This week – July 5 through July 11 – central banks from 7 countries or jurisdictions are scheduled to decide on monetary policy: Israel, Australia, Malaysia, Mauritius, Sri Lanka, Serbia and Peru.

Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.

The MacNeill family also runs a company named 49North Resources Inc. (FNR:TSX.V) that is pretty much a fund holding positions in about 60 different juniors in both energy and minerals. FNR owns 45 million shares of OMM. With OMM at $0.68 that makes the portion owned by FNR worth about $30 million.

With FNR shares selling for $0.14, that makes FNR’s market cap about $11.6 million. FNR does have debt in the form of a convertible debenture but they also have pieces of about 59 other companies than Omineca.

So if you buy 49North shares today you are basically buying Omineca shares at half price.

Omineca Mining is not an advertiser and I have no financial relationship other than having participated in the last PP at $0.12 with a full $0.20 warrant. The four-month hold doesn’t expire until August 28th so there is literally no overhead.

49North Resources is also not an advertiser but I can both add and subtract so I have picked up shares in the open market.

To the extent that everyone that owns shares is somewhat biased, I am biased so you should do your own due diligence.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Omineca Mining and 49North. Neither company is an advertiser on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: Omineca Mining and Metals. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Omineca Mining and Metals. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Omineca Mining, a company mentioned in this article.

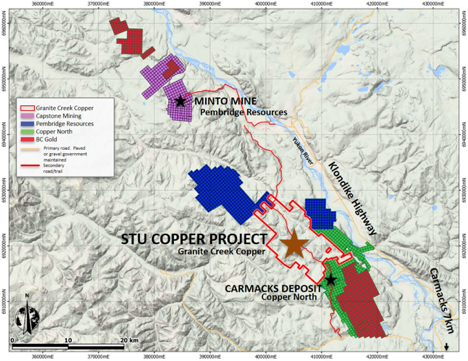

The president and CEO of Granite Creek Copper outlines prospects for the Stu Copper-Gold project in this conversation with Maurice Jackson of Proven and Probable.

Maurice Jackson: Welcome to Proven and Probable. Today, we’re going to highlight an early-stage exploration company focused on copper, gold and silver located in the Yukon, in Canada’s prolific Minto Copper District, Granite Creek Copper Ltd. (GCX:TSX.V). Our featured company has seen its share price increase from $0.03 to $0.10 in less than 60 days. They’re fully cashed up and ready to begin their 2020 field season. Joining us for a conversation is Tim Johnson, president and CEO of Granite Creek Copper.

Mr. Johnson, glad to have you back. It’s been a while. And since that time, Granite Creek has achieved a couple of significant milestones, including a successful financing (click here) and the launch of your 2020 field season.

But before we get into that, Mr. Johnson, give us a basic overview of Granite Creek Copper and the Stu Copper-Gold project.

Tim Johnson: The Stu Copper-Gold project was acquired by the company in January of 2019. It was a land package that had been held by a Yukon prospector and he had, over the years since the 1980s, been acquiring claims and assembling this land package in a significant copper belt. GCX is located in central Yukon. The nearest town is the village of Carmacks, and we’re on a paved highway from the capital Whitehorse, with good infrastructure. We have hydro within 20 kilometers of the property, along with good road access into the center of the property. We sit just south of the operating Minto mine and we are north and adjacent to the advanced-stage Carmacks deposit.

Maurice Jackson: In terms of progress to date, you’ve been rather aggressive, I should say, including securing an existing database containing some prior drilling, is that correct?

Tim Johnson: Shortly after acquiring the property, we were made aware of a private database that held information that had never been made public, and we were able to acquire that. And then, subsequently, we also acquired raw data from an airborne survey that was flown in 2008. And again, that survey had only a portion of it made public and no work had been done on that data. When you typically fly a geophysics survey. . .all sorts of post-processing work is done to help focus your efforts on the ground. None of that work had been done so it was quite a treasure trove of information that we were able to get and put together.

Maurice Jackson: Allow me to be the first, Mr. Johnson, to congratulate you and the entire team for successfully completing the financing and the beginning of your 2020 field work. What’s the strategy there, and the plan, and take us through some of the geology that you’re seeing and what that might mean in terms of opportunity for us.

