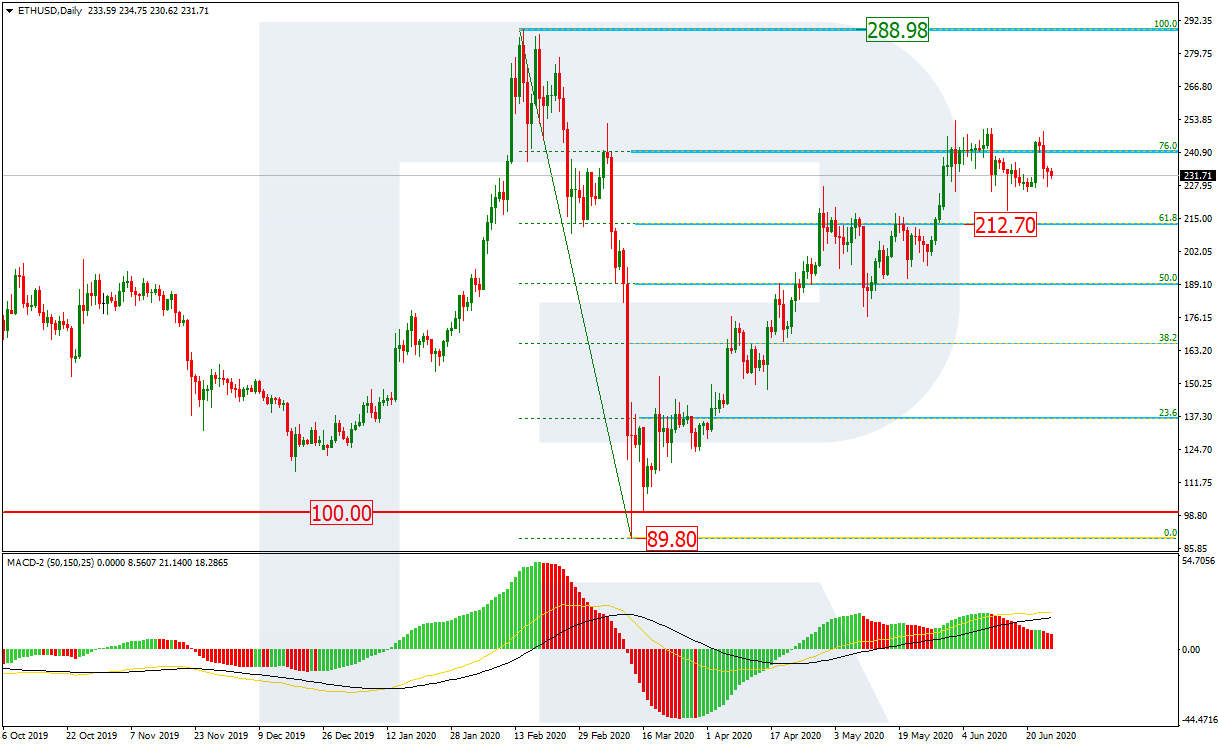

As we can see in the daily chart, Ethereum moving close to 76.0% fibo. Earlier, the asset tried to resume moving downwards but failed to break the support at 61.8% fibo at 212.70. The bearish scenario remains more probably but once shouldn’t exclude the possibility of further growth towards the fractal high at 288.98.

