Risk appetite is stepping hesitantly into the second half of the year, with Asian stocks edging higher while US futures slipped into the red. Over the past three months, the S&P 500 posted its best quarterly performance since Q4 1998 with a near-20 percent advance while the Dow climbed 17.8 percent.

It’s highly unlikely that US equities can better its Q2 performance over the coming months, with the rally having stalled of late. Last month, the Dow Jones index has been sandwiched mostly between its 200-day and 100-day simple moving averages, with the 50-SMA offering support.

Stock markets have priced in most of the optimism surrounding the US economy’s reopening, and are in need of fresh catalysts to gain another leg up. To be fair to equity bulls, recent economic data appear to justify the stellar climb in stocks over recent months. June’s consumer confidence reading surpassed market expectations to register its biggest one-month gain since 2011. The ISM Manufacturing print should show that the sector is moving closer towards returning to expansionary territory. Thursday’s US non-farm payrolls print is expected to show an increase of over three million jobs last month following May’s positive shocker, while jobless claims and the unemployment rate are set to moderate further.

Yet, scepticism has begun creeping in and investors are now second guessing the amount of upside that remains in stocks over the near-term. The rise in Covid-19 cases in some US states warrants a cautious outlook as they threaten to throw the US economy off its course towards the post-pandemic era.

Perhaps the thing to jolt equities out of its sideways saunter could come at the hands of the upcoming US earnings season in two weeks for now, or as the US Presidential race heats up. Until then, developments surrounding the pandemic are expected to continue holding court among global investors.

Gold moving upwards, slowly but surely

Gold has taken its own sweet time in making its ascent, defying expectations that the safe haven asset would soar amid the global pandemic. To be sure, spot Gold capped a 17.38 percent gain in the first half of 2020, and is now inching closer to that psychologically-important $1800 level. With Gold futures (for August delivery) breaching the $1800 mark for the first time since 2011 before moderating, it appears to be just a matter of time before spot prices would emulate the feat.

Bullion should continue facing upward pressure due to the persistent concerns among global investors, along with near-zero US interest rates that are set to stick around for longer. Still, in carving out more gains, Gold has to contend with a resilient US Dollar, as well as bouts of risk-on sentiment that are just raring to break through, at the expense of safe haven assets.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Colombia’s central bank lowered its policy interest rate for the fourth time this year, as expected, as it continues the countercyclical momentum of monetary policy to boost the economy amid what it said was a persistent uncertainty about the outlook for the global economy. The Central Bank of Colombia cut its main interest rate by another 25 basis points to 2.50 percent and has now cut it by 175 points this year following earlier cuts in March, April and May. A majority of five of the bank’s seven-member board voted for the rate cut, the bank said. Today’s 25-basis-point cut is smaller than the previous cuts this year that were all 50 points. Colombia’s inflation rate fell to 2.85 percent in May from 3.86 percent in April, and inflation expectations continued to decline to below 3.0 percent, reflecting weak demand, a deterioration of employment and excess productive capacity, the bank said. Downward revisions to local and global growth suggest this excess productive capacity will expand and labour markets will deteriorate further, the bank said, adding its main trading partners will only expand slowly during the rest of the year. Although conditions in financial markets have improved from the start of the Covid-19 pandemic, there is still great uncertainty about the global economy, the central bank said. Colombia’s gross domestic product slumped to annual growth of 1.1 percent in the first quarter of this year from 3.5 percent in the previous quarter and on a quarterly basis GDP contracted by 2.4 percent in the first quarter from the fourth quarter of last year. Colombia’s finance ministry expects the country’s economy to contract 5.5 percent this year while the central bank in May forecast a contraction of between 2.0 and 7.0 percent this year, including a 10-15 percent annual contraction in the second quarter.

Charlotte, North Carolina (June 30, 2020) – A national precious-metals dealer has teamed up with a sound money policy group to help students pay for the ever-increasing costs of college.

Money Metals Exchange has joined with the Sound Money Defense League to offer the Sound Money Scholarship — the first gold-backed scholarship of the modern era. Starting in 2016, these organizations have set aside 100 ounces of physical gold (worth about $180,000 based on current Gold price) to reward outstanding students who display a thorough understanding of economics, monetary policy, and sound money.