Tim Johnson: Well, it all references back to that database that we acquired. So, the property was drilled in the 1980s, but the company that drilled at the time had the entire belt. What they discovered is that the Minto geology was much easier to figure out, as it was more exposed at surface. Therefore, their efforts were focused there and they never really completed their exploration program on what is now the Stu properties. They let that property lapse and, like I said, it’s been held private since the 1980s. There was roughly 5,000 meters of drilling done and only 20% of that core was ever sampled. They only sampled the obvious high-grade material. There is a mineralized core on the property that’s never been assayed.

What we’ve since discovered is that they weren’t focused on precious metals and were using an in-house lab with very high detection limits on precious metals. Noteworthy to mention that a lot of stuff, say sub-gram gold material, wasn’t even recognized. Granite Creek Copper’s program this summer is going to focus on re-assaying as much of that core as we can using a modern lab with modern detection limits. And we hope that we’re going to be able to bring some of those precious metals that we know likely are there, but had been previously below the detection limit, into our resource model.

Maurice Jackson: Let’s go to the Stu Copper-Gold project. In terms of the district, it’s all there. You’ve got highway, power access and an operator to the north. How does that all come together for the benefit of Granite Creek shareholders?

Tim Johnson: This is a key point for investors because it gives us three exit strategies. If we find a modest resource, we’ll be able to do a toll milling or potentially some sort of an agreement with our neighbor to the north with an operating mill that we know is underutilized right now. They can take mill feed. If we find a larger resource, then we become a takeover target for them as they would want to secure that resource.

And if we find a larger resource yet, then we attract a major player to the belt. And we think probably the best value for investors, and the highest potential, is that we can show the larger players in the copper space the potential for the belt. We think there’s multiple billion pounds of copper within the belt, from the Carmacks deposit to the south up to Minto, and that’s what we want to prove up.

Maurice Jackson: Now that the financing is complete, please provide us with an update on the capital structure.

Tim Johnson: Granite Creek Copper has 60 million shares outstanding. We’ve got about a 100 million fully diluted, and that portion would bring in about $2.5 million in cash, should all those warrants be exercised. We have just about $1.5 million in the bank. And we also have, on top of that, securities of 30% ownership in Copper North Mining Corp. that gives our investors access to, or exposure to, an existing resource. We want to build on that resource on our own ground and see what the economics of putting those two resources together is going to look like.

Maurice Jackson: On March 23, the share price was $0.03. Fast forward 60 days later, Mr. Johnson, what is the current share price?

Tim Johnson: The current share price is $0.10. We’re pretty pleased with that and we see upside potential for our share place.

Maurice Jackson: Last question, sir: What did I forget to ask?

Tim Johnson: You forgot to askor maybe I forgot to sayabout the nature of our collaborative approach to development within the belt. We keep our neighbors informed of what we’re doing, and they keep us informed of what they’re doing. We think the best strategy here is to attract a large player to the belt. And we’re only going to do that if we work together.

Maurice Jackson: Mr. Johnson, for readers that want to get more information on Granite Creek Copper, please share the contact details.

Maurice Jackson: Granite Creek Copper trades on the TSX.V: GCX. Granite Creek Copper is a sponsor of Proven and Probable and we are proud shareholders for the virtues conveyed in today’s message. Before you make your next bullion purchase, make sure you call me. I’m a licensed representative for Miles Franklin Precious Metals Investments, where we have several options to expand your precious metals portfolio. From physical delivery, off-shore depositories, and precious metal IRAs. Call me at (855) 505-1900, or you may email [email protected]. Finally, please subscribe to Proven and Probable for mining insights and bullion sales. Subscription is free.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Granite Creek Copper. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Granite Creek Copper is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Granite Creek Copper. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Granite Creek Copper, a company mentioned in this article.

Disclosures for Proven and Probable: Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Bob Moriarty of 321gold discusses the resource calculations at this company’s gold project in Brazil and explains why he’s an investor.

I fully approve of garimpeiro miners. Rarely can they read and write. They can live under conditions that the majority of us could never handle. They mine in a totally different way than do the junior resource companies in the space. They all make money. That’s right, 100% of garimpeiro miners make money regardless of what the price of the commodity is. They have to, because if they don’t, they don’t eat or provide food for their family.

Junior mining companies believe that spending money for twenty years and never making a dime in profit makes perfect sense. In fact, most geologists believe that geology is all about spending money. And they will spend money until frustrated investors finally give them the boot.