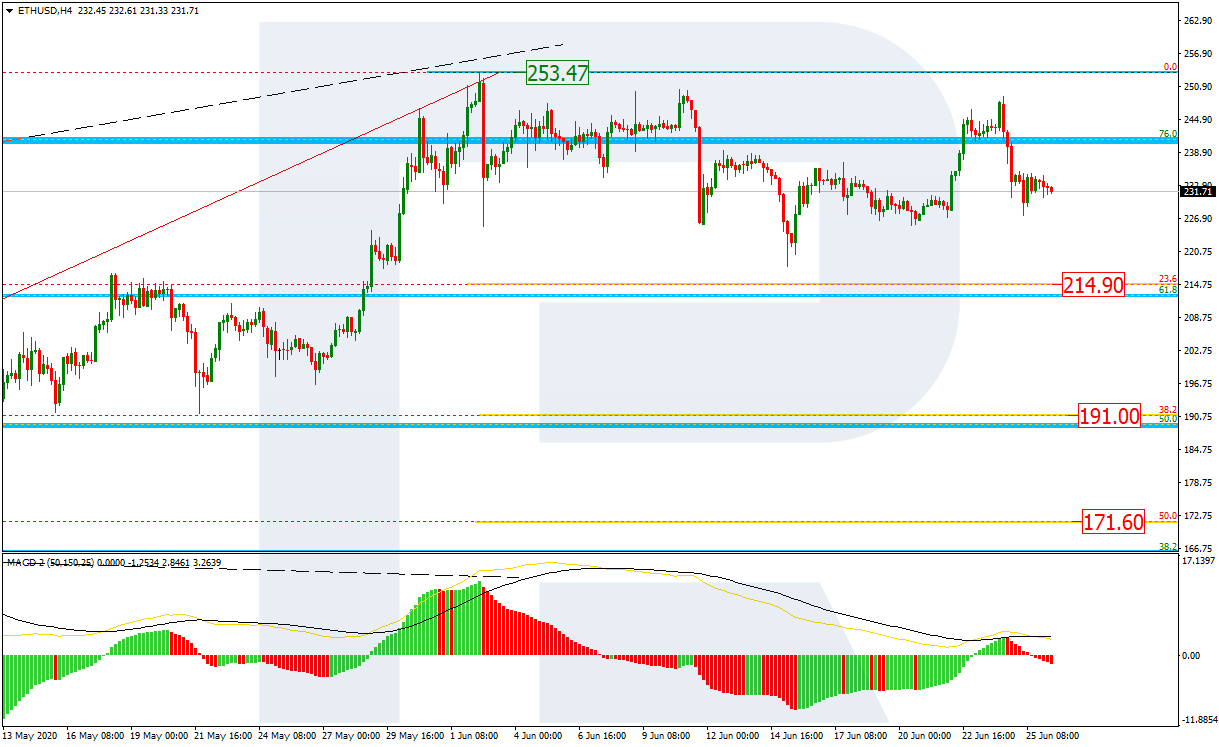

The H4 chart shows a more detailed structure of the current descending wave after an attempt to test the high at 253.47. The downside target may be 23.6%, 38.2%, and 50.0% fibo at 214.90, 191.00, and 171.60 respectively.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Mexico’s central bank cut its benchmark interest rate for the fifth time this year, saying the risks to the economy remain to the downside and there is persistent uncertainty about the economic recovery after a considerable impact from the Covid-19 pandemic. The Bank of Mexico, known as Banxico, cut its target for the overnight interbank interest rate by another 50 basis points to 7.0 percent and has now cut it 225 points this year following cuts in February, March, April and May. It is also Banxico’s 9th rate cut since August 2019 when it began to unwind some of rate hikes – a total of 500-basis-points – between December 2015 and December 2018. Since August last year the rate has been cut 325 points. The bank’s board said its decision today was unanimous and future actions will be based on the impact on economic activity from the Covid-19 pandemic and the evolution of the financial shock so the policy rate is consistent with inflation around Banxico’s target. Mexico’s economy has contracted in the last four quarters, with gross domestic product in the first quarter down 1.2 percent from the previous quarter. In late May Banxico forecast the economy would contract as much as 8.8 percent this year. Banxico said the reopening of parts of the economy in May and June will lead to some recovery though the impact of the pandemic have been “considerable and uncertainty persists” and growth risks remain significantly biased to the downside. Mexico’s inflation rate rose to 2.84 percent in May and 3.17 percent in the first half of June from 2.15 percent in April and the central bank said expectations are for inflation to remain above its 3.0 percent goal.

