The upward movement is observed when gold rises in price and the S&P500 stock index decreases. In the USA, there is an increase in coronavirus cases, which may have a negative impact on the economy and stock prices. However, gold may be in demand as a protective asset. Several US states (Alabama, California, Idaho, Mississippi, Missouri, Nevada, Oklahoma, South Carolina, and Wyoming) announced a record increase in Covid-19 cases last week. Texas and Florida have restored a number of quarantine measures. There are currently 2.5 million people in the United States who have contracted the disease. Of these, 127,000 have already died and 700,000 have recovered (i.e. since the epidemic began). In the European Union, there are 750,000 patients with coronavirus, of whom 61,000 died. According to the World Health Organization (WHO), this week the number of Covid-19 patients worldwide will reach 10 million, and the number of deaths – 500 thousand. Probably, the quotes of this gold instrument may depend on information on the development of the situation with the coronavirus pandemic in the world and in the USA.

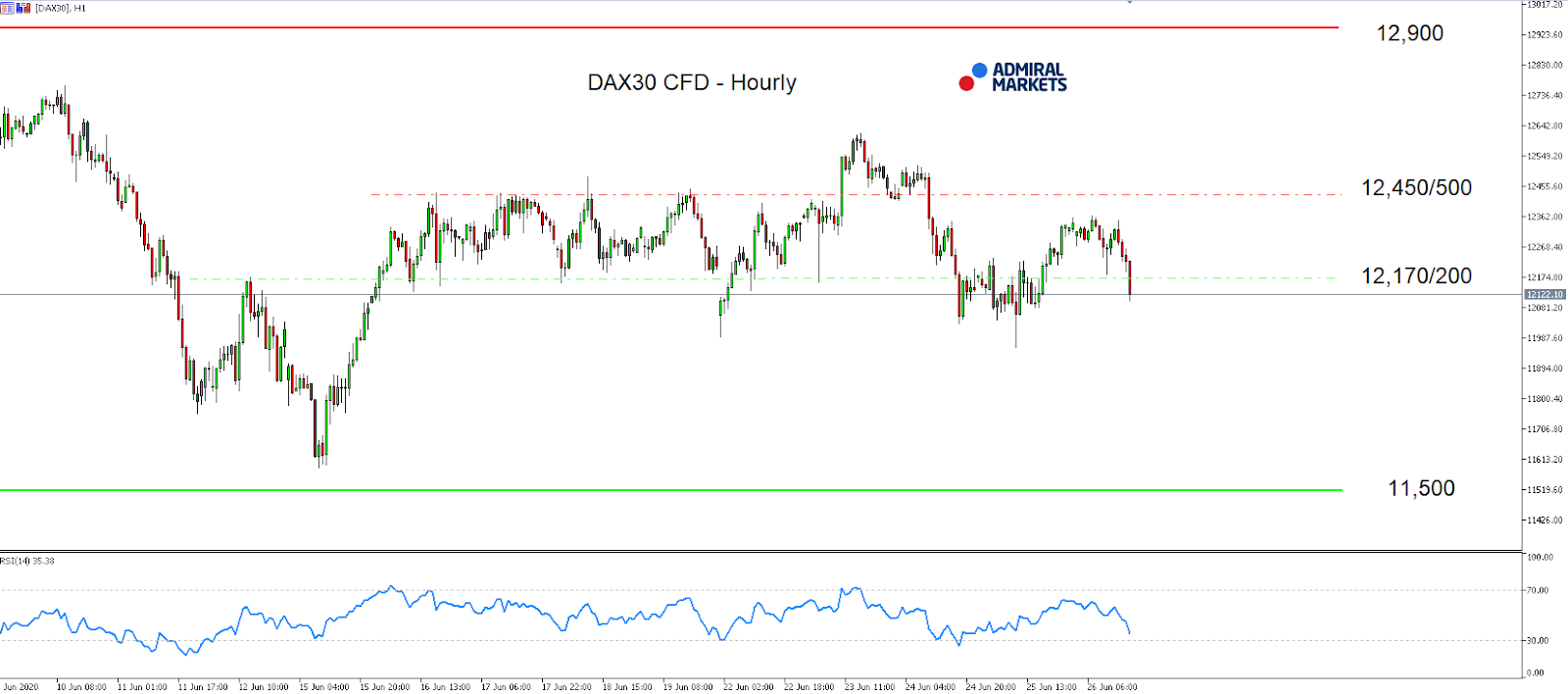

After the weak start into last Thursday with the break below 12,000 points, it looked as if the German index could suffer further losses and drop even further into the quarterly close.

This came after speculations arose that some asset allocators, like pension funds, could take the big gains from the stock market in Q2/2020 and move them into bonds, as Wells Fargo estimates that the rebalance into bonds could be the largest in six years.

But instead, bulls recaptured quickly control and with US equities and here the S&P500 seeing the biggest last hour gain Thursday evening, the DAX not only pushed back above 12,000 points, but also above 12,200 points into its consolidation zone.

While it certainly needs to be seen whether Thursday’s move is sustainable, chances of another stint up to 12,600 points, the pre-weekly highs, and a break higher activating the region around 12,900 points, is definitely on the table after the stable performance of the DAX on Friday.

On the other hand: if we get to see a break below 12,000 points, the technical main focus will be on the region around 11,800 points, a break lower makes a deeper correction possible and could see a re-test of the region around 11,450/500.

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Hourly chart (between June 9, 2020, to June 26, 2020). Accessed: June 26, 2020, at 10:00pm GMT