Garimpeiro miners think that spending money and not producing profit is daft. Because it is daft. When they can’t make money on a project, they stop spending money and time in fruitless activity. The “professionals” in the junior mining space don’t think much of the artisan miners but they could learn a lot from them.

Cabral Gold has doubled since the crash lows in mid-March and is still cheap. The company has a 100% interest in the 36,000 square km Cuiú Cuiú project with a million ounces of gold in 43-101 resources. The region was the world’s largest gold rush in the last 100 years with the artisan miners taking out somewhere between 20 and 30 million ounces of gold from near surface and surface mining. Their Cuiú Cuiú deposit produced 2 million of those ounces already. No doubt the locals left a few ounces, artisan mining leaves a lot of gold behind.

As a matter of general interest, Eldorado Gold is going into production at their 2.1 million ounce gold deposit only 20 km away. For many years infrastructure has been one of the biggest hurdles junior mining companies face in Brazil but the government put in a new road within the last five years that Eldorado linked into. Cabral has built a spur road from that. Brazil plans new hydroelectric plants in the area so power costs will drop and there will be more interest in the area.

The president, one of the largest shareholders of Cabral, Alan Carter, contacted me a year ago and pitched me on the project. My response to him was that all he needed to do was increase his visibility and the market would bid up the shares. He ignored me. The stock went down in spite of having compelling economics.

He called back this year. I told him the same thing. He’s on board now. The company just completed a major private placement and is sitting on $3 million cash reserved for drilling and exploration. Recent results that are now incorporated in the 43-101 show wonderful numbers including 3.4 meters of 36.9 g/t gold and 2.8 meters of 19.5 g/t Au. Surface samples from a newly discovered region called Alonso show grades of 11.6 to 200.3 g/t Au.

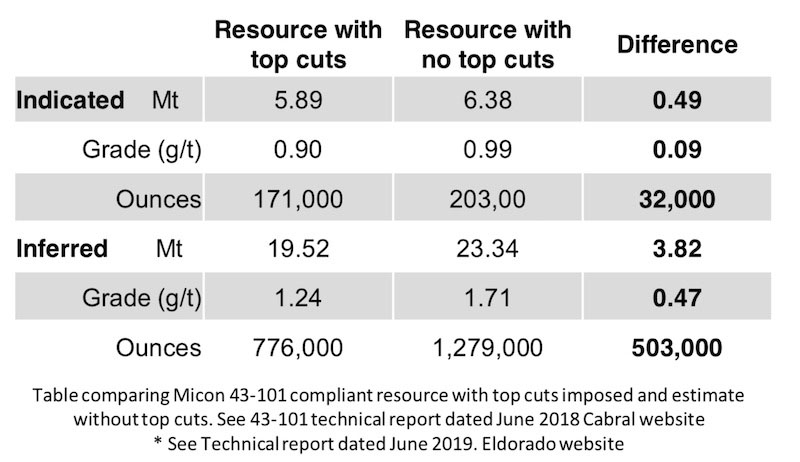

I highly suggest potential investors download the corporate presentation and go to page 11. I totally disagree with how Micon calculated the resource. When you are dealing with this form of gold, it has large nuggety gold in the saprolite layer at the surface decreasing to a tiny size in the laterite lower down: you get a really wide variation in size. Most investors, indeed most geologists don’t understand this but gold is highly mobile. In a very wet area such as Brazil half the year, the gold actually grows at surface in chemical remobilization. So using a top cut where you just ignore the very high grade simply is not accurate.

So I don’t buy the current 1 million ounce 43-101. It’s really 1.5 million ounces using the existing numbers but not being so anal about being conservative. Perfection is being accurate, not being perfect.

So their market cap is about $10 million USD and they have for all real purposes, 1.5 million ounces. That makes gold under $7 an ounce. If you must be anal retentive, it’s still gold for under $11 an ounce USD.

Given that the FED has guaranteed hyperinflation and the banks are going to close one day soon, owning a real resource run by real management where their interests are aligned with that of shareholders is probably a very good idea.

Cabral has major drill programs scheduled for the next six months so expect a lot of news. And this year the company is going to keep telling people what they have and that’s a really good thing.

Cabral is an advertiser. I missed the pp but I have bought shares in the open market. Do your own due diligence.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Cabral Gold. Cabral Gold is an advertiser on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Cabral Gold, a company mentioned in this article.

Recent drill results from Troilus Gold’s Quebec project are analyzed in a Red Cloud Securities report.