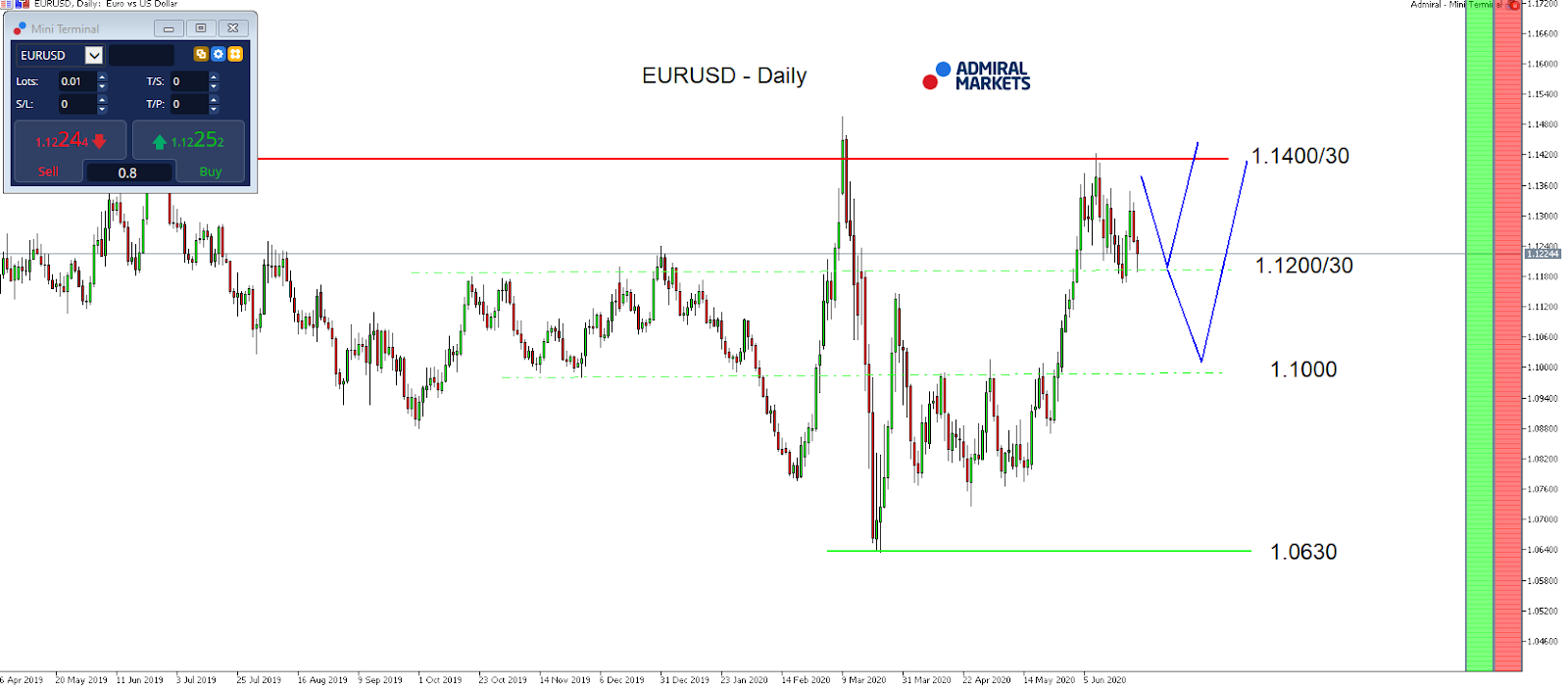

After the EUR/USD re-tested the region around 1.1150/1200, the Euro took on bullish momentum again, quickly recapturing 1.1300.

A potential driver for this comes from recent unexpected European economic indications over the last few days, such as the Manufacturing PMI for France last Tuesday increasing to 52.1 for June, beating market forecasts of 46 and pointing to the biggest expansion in the manufacturing sector since September of 2018. There also was the German ifo Business Climate indicator last Wednesday, rising by 6.5 points from the previous month to a four-month high of 86.2, beating market expectations 85.0 and pointing to the largest monthly increase in the index ever.

While we certainly remain cautious in regards to the sustainability of these numbers after the Corona lockdown, the overall picture in the Euro against the US dollar stays definitely positive with the focus on the upside around 1.1400/50.

For the weekly close, US economic projections will be our focus, particularly regarding Personal Spending and Personal Income.

What will also be of interest is whether the tendency over the last weeks and the Citi US Economic Surprise Index hitting record high after record, continues.

If not, and 10-year US yields see another attempt to break below 0.60%, EUR/USD will likely see a deep green weekly close, bringing the region around 1.1400/50 into our focus into the end of the Q2 2020:

Source: Admiral Markets MT5 with MT5-SE Add-on EUR/USD Daily chart (between April 26, 2019, to June 25, 2020). Accessed: June 25, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of the EUR/USD fell by 10.2%, in 2016, it fell by 3.2%, in 2017, it increased by 13.92%, 2018, it fell by 4.4%, 2019, it fell by 2.2%, meaning that after five years, it was down by 7.3%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

US stock markets could see a massive spike in trading volume today, as the Russell indexes reconstitution takes place. The once-a-year process involves adjusting the list of stocks that makes up the indexes, with an estimated US$9 trillion in assets linked to those benchmarks. Bank of America is expecting “record-breaking changes” for this year’s episode, while Keefe, Bruyette & Woods estimates net trading to be around US$65 billion.

This imminent reconstitution may have an outsized impact, due to the immense changes to the equities landscape amid the global pandemic, along with the already elevated trading volumes in US stock markets seen for much of this year. Volumes are still near the highest levels since 2009.