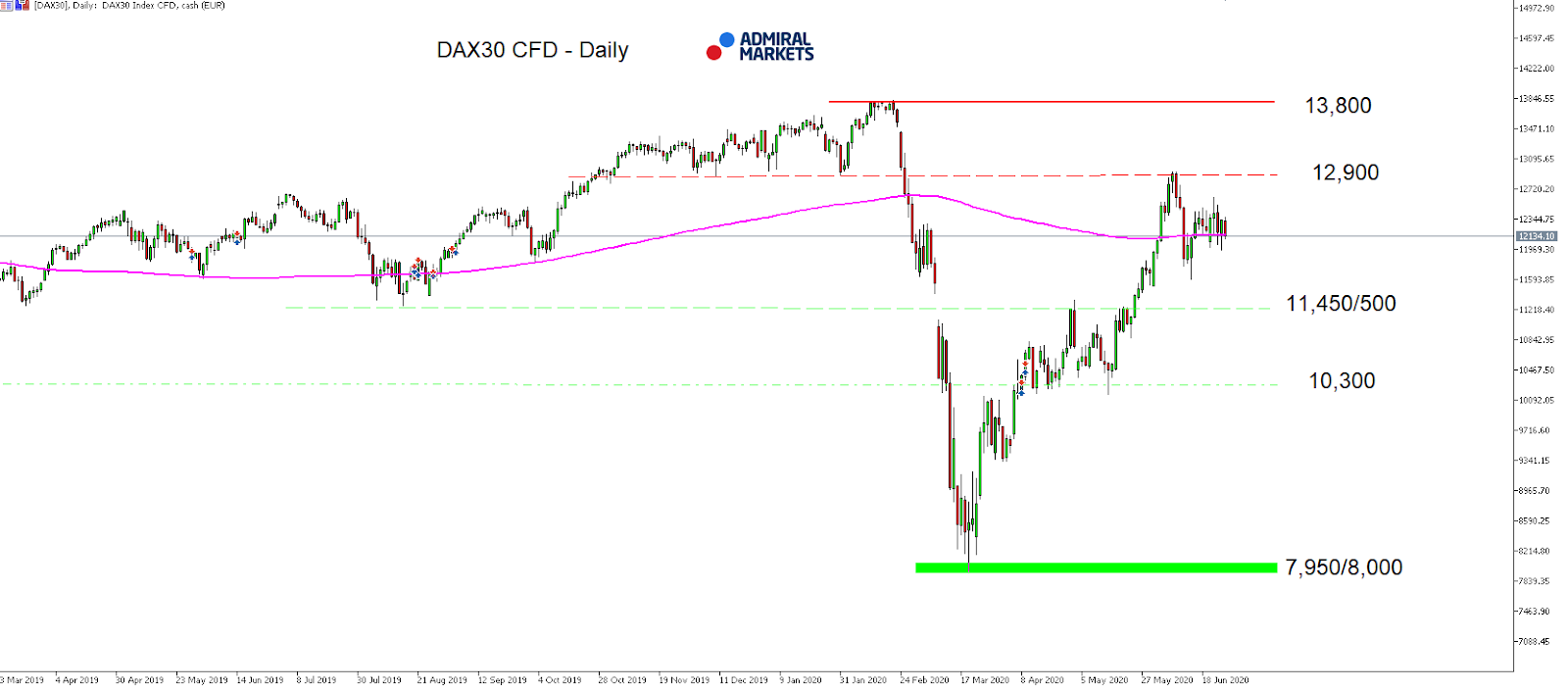

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Daily chart (between March 13, 2019, to June 26, 2020). Accessed: June 26, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of the DAX30 CFD increased by 9.56%, in 2016, it increased by 6.87%, in 2017, it increased by 12.51%, in 2018, it fell by 18.26%, in 2019, it increased by 26.44% meaning that after five years, it was up by 34.2%.

Check out Admiral Markets’ most competitive conditions on the DAX30 CFD and start trading on the DAX30 CFD with a low 0.8 point spread offering during the main Xetra trading hours!

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

“Coronavirus deaths topped 500,000 worldwide”, is the first headline to grab investors’ attention this morning. The mission is unaccomplished and the virus is still winning the fight in several countries, particularly in the US, Brazil and India.

Hopes of a robust economic recovery following the pandemic are now shattered. The risks of re-imposing lockdowns are high, and monetary policy stimulus which explains most of the recovery in asset prices from the March lows will become less effective going forward if it doesn’t translate into a rebound in economic activity and better prospects for corporate earnings. Risk asset valuations remain elevated and the next few weeks ahead will tell us whether they will continue to hold or get bumped.

At this stage, there is a lack of visibility as even technical indicators share a similar view. The S&P 500 closed Friday 11 points below its 200-day moving average and is just hovering around the psychological 3,000 level. If the index trades for two to three days below these two benchmarks, that will attract more sellers and could drive the index 5 – 10% lower from current levels. However, holding above may have the opposite impact but that will lead to a further divergence from fundamentals, which in theory should not hold for long unless the Administration provides new fiscal stimulus plans.

The divergence is not just among asset prices and fundamentals, but also within assets themselves. US 10-year and 30-year treasury yields are sitting at one-month lows of 1.37% and 0.64% respectively, indicating there’s still huge demand for the safety of US government bonds. If yields on long term maturities continue to head lower that should mean the big players are reducing their risk exposure heading into the third quarter.

While the trajectory of the Covid-19 infections and deaths remains the most effective barometer for risk, investors need to keep an eye on several other factors this week.

The US job’s report will be released on Thursday instead of Friday due to the Independence Day holiday. Markets anticipate the headline figure will add three million jobs in June following 2.5 million added in May. Given the volatility in the employment data, we may see another surprise although a positive one is needed to prove that economic activity is gathering pace. Investors will also be focusing on Fed Chairman Jerome Powell when he testifies before the House Financial Service Committee tomorrow for any hints on new monetary policy measures, while also needing to closely scrutinize the FOMC minutes on Wednesday.

Longer-term, market participants need to keep an eye on US election polls. So far Joe Biden is leading by a significant margin and that doesn’t seem to be priced in yet. Biden made it clear that he will roll back Trump’s corporate tax reforms, and that requires substantial revisions for earnings expectations in 2021. If he continues to lead in the polls, expect a further pull back in stocks.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Global equities are in red currently after a risk off trading last week. Investors’ risk appetite appears in short supply after reports of rising coronavirus cases globally emboldened bears who drove US stock indexes to their lowest levels in about two weeks.

Forex news

Currency Pair

Change

EUR USD

-0.82%

GBP USD

+0.74%

USD JPY

-0.01%

The Dollar strengthening has reversed currently. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, gained 0.04% Friday as consumer spending climbed in May to a record 8.2% after tumbling in April while personal incomes sank 4.2% last month. GBP/USD continued falling Friday while EUR/USD reversed its sliding despite report German import prices recovery was slower than anticipated in May. Both pairs are up currently. Both AUD/USD and USD/JPY reversed their sliding on Friday with both pairs lower currently.

Stock Market news

Indices

Change

Dow Jones Index

+0.31%

GB 100 Index

-0.11%

Nikkei Index

-2.38%

Hang Seng Index

-1.01%

US equity markets are edging higher today after ending sharply lower on Friday led by financial shares as Federal Reserve suspended share repurchases and cap dividend payments for banks in the third quarter following results of annual bank stress tests. The three main US stock indexes recorded daily losses ranging from 2.4% to 2.8% as Texas and Florida postponed reopening their economies on rise of new coronavirus cases. European stock indexes are rebounding currently after ending lower on Friday despite European Central Bank President Lagarde’s comment the euro zone is “probably past” the worst of the economic crisis caused by the outbreak. Asian indexes are in the red today led by Nikkei .