In a May 15 research note, Red Cloud Securities analyst Jacob Willoughby reported that drilling continues to grow the Southwest zone at Troilus Gold Corp.’s (TLG:TSX; CHXMF:OTCQB) Troilus project in Quebec.

Willoughby reviewed Troilus Gold’s recently reported results of six holes drilled in Southwest. They showed that in the zone, several high-grade gold intercepts occur within larger envelopes of disseminated gold. One such intercepts was 13.28 grams per ton (13.28 g/t) gold equivalent (Au eq) over 1 meter (1m) within 1.18 g/t Au eq over 21m, seen in hole TLG-ZSW20-181. Hole TLGZSW20-186 returned 16.1 g/t Au eq over 1.1m, 1.33 g/t Au eq over 5m and 1.43 g/t Au eq over 5m. Hole TLG-ZSW20-190 demonstrated 46.4 g/t Au eq over 1m.

These intercepts further suggest that the overall grade of the Southwest zone could exceed that of the existing resource, 0.95 g/t Au eq. As of now, the weighted average derived from all Southwest drilling reported so far is 1.05 g/t Au eq (unchanged) over an average 11.5m (down from 11.9m), and this represents an 11% improvement over the current resource grade.

The drill results also indicate that the mineralization in Southwest extends for 1-plus kilometers and remains open along trend and at depth.

Willoughby noted that he expects Southwest to improve the project’s overall grade and expand the current resource. Troilus Gold plans to revise the project’s mineral resource to include the Southwest drill results; the update could be released in Q2/20.

Looking forward, Willoughby commented, “Given previous operators (Inmet Mining Corp.) did almost no near-mine exploration, we expect the shares of Troilus to materially rerate over the next six to 12 months as the company demonstrates organic resource expansion potential along strike from the J zone, Z87 and the new Southwest zone areas.”

Red Cloud has a Buy rating and a CA$1.80 per share price target on Troilus Gold, the stock of which is now trading at around CA$1.05 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Troilus Gold. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Red Cloud Securities, Troilus Gold Corp., Exploration Update, May 15, 2020

Part of Red Cloud Securities Inc.’s business is to connect mining companies with suitable investors. Red Cloud Securities Inc., its affiliates and their respective officers, directors, representatives, researchers and members of their families may hold positions in the companies mentioned in this document and may buy and/or sell their securities. Additionally, Red Cloud Securities Inc. may have provided in the past, and may provide in the future, certain advisory or corporate finance services and receive financial and other incentives from issuers as consideration for the provision of such services.

Company Specific Disclosure Details

3. In the last 12 months preceding the date of issuance of the research report or recommendation, Red Cloud Securities Inc. has performed investment banking services and has been retained under a service or advisory agreement by the issuer. 4. In the last 12 months, a partner, director or officer of Red Cloud Securities Inc., or the analyst involved in the preparation of the research report has received compensation for investment banking services from the issuer.

Analyst Certification The Red Cloud Securities Inc. Analyst named on the report hereby certifies that the recommendations and/or opinions expressed herein accurately reflect such research analysts personal views about the company and securities that are the subject of this report; or any companies mentioned in the report that are also covered by the named analyst. In addition, no part of the research analysts compensation is, or will be, directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

– Investors entered the trading week adopting a cautious stance as the number of coronavirus cases worldwide exceeded 10 million, with the death toll topping 500,000.

So much has happened the start of 2020 with the shocking events sparking explosive levels of volatility. On Tuesday, we discussed the FX winners and losers of 2020 so far, highlighting how the Dollar and Japanese Yen were top performers year-to-date.

Mid-week the risk pendulum swung back and forth thanks to confusing data from the United States. As the resurgence of new coronavirus cases strained global sentiment and fuelled lockdown fears, most started to question what could be next for markets after the Q2 rally?

The main risk event was June’s US jobs report on Thursday which smashed market expectations. Payrolls surprised by rising 4.8 million while the unemployment rate plunged to 11.1% but the devil is in the details. With the number of permanent job losses rising and average hourly wages on a slippery decline, it may be too early for any celebrations.

Given how the coronavirus chaos, global growth concerns, US-China trade tensions and Brexit among many other negative themes are set to rock sentiment over the coming months, could volatility be here to stay?