The Russell reconstitution could also roil markets as the keenly-awaited event comes amid persistently elevated volatility, with the VIX index holding stubbornly above the 30 level.

To be sure, US equities appear to have enough resilience to weather today’s episode, going by recent past performance. During the June 19 quadruple witching and S&P quarterly rebalancing, total US stocks trading volumes surged by 61.5 percent compared to the day prior, which is its largest increase since December 20, 2019. The S&P 500, which has an estimated US$11.2 trillion in assets tied to it according to S&P Dow Jones, ended down 0.56 percent last Friday, and has declined by a further 0.45 percent since.

Even if it’s all smooth-sailing for US stocks going into the weekend, the final trading days of June could see pension funds and other major investors rebalancing their respective portfolios, potentially booking some of the tremendous gains seen in US equities this quarter. Since March 31, the S&P 500 has climbed over 19 percent, the Dow is up by more than 17 percent, while the Nasdaq composite has soared by 30 percent. Wall Street estimates for the quarter-end pension fund rebalancing ranges between US$35 billion to US$76 billion.

These technical events could inject a huge dose of volatility into the markets over the coming days, potentially exacerbating the effects of major developments that sway global risk sentiment, such as the flare up in US coronavirus cases. Risk assets have clearly grown comfortable ignoring the world’s gloomy fundamentals, with the IMF adding to the chorus that’s highlighting the disconnect between financial markets and the economic outlook. Yet, with global equities having lost much of its upward momentum of late, perhaps the induced volatility could be the jolt markets need in order to break out of its sideways saunter.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Guatemala’s central bank lowered its monetary policy rate for the third time this year, saying this is aimed at lowering the cost of credit for companies and households and thus help promote a recovery of economic activity. The Bank of Guatemala cut it policy rate by a further 25 basis points to 1.75 percent and has now cut it 100 points this year following two rate cuts in March. This includes a 50-basis-point cut on March 19 at an extraordinary board meeting, the same week when 46 other central banks, including the U.S. Federal Reserves, lashed their rates in response to the global measures to prevent the spread of the Covid-19 pandemic. The bank’s monetary board said in a statement released on June 25 that its policy decision, which was taken at its June 24 meeting, was unanimous. A significant slowdown in economic activity in Guatemala and imports has been partially moderated due to a better-than-expected performance of exports, family remittances and bank credit to the private sector, the central bank said, referring to the monthly index of economic activity (IMEA). However, the central bank still lowered its forecast for the economy to contract between 3.5 and 1.5 percent this year from its previous forecast of a contraction of 0.5 percent. In 2019 Guatemala’s economy grew an estimated 3.8 percent. The economy should recover next year and expand between 2.0 and 4.0 percent, the bank added. Guatemala’s inflation rate has been relatively steady in recent months – it eased to 1.8 percent in May from 1.88 percent in April – and the central bank said its latest forecast show a moderation this year and in 2021, with inflationary expectations anchored to its target. The Bank of Guatemala, which has targeted inflation since 2005, currently targets inflation of 4.0 percent, plus/minus 1 percentage point. Guatemala’s quetzal has been relatively stable since October 2018 and was trading at 7.7 to the U.S. dollar today, unchanged since the start of this year. Earlier this month the executive board of the International Monetary Fund approved emergency financial assistance to Guatemala of US$594 million to help meet some of the cost of containing Covid-19 at a time of a hit to economic growth and a drop in remittances from abroad and lower exports.

Global stocks are mixed today after a rebound on Thursday. US markets ended higher yesterday after the Federal Reserve announcement the central bank is planning to loosen the restrictions imposed by the Volcker rule which will allow banks to more easily make large investments into venture capital and similar funds.

Forex news

Currency Pair

Change

EUR USD

-1.01%

USD JPY

-0.23%

USD CHF

-0.16%

The Dollar strengthening continues today ahead of US inflation and personal spending reports. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.2% Thursday as US Census Bureau reported durabl;e goods orders rose above expected 15.8% over month in May. Both GBP/USD and EUR/USD continued their sliding yesterday despite GfK report German consumer confidence continued to recover in June. Both pairs are lower currently. AUD/USD joined USD/JPY’s continued climbing yesterday with yen higher currently against the greenback while Australian dollar is down.