Commodity Market news

Commodities

Change

Brent Crude Oil

-0.68%

WTI Crude

-0.85%

Brent is edging higher today. Oil prices ended lower last session as Baker Hughes reported a decline of just 1 in weekly US oil-rig count to 188. The US oil benchmark West Texas Intermediate (WTI) futures ended marginally lower Friday: July WTI slid 0.6% and is lower currently. August Brent crude slipped 0.1% to $41.02 a barrel on Friday.

Gold Market News

Metals

Change

Gold

-0.43%

Gold prices are pulling back today. August gold rose 0.6% to $1780.30 an ounce on Friday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

US stocks are set to pare some of Friday’s declines, with futures edging into positive territory at the start of the week. Asian stocks are however lower at the time of writing, despite China’s May industrial profits posting a positive surprise with a six percent year-on-year growth.

Fears over the global coronavirus pandemic are retaining their place as the primary driver of global market sentiment. Over the weekend, the number of cases worldwide exceeded 10 million, with the death toll now more than 500,000.

The figures call into question the optimism that has been priced into global stocks, which had seen a stunning surge since March. Yet amid such doubts, S&P 500 minis are attempting to break back above its 200-day simple moving average, or risk sinking back into the sub-3000 domain.

With the average number of cases per day standing at 150,000 as of mid-June, such alarming figures are denting optimism that the worst of the pandemic is over. Concerns are now mounting that the US economic recovery will prove to be a longer-than-expected slog, with some US states reversing their respective reopening plans.

Any further stumbles in America’s quest to overcome the pandemic could chip away at the gains seen in equities over recent months. Another violent capitulation in equities cannot yet be ruled out, more so if the global pandemic takes a sharp turn for the worse and markets swiftly adopt a risk-averse stance. Global investors would do well to tread carefully amid such uncertain times, especially seeing that the upward momentum in risk assets has waned and near-term gains are not guaranteed.

Brexit negotiations could sway Sterling

The Pound is coming face-to-face with a familiar foe once more, as Brexit negotiations resume this week. Over the weekend, UK Prime Minister Boris Johnson reiterated his willingness to walk away from the negotiations if insufficient progress is made on reaching an agreement.

Four years since the referendum, and the currency still cannot shake off the woes that have accompanied the UK’s plans to leave the European Union. Having already tumbled by nearly 17 percent since the Brexit referendum on 23 June 2016, GBPUSD could carve a path back towards the psychologically-important 1.20 level, if investors get the sense that it is likelier that the UK will leave the EU without a deal.

Pound traders are expecting a pickup in volatility as talks intensify over the next few weeks, leaving the currency susceptible to Brexit-related woes throughout the second half of the year in the absence of a trade deal. Such concerns would only compound fears over the UK’s pandemic response as well as the prospects of the BOE adopting negative interest rates, with all the mentioned factors potentially combining to exert sustained downward pressure on Sterling.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

This week – June 28 through July 4 – central banks from 6 countries or jurisdictions are scheduled to decide on monetary policy: Kyrgyz Republic, Jamaica, Bulgaria, Colombia, Sweden and Albania.

Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.

– Many months ago, our research team suggested any future collapse in the global markets would likely prompt a global capital shift in how capital identifies and is deployed for ROI. We’ve continued to suggest that the more mature, global economies will become beneficiaries of any massive global collapse event and that capital will actively seek out security and safety while attempt to attain moderate returns. We suggest reading this past research post on global central banks moves to keep the party rolling.

In 2019, we predicted a major Super-Cycle event would take place on or near August 19, 2019. We believed this event would prompt a major downside price rotation that would prompt a shift in how capital is deployed throughout the world’s financial markets. At that time, and still, we believe a long-term price cycle event is taking place which will prompt a deeper price bottom event that will likely complete near August or September 2020. This raises an interesting setup related to Technical Analysis for skilled traders…

If our analysis is correct, the Q2 and Q3 global economic data will be very distressing and likely prompt a continued downside price contraction in stock price levels and valuations. The disruption to the global economy has likely shaved 5% to 15% (or more) off total global GDP output for this year. Still, the US Fed and global central banks have poured more and more capital into the markets attempting to front-run this contraction in the global markets. We believe this “reprieve” in selling is likely temporary right now. The broader, longer-term, price cycle we’ve identified it still taking place and will likely prompt a deeper price bottom in the global markets before the end of 2020.