The Sound Money Scholarship is open to high school seniors, undergraduate, and graduate students with an interest in economics, specifically the free-market tradition. Applicants do not have to be economics majors to be eligible to receive this scholarship – and the deadline for applications is September 30.

Money Metals Exchange and the Sound Money Defense League also announced this year’s blue-ribbon panel of judges:

Dr. Will Anderson is a Fellow of the Mises Institute and professor of economics at Frostburg State University. He earned his MA in economics from Clemson University and his PhD in economics from Auburn University, where he was a Mises Research Fellow. He has been writing about Austrian economics since 1981. In 1982, he won the Olive W. Garvey Economic Essay Contest and presented his paper at the Mont Pelerin Society in the former West Berlin.

He has published numerous articles and papers on economics and political economy, including articles in The Independent Review, Reason Magazine, The Free Market, The Freeman, Public Choice, The American Journal of Economics and Sociology, Quarterly Journal of Austrian Economics, The Journal of Markets and Morality, Regulation, Freedom Daily and others

Dr. Per Bylund, PhD, is a Fellow of the Mises Institute and Assistant Professor of Entrepreneurship & Records-Johnston Professor of Free Enterprise in the School of Entrepreneurship in the Spears School of Business at Oklahoma State University, and an Associate Fellow of the Ratio Institute in Stockholm. He has previously held positions at Baylor University and the University of Missouri.

Dr. Bylund has published research in top journals in both entrepreneurship and management as well as in both the Quarterly Journal of Austrian Economics and the Review of Austrian Economics. He is the author of two full-length books

Larry Reed is the Foundation for Economic Education’s (FEE) President Emeritus and Humphreys Family Senior Fellow. Reed served as president of FEE from 2008-2019 after serving previously as chairman of its board of trustees in the 1990s and both writing and speaking for FEE since the late 1970s. Prior to becoming FEE’s president, he served for 21 years as president of the Mackinac Center for Public Policy in Midland, Michigan. He also taught economics full-time from 1977 to 1984 at Northwood University in Michigan and chaired its department of economics from 1982 to 1984.

He holds a B.A. in economics from Grove City College (1975) and an M.A. degree in history from Slippery Rock State University (1978), both in Pennsylvania. He holds two honorary doctorates, one from Central Michigan University (public administration, 1993) and Northwood University (laws, 2008).

Michael Maharrey serves as the national communications director for the Tenth Amendment Center. He hosts his own podcast, Thoughts from Maharrey Head, as well as the Friday Gold Wrap. Michael is the author of four books and several e-books on the US Constitution and nullification.

Michael earned a degree in Mass Communications from the University of South Florida St. Petersburg and a B.S. in Accounting from the University of Kentucky. He speaks at events across the United States, and frequently appears as a guest on local, national, and international radio shows advancing constitutional history and America’s founding principles.

In prior years, the Sound Money Scholarship has received entries from students attending more than 180 different schools in 44 states, Puerto Rico, Washington D.C., six countries, and three continents.

The deadline to submit applications is September 30, 2020.

Sound Money Defense League is a public policy group working nationally to promote sound money across the U.S.