Stock Market news

Indices

Change

Dow Jones Index

-0.79%

GB 100 Index

-0.63%

Nikkei Index

-1.12%

Hang Seng Index

+0.42%

Futures on three main US stock indexes are edging lower currently after a choppy trading Thursday. The three main US stock indexes rebounded ahead of Fed release of the results of its bank stress tests, recording gains ranging from 1.1% to 1.2% led by banking stocks. US Senate passed a legislation that would impose mandatory sanctions on people or companies that back efforts by China to restrict Hong Kong’s autonomy, that has to pass the House and be signed by President Trump. European stock indexes are retreating today after ending higher Thursday. Asian indexes are mostly higher today led by Australia’s All Ordinaries ASX 200 Index .

Commodity Market news

Commodities

Change

Brent Crude Oil

-0.27%

WTI Crude

+0.73%

Brent is extending gains today. Oil prices advanced yesterday buoyed by White House Economic Advisor Larry Kudlow comment the US was not going to shut the economy down despite reports of rising coronavirus cases. The US oil benchmark West Texas Intermediate (WTI) futures ended solidly higher yesterday: August WTI rose 1.9% and is higher currently. August Brent crude closed 1.8% higher at $41.05 a barrel on Thursday.

Gold Market News

Metals

Change

Silver

-0.01%

Gold prices are edging lower today . August gold slipped 0.3% to $1770.60 an ounce on Thursday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Shares of green hydrogen solutions provider Plug Power established a new 52-week high after the company reported it completed two acquisitions and raised 2024 Revenue and EBITDA targets.

Global hydrogen fuel cell solutions company Plug Power Inc. (PLUG:NASDAQ) yesterday announced that it has completed the acquisitions of United Hydrogen Group Inc. and Giner ELX. The firm advised that “the acquisitions are in line with its vertical integration strategy in the hydrogen business laid out in September of 2019 with plans to have more than 50% of the hydrogen used to be green by 2024.”

The company indicated “that these activities further enhance Plug Power’s position in the hydrogen industry with capabilities in generation, liquefaction and distribution of hydrogen fuel complementing its industry-leading position in the design, construction, and operation of customer-facing hydrogen fueling stations and that these activities establish a clear pathway for Plug Power to transition from low-carbon to zero-carbon hydrogen solutions.”

The company additionally reported that with the closing of the acquisitions “it is raising its 2024 financial targets to achieve $1.2 billion in revenue (up from $1 billion), $210 million in operating income (up from $170 million), and $250 million in adjusted EBITDA (up from $200 million).” The firm added that the higher estimates are based upon the added value of this vertical integration, significant margin improvement and anticipated global growth in the electrolyzer market.

The firm stated that the planned capacity addition will serve the significant and rapidly growing demand for green hydrogen. Presently, Plug Power projects that its current clients will be using nearly 100 tons of hydrogen daily by 2024 with over 50% of that to be green hydrogen. The company mentioned that the additional green hydrogen generation capabilities will enable it to serve customers in the ammonia, fertilizer and steel manufacturing markets.

The company explained that one of the acquired firms, United Hydrogen, has the capability to produce 6.4 tons of hydrogen each day with plans to increase that capacity to 10 tons daily.

The other firm, Giner ELX, includes experienced teams in PEM electrolysis. The company stated that “Giner ELX’s offerings include one of the world’s largest, most efficient and cost-effective PEM hydrogen generators; grid-level renewable energy storage solutions; and on-site hydrogen generation systems for fuel cell vehicle refueling stations and industrial uses.” Plug Power noted that acquiring Giner ELX adds significant manufacturing capabilities to serve the global electrolyzers market.

The company’s CEO Andy Marsh remarked, “Plug Power is working to build the modern clean hydrogen economy…Every decision we make is with an eye to the future, not the past. This closely aligns with the efforts that companies like United Hydrogen and Giner ELX have made to secure broad participation in the hydrogen economy, and to achieve the objectives of a clean environment and reduced dependence on foreign oil. We welcome these organizations into the Plug Power family where, as a team, we can accelerate the adoption of low carbon and zero carbon hydrogen on a global scale.”

Plug Power is based in Latham, N.Y., and stated that “it is building the hydrogen economy as the leading provider of comprehensive hydrogen fuel cell turnkey solutions.” The company’s technology is used to power electric motors with hydrogen fuel cells. The firm pointed out that it has now deployed over 32,000 fuel cell systems for e-mobility. The company noted that it has built and operated a hydrogen highway across North America and is the largest buyer of liquid hydrogen.