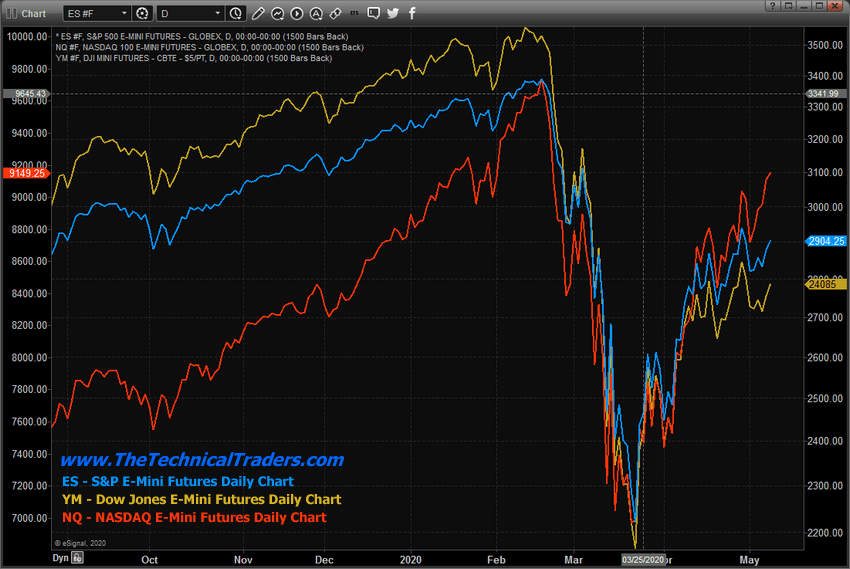

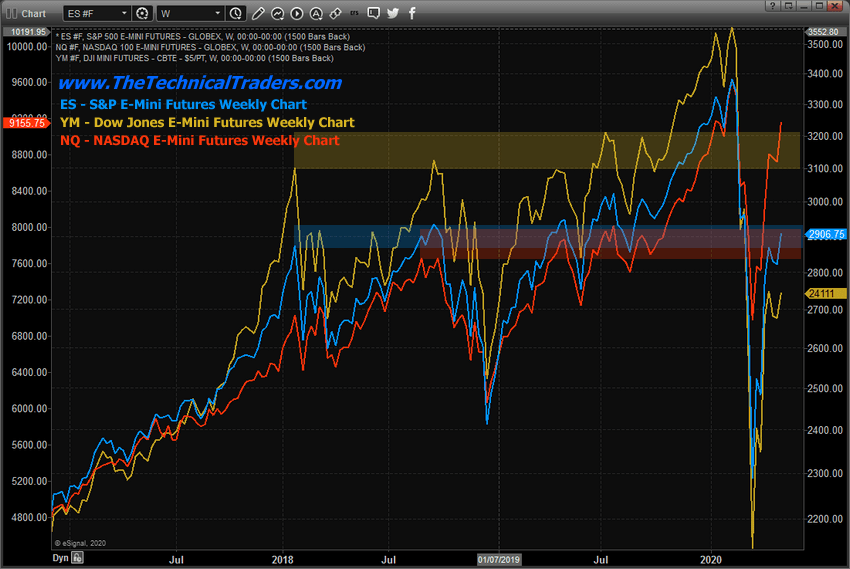

The one aspect of recent buying that we find rather interesting is that the NASDAQ (NQ) is really the only US market sector that is outperforming all the other sectors. This suggests that the US and global investors are piling into technology, biotech, and other NASDAQ symbols expecting these segments of the US economy to outperform the others. This is one component of the “capital shift” we have been warning investors about.

When the crisis event begins to unfold, capital (cash) will seek out and identify various opportunities as global markets and regional market segments shift from overvalued to undervalued – from risk to opportunity. We believe this is happening right now in the NASDAQ (NQ) and we believe the opportunity investors have piled into recently may turn into renewed risk in the near future as Q2 and Q3 economic data pushes reality into the markets.

Daily Comparison Chart shows the ES, YM, and NQ

This Daily Comparison Chart shows the ES, YM, and NQ in Log scale and highlights the collapse event for all three major indexes (almost in unison) as well as the incredible upside price rally in the NQ (RED) compared to the ES and YM. It is fairly easy to see how the NQ (RED Line) rallied over the past 30+ days much more efficiently than the ES and YM levels. As skilled traders were seeking opportunity, they identified the NQ as the best opportunity to deploy their capital.

Yet, if our analysis is correct and a deeper price low will be necessary to complete the broader price cycle setup that is taking place, this also means the recent opportunity in the NQ may turn into excessive risk if the markets suddenly turn downward – targeting our predicted deeper price bottom.

Weekly Comparison Chart shows the ES, YM, and NQ

This Weekly Comparison Chart shows the same three US major indexes and highlights previous price high levels which acted as resistance in the past. Both the ES and YM are currently trading below these resistance levels. The NQ is trading well above the resistance level (red). This continues to suggest that skilled traders have piled into the NQ rally expecting it to continue to outperform the S&P and Dow Jones in the future.

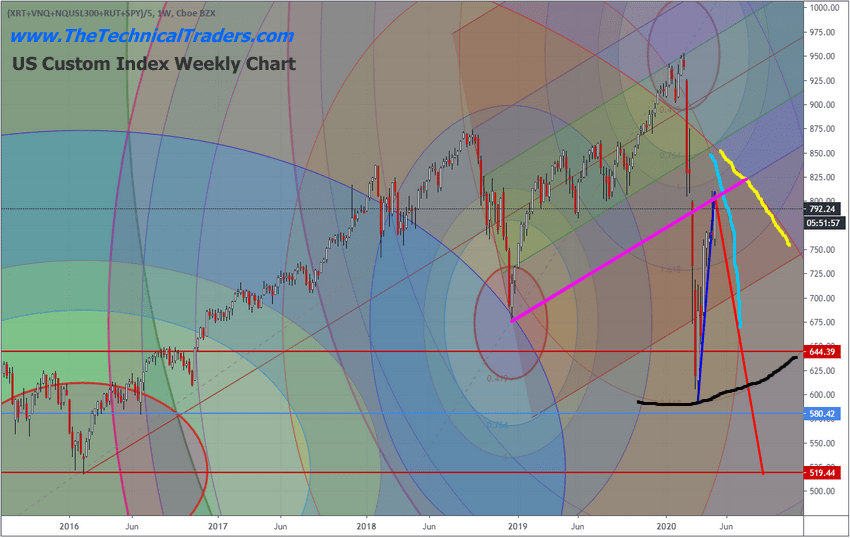

Weekly Custom US Index Chart

This Weekly Custom US Index chart helps to paint a very clear picture of the price trend and support/resistance levels that are active within the markets. In this chart, you’ll see many aspects of advanced technical analysis that helps us to determine where and when certain types of price action may take place. One of our tools is the Fibonacci Price Amplitude Arc technique – which attempts to deploy the Fibonacci price theory based on a price trend frequency/amplitude basis. This means each major and minor price trend (up or down) generates its own frequency/amplitude levels which project out in the past/future as key trigger levels for future price setups (tops/bottoms/rotations). We’ve also drawn a Std. Deviation Pitchfork across the 2018 top and bottom to highlight 1.0 and 2.0 Std. Deviation ranges related to current price peaks and bottoms.

As you can probably see from the chart, the deep lows in 2020 touched a broad Fibonacci Price Amplitude Arc registering a 2.618 expansion (highlighted in BLACK). Price has, subsequently, rallied back to the 1.0 StdDev lower price range on the Pitchfork. Additionally, there is a very important resistance price Arc that is setting up from the December 2018 price lows (highlighted in CYAN). Lastly, another major price resistance Arc originating from the 2016 lows aligns very closely with current price levels (highlighted in YELLOW).

Our researchers have identified a price inflection date trigger somewhere between May 8th and May 12th which we believe will prompt the start of a new trend or trend reversal trigger. We believe this inflection point suggests a bigger move will initiate near or shortly after this inflection point date. These types of inflection points typically result in larger volatility and/or broad price trend moves as they represent price breaking through resistance, support, or some major barrier in price. The energy it takes to break through these barriers translates into increased volatility and bigger price moves typically.

Currently, because of the technical setups we see that are about to trigger, we are very cautious in terms of taking unwanted risks in the markets related to trades. These inflection points could prompt a very big upside or downside price move within the next 5+ days and even though we believe the markets will attempt to move lower in a process that completes the deeper downside bottom formation, a “washout high” price rotation may occur as price reaches and breaches this inflection point.

In our view, it is better to wait for the market to confirm trends once this inflection point is processed to determine where the next opportunity for any new trade will present itself. As we’ve tried to highlight within this article, even though the NQ appears to be rallying back to near all-time highs, the major markets have set up a completely different set of technical analysis outcomes that suggest Q2 and Q3 weakness will likely prompt a deeper bottom pattern in the future.