Money Metals Exchange—a national precious-metals retailer recently named “Best in the USA” by an independent global-ratings group—buys, sells, and securely stores physical gold, silver, platinum, and palladium.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Jamaica’s central bank kept its key interest steady, saying this is based on its continued view this rate is generally appropriate to support inflation remaining within its target of 4.0 to 6.0 percent over the next two years. The Bank of Jamaica (BOJ) left its rate on overnight deposits at 0.50 percent, unchanged and at a historic low since August 2019, but added the outlook remains “highly uncertain” in the context of the ongoing Covid-19 pandemic and it “stands ready to implement other policy measures, if the need arises.” In a statement from June 29, BOJ said the risks to its forecast for gross domestic product were slightly skewed to the upside as the government’s decision to re-open the country’s ports to incoming passengers in June could improve growth prospects, along with the prospects of stronger economic activity in the United States. However, material risks to the downside remain, BOJ added. In its May outlook, BOJ forecast GDP would contract an average 5.1 percent in the current fiscal year, which began April 1, and then partially recover in fiscal 2021/22 with growth ranging from 2.5 to 5.5 percent. Jamaica’s economy stagnated in the fourth quarter of 2019, with GDP at zero percent growth year-on-year, down from growth of 0.6 percent in the third quarter, with output hit by measures to contain the pandemic. On a quarterly basis, GDP shrank 0.5 percent from the third quarter following a quarterly contraction of 0.2 percent in the third quarter, with the decline mainly seen in hotels and restaurants, mining, wholesale and retail, transport, storage and communications, and other services. Inflation declined to 4.8 percent in March from 6.0 percent in February. Although BOJ left its rate steady at its last policy meeting on May 20, on May 15 it lowered the cash reserve requirement by 200 basis points to 5 percent to boost liquidity in the financial system by releasing some J$14 billion to deposit-taking institutions. It also cut the foreign currency cash reserve requirement by 200 points to 13 percent, which returned some US$70 million to institutions. In May BOJ forecast inflation would average 4.4 percent over the next two years and today it said the current assessment is inflation is likely to be slightly higher due to higher agricultural, energy and transport prices, and upward pressures from higher-than-expected demand in connection with an earlier-than-expected re-opening of the economy and a more expansionary fiscal stance. Jamaica’s dollar has firmed slightly this month but remains down 5 percent since the start of this year at 140.0 to the U.S. dollar.

The Bank of Jamaica issued the following statement:

“Bank of Jamaica announces its decision to hold the policy interest rate (the rate offered to deposit-taking institutions on overnight placements with Bank of Jamaica) unchanged at 0.50 per cent per annum. The decision to hold the policy rate unchanged is based on the Bank’s continued view that monetary conditions are generally appropriate to support inflation remaining within the target of 4.0 per cent to 6.0 per cent over the next two years. The economic outlook for Jamaica remains highly uncertain in the context of the ongoing COVID-19 pandemic. Bank of Jamaica will continue to assess incoming data and stands ready to implement other policy measures, if the need arises. Inflation Annual inflation at March 2020, as reported by the Statistical Institute of Jamaica, was 4.8 per cent, lower than the 6.2 per cent at December 2019 and firmly within the target range. Underlying or core inflation, which measures the change in prices excluding agricultural food and fuel prices, remained relatively low at 3.3 per cent. At our assessment in May 2020, Bank of Jamaica’s forecast was for inflation to average 4.4 per cent over the next two years. The forecast was mainly predicated on the impact of the COVID- 19 pandemic, which was expected to induce a deceleration in agricultural food prices and a decline in energy and transport related costs. In addition, the forecast included the impact of administered price increases. Bank of Jamaica’s current assessment is that inflation is likely to be slightly higher than previously forecasted over the forecast period but is still expected to track within the target range of 4.0 per cent to 6.0 per cent. This updated view of the inflation outlook stems from expectations for higher agriculture prices as well as higher energy and transport costs, compared with the Bank’s earlier forecast. In addition, upward price pressures could emanate from higher than expected aggregate demand, consistent with an earlier than expected re-opening of the economy as well as a more expansionary fiscal stance. Other Economic Variables At the assessment in May 2020, Bank of Jamaica’s forecast anticipated that, for the current fiscal year (June 2020 to March 2021 quarters), the Jamaican economy would contract, on average, by 5.1 per cent. In the following year (up to the March 2022 quarter), the Jamaican economy is projected to partially recover, with real GDP growth in the range 2.5 per cent to 5.5 per cent. The fall in real GDP in FY2020/21 was expected to be mainly reflected in Hotels & Restaurants, Mining, Wholesale & Retail, Transport, Storage & Communication and Other Services. These expected declines are largely based on the adverse impact of the global COVID- 19 pandemic on travel, production, distribution and entertainment activities.