The Dollar Index’s (DXY) price action on Friday was reminiscent of watching paint dry. Prices remain in a range on the daily timeframe with support at 96.00 and resistance at 97.80. Should 97.15 prove to be a pivotal level, prices may rebound towards the 97.80 in the new trading week.

EURUSD indecisive as usual

Seems the Euro is struggling to decide whether to push higher or sink lower against the Dollar. Some fresh direction may be provided in the week ahead. Investors may be keeping a close eye on how prices behave between the 1.1270 and 1.1200 level.

GBPUSD ends week on a flat note

Talk about an anticlimactic end to a volatile week. After displaying explosive levels of volatility earlier in the week, the GBPUSD has entered standby mode for now. A breakout/down setup could be on the cards here with support at 1.2250 and resistance and 1.2550.

USDJPY on standby

Same story with the USDJPY, much attention should be directed towards the 107.00 support and 108.00 resistance level.

Gold grinds higher

A solid weekly close above $1765 should open the gates towards $1796 and $1800. If the $1765 level gives way, then prices may sink back towards $1747.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The economic impact so far has been greater than that of the Bali bombings of 2002, with losses of around 9.7 trillion rupiah (about £551.3 million) a month.

In the past, the island’s image as a peaceful paradise with a rich cultural and religious heritage has made it a highly resilient tourist destination. Bali recovered swiftly in the wake of past crises, both natural and man made, including the Gulf War (1990), a cholera outbreak (1995), Sars (2003) and bird flu (2007).

But without significant investment and diversification, there are widespread concerns that this crisis could be different.

A different approach may now be needed to save the tourism industry – and to make sure its benefits are more evenly spread. We believe that now is the time to adjust the model in Bali away from surf, parties, and yoga towards rural villages with high poverty rates across the island (especially the underdeveloped north-east).

To do this, government support is required to build small-scale tourism that will provide new livelihoods. This might include everything from dolphin watching and snorkelling trips, to food tourism and “experience tourism” focused on traditional fishing and farming.

That support does not necessarily need to be in the form of cash. When we interviewed small-business representatives in Bali last year, they called not for financial subsidies, but for marketing training and access to tourism-research data.

As one entrepreneur told us: “Many local creative businesses are managed as informal family businesses. They lack knowledge in professional management and marketing skills.”

He also spoke of the need for improved collaboration between IT experts, business consultants, local universities and policymakers.

Yet there are important risks to consider when attempting to build a new kind of tourism. “Authentic” experiences can often be manufactured by large businesses, preventing regional economic development (other than occasional low-paid work) in the most deprived areas.

And without investment in tourist infrastructure, it would be too easy for tourists to prefer the manufactured version over the true “authenticity” on offer from local communities. Carefully considered investment, however, could lead to sustainable development.

According to Dr Luh Putu Mahyuni, a sustainable business consultant and economist at Undiknas University: “The pandemic provides a wake up call for Bali to foster […] new types of tourism such as gastronomic tourism.”

She told a webinar we hosted in May: “The tourism sector needs to develop products with other sectors so as to create a more resilient and sustainable economy.”

To boost that economy, the island should also consider a tourist tax, while reducing taxes on small-scale home-stays, and better regulating the presence of Airbnb. It also needs to restrict foreign ownership of property, limit destruction of viable farmland and limit business sizes in the south of the island.

An island of opportunity

Notwithstanding all the devastation it has caused, COVID-19 has given the world an opportunity to pause and reflect on how things may change in its aftermath. The tourism industry in Bali (and many other places) is no exception.

For tourism is often seen as a solution to all kinds of problems, from economics to conservation. But as our research has shown, unless tourist money is kept in the local community, the benefits do not materialise.

And besides the major financial concerns on Bali, and the need for a tourism-led recovery, the authorities must also face up to deeply entrenched levels of structural inequality. Poverty, homelessness and dispossession existed long before the pandemic.

The island must learn from what happened 18 years ago, when the bombings led to job losses and increased rates of depression, alcoholism and crime. And we hope that Bali can use the current crisis as an opportunity to look at the causes of such social problems, rather than the symptoms. To move on and build a more resilient island, where responsible tourism plays a major role in alleviating poverty.

Akero Therapeutics shares traded 28% higher and established a new 52-week high after the company reported that it recorded positive histological data across all Efruxifermin dosage groups in its Phase 2a BALANCED Study in NASH patients.