The one thing we are certain of is that capital has already entered the “capital shift” process we have been suggesting over the past 24+ months. Capital will continue to roll into and out of various US and global market segments seeking safety, returns, and opportunity while attempting to avoid risks. We feel the US markets are very close to another topping event based on our research and believe waiting for clarity right now is the best decision skilled traders can make. One way or another, the market will tell us what to expect after breaking past this inflection point.

This is the start of a significant turning point for stocks and safe havens this week. Enormous patterns have been formed.

I love what is happening in the markets for the last few weeks. We want a big bounce and all the bullish emotions that come with it because it will set us up with a substantial long term investment position once price confirms this next entry signal.

If you are using our free public research for your own trading decision-making and/or using it as an opportunity to find and execute successful trades, please remember you are the one ultimately making the decisions to trade based on our interpretation and free research posts. We, as technical traders, will continue to post new research articles and content that we believe is relevant to the current market setups.

If you want to improve your accuracy and opportunities for success, then we urge you to visit TheTechnicalTraders.com to learn how you can enjoy our research and our members-only trading triggers (see the first chart in this article). If you are managing your retirement account or 401k, then we urge you to visit www.TheTechnicalInvestor.com to learn how to protect your assets and grow your wealth using our proprietary longer-term modeling systems. Our goal is to help you find and create success – not to confuse you.

Our researchers will generate free research on just about any topic that interests them. As technical traders, we follow price, predict future price moves, tops, bottoms, and trends, and attempt to highlight incredible setups that exist on the charts. What you do with it is up to you. Visit TheTechnicalTraders.com to review all of our detailed free research posts.

In closing, we would like to suggest that the next 5+ years are going to be incredible opportunities for skilled traders. Remember, we’ve already mapped out price trends 10+ years into the future that we expect based on our advanced predictive modeling tools. If our analysis is correct, skilled traders will be able to make a small fortune trading these trends and Metals will skyrocket. The only way you’ll know which trades to take or not is to become a member.

Chris Vermeulen Chief Market Strategist Founder of Technical Traders Ltd.

A Cormark Securities report highlights that recent exploration by Troilus Gold yields one of the best holes ever drilled on the property.

In an April 22 research note, Cormark Securities analyst Richard Gray reported that Troilus Gold Corp.’s (TLG:TSX; CHXMF:OTCQB) “Southwest zone is starting to bring the heat,” and the company recently drilled one of the best holes ever on the property.

The Southwest zone is part of its Troilus gold project in Quebec and is located about 3.5 kilometers (3.5 km) from the main mineralized zone at Z87. Southwest and the main mineralized zone share similar geology.

Gray relayed that the highlight hole, TLG-ZSW20-189, drilled in Troilus’ Southwest zone, returned 2.05 grams per ton (2.05 g/t) gold equivalent (Au eq) over 48 meters (48m) within a larger intercept of 1.56 g/t Au eq over 73m. The grade is more than double the average grade of the existing resource of 0.95 g/t Au eq.

Results of another highlighted hole that Troilus reported along with this one, TLG-ZSW20-185, showed 1.02 g/t Au eq over 15m.

“These drill results further demonstrate the potential of the Southwest zone to add to the current mineral inventory of 6,470,000 ounces of Au eq at the Troilus project,” Gray noted.

Currently, Southwest, defined by the Main and West zones, extends for 1 km along strike and ranges from 1070m in width. An initial resource estimate for Troilus is expected later this year.

“Troilus could be a breakout explorer name in 2020,” Gray stated.

“The project has the size and scope to garner a significant re-rating as the company achieves further de-risking catalysts over the next 12-18 months, or become an attractive acquisition target for senior and midtier producers looking for large and undervalued resources in what is one of the safest jurisdictions in the world,” Gray concluded.

Cormark has a Buy recommendation and a CA$3.65 per share target price on Troilus Gold. The stock is trading now at about CA$0.98 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Troilus Gold. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Cormark Securities, Troilus Gold Corp., Morning Meeting Notes, April 22, 2020

Analyst Certification: We, Richard Gray and Nicolas Dion, hereby certify that the views expressed in this research report accurately reflect our personal views about the subject company(ies) and its (their) securities. We also certify that we have not been, and will not be receiving direct or indirect compensation in exchange for expressing the specific recommendation(s) in this report.

The Disclosure Statement Chart for Troilus Gold can be found on the website.

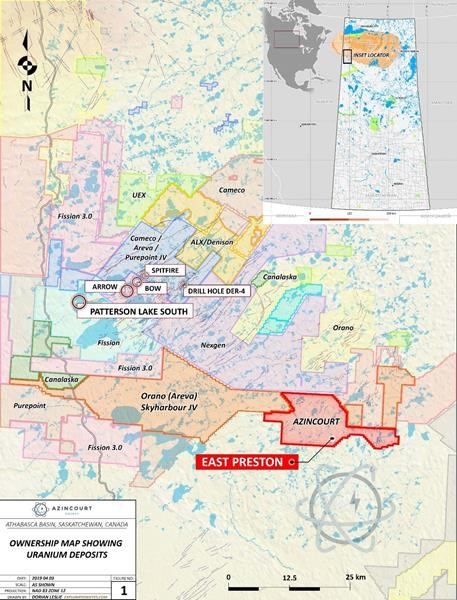

East Preston is located in the western part of the Athabasca Basin, one of the world’s highest-grade uranium regions, and counts among its neighbors NexGen Energy’s Arrow deposit, Fission Uranium’s Triple R deposit and AREVA-Cameco-Purepoint’s joint venture, Spitfire.

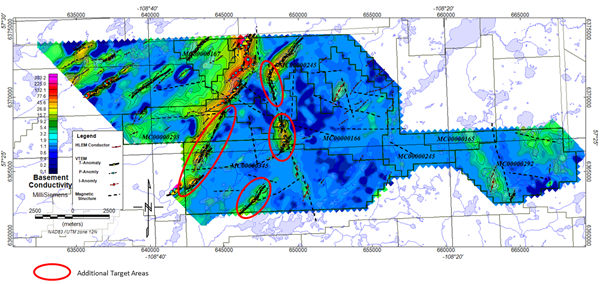

Drilling at East Preston takes place over the winter because it’s much easier to punch holes into the swampy terrain when it’s frozen, and the company recently announced results from this past winter’s 2,431-meter, nine-hole drill program. While the project totals more than 25,000 hectares, the drilling tested three areas in a 7 km by 2 km portion.