The Bank’s current assessment suggests that the risks to the forecast for GDP are slightly skewed to the upside, suggesting the possibility of a better than previously anticipated outturn. The Government’s announcement of the re-opening of Jamaica’s international ports to incoming passengers in June is a key development that could contribute to improved growth prospects for the economy and is supported by the prospects of stronger economic activity in the USA. However, material downside risks to economic activity remain. At our assessment in May 2020, the current account deficit (CAD) of the balance of payments (BOP) was projected to deteriorate to 7.5 per cent of GDP for FY2020/21, mainly due to the forecast of a sudden stop in visitor arrivals due to the closure of borders to visitors until September 2020, as well as a significant decline in remittance inflows. The CAD was projected to improve gradually over the medium term. Given recent developments, particularly the earlier than anticipated re-opening of Jamaica’s borders in mid-June 2020 and a stronger performance of remittance inflows, the CAD could likely be lower than previously anticipated. Monetary Policy Bank of Jamaica remains committed to ensuring that inflation remains low and stable within its target and, at the same time, is prepared to take all necessary actions to ensure that Jamaica’s financial system remains sound. The next policy decision announcement date is 18 August 2020.” www.CentralBankNews.info

Technical analyst Clive Maund discusses the price of gold in various currencies and what he believes is ahead for gold, the U.S. dollar and the stock markets.

We will start this update by looking at gold’s price measured against various important currencies. These long-term charts quickly make clear that gold is in a major bull market, which is another way of saying that these currencies are losing purchasing power.

Gold in Australian dollars

Gold in Canadian dollars

Gold in Japanese Yen

Gold in Swiss Francs

So we should clearly not allow ourselves to be fooled by gold not breaking out to new high against the U.S. dollar, especially given the Fed’s recent extreme profligacy involving the creation of trillions of dollars for the purpose of backstopping the credit markets, bailing out favored crony corporations, and paying countless millions of newly unemployed people to sit at home twiddling their thumbs, none of which can be classified as productive use of the money. All this extra money means that eventually there will be a lot more money chasing the same, or rather a reduced supply of goods and services, now that the economy is a lot less productive thanks to lockdowns and closures, etc. The only reason that the Fed has been able to get away with it so far without rampant inflation is because the economy is dead, so there is no money velocity, but this money will find its way out eventually and when it does we will be looking at robust inflation trending towards hyperinflation. Needless to say this will lead to gold appreciating dramatically against the dollar, as the dollar’s purchasing power shrinks.

Bearing all the above in mind it is thus interesting to observe that even though gold has not (yet) broken out to new highs against the U.S. dollar, it has also done well in this currency over the past two years and is getting close to doing so. Therefore it is not too difficult to deduce that with the creation of new dollars ramping up exponentially, it is only a matter of time, and not too much at that, before gold does go on to make new highs against the dollar, a development that will usher in a period of accelerated advance.

Gold in U.S. dollars

This is a good point to add Larry’s latest gold chart showing the gigantic Cup pattern, which points to an explosive move up soon, even if we see a brief break lower before it. As Larry himself points out: “A Cup & Handle formation will need to carve out a Handle to be complete,” however, the way things are deteriorating it is hard to imagine gold hanging around for more than a short time marking out a Handle to complement this Cup. If you want to send feedback to Larry about this, his email address is on the chart.

The Great Gold Cup

To those who say “old will never go up much because ‘they’ will not allow it to, because it reveals their fiat money scam to be increasingly defunct, and they will suppress it with paper shorting on the Comex, etc.” I say this: the fiat money system is already breaking down as we head into the end game of a hyperinflationary firestorm that will render most currencies worthless. Astute investors who understand the power of gold and its intrinsic value know this, and are not fooled by games on the paper markets. If they continue to try to suppress the price of gold on the paper markets, all that will happen is that the already large premiums for physical metal will grow wider to the point where it becomes untenable, with the paper markets increasingly perceived as a manifest absurdity that will be bypassed by investors who will go straight to physical which will skyrocket in price before becoming unobtainable, and the same will happen with silver. This process has already started.

Even though we have observed that gold is in a major bull market that is set to accelerate dramatically as we trend towards hyperinflation, does this mean that it is immune to potentially sharp corrections? No, it doesn’t. As we know, the stock market has lost all touch with economic reality. The economy is flat on its back and comatose, yet the stock market has been going higher and higher until the NASDAQ actually made new highs a week or so ago. The reason for this is the Fed creating trillions out of thin air to throw at pumping it up. Therefore, anytime the Fed fails to pony up with the additional liquidity that the market thinks is its due, it is going to throw a nasty tantrum, like it did in March, and we should all be aware that the Fed may actually do this by design, so that it can smack the market down and then move in and scoop up more assets on the cheap. The charts show that we are right now at a time where that could happen and if it does the precious metals sector is likely to get taken down with it, as happened in March, in accordance with the old “baby and the bathwater” adage. Should this happen it will be viewed as presenting an outstanding opportunity to move in acquire more precious metal sector assets, because the Fed is likely to come riding to the rescue once more with a torrent of liquidity.