Plug Power has a has a market capitalization of around $2.1 billion with approximately 324.3 million shares outstanding and a short interest of about 21.6%. PLUG shares opened almost 13% higher today at $7.25 (+$0.82, +12.75%) over yesterday’s $6.43 closing price and reached a new 52-week high price this morning of $7.75. The stock has traded today between $6.91 and $7.75 per share and is currently trading at $7.54 (+$1.11, +17.23%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Troilus Gold’s most recent drill results at its past-producing Quebec project are discussed in a Stifel GMP report.

In a May 15 research note, Stifel GMP analyst Tyron Breytenbach reported that Troilus Gold Corp.’s (TLG:TSX; CHXMF:OTCQB) new model of the past-producing Troilus gold project in Quebec “uncovered high-grade gold the base metal miners neglected.”

Breytenbach reviewed results of Troilus’ recent drilling there, which “continues to show that the SW Zone has a brittle, high-grade component within the broader bulk volume.” He also noted that “the newly discovered >1 km mineralized trend remains open along strike andat depth.”

The analyst highlighted that the geology of the holes, all of which hit the targeted system, was consistent with that of the main resource area Z87 that is less than 3.5 kilometers to the northeast of the SW Zone.

He also pointed out that SW Zone drilling encountered several high-grade intercepts that were within wider intervals of disseminated gold, which has a geology similar to the main deposit. “We expect that tighter data density will improve the average grade of the resource,” commented Breytenbach.

Returned assays from the SW Zone included 46.4 grams per ton (46.4 g/t) gold equivalent (Au eq) over 1 meter (1m) in hole TLG-ZSW20-190. Other highlight intercepts came in hole LG-ZSW20-181, which showed 13.28 g/t Au eq over 1m within a broader intercept of 1.18 g/t Au eq over 21m, starting 143m downhole.

Hole TLG-ZSW20-186 returned 16.1 g/t Au eq over 1.1m, 1.33 g/t Au eq over 5m and 1.43 g/t Au eq over 5m with the zone starting 156m downhole.

Breytenbach highlighted that the “trajectory of the grade is upwards which, along with the >$500 million worth of inherited infrastructure, will drive a re-rating of the ounces as the current $14.0/oz valuation is an unusually high discount for a Canadian asset.”

Stifel has a Buy rating and a CA$3.40 per share price target on Troilus Gold. The stock is currently trading at about CA$0.97 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Troilus Gold. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Stifel GMP, Troilus Gold, May 15, 2020

Important Disclosures and Certifications Each research analyst and associate research analyst who authored this document and whose name appears herein certifies that: (1) the recommendations and opinions expressed in the research report accurately reflect their personal views about any and all of the securities or issuers discussed herein that are within their coverage universe; and (2) no part of their compensation was, is or will be, directly or indirectly, related to the provision of specific recommendations or views expressed herein.

Company-Specific Disclosures: 1. Stifel Canada or an affiliate has, within the previous 12 months, provided paid investment banking services to the issuer. 2. Stifel or an affiliate act as corporate broker and/or adviser to the Company. 11. Stifel Canada or an affiliate managed or co-managed a public offering of securities for the subject company in the past 12 months.

These results of a study evaluating Targovax’s lead candidate are reviewed and commented on in an H.C. Wainwright & Co. report.

In a June 22 research note, H.C. Wainwright & Co. analyst Joseph Pantginis reported that Targovax ASA’s (TRVX:OSE) ONCOS-102, in trial results, showed efficacy and immunogenicity in malignant pleural mesothelioma (MPM) patients at 12 months post treatment.

ONCOS-102, Targovax’s lead candidate, is an oncolytic adenovirus containing an immune-stimulating transgene. It recently was assessed in the randomized Phase 1/2 trial in combination with standard of care chemotherapy in 31 patients with MPM. In the study, the 20 members of the experimental group received both treatments whereas the 11 in the control group were treated only with standard of care chemotherapy.

Pantginis reviewed the study findings at 12 months and commented, “Given the potent immunogenicity, the data provide a strong rationale for the use of ONCOS-102 to enhance patients’ responses to checkpoint inhibitor regimens and ameliorate outcomes.”

Specifically, the data show that ONCOS-102-treated patients experienced clinical benefits that those in the control group did not experience or experienced to a lesser extent. Those benefits included increased infiltration of cytotoxic T cells in the tumor, upregulation in the expression of genes associated with adaptive immunity and cytotoxicity, polarization of macrophages toward the M1 pro-inflammatory anti-tumor phenotype and increased PD-L1 expression.

The trial results, Pantginis wrote, confirmed the previously reported 8.9 months of median progression-free survival, which compares to 7.6 months among the control group and 5.77.3 months historically for standard of care.