“We are very encouraged with the results from the 2020 winter drill program at East Preston,” said Ted O’Connor, Azincourt director and technical advisor for East Preston. “We continue to see the right basement unconformity uranium settingrocks, structure and alterationfrom drilling on the project.” O’Connor has more than 27 years of experience in the uranium-lithium industry, including 20 years with Cameco Corp., focused on acquisitions, new projects and strategic alliances.

O’Connor discussed the East Preston project’s geology. “The helicopter surveys that we did, followed up by ground geophysical surveys, got us into these long linear corridors of conductive rocks and that’s a first order criteria. Then we look at what else is going on over those corridors. Are there breaks in them that suggest it could be structural disruption or fault zones? We have no sandstone cover on this project because it’s right at the southern edge of the Athabasca Basin. We have uncovered this rare earth element enrichment that could be related to uranium mineralizing processes right in those conductive fault zones, and they’re all faults that have been reactivated at what we think is the right timing for uranium mineralization” O’Connor told Streetwise Reports.

“Drilling continues to show us we are on the right track at East Preston,” said Azincourt President and CEO Alex Klenman. The presence of rare earth element mineralization, potentially similar to Denison Mines’ Wheeler River uranium project, adds to the growing prospectivity of the project. This data is a positive development that demonstrates East Preston continues to reveal it has the necessary environment for uranium deposition.”

“My interpretation of this rare earth element mineralization is that this could be a basement expression of REE mineralization similar to that observed in sandstone-hosted systems associated with unconformity uranium deposits on the Wheeler River projectbut we’re in the basement rocks below the Athabasca sandstone,” O’Connor explained.

O’Connor delved into the geology of the area. “We have essentially two end members of the uranium deposits in the Athabasca Basin and variations in between. If you look at the uranium deposits that are in the sandstone, at the unconformitythe place where the sandstone and the basement rock meetor just above the unconformity, they tend to be what we call complex; they’re different. They often have cobalt and arsenic and nickel associated with the uranium mineralization.”

“The uranium deposits that are in the basement rocks are different, and they are called simple,” O’Connor continued. They are mostly uranium only with a few other, but different, elements. And so I’m looking at this rare earth element enrichment in these fault zones within these correct graphitic rocks and structures and my interpretation is it’s a basement analog. It’s mineralogically, and elementally chemically different, but it’s the same system style.”

“We think at the right time, the sandstone was there when the fault zone mineralization was introduced. What makes that significant is at the MAW Zone at Denison’s Wheeler River Project on the eastern Athabasca, 5 kilometers from the Phoenix uranium deposit, in the sandstone there’s uranium mineralization all around it associated to the same conductive trends, just with slightly different fluid chemistries at the mineralizing time. The MAW Zone being surrounded by multiple uranium mineralized zones and uranium deposits along strike and along sub-parallel graphitic-structural corridors is similar to the East Preston basement litho-tectonic setting,” O’Connor explained.”

“I believe it’s another piece of the puzzle that says not only do we have the right rocks, but also there’s actually been some post-sandstone mineralizing fluid systems going on in the right rocks,” he said. “We have the exact same rocks we had in the first year of drilling. And they are the right rocks that are known to host deposits further west in at Fission’s Triple R deposit and NextGen’s Arrow deposit.”

“So the rocks are right, the structures right and we have now we think we have evidence of mineralizing fluid systems,” O’Connor explained.

Jordan Trimble, CEO of Skyharbour Resources, noted, “If you look at the discoveries made in the last 20 to 30 years in the Athabasca Basin and the deposits, some of which are now being mined, there’s been a paradigm shift, particularly in the last decade or so, with sandstone versus basement hosted deposits; a lot more exploration is being carried out deeper into the basement rock or outside of the Basin margin. That was a big part of the discovery of the entire western side of the Basin with the high-grade boulders for Fission and looking at an area that was overlooked because it was outside or on the margin of the sandstone cover.”

“That’s what this project is,” Trimble continued. It’s south of the Basin margin. But there’s no reason that you can’t have major deposits that are in these basement rocks. As they are finding here at East Preston, if you are finding the right indicator minerals, the right structures, having a reactivation event and older rocks is key; you are finding all the right smoke.”

“This is a property that doesn’t have hundreds of thousands of meters drilled on it. This is an exploration property,” Trimble stressed. “And this was really the first meaningful drill program carried out on the project. There’s a little bit of drilling that was done back in 20142015, but not a lot. And then this was the first larger program carried out by Azincourt. So the fact that they’re finding what they’re finding with only a few thousand meters drilled is important, and additional exploration and drilling is going to continue to vector in on what we all believe to be a larger deposit sitting on the project.”

Looking ahead, O’Connor said, “Later this summer and into the fall, we are planning to conduct ground gravity and electromagnetic geophysics, in this case, probably a Horizontal Loop Electromagnetic (HLEM) survey. We previously conducted a property-wide helicopter airborne survey that basically got us these corridors. The idea is to go in on the ground, cut some lines, run these geophysical surveys overtop of them to essentially refine these corridors and see if are there one or two conductors side by side and more exactly locate them on the ground.”

Azincourt is also looking at gravity geophysics because “minute differences in gravity response over the rocks over the surface can tell you things like where there might be structural disruption, where there might be alteration and it’s another layer of information that could tell you if one part of the conductor is better than another,” O’Connor explained.

Of the 25,000 hectare property, the 7 km long area that has seen some drilling represents only about a quarter of the strike lengths. “There’s at least 20+ kilometers of conductive strike corridors on the project, and we’ve conducted initial tests on at the most about two areas out of seven,” O’Connor said.

“The project is certainly target rich and we’re just beginning to scratch those targets,” Azincourt CEO Klenman said. “It’s early in the game. The more data that we can glean, the more targets present themselves.”

Azincourt expects to meet the spend threshold of the joint venture agreement by the end of summer. After that there is a one-time CA$400,000 payment that is due by March 2021 to complete the 70% earn-in. After that, the project reverts to a joint venture, with each party paying a pro-rata share of the expenses.

In addition to East Preston, Azincourt holds the Escalera projects in Peru: the Lituania, Condorlit and Escalera concessions total 7,400 hectares. Rock grab sampling at the property in 2018 yielded assays as high as 8,061 ppm uranium (0.95% U3O8). The company plans to follow up when conditions allow.

Azincourt’s CEO, Alex Klenman, also serves as CEO of Nexus Gold Corp, and sits on the boards of Arbor Metals, Tisdale Resources and Leocor Ventures.

Azincourt has 192 million common shares outstanding. Institutions hold 18%, insiders and close associates 10%, and family and friends 15%.