There are many who think that the Fed’s taking full advantage of the dollar’s reserve currency status to create countless trillions of new dollars will nevertheless cause it to lose value in a big way against other currencies, but a mitigating factor is that the Fed is not only flooding the U.S. with extra dollars, it is flooding the whole world, by pumping them into countless other central banks around the world which it controls in an act of economic colonialism. So pretty much all currencies are set to drop in lockstep. The main point is that the stagflationary depression that the world has now entered will impel governments everywhere to create exponentially more and more money in an effort to maintain liquidity and keep a lid on interest rates. This is why gold MUST rise in price to reflect the loss in value of fiat, and it will go further than that as investors will eventually flock to gold as the last safest place to put money where it will retain its value (stock markets may be rising nominally but losing value in real terms).

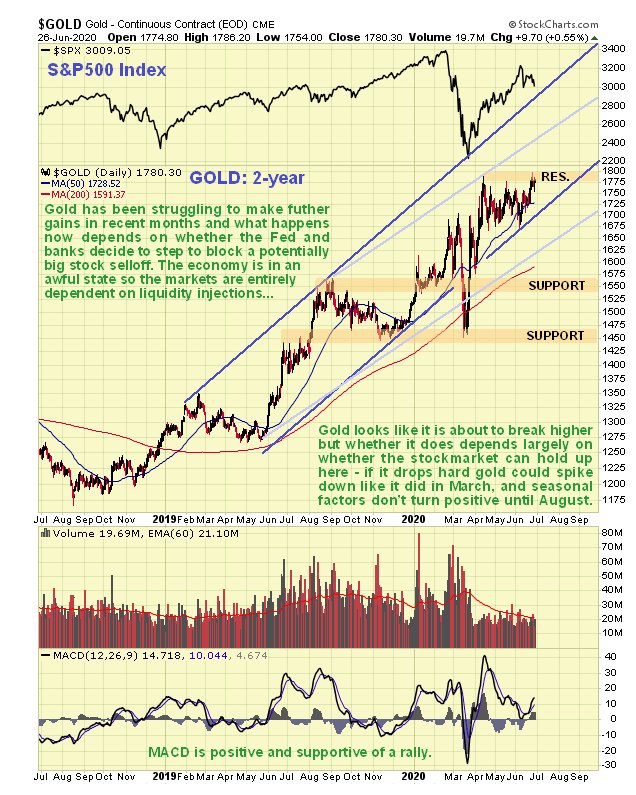

Gold, the stock market and the dollar are all at a critical juncture where they could break in either direction. What this usually means is that the markets are waiting on some fundamental development like, for example, whether the Fed is going to divvy up another trillion or two to throw at driving the stock market still higher, and maybe at the same time throw a bone to the 40+ million unemployed in the form of say $100 billion extra for checks to spend on flat screen TVs. On gold’s 2-year chart we can see that it has been struggling to make further progress within its uptrend over the past several months, and although in position to break higher, is vulnerable to a smackdown if the stock market should suddenly plunge. From a trading standpoint what would be ideal here would a short-term selloff that provides a buying opportunity ahead of the seasonally strong period in and August and September. If the stock market takes a hit it could do what it did in March.

The 6-month chart looks positive, with the price well placed to break higher after a trading range from mid-April that has allowed time for its earlier oversold condition to unwind. Moving averages and the MACD are supportive of an advance from here. As mentioned above though, a stock market selloff could abort this scenario with a rude reversal and steep drop.

Turning now to the dollar, we see on the 3-year dollar index chart that it has made no net progress for almost two years, having been stuck within a shallow uptrend trading range. The spike in March was due to the specter of a deflationary implosion which was banished by the Fed boldly riding to the rescue with trillions of crisp new dollars. The recent drop caused by the Fed’s manic money creation, found support in the 95 area.