Clinical-stage biotechnology company Akero Therapeutics Inc. (AKRO:NASDAQ), which develops and commercializes treatments for serious metabolic diseases, yesterday announced “results of a 16-week analysis of secondary and exploratory endpoints in its Phase 2a BALANCED study of efruxifermin (EFX), formerly known as AKR-001, in patients with nonalcoholic steatohepatitis (NASH).”

The firm highlighted that “of the 40 treatment responders who had end-of-treatment biopsies, it observed that 48% achieved at least a one-stage improvement in fibrosis without worsening of NAFLD activity score and 28% achieved at least a two-stage improvement in fibrosis.”

Stephen Harrison, M.D., medical director of Pinnacle Clinical Research, remarked, “These substantial improvements observed in multiple measures of liver health, particularly the one- and two-stage improvements in fibrosis, are extremely encouraging and among the strongest biopsy results reported in NASH to date…I believe Efruxifermin continues to set itself apart as one of the most promising drug candidates in NASH, with impressive histology results after just 16 weeks of treatment.”

Akero Therapeutics’ President and CEO Andrew Cheng, M.D., Ph.D., commented, “We believe the BALANCED study data, which exceeded our expectations, demonstrate the strong potential of efruxifermin to be a foundational monotherapy for the treatment of NASH…We look forward to the continued development of efruxifermin and are working diligently to deliver this potentially leading treatment to patients. We are extremely grateful to all of our investigators and study patients, particularly given that this study cohort was completed amidst the COVID-19 pandemic.”

The company advised that the BALANCED study is an ongoing clinical trial in NASH patients and that the firm previously reported that several EFX dose groups in the study had met the primary endpoint compared to placebo.

The Phase 2a BALANCED study enrolled a total of 80 patients and was described as “a multicenter, randomized, double-blind, placebo-controlled, dose-ranging trial in biopsy-confirmed adult patients with NASH.”

The firm explained that NASH (non-alcoholic steatohepatitis) is a serious form of NAFLD (non-alcoholic fatty liver disease) that is closely linked to obesity and diabetes epidemics observed worldwide. The company stated that NASH affects around 17 million Americans and is a leading cause of liver transplants both in the US and Europe.

The company additionally listed that Efruxifermin (EFX) is its lead product candidate for NASH and “it is designed to reduce liver fat and inflammation, reverse fibrosis, increase insulin sensitivity and improve lipoproteins.”

Akero Therapeutics is headquartered in South San Francisco, Calif., and described it business as “a cardio-metabolic NASH company dedicated to reversing the escalating NASH epidemic by developing pioneering medicines designed to restore metabolic balance to improve overall health.”

Akero Therapeutics started the trading day with a market capitalization of around $714.6 million with approximately 28.67 million shares outstanding. AKRO shares opened 40% higher today at $35.10 (+$10.18, +40.85%) over yesterday’s $24.92 closing price and reached a new 52-week high price this morning of $35.30. The stock has traded today between $31.12 and $35.30 per share and is currently trading at $32.00 (+$7.08, +28.41%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

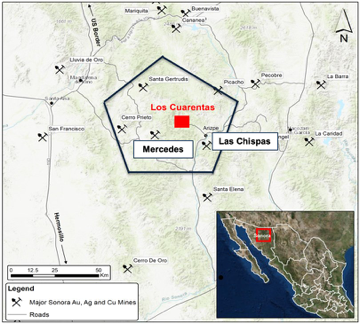

In conversation with Maurice Jackson of Proven and Probable, the president and CEO of Riverside Resources describes his company’s option agreement with Hochschild Mining and plans to move the Los Cuarentas Gold-Silver Project forward.

Maurice: Today, we’re going to highlight Riverside Resources Inc. (RRI:TSX.V; RVSDF:OTCQB), a project generator that just consummated a definitive option agreement with a two-prong earn-in agreement worth $11 million and an additional $20 million for a buyout, with a 1% net smelter return.

Dr. Staude, pleasure to speak with you today.

John-Mark: Great to be here, Maurice.

Maurice: John-Mark, you have some exciting news for shareholders regarding a definitive option agreement on the Los Cuarentas Gold-Silver Project (press release). Dr. Staude, what would you like to share with us?

John-Mark: We’re so excited. We’ve been working a long-time on the Los Cuarentas project, and to have a major partner like Hochschild Mining Plc (HOC:LSE) join us in conducting the exploration is wonderful. The option is for them to earn a 51% interest by investing over US$8 million into the ground, with us as the operator. For us, this is the perfect example of prospect generation. We generate projects, progress them, and now have the major command with an aggressive drill program, aggressive exploration to unlock the value for us and our partners. We’re in a great position. We’re very excited today about this news.