Disclosure: 1) Patrice Fusillo compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Skyharbour Resources. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Azincourt Energy. Please click here for more information.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Azincourt Energy, a company mentioned in this article.

Ralph Aldis, portfolio manager at U.S. Global Investors, in this interview with Streetwise Reports, looks at precious metals during the global downturn, and discusses M&A in the industry as well as companies he sees as undervalued.

Streetwise Reports: Ralph, thanks for joining us today. Let’s start with gold, which has seen a steep rise in the last few months amid the global pandemic and moves by central banks to shore up the economy and the markets. What do you think is ahead for the metal?

Ralph Aldis: I think that the backdrop of government spending and monetary intervention by the Federal Reserve to keep interest rates low provides a solid foundation for gold to still move higher. You throw in a potential change in leadership in the White House in November and maybe we will see gold take out its previous high. In 2016, gold rallied pretty hard for the first nine months but lost its momentum with the election of President Trump and the focus on wealth creation and the stock market. All the uncertainty risk that tariffs and other unexpected policies have created have really raised the foundation for higher gold prices. I think that’s why we’ve seen it steadily march higher over these last three years despite the focus on the stock market.

SWR: Gold has long been outperforming silver, and the ratio is around 100 right now, after coming down a little bit. What do you see ahead for the relationship between the two metals?

RA: There has been a lot of excitement about the gold-silver ratio recently. The last time it was at 80 roughly was back in September 2019, but with this first wave of COVID coming through, the ratio blew out as far as 124:1. It’s now tightened back to about 100:1. But we know what was driving that was low industry demand for silver with the lockdown and increased investment demand for gold going up at the same time. That’s what really drove it so far out there.

Perhaps a good indicator of where it could go next would be again to look back at July of 2016 when we had that last rally. The ratio at that point compressed down to 66:1, so that was quite a bit of contraction. We’re at 100:1 right now. A 60:1 move would be great. But should this gold market really get a new round of buyers as we head into 2021, I think silver will be recognized as a cheaper entry point into the precious metals trade.

SWR: Do you feel at this point people should be investing in the physical metal, mining stocks or both?

RA: We typically recommend a 10% allocation to precious metals and mining stocks as a prudent allocation. Investors now have an easier access to bullion price moves through exchange-traded proxies, but the capital gains tax rate is still 28% for collectibles versus 15% for most other investments. So that really favors the mining stocks. And the leverage to rising metal prices is best captured through owning mining stocks, which offer more upside. But holding bullion can be less volatile than owning the market. There are periods when bullion outperforms the mining stocks and vice versa. But traditionally, you typically get 3 to 1 leverage out of the mining stocks versus the bullion, and so that’s probably an attractive place to start to have exposure.

SWR: You run the Gold and Precious Metals Fund (USERX) and the World Precious Minerals Fund (UNWPX). What are some of the trends that you’re seeing with mining stocks?

RA: Much of the focus on price action in the gold space up until now has been concentrated on new leadership teams at Barrick Gold Corp. (ABX:TSX; GOLD:NYSE) and Newmont Corp. (NEM:NYSE), and they deserve the attention. The returns on invested capital for both companies have been rising in each of the last three quarters. Their asset sales have largely been completed, and now there are even some investments being made by these companies in the junior space. Barrick bought into Reunion Gold Corp. (RGD:TSX.V) last year, and Newmont made a strategic investment in GT Gold Corp. (GTT:TSX.V), which has an exciting discovery. So I think the fear of doing a transaction in the gold space is now behind us.

For our Gold and Precious Metals Fund, consolidation is good as we tend to be more positioned in the midtier precious miners and that’s where consolidation tends to play out. The larger cap miners have had their valuations lifted with the money flows into the exchange traded funds (ETFs), and many analysts are now suggesting that investors look downcap for smaller companies that have lagged. We’re starting to see more deals materialize in the midtier space, too, and we can talk about that here in a little bit.

I would say for our World Precious Minerals Fund, the tune of underperformance may be changing. For instance, coming off the bottom of the COVID-19 low on March 18, the fund is up 96.32%, while the VanEck Vectors Gold Miners ETF (GDX:NYSE.Arca) and the VanEck Vectors Junior Gold Miners ETF (GDXJ:NYSE.Arca) gained 76.52% and 87.36%, respectively. This is a short time window, but we’ve outpaced them coming out of the bottom, so I find that to be very encouraging. Over the last few years, we’ve had an investment mania in cannabis and Bitcoin. They were really competing for the speculative dollars, and mining was not really doing that much. Now those trades have largely faded away, and investors are beginning to sniff out the value proposition that these junior miners and exploration development companies present.

For World Precious Minerals, there is not an ETF available for exposure to these companies, and no other mutual fund has more junior miners and exploration exposure as a percentage of the fund than World Precious Minerals. The seniors, they’ve touched a toe on some of these stocks, and we’re also seeing some activity with the midtiers: Alamos Gold Inc. (AGI:TSX; AGI:NYSE) has been taking investment positions in the exploration space with GFG Resources Inc. (GFG:TSX.V; GFGSF:OTCQB) and then Red Pine Exploration Inc. (RPX:TSX.V; RDEXF:OTCMKTS) along with a couple of others. So the miners see the deep value in the space, and they are now buying these names. What we haven’t seen is the retail buyer show up yet, so I think that is where the opportunity is. If the seniors and the midtiers are buying the juniors, I think it won’t be too long before the retail space wakes up and starts paying attention to these names and tries to get a position.

SWR: What are some of the resource companies on your Buy list?

RA:TriStar Gold Inc. (TSG:TSX.V) would be one of my top ones. It has a real geological science team of professionals creating value through the drill bit. TriStar’s last resource update increased its ounces by a factor of seven. It mainly was because prior to that there was no money being allocated to drilling budgets for exploration. But once it got some money, the resource grows sevenfold. Royal Gold Inc. (RGLD:NASDAQ; RGL:TSX) has also provided TriStar some money, so it is continuing to work. It has cash; it is not going to go bankrupt. And this deposit is a Tarkwa/Jacobina-style deposit, but there are modern day analogs of these deposits of this type of genesis right now forming off the coast of Nome, Alaska, and off the coast of New Zealand. The exploration markers for finding more gold in this type of system are pretty well understood now. I was at the site in Brazil in February and got to see a lot of it firsthand. It was a great site visit, and this is, I think, a name that’s going to be a big mine at some point in the future.