Like the stock market and gold, the dollar is evidently waiting on some development that could result in it breaking either way, depending on what happens. This is why the fairly tight range of the past two weeks or so shown on the 6-month chart could be either a bear Flag or some kind of intermediate base pattern.

The conclusion to all this is that gold is in a powerful bull market which is expected to accelerate. Near term, while it looks set to take off higher and should do if the stock market holds up, it is vulnerable to a potentially sharp correction if it doesn’t which would be viewed as a buying opportunity for the sector.

Finally, I want to take this opportunity to recommend that you do whatever you can you make sure that you have at least some physical gold and silver in your possession. Very bad times are headed our way and most Americans have no idea what’s coming down the pike. If you have to pay a premium then pay it, because the premiums are only going to get bigger with passing time, and eventually physical metal will be very hard to come by. I particularly like silver for two reasonsone is that it is still very undervalued relative to gold, and the other is that you are less likely to be hit over the head or shot when you try to trade it for goods. Silver coins of varied denomination are viewed as ideal. Gold buried in vaults thousands of miles away may sound like a great idea, but when things get really bad, you may not be able to get to it, or it to you. If you have sufficient resources it’s still a good idea, but you still want a quantity of physical in your possession that you can trade, and of course the means and willingness to defend your stash from marauders.

Here is an important and timely video by Jeremiah Babe entitled “US ECONOMY WALKING DEAD.” Although directed at Americans it is considered important viewing wherever you are, because when America goes down, the shockwaves will reverberate around the world.

Originally published on CliveMaund.com on June 28, 2020.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. Clive Maund is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Clive Maund was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Much of what is written in the parallel Gold Market update is equally applicable to silver and it will not be repeated here.

Although silver has picked up significantly since its March low it has greatly underperformed gold over the past two years. But this is normal during the earliest stages of a major sector bull market, when gold is favored over silver.

On its 20-year chart we can see that silver remains stuck within a giant base pattern that started to form as far back as 2013. This chart makes clear that once gold breaks out to new highs against the dollar, then silver should break out of this base to enter a dynamic advancing phase.

The 5-year chart reveals that silver is battling a lot of resistance in this zone, so if gold should back off soon for whatever reason, like the stock market dropping hard, then it will likely drop back for a while too.

Here we should note that if the stock market does go into another down wave soon, then the Fed can be expected to print up another couple of trillion [dollars] to drive it back up again, which will be hyperinflationary and very bullish for gold and silver. Keep in mind that if the Fed (or its proxies) wade in here, buying stocks, they can head off any decline and get it moving higher again.

The 2-year chart for silver, with the S&P500 index shown at the top, is useful as it makes clear that there is a crude but important correlation between silver and the stock market, which can be expressed bluntly as “when the stock market tanks, it takes silver with it.” The message from this chart is thus clearif the stock market continues to advance, courtesy of continued Fed pumping, then there is a good chance that silver will break out of its base pattern. But if the Fed “falls down on the job” and the stock market tanks again, so will silver. Big Money doesn’t care about either the economy or the unemployedall it cares about is the stock market and how much it can make off of deals, etc.

On this chart we see that although silver’s overbought condition has neutralized in recent weeks, putting it theoretically in position to break out of its giant base, there is a lot of resistance above the current price that we can expect to turn it down if the stock market weakens.

Finally, on the 6-month chart we can see that silver is at a critical juncture here, with the 50-day moving average pulling up close to the price and the 200-day, and a small, potential head-and-shoulders top completing, so we can expect a bigger move soon.

Originally published on CliveMaund.com on June 28, 2020.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. Clive Maund is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Clive Maund was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr. Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

As we begin to engage with the climate emergency and the impact of carbon dioxide emissions, calls have grown to stop investing in companies engaged in fossil fuel production – a practice known as divestment.

The University of Oxford became one of the latest institutional investors to pledge to drop all fossil fuel companies from their £3 billion endowment. Enormous pressure from students and staff alike has been put on other universities to follow suit, creating a culture of shame on those that continue to hold these shares.

Many scholars in the UK may be horrified to hear that one of the largest university pension schemes, the University Superannuation Scheme (or USS) has the oil company Shell as its largest holding of £500 million. Recent changes to the USS investment strategy ended its investment in a number of controversial holdings, including tobacco manufacturing, coal mining, cluster munitions (a form of explosive) and landmines. But USS continues to invest in a number of fossil fuel companies saying they intend to engage with them as a “force for good”.