Maurice: There’s some history between Hochschild and Riverside Resources. How did that factor into the consummation on the option agreement on the Los Cuarentas?

John-Mark: We’re so lucky. We worked with them in the past. We had a strategic exploration alliance where we generated projects, forwarded those, and built out a portfolio working with Hochschild. We also really enjoyed working with them. In these difficult times, when things went down, they stuck with us and we stuck with them.

So now, here we are in COVID, yet again in challenging times, and we’re delighted to know we’re going with a partner that we worked within the past. We have good alignment in values, vision and particularly in a goal to make discoveries working with Hochschild and Riverside. So. . .now we get to go forward with a big drill program. We’re in a great position.

Maurice: Speaking of the drill program, can you define the roles of Riverside and Hochschild’s respectively? And when will it begin?

John-Mark: It’s starting right away. Right now, we’re working on the budget. We went out to the site earlier in January, and it’s so lucky we did, because in March, as we know, things changed so much.

But by going out to site, we began to layout the program. And so now we’re able to go out in the field; we have a team in Hermosillo, Mexico. We live and work there. We can work from that location and then up at the project site to carry out the exploration over the next months and be ready to drill. During this year, we’ll have drill results and go for a drill discovery. We’ll be pushing hard first, with geophysics and then with drilling. So we’re in a great position now.

Maurice: John-Mark, why does Riverside like this epithermal gold-silver district so much?

John-Mark: Mexico has been a world leader for five centuries with epithermal. These are shallow systems where hot water brings gold and silver and deposits it with silica near the surface. The reason we like it is, first, it’s rich. Second, it’s often fairly easy to mine. Third, it’s company makers. Many companies have been built out of this style of deposit, Hochschild, who’ve made their careers mining epithermal.

And right next to us, just to the east of us, is SilverCrest Metals Inc. (SIL:TSX.V; SILV:NYSE.American), with their mining operations and exploration that they’re doing with the Los Chispas mine. And to the west of us is the Mercedes mining district. . .where we see Premier Gold Mines Ltd. (PG:TSX) developing and mining. To the north of us, we have Santa Gertrudis mine with Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE), and to the south of us, we have First Majestic Silver Corp. (FR:TSX; AG:NYSE; FMV:FSE) and the Santa Elena mine.

And all of those are within this world of epithermal, shallow mineralizationyoung, gold, very positive. So we’re so excited to be right in the middle with this project. And these are the type of deposits we want to be a part of making in the discovery through exploration.

Maurice: Location, location, location. John-Mark, walk us through the transaction details, beginning with phase one of the earn-in option agreement.

John-Mark: In phase one, there’s US$750,000 exploration funding in the first year. It’s a four-year option. In the first phase. . .Hochschild will be spending $8 million in work [with] Riverside as the operator. Also, Hochschild is covering any of the lingering, underlying costs to buy out the underlying owners, and to pay for any of their taxes and other things like that. So for us, we’ve generated this in this phase one. We’ve got to test these targets that we’ve already come up with, and explore the property-wide program. It’s a great situation for all parties.

Maurice: How about phase two?

John-Mark: Phase two is really exciting as well. Hochschild gets to go to 75% by doing another $3 million of work and completing a study, and of course, paying us, as well some more fees.

So it’s a really good situation, and that’s the type of deal we like to do where it gives them the upside, but it also gives us a chance where, if they carry it forward further, or it doesn’t dilute us, or if we make a joint venture, we’re able to be a large holder in it. So phase two is a great step, as well, for both companies.

Maurice: John-Mark, this is another great demonstration of the business acumen and on behalf of all the shareholders, as I am one myself, thank you. This is great.

All right, switching gears, John-Mark, please share the current share price and the capital structure for Riverside Resources.

John-Mark: Riverside right now is trading in about CA$0.20, and on the U.S. side is about $0.14 cents. Our share structure: 63 million shares. We’re in a good position with over $2 million cash in the bank and no debt. Riverside’s poised for doing well for the remainder of 2020 and onward.

Maurice: In closing, what did I forget to ask?

John-Mark: I think what took us so long to get this deal done was because of COVID. We wanted to get this done, but we had to wait a while to make sure we had it all aligned. We’ve all been very respectful, so delighted to work with Hochschild, and now we’re ready to go ahead.