Another company that I think actually offers a lot of opportunity right now is Roxgold Inc. (ROXG:TSX). When we look at companies and model them, we look at the resource base and we look at the quality of that resource base, whether it’s grade, the covariance of the resource and the science and the statistics behind it. We try to assess what an equivalent asset trades for in the market. For Roxgold, we see the company as being 60% undervalued relative to other operating assets that have equivalent type ounces and grades. The returns on invested capital have fallen with the average grades coming down, but Roxgold did an acquisition from Newcrest Mining Ltd. (NCM:ASX), Séguéla, in the Ivory Coast, and that looks to be a very prospective land package. Roxgold has conserved its capital, and it has made a very good capital allocation decision on this property. I think it is going to be a game-changer for it.

Another one that is in both of our funds and is a top position is K92 Mining Inc. (KNT:TSX.V). We see that one right now 31% underpriced relative to other operating assets, and it has a lot of exploration potential yet to be fully recognized. So there may be still a lot in there.

So those are my Top 3 buys right now.

SWR: You alluded to M&A activity, and there has been a fair amount recently. We have Argonaut Gold Inc. (AR:TSX) and Alio Gold Inc. (ALO:TSX; ALO:NYSE.American); Silvercorp Metals Inc. (SVM:TSX; SVM:NYSE)/Gran Colombia/Zijin Mining bidding for Guyana Goldfields Inc. (GUY:TSX); Wallbridge Mining Co. Ltd. (WM:TSX; WLBMF:OTCMKTS) and Balmoral Resources Ltd. (BAR:TSX; BALMF:OTCQX) and, most recently, Evrim Resources Corp. (EVM:TSX.V) and Renaissance Minerals Ltd. (RNS:ASX). What trends are you seeing with these mergers? Do you expect to see more deals?

RA: Yes. The seniors, for two or three years there, it is like they were petrified to do an acquisition because they figured they’d get taken out to the woodshed and shot because some of the capital allocation decisions historically have been guided by net asset value models, investment bankers and so on, and not based on where real assets are actually trading and what they should be valued at. But I think the companies’ capital allocations are much better now, and they are willing to do transactions.

Argonaut brings a wealth of knowledge to Alio on improving the productivity of that asset. I think Silvercorp’s bid for Guyana Goldfields was opportunistic, meaning, if it got it, great, but obviously it was willing to walk away at a price. Then Wallbridge and Balmoral, they basically brought a lot of synergies together with a good mineral property and the mill that they can actually work with, too. So I think the M&A is on. Right now, we’re just at the beginning of the game.

SWR: If we’re at the beginning of the game, what companies would you put on your list that you expect to see as merger candidates?

RA: Well, I worked on this last night and the serendipity of the way it happened is that this company had a takeover offer today, a second one. I think the key thing right now is that single asset companies that have shovel ready projects could be at the top of the list. And the example I was using is Cardinal Resources Ltd. (CDV:ASX). It certainly fits that description. And the government of Ghana is totally backing the project with its purchase of the debt that Sprott Resource Lending had with the Ghana Infrastructure Investment Fund, a Ghana-owned investment vehicle, buying the debt. It looks like in taking that out, that may have been one of the catalysts.

But all of the major gold mining companies have operations in Ghana. So where are you going to go to replace a potential steep depletion rate with a new mine when the country has your back? So I think the government is certainly behind this. I wrote this last night, and when I came in this morning I found out that Shandong Gold Mining Co. (600547:SHA; 1787:HK) has made an all-cash bid for Cardinal, topping the bid made by Nordgold by 31%. I think this is a real question right now: Will there be a counterbid or a new interloper entering the mix? We will see. But I think the bidding is on for assets. As I review recent filings, both MM Asset Management Inc. and Macquarie Bank Limited have lodged reports showing they raised their exposure to Cardinal since the Shandong offer was announced.

There are other companies, too. Just think about single asset companies. Any single asset company is probably a target, but also a single asset company could be looking at another project to combine with it to get some synergies. So I think the game is on right now.

SWR: Is there anything else that you’d like our readers to know?

RA: I recommend investors stick to a sound asset allocation plan. Don’t put all of your wealth into gold by any means. A small part will give you good benefits in terms of reducing your overall portfolio volatility. When we look at the economy right now, there’s a lot of push to keep interest rates as low as possible. The Fed has some bullets, but it’s tough right now. I think the bigger issue also that we’re dealing with is social reforms are coming. That may imply higher taxes, but a lot of those things have been sorely underinvested. If you’re not investing in people, then you don’t really have a business or a country if you don’t really take care of the population and give people opportunity, and not just a few people, but lots of people.

SWR: Thanks for your insights, Ralph.

Ralph Aldis, CFA, portfolio manager of U.S. Global Investors, is responsible for analyzing gold and precious metals stocks for the World Precious Minerals Fund (UNWPX) and the Gold and Precious Metals Fund (USERX). In addition, Aldis serves as co-portfolio manager for the Global Resources Fund (PSPFX), Holmes Macro Trends Fund (MEGAX), All American Equity Fund (GBTFX), Emerging Europe Fund (EUROX), Near-Term Tax Free Fund (NEARX), U.S. Government Securities Ultra-Short Bond Fund (UGSDX), the China Region Fund (USCOX), and the U.S. Global Jets ETF (JETS). In 2011, and again in 2015, Aldis was named a U.S. Metals and Mining “TopGun” by Brendan Wood International. In 2016, he and Frank Holmes were named Best Americas-Based Fund Manager by the Mining Journal. Aldis received a master’s degree in energy and mineral resources from the University of Texas at Austin in 1988 and a Bachelor of Science in Geology, cum laude, in 1981, from Stephen F. Austin University. Aldis is a member of the CFA Society of San Antonio.

Disclosure: 1) Patrice Fusillo conducted this interview for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She owns, or members of her immediate household or family own, shares of the following companies mentioned in this article: None. She is, or members of her immediate household or family are, paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this interview are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Ralph Aldis: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: N/A. I, or members of my immediate household or family, are paid by the following companies mentioned in this article: N/A. My company has a financial relationship with the following companies mentioned in this interview: N/A. Funds controlled by U.S. Global Investors hold securities of the following companies mentioned in this article: Barrick Gold Corp, Newmont Corp., Reunion Gold Corp., GT Gold Corp., TriStar Gold Inc., Royal Gold Inc., Roxgold Inc., K92 Mining Inc., Argonaut Gold Inc., Alio Gold Inc., Silvercorp Metals Inc., Gran Colombia Gold Corp., Cardinal Resources Ltd., Balmoral Resources Ltd. I determined which companies would be included in this article based on my research and understanding of the sector. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview. 4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Newmont, GFG Resources and Evrim Resources, companies mentioned in this article.