So long as they do wield this influence, we believe this is the right approach for investors who want to combat climate change. Many of those lobbying for divestment will have good intentions. Divesting from fossil fuel companies is likely to make investors feel morally cleansed, having washed their hands of dirty investments that make profits from environmental damage. But it may act as a diversion tactic, allowing the lobbyists and investors who follow their lead to feel good about themselves. And yet they will have done little to combat climate change.

Divestment, leading to the selling of fossil fuel company shares, should put downward pressure on the share price, making it harder for the company to raise new capital. But for the majority of them, even in the face of substantial divestments, it will be very much business as usual, having no effect at all on their day-to-day operations.

If more people want to sell shares than buy them, this will affect the share price – but most oil companies are well beyond the situation where it would cause them significant issues. Neither BP nor Shell, for example, are likely to need to raise new financing in the foreseeable future as they have large cash reserves. Both have share repurchase schemes, where they are able to use dips in their share prices to buy their own shares back, allowing investors to benefit without paying taxable dividends.

But if a company’s shares become sufficiently cheap relative to its profit stream, it will be ripe for a takeover. Most likely this will come from an even bigger, non-European oil company or by a wealth fund. It is highly likely in either case that the new purchaser will be less concerned about minimising the company’s environmental impact than those divesting. And any such commitments could easily be dropped in favour of a more concentrated focus on profits.

More worryingly, divestment is highly likely to constitute a small step in a chain of events that will perversely lead to precisely the opposite of the lobbyist’s desired outcome. When the University of Oxford (for example) sells its shares, they won’t simply disappear – rather they will be sold on the market to another investor. And the investors that are actively buying oil shares right now are unlikely to be those who are concerned about the environment.

Shareholder rights

The divestor also gives up the opportunity for shareholder activism – something USS does with the fossil fuel companies in which it holds investments. This is where shareholders can put pressure on companies they part own to introduce more sustainable ways of doing business. Although there is still much to be done, there is growing evidence that this kind of activism is having a positive effect on fossil fuel companies.

Many European oil companies are much better than their peers when it comes to environmental performance. While oil extraction and refinement is by its nature a dirty business, Shell, for instance, has a strong commitment to climate change mitigation. It aims to cut its net carbon footprint by 30% by 2035, and by 65% by 2050, meanwhile increasing the role of renewables in its energy production. Contrast this with some oil majors in the US whose only commitment is to the development of more effective extraction processes and more efficient fuel.

A counter-intuitive strategy for divestment activists would be for them to actually encourage the maintenance of large equity holdings in fossil fuel companies by sympathetic institutional investors, such as universities and USS. Then, by working together with other large shareholders and shareholder activist groups, bring real ownership pressure to bear in order to reduce the polluting activities of these companies. This would work by hitting them where it hurts – for instance, by blocking the awards of executive pay rises and bonuses.

Divestment puts shares in big oil into the hands of those who don’t give two hoots about the climate emergency, discourages such companies from taking mitigating steps and does nothing whatsoever to curb fossil fuel usage. If the question is how to tackle climate change, divestment is not even part of the answer.

Two releases of US data have given a conflicting picture of the world’s largest economy this afternoon. After a mixed outlook in May, where current conditions dipped but expectations rose, US Consumer Confidence figures rebounded strongly, smashing forecasts of 91.5 with a 98.1 print. Both current and future expectations surged, although it should be noted that the headline confidence remains very low compared to the more ‘normal’ reading in February.

On the flip side, the Chicago PMI suffered its biggest miss in five years, barely rising above the level from April. The dollar has barely flinched and is trading marginally higher on the day amid continued concerns over more lockdowns. Month end and quarter end flows may have helped lift the greenback recently.

US stocks have opened up higher as they continue their sideways trading around the 200-day moving average. Traders are eyeing seasonal trends which suggest volatility in risky assets as we head into the ‘quieter’ summer months.

Lacklustre Loonie

CAD has lagged behind the rebound in AUD and NZD, with soft Oil prices dampening the loonie’s recovery. That said, the Canadian Covid response has been good and should offer some support. The July 1 holiday may see choppy trading in the near term.