We had a bit of a hiatus during COVID, but we’re set to go. We’ve gotten through that. Now, we’re ready to go in the field. So I think that’s our excitement now, is getting going with results.

Maurice: Dr. Staude, for someone listening that wants to get more information on Riverside Resources, please share the contact details.

Maurice: Dr. Staude, thank you for joining us today on Proven and Probable.

Riverside Resources trades on the TSX.V: RRI | OTCQB: RVSDF. Before you make your next bullion purchase, make sure you call me. I’m a licensed representative for Miles Franklin Precious Metals Investments. We have several options to expand your precious metals portfolio from physical delivery, offshore depositories and precious metal IRAs. Call me at (855) 505-1900, or you may e-mail [email protected].

Finally, please subscribe to Proven and Probable for mining insights and bullion sales. Subscription is free.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Riverside Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Riverside Resources is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Riverside Resources, a company mentioned in this article.

Disclosures for Proven and Probable: Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Axsome Therapeutics’ latest news and clinical outlook are discussed in an H.C. Wainwright & Co. report.

In a June 30 research note, H.C. Wainwright & Co. analyst Ram Selvaraju reported that the U.S. Food and Drug Administration (FDA) designated Axsome Therapeutics Inc.’s (AXSM:NASDAQ) AXS-05, an NMDA receptor antagonist, a breakthrough therapy for Alzheimer’s disease agitation.

AXS-05 received the same status previously in another indication, major depressive disorder. The designation, in part, means a drug will get priority review, in 6 versus 10 months.

Selvaraju explained that breakthrough designation is “granted to expedite development and review timelines for a promising investigational medicine when preliminary clinical evidence indicates that it may show substantial improvement on one or more clinically significant endpoints over available therapies for a serious or life-threatening condition.”

The analyst indicated that positive data from Axsome’s recent pivotal Phase 2/3 ADVANCE-1 study support the breakthrough designation of AXS-05 for Alzheimer’s disease agitation. In the trial, patients treated with AXS-05 experienced “rapid, substantial, and statistically significant improvement in agitation.” Adverse events, from most to least common, were somnolence, dizziness and diarrhea.

Selvaraju highlighted that H2/20 should be a catalyst-rich period for U.S.-based Axsome, with completion of its regulatory filings for AXS-05 in major depressive disorder and for AXS-07 in migraine, with potential FDA approvals to follow by year-end 2021.

Also next year, clinical data are expected in the way of pivotal AXS-05 results in treatment-resistant depression and possibly Alzheimer’s disease-associated agitation along with Phase 3 AXS-12 findings in narcolepsy.

Selvaraju concluded that Axsome is “still undervalued” and “by 2022 Axsome could have four drugs on the market in the U.S., spanning a total of at least six indications. . .We feel that added clarity from regulators in the wake of multiple FDA meetings that Axsome is likely to have in the course of the coming months should provide significant risk mitigation and substantially increase investor confidence in the company’s clinical development and regulatory approach.”

H.C. Wainwright has a Buy rating and a $210 per share target price on Axsome; the current stock price is $85.02 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from H.C. Wainwright & Co., Axsome Therapeutics Inc., Company Update, June 30, 2020

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placement of securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a company or one of its affiliates or subsidiaries within the past 12 months.

I, Raghuram Selvaraju, Ph.D., certify that 1) all of the views expressed in this report accurately reflect my personal views about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor any members of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analyst’s household has a financial interest in the securities of Axsome Therapeutics, Inc. (including, without limitation, any option, right, warrant, future, long or short position).

As of May 31, 2020 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securities of Axsome Therapeutics, Inc.

Neither the research analyst nor the Firm has any material conflict of interest in of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon any specific investment banking services or transaction but is compensated based on factors including total revenue and profitability of the Firm, a substantial portion of which is derived from investment banking services.

The firm or its affiliates received compensation from Axsome Therapeutics, Inc. for non-investment banking services in the previous 12 months.

The firm or its affiliates did receive compensation from Axsome Therapeutics, Inc. for investment banking services within twelve months before, and will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

H.C. Wainwright & Co., LLC managed or co-managed a public offering of securities for Axsome Therapeutics, Inc. during the past 12 months.

The Firm does not make a market in Axsome Therapeutics, Inc. as of the date of this research report.