The survival rate among the patients who received the treatment combination was encouraging, at 64%, versus 50% among the control group patients, Pantginis noted.

The study findings also confirmed ONCOS-102’s mechanism of action, which is “enhancing immune responses and modulating the tumor microenvironment and its consequent correlation with positive outcomes,” relayed Pantginis. This suggests that “ONCOS-102 in combination with chemotherapy achieves responses with an extent similar to those obtained with CKI.”

As such, Norway-based Targovax next plans to conduct one or more triple combination studies, testing ONCOS-102 plus standard of care chemotherapy plus a checkpoint inhibitor, in firstline MPM patients.

Pantginis concluded that all of the positive mesothelioma data Targovax has accumulated to date “provide strong rationale for moving mesothelioma forward as first path to market.”

H.C. Wainwright & Co. has a Buy rating and an NOK19 per share price target on Targovax, the stock of which is currently trading at about NOK7.32 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Disclosures from H. C. Wainwright, Targovax ASA, Company Update, June 22, 2020

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placement of securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a company or one of its affiliates or subsidiaries within the past 12 months.

I, Joseph Pantginis, Ph.D., certify that 1) all of the views expressed in this report accurately reflect my personal views about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor any members of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analyst’s household has a financial interest in the securities of Targovax ASA (including, without limitation, any option, right, warrant, future, long or short position).

As of May 31, 2020 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securities of Targovax ASA.

Neither the research analyst nor the Firm has any material conflict of interest in of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon any specific investment banking services or transaction but is compensated based on factors including total revenue and profitability of the Firm, a substantial portion of which is derived from investment banking services.

The Firm or its affiliates did not receive compensation from Targovax ASA for investment banking services within twelve months before, but will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

The Firm does not make a market in Targovax ASA as of the date of this research report.

H.C. Wainwright & Co., LLC and its affiliates, officers, directors, and employees, excluding its analysts, will from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives (including options and warrants) thereof of covered companies referred to in this research report.

Pakistan’s central bank cut its key interest rate for the fifth time this year and for the third month in a row, saying this decision reflects a further improvement in the outlook for inflation while the slowdown of the country’s economy continues and downside risks to growth have risen. The State Bank of Pakistan (SBP) cut its policy rate by another 100 basis points to 7.0 percent and has now cut it by 625 points this year following previous cuts in March, April and May. Noting its mandate to support households and businesses through the Covid-19 pandemic and to minimize the damage to the economy, SBP’s monetary policy committee said after a surprise meeting that from a risk management point of view “a prompt response to downside risks to growth was called for given the improved inflation outlook.” The central bank added that some 3.3 trillion rupees of loans were due to be repriced by early July, making this an opportune moment to take action as the benefits of interest rate reductions would be passed on to households and businesses in a timely manner. Pakistan’s inflation rate eased to 8.22 percent in May from 8.5 percent in April and 14.6 percent in January due to the government’s cut in diesel and petrol prices and SBP said data shows this moderation was continuing in June despite a rise in some food prices, such as wheat. While supply shocks could trigger some volatility in inflation, SBP said this was likely to be transitory given the weak demand and given the absence of any demand-side pressures, average inflation could fall below the previously expected range of 7-9 percent in fiscal 2020/21, which begins July 1. In May SBP also forecast inflation for the current fiscal year to be close to the low end of its expected range of 11-12 percent. “With the current reduction in the policy rate to 7 percent, the MPC felt that real rates on a forward-looking basis (defined as the policy rate less expected inflation) would be kept close to zero, which is appropriate under the current circumstances,” SBP said. High-frequency data, such as cement dispatches, automobile sales, food and textile exports, and petroleum sales were continuing to contract in April though the rate was lower than in the previous two months and looking ahead SBP expects a gradual recovery in the fiscal 2021 although risks are still skewed to the downside and dependent on the evolution of the pandemic. Pakistan’s rupee, which had stabilized in June last year after an agreement with the International Monetary Fund (IMF), fell sharply in March but then recovered in April. But since late May the rupee has again been falling and was trading at 167.4 to the U.S. dollar today, down 7.5 percent this year. SPB said the flexible exchange rate had played “its valuable shock absorber role,” helping cushion the economy from any tightening of financial conditions from capital outflows and deteriorating global sentiment, adding the rupee’s depreciation had been lower than in many other emerging markets, reflecting the increased reserve buffers accumulated over the last year.

The State Bank of Pakistan issued the following statement:

1. At its meeting on 25th June 2020, the Monetary Policy Committee (MPC) decided to reduce the policy rate by 100 basis points to 7 percent. This decision reflected the MPC’s view that the inflation outlook has improved further, while the domestic economic slowdown continues and downside risks to growth have increased. Against this backdrop of receding demand-side inflation risks, the priority of monetary policy has appropriately shifted toward supporting growth and employment during these challenging times. 2. Consistent with its mandate, the MPC re-asserted its commitment to supporting households and businesses through the Covid-19 crisis and minimizing damage to the economy. In this context, the MPC felt that from a risk management point of view, a prompt response to downside risks to growth was called for given the improved inflation outlook. In addition, the MPC noted that with approximately Rs. 3.3 trillion worth of loans due to be repriced by early July 2020, this was an opportune moment to take action from a monetary policy transmission perspective. In this way, the benefits of interest rate reductions would be passed on in a timely manner to households and businesses. 3. The MPC noted that the Covid-19 pandemic is spreading in many emerging markets, including Pakistan, and there are fears of a second wave in several other countries. The MPC observed that risks to the global outlook are heavily skewed to the downside and the path of recovery remains uncertain. The MPC also noted that in its update of the World Economic Outlook (WEO) released yesterday, the IMF downgraded its 2020 global growth forecast further to -4.9 percent, 1.9 percentage points lower than in April, and projected a more gradual recovery than previously anticipated. 4. Domestically, the moderation of underlying inflation has continued. Notwithstanding a seasonal uptick in food prices associated with the Eid holiday, headline inflation declined further to 8.2 percent in May on the back of the recent cut in diesel and petrol prices. In addition, month-on-month inflation rates continue to be low. Recent SPI data also suggests continued moderation in overall price pressures in June, despite price increases in some food items, notably wheat. The FY2020/21 budget is also expected to be neutral for inflation as the freeze on government salaries, absence of new taxes, and lower production cost from reduced import duties should offset the decline in subsidies in some sectors. While supply shocks could create some volatility in inflation, the MPC felt that these are likely to be transitory given weak domestic demand, such that monetary policy should generally look past them. Given the absence of demand-side pressures, average inflation could fall below the previously announced range of 7-9 percent for next fiscal year. With the current reduction of the policy rate to 7 percent, the MPC felt that real rates on a forward-looking basis (defined as the policy rate less expected inflation) would be kept close to zero, which is appropriate under the current circumstances. 5. On the real side, the decline in LSM deepened to 41.9 percent (y/y) in April, when lockdowns were still in place. In May, high-frequency indicators of activity such as cement dispatches, automobile sales, food and textile exports, and POL sales also continued to contract, although mostly at a lower rate than in the previous two months. Looking ahead, the economy is expected to recover gradually in FY21, supported by easing lockdowns, supportive macroeconomic policies and a pick-up in global growth. However, risks are skewed to the downside and the recovery will depend critically on the evolution of the pandemic both in Pakistan and abroad.

6. On the external front, the current account swung into surplus in May on the back of a reduction in the trade deficit and a pick-up in remittances compared to the previous month. Meanwhile, portfolio outflows slowed considerably compared to the previous two months and FDI has been resilient, nearly doubling to $2.4 billion so far in FY20 compared to the same period last year. SBP reserves declined to US$ 9.96 billion as of 19th June 2020 largely due to debt repayments. However, since then, SBP has received fresh disbursements from multilateral agencies including around $725 million from World Bank and $500 million from ADB, and another $500 million is expected shortly from the Asian Infrastructure Investment Bank (AIIB). 7. During this period of external volatility, the MPC observed that the flexible exchange rate has played its valuable shock absorber role, helping cushion the economy from the tightening of financial conditions associated with capital outflows from emerging markets and deteriorating global sentiment. The MPC noted that the depreciation in the rupee has been lower than in many other emerging markets, reflecting the increased reserve buffers accumulated over the last year. The outlook for the external sector remains stable. Recent data confirms the view that the current account deficit should remain bounded through the Covid-19 crisis due to lower oil prices. In addition, projected official and private inflows are expected to keep the external position fully funded. 8. Today’s decision brings the cumulative reduction in the policy rate since mid-March to 625 basis points, commensurate with the decline in inflation during this period. The MPC noted that the take-up of several other SBP initiatives has risen significantly in recent weeks, notably concessional refinancing facilities to protect employment and support the health sector as well as regulatory measures to provide debt servicing relief. Together, this strong and data-driven monetary policy response should support growth and employment, while keeping inflation expectations anchored and maintaining financial stability.” www.CentralBankNews.info