The broader grind higher from the mid-June low has come up against resistance in the low 1.37 zone. This is trend resistance from the March high so may prove tough to crack as trend strength signals are weak. A clear break through here could see 1.3850 and the April low pretty quickly.

AUD/USD up on China data

The aussie continues to fluctuate within a tight range, pending further directionality on the risk front. The uptrend from the March lows is still nicely on track but prices will need to conquer the June high through 0.7064 to see more upside.

The RBA Deputy Governor Debelle had earlier in the day reiterated that there was no need to negative rates, while the positive Chinese PMI data had also helped push AUD into positive territory.

Commodity Spotlight: Gold

The yellow metal is shining today, breaking higher to levels not seen since 2011. The August futures contract has actually pushed above $1800.

Falling US real yields are helping, plus emerging market demand is starting to rebound after massive falls in recent months when India’s gold imports plunged by 99% in April/May.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Kyrgyzstan’s central bank, one of only five central banks to have raised interest rates this year, left its key interest rate steady again to maintain stimulus to the economy, adding it would take “appropriate monetary policy measures” if there are any risks to inflation. The National Bank of the Kyrgyz Republic (NBKR) kept its discount rate at 5.0 percent, unchanged since it raised it in February by 75 basis points to dampen inflationary pressures. Inflation in Kyrgyzstan – sandwiched between China, Kazakhstan, Uzbekistan and Tajikistan – eased to 6.1 percent as of June 19 from 7.2 percent in May and 8.6 percent in April. Weaker domestic demand is determining the downward dynamics of inflation, the central bank said, pointing to the downward trend in remittances and export earnings along with a decline in the output of almost all sectors of the economy. The central bank maintained its forecast for inflation to average around its target of 5.0 to 7.0 percent by the end of the year based on the assumption of weaker domestic and foreign demand. “The recession in the global economy is expected to be significant,” NBKR said, adding its own economy remains susceptible to changes in global and regional economies and international financial organizations are revising forecasts lower despite some signs of recovery in some countries after quarantine measures have been lifted. Expansion by the public sector and support of credit operations by the central bank have led to excess liquidity in the banking system and NBKR continues to carry out sterilization operations in the short end of the money market, the central bank said, adding the foreign exchange market has been relatively stable. NBKR is in the process of transitioning to a monetary framework that is based on inflation targeting and from mid-March to early April, the Kyrgyzstani som tumbled 18 percent, hitting 84.9 to the U.S. dollar by April 4. Since the the som has firmed though it has eased during the month of June and was trading at 75.99 today, down 8.3 percent this year.

The euro made attempts to rise above the resistance level of 1.1261 level on Monday. However, price action was trading weaker as the euro failed to breakout above the technical resistance.

For the moment, the euro is trending lower in the medium term.

We expect the declines to see a test of the lower support area near 1.1132.

That said, there is a possibility that the euro might find minor support near the lows of 1.1171.

In the medium term, EURUSD will most likely move into a sideways range.

GBPUSD Breaks Down Below Support Level

The British pound sterling is trading slightly weaker, but declines are accelerating after prices broke down off the technical support.

The price level near 1.2344 has held up as support in previous tests. But the current breakdown off this level now puts the downside in focus.

We now expect the GBPUSD to post declines down to 1.2233 level. There could be a slight rebound off this level that might keep prices range-bound.

Crude Oil Attempts To Push Higher

Oil prices are trading bullish on Monday as prices rose over 3.5% on the day.

Price action is finding support off the rising trend line, leading to this rebound.

However, the current gains will see price challenging the technical resistance area near 40.42 – 40.18 level.

A strong breakout above this level is required in order to maintain further gains.

Failure to do so could keep prices subdued and will potentially open up the downside risks in crude oil.

Gold Holds Steady Near Previous Highs

The precious metal is trading rather flat on the day following an attempt to push higher.

However, with prices trading just below the previous highs, we expect this consolidation to result in a breakout.

The bias is slightly to the downside, following the double top pattern forming near 1774.20.

If gold prices break down below 1760, then we expect a decline back to the 1747.20 level of support.

To the upside, clearly, gold needs to make a breakout above 177420 to continue the bullish